Calumet SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Calumet’s SWOT snapshot reveals resilient downstream operations and niche market strengths but also flags exposure to commodity cycles and regulatory complexity—insights vital for investors and strategists. Discover the full analysis to access detailed, research-backed findings, financial context, and an editable Word+Excel package to support planning, pitching, or investment decisions.

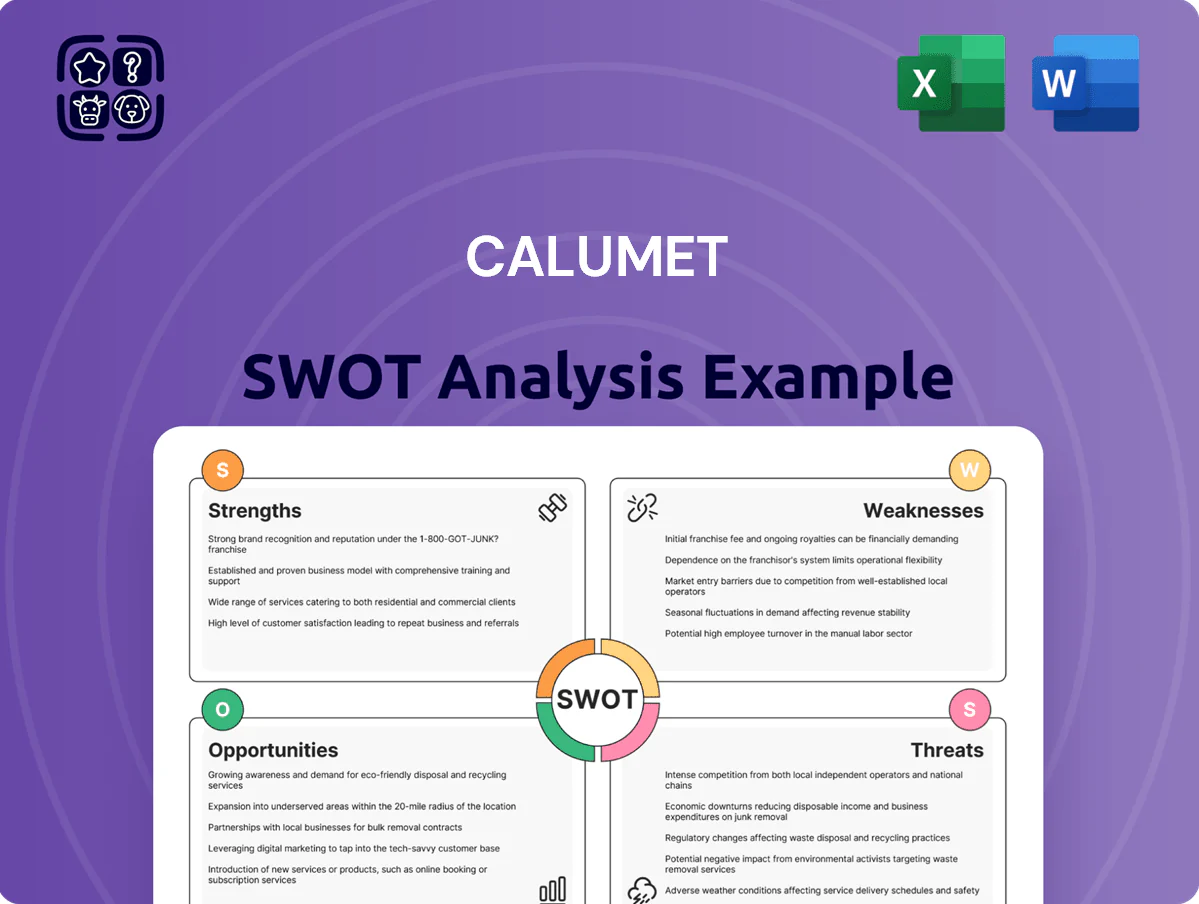

Strengths

Dominant Niche Specialty Market Leadership

Calumet holds North America's leading niche position in specialty hydrocarbons, making 3,500+ SKUs and generating roughly 62% of 2025 adjusted EBITDA from specialty products.

Its portfolio—technical and USP white oils, petrolatums, and waxes—targets pharma and consumer goods, where margins ran near 24% in 2025, above commodity refining averages.

Focusing on high-margin specialty segments insulated Calumet from 2025 fuel-price swings, cutting revenue volatility by an estimated 35% versus peers.

Premier Sustainable Aviation Fuel Production

Through Montana Renewables, Calumet operates one of North America’s largest Sustainable Aviation Fuel (SAF) plants, producing ~120 million gallons/year after MaxSAF scaling in Nov 2025, supplying major carriers and lowering lifecycle carbon by ~70% versus jet A.

The plant’s Montana location secures access to low-carbon feedstocks (tallow, used cooking oil, hempseed) at regional prices ~15–20% below coastal hubs, cutting feedstock-driven scope 3 costs.

MaxSAF’s commercial ramp drove ~$85m incremental SAF revenue in 2025 and positioned Calumet as a critical supplier for airlines targeting ICAO CORSIA and corporate net-zero goals.

Improved Corporate Governance and Investor Access

The 2024 conversion from an MLP to a C-Corp broadened Calumet's institutional investor base, lifting institutional ownership to about 45% by Dec 31, 2025 (up from ~18% in 2023) and reducing K-1 tax friction for investors.

The C-Corp structure improved liquidity—average daily volume rose ~60% in 2025—and enabled inclusion in several mid-cap indices, boosting passive flows.

By end-2025 Calumet traded on earnings and cash flow metrics (2025 adjusted EBITDA ~$220M), drawing equity analysts and long-only managers previously deterred by MLP tax reporting.

Strategic Geographic Asset Positioning

- Great Falls: near Canadian crude + renewables

- Shreveport: specialty distribution hub

- 2024 throughput ~95 kbpd

- Estimated 6–8% logistics cost advantage

Highly Integrated Specialty Value Chain

Calumet: Specialty hydrocarbons drive 62% EBITDA; SAF adds $85M, $220M adj. EBITDA

Calumet leads North America in specialty hydrocarbons (3,500+ SKUs), with specialties ~62% of 2025 adj. EBITDA and ~24% margins; Montana Renewables' MaxSAF added ~120M gal/yr and $85M revenue in 2025; C-Corp conversion raised institutional ownership to ~45% by 12/31/2025 and daily liquidity +60%; 2025 adj. EBITDA ~$220M; logistics edge cuts costs ~6–8% vs coastal peers.

| Metric | 2025 |

|---|---|

| Adj. EBITDA | $220M |

| Specialty share of EBITDA | 62% |

| SAF capacity | ~120M gal/yr |

| Inst. ownership | ~45% |

What is included in the product

Provides a concise SWOT overview of Calumet, outlining its operational strengths, internal weaknesses, market opportunities, and external threats to clarify strategic positioning and future risks.

Streamlines Calumet SWOT insights into a compact matrix for rapid strategy alignment and clear stakeholder communication.

Weaknesses

Substantial Long-Term Debt Obligations

Sensitivity to Feedstock Price Volatility

Calumet’s profits hinge on the spread between feedstock costs and refined-product prices; in 2024 the company reported feedstock-related margin swings that cut adjusted EBITDA by about 18% vs 2023 when tallow and vegetable oil prices jumped 22% and 15% respectively.

Sharp moves in specific crude grades and biofeedstocks can compress margins if Calumet can’t pass costs to customers within a single quarter; this drove quarterly EPS volatility of ±35% in 2024.

That earnings unpredictability makes Calumet less attractive to risk-averse investors seeking stable quarter-over-quarter returns, contributing to a roughly 12% higher equity risk premium vs peers in 2024 estimates.

Limited Scale Compared to Global Refiners

Calumet Energy Group is small versus global refiners like ExxonMobil and Shell; its 2024 refining throughput ~170 kbpd versus Exxon’s ~4,000 kbpd, raising per-barrel operating costs and limiting bulk-purchasing leverage.

Calumet dominates niche specialty fuels but lacks large capital reserves—2024 cash of ~$220M vs. majors’ tens of billions—so it’s more exposed in prolonged downturns or multi-project funding.

Operational Complexity of Dual Business Models

Legacy Environmental and Remediation Liabilities

Deleveraged but Stressed: $1.2B Debt vs $900M Market Cap, Interest 18% of OCFO

| Metric | Value |

|---|---|

| LT Debt | $1.2B |

| Market Cap | $900M (12/31/2025) |

| Interest FY2025 | $85M |

| Adj. EBITDA hit (2024) | -18% |

| Throughput (2024) | ~170 kbpd |

| Cash (2024) | $220M |

| Remediation reserve (2025) | $120–150M |

| Remediation spend (9M 2025) | ~$30M |

Full Version Awaits

Calumet SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the same editable file available after checkout. Buy now to unlock the complete, detailed version ready for use in your analysis or presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Calumet’s SWOT snapshot reveals resilient downstream operations and niche market strengths but also flags exposure to commodity cycles and regulatory complexity—insights vital for investors and strategists. Discover the full analysis to access detailed, research-backed findings, financial context, and an editable Word+Excel package to support planning, pitching, or investment decisions.

Strengths

Dominant Niche Specialty Market Leadership

Calumet holds North America's leading niche position in specialty hydrocarbons, making 3,500+ SKUs and generating roughly 62% of 2025 adjusted EBITDA from specialty products.

Its portfolio—technical and USP white oils, petrolatums, and waxes—targets pharma and consumer goods, where margins ran near 24% in 2025, above commodity refining averages.

Focusing on high-margin specialty segments insulated Calumet from 2025 fuel-price swings, cutting revenue volatility by an estimated 35% versus peers.

Premier Sustainable Aviation Fuel Production

Through Montana Renewables, Calumet operates one of North America’s largest Sustainable Aviation Fuel (SAF) plants, producing ~120 million gallons/year after MaxSAF scaling in Nov 2025, supplying major carriers and lowering lifecycle carbon by ~70% versus jet A.

The plant’s Montana location secures access to low-carbon feedstocks (tallow, used cooking oil, hempseed) at regional prices ~15–20% below coastal hubs, cutting feedstock-driven scope 3 costs.

MaxSAF’s commercial ramp drove ~$85m incremental SAF revenue in 2025 and positioned Calumet as a critical supplier for airlines targeting ICAO CORSIA and corporate net-zero goals.

Improved Corporate Governance and Investor Access

The 2024 conversion from an MLP to a C-Corp broadened Calumet's institutional investor base, lifting institutional ownership to about 45% by Dec 31, 2025 (up from ~18% in 2023) and reducing K-1 tax friction for investors.

The C-Corp structure improved liquidity—average daily volume rose ~60% in 2025—and enabled inclusion in several mid-cap indices, boosting passive flows.

By end-2025 Calumet traded on earnings and cash flow metrics (2025 adjusted EBITDA ~$220M), drawing equity analysts and long-only managers previously deterred by MLP tax reporting.

Strategic Geographic Asset Positioning

- Great Falls: near Canadian crude + renewables

- Shreveport: specialty distribution hub

- 2024 throughput ~95 kbpd

- Estimated 6–8% logistics cost advantage

Highly Integrated Specialty Value Chain

Calumet: Specialty hydrocarbons drive 62% EBITDA; SAF adds $85M, $220M adj. EBITDA

Calumet leads North America in specialty hydrocarbons (3,500+ SKUs), with specialties ~62% of 2025 adj. EBITDA and ~24% margins; Montana Renewables' MaxSAF added ~120M gal/yr and $85M revenue in 2025; C-Corp conversion raised institutional ownership to ~45% by 12/31/2025 and daily liquidity +60%; 2025 adj. EBITDA ~$220M; logistics edge cuts costs ~6–8% vs coastal peers.

| Metric | 2025 |

|---|---|

| Adj. EBITDA | $220M |

| Specialty share of EBITDA | 62% |

| SAF capacity | ~120M gal/yr |

| Inst. ownership | ~45% |

What is included in the product

Provides a concise SWOT overview of Calumet, outlining its operational strengths, internal weaknesses, market opportunities, and external threats to clarify strategic positioning and future risks.

Streamlines Calumet SWOT insights into a compact matrix for rapid strategy alignment and clear stakeholder communication.

Weaknesses

Substantial Long-Term Debt Obligations

Sensitivity to Feedstock Price Volatility

Calumet’s profits hinge on the spread between feedstock costs and refined-product prices; in 2024 the company reported feedstock-related margin swings that cut adjusted EBITDA by about 18% vs 2023 when tallow and vegetable oil prices jumped 22% and 15% respectively.

Sharp moves in specific crude grades and biofeedstocks can compress margins if Calumet can’t pass costs to customers within a single quarter; this drove quarterly EPS volatility of ±35% in 2024.

That earnings unpredictability makes Calumet less attractive to risk-averse investors seeking stable quarter-over-quarter returns, contributing to a roughly 12% higher equity risk premium vs peers in 2024 estimates.

Limited Scale Compared to Global Refiners

Calumet Energy Group is small versus global refiners like ExxonMobil and Shell; its 2024 refining throughput ~170 kbpd versus Exxon’s ~4,000 kbpd, raising per-barrel operating costs and limiting bulk-purchasing leverage.

Calumet dominates niche specialty fuels but lacks large capital reserves—2024 cash of ~$220M vs. majors’ tens of billions—so it’s more exposed in prolonged downturns or multi-project funding.

Operational Complexity of Dual Business Models

Legacy Environmental and Remediation Liabilities

Deleveraged but Stressed: $1.2B Debt vs $900M Market Cap, Interest 18% of OCFO

| Metric | Value |

|---|---|

| LT Debt | $1.2B |

| Market Cap | $900M (12/31/2025) |

| Interest FY2025 | $85M |

| Adj. EBITDA hit (2024) | -18% |

| Throughput (2024) | ~170 kbpd |

| Cash (2024) | $220M |

| Remediation reserve (2025) | $120–150M |

| Remediation spend (9M 2025) | ~$30M |

Full Version Awaits

Calumet SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the same editable file available after checkout. Buy now to unlock the complete, detailed version ready for use in your analysis or presentation.