Cameco Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Cameco faces moderate supplier power and regulatory scrutiny, strong buyer concentration from utilities, limited substitutes but cyclical demand, and high competitive rivalry amid global uranium producers; this snapshot highlights where strategic risks and advantages lie.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Cameco to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized Mining Equipment and Technology

The procurement of high-tech mining machinery and specialized nuclear processing tech comes from a handful of global vendors, giving suppliers moderate bargaining power since those assets are critical to Cameco’s Tier-1 production and safety; about 60–70% of capital spares for mills trace to three major OEMs as of 2025. Still, Cameco’s 2024 revenue of CAD 1.6B and 30+ year industry footprint let it secure favorable long-term service and maintenance contracts, lowering supplier leverage.

Highly Skilled Nuclear Labor Force

The nuclear sector’s need for certified technicians and security-cleared staff gives suppliers of skilled labor strong bargaining power; Canada had a 2024 shortfall of about 2,400 skilled nuclear workers per the Canadian Nuclear Association, pushing wages up ~6–8% in 2023–24. Unions and specialist groups can raise operating costs via wage and safety demands, so Cameco reduces risk by funding internal training (established apprenticeship pipelines since 2019) and long-term contracts to keep turnover below industry average (~5% vs 9%).

Regulatory and Environmental Compliance Services

Government agencies and environmental consultants act as indirect suppliers for Cameco, setting non-negotiable rules that shape uranium mine design, permitting, and closure; in Canada, federal and provincial approvals can add 18–36 months to project timelines and raise upfront compliance costs by an estimated CAD 50–150 million for mid-sized projects (2024 industry averages).

Energy and Consumable Inputs

Mining and refining are energy-intensive: Cameco reported 2024 fuel and electricity costs represented about 8–10% of operating expenses at its key Saskatchewan operations, making prices for electricity, diesel and sulfuric acid critical to margins.

These inputs are commodities with local volatility—2022–24 regional power price spikes and a 15–25% rise in reagent costs in 2023 showed disruption risk—so Cameco uses long-term supply contracts and hedges to reduce supplier leverage.

- Energy ≈8–10% of OPEX (2024)

- Reagent costs +15–25% (2023 spike)

- Long-term contracts + hedging mitigate supplier power

Logistics and Specialized Transportation

Cameco faces supplier power in logistics because transporting radioactive uranium fuel needs rare, certified carriers; only a handful of firms handle international nuclear shipments, giving them pricing leverage.

Cameco’s vertical integration and partnerships—plus 2024 transport contracts covering ~60% of its outbound volumes—mitigate but do not remove this cost pressure.

Supplier leverage rises: OEM concentration, labor gap and cost shocks squeeze margins

Suppliers hold moderate-to-strong power: critical OEMs supply 60–70% of capital spares (2025), certified labor shortfall ~2,400 workers (CNA, 2024) pushed wages +6–8% (2023–24), energy = 8–10% of OPEX (Cameco 2024), reagent costs spiked +15–25% (2023); long-term contracts/hedges and vertical integration cover ~60% transport volumes (2024) but don’t eliminate pricing risk.

| Metric | Value |

|---|---|

| Capital spares concentration (to 3 OEMs) | 60–70% (2025) |

| Skilled worker shortfall | ~2,400 (2024) |

| Wage inflation | +6–8% (2023–24) |

| Energy share of OPEX | 8–10% (2024) |

| Reagent cost spike | +15–25% (2023) |

| Outbound volumes under contract | ~60% (2024) |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and entry risks specific to Cameco, highlighting disruptive forces, pricing leverage, and strategic levers that protect its market position.

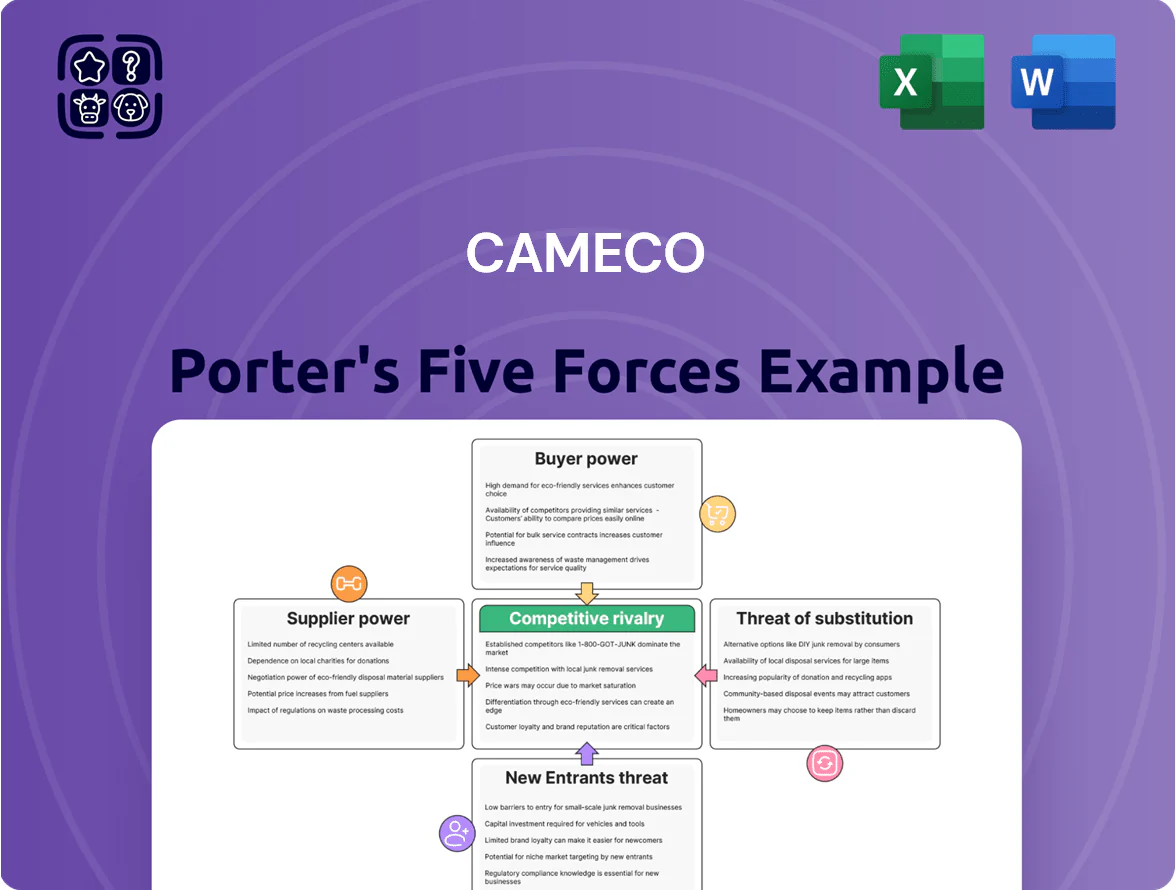

A concise, one-sheet Porter's Five Forces for Cameco that clarifies uranium market pressures and strategic levers—ideal for rapid boardroom decisions or investor notes.

Customers Bargaining Power

Concentration of Nuclear Utilities

The global uranium customer base is dominated by a few large nuclear utilities—Top 10 utilities account for roughly 55% of reactor demand—giving buyers concentrated leverage in contract talks. These utilities often buy in bulk (annual purchases per utility can exceed 3–10 Mlb U3O8 equivalent), pressuring suppliers on price and delivery terms. By late 2025, consolidation in markets like China, Europe, and the US centralized buying among fewer decision-makers, raising Cameco’s negotiation risk.

Long-term Contractual Structures

Most of Cameco’s revenue—about 70% in 2024—comes from long-term contracts that stabilize prices for both the producer and utilities, shielding the company from spot uranium volatility; here’s the quick math: 2024 sales C$2.4bn, ~C$1.68bn tied to LT deals. These contracts limit Cameco’s exposure but also lock in terms that are hard to renegotiate if market prices rise. Customers leverage these commitments to demand high reliability and security of supply, often with penalty clauses and delivery guarantees.

Utility Inventory Management

Nuclear utilities keep strategic uranium stockpiles, letting them defer purchases when prices spike; buyers used this to time entries and cap spot-market exposure. By end-2025, global civil uranium inventories fell ~18% from 2020 levels to roughly 1.6 million tU (tetravalent uranium equivalent), slightly reducing that waiting power as utilities now face tighter refill needs.

Availability of Alternative Suppliers

Buyers can source uranium from Kazatomprom or the spot market, so Cameco must stay price-competitive and stress its role as a reliable Western supplier; Kazatomprom produced ~22,000 tU in 2024 vs Cameco ~13,000 tU, keeping downward price pressure.

The push for energy security after 2022 lifted demand for Western partners, reducing some switching to lower-cost state firms and supporting Cameco’s long-term contract premiums.

- Kazatomprom ~22,000 tU (2024)

- Cameco ~13,000 tU (2024)

- Spot/contract mix shifts buyer leverage

- Energy security raises Western-supplier premium

Sensitivity to Nuclear Operating Costs

While uranium is a small share of nuclear operating costs (roughly 5–10% in 2024), utilities face price pressure from cheaper renewables and gas, so a sharp uranium price rise prompts customer pushback on fuel costs and demand for more efficient fabrication.

That pressure ripples to suppliers: Cameco must price to protect utilities’ long-term viability—2024 spot uranium volatility (price range US$50–70/lb) raised contract negotiation leverage for buyers.

- Uranium ≈5–10% of plant OPEX (2024)

- Spot price 2024 range US$50–70/lb

- Utilities can demand better fabrication or push contract timing

- Cameco needs customer-aligned pricing to sustain long-term demand

Concentrated buyers boost bargaining power as inventories tighten and producers diverge

Buyers are concentrated—Top 10 utilities ≈55% reactor demand—and buy large volumes (3–10 Mlb U3O8 each), giving strong negotiation leverage versus Cameco; long-term contracts provided ~70% of Cameco’s 2024 revenue (C$2.4bn sales, ~C$1.68bn LT), reducing spot exposure but limiting upside when prices rise. Global inventories fell ~18% from 2020 to ~1.6M tU by end-2025, tightening supply; Kazatomprom 22,000 tU vs Cameco 13,000 tU (2024).

| Metric | 2024/2025 |

|---|---|

| Top-10 utility share | ≈55% |

| Cameco revenue from LT contracts | ≈70% of C$2.4bn |

| Global civil inventories | ~1.6M tU (−18% vs 2020) |

| Production (2024) | Kazatomprom 22,000 tU; Cameco 13,000 tU |

What You See Is What You Get

Cameco Porter's Five Forces Analysis

This preview shows the exact Cameco Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use. The file displayed is the finished document, containing the same strategic insights, force-by-force evaluation, and concise conclusions included in the downloadable deliverable. Purchase grants instant access to this identical report for your decision-making needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Cameco faces moderate supplier power and regulatory scrutiny, strong buyer concentration from utilities, limited substitutes but cyclical demand, and high competitive rivalry amid global uranium producers; this snapshot highlights where strategic risks and advantages lie.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Cameco to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized Mining Equipment and Technology

The procurement of high-tech mining machinery and specialized nuclear processing tech comes from a handful of global vendors, giving suppliers moderate bargaining power since those assets are critical to Cameco’s Tier-1 production and safety; about 60–70% of capital spares for mills trace to three major OEMs as of 2025. Still, Cameco’s 2024 revenue of CAD 1.6B and 30+ year industry footprint let it secure favorable long-term service and maintenance contracts, lowering supplier leverage.

Highly Skilled Nuclear Labor Force

The nuclear sector’s need for certified technicians and security-cleared staff gives suppliers of skilled labor strong bargaining power; Canada had a 2024 shortfall of about 2,400 skilled nuclear workers per the Canadian Nuclear Association, pushing wages up ~6–8% in 2023–24. Unions and specialist groups can raise operating costs via wage and safety demands, so Cameco reduces risk by funding internal training (established apprenticeship pipelines since 2019) and long-term contracts to keep turnover below industry average (~5% vs 9%).

Regulatory and Environmental Compliance Services

Government agencies and environmental consultants act as indirect suppliers for Cameco, setting non-negotiable rules that shape uranium mine design, permitting, and closure; in Canada, federal and provincial approvals can add 18–36 months to project timelines and raise upfront compliance costs by an estimated CAD 50–150 million for mid-sized projects (2024 industry averages).

Energy and Consumable Inputs

Mining and refining are energy-intensive: Cameco reported 2024 fuel and electricity costs represented about 8–10% of operating expenses at its key Saskatchewan operations, making prices for electricity, diesel and sulfuric acid critical to margins.

These inputs are commodities with local volatility—2022–24 regional power price spikes and a 15–25% rise in reagent costs in 2023 showed disruption risk—so Cameco uses long-term supply contracts and hedges to reduce supplier leverage.

- Energy ≈8–10% of OPEX (2024)

- Reagent costs +15–25% (2023 spike)

- Long-term contracts + hedging mitigate supplier power

Logistics and Specialized Transportation

Cameco faces supplier power in logistics because transporting radioactive uranium fuel needs rare, certified carriers; only a handful of firms handle international nuclear shipments, giving them pricing leverage.

Cameco’s vertical integration and partnerships—plus 2024 transport contracts covering ~60% of its outbound volumes—mitigate but do not remove this cost pressure.

Supplier leverage rises: OEM concentration, labor gap and cost shocks squeeze margins

Suppliers hold moderate-to-strong power: critical OEMs supply 60–70% of capital spares (2025), certified labor shortfall ~2,400 workers (CNA, 2024) pushed wages +6–8% (2023–24), energy = 8–10% of OPEX (Cameco 2024), reagent costs spiked +15–25% (2023); long-term contracts/hedges and vertical integration cover ~60% transport volumes (2024) but don’t eliminate pricing risk.

| Metric | Value |

|---|---|

| Capital spares concentration (to 3 OEMs) | 60–70% (2025) |

| Skilled worker shortfall | ~2,400 (2024) |

| Wage inflation | +6–8% (2023–24) |

| Energy share of OPEX | 8–10% (2024) |

| Reagent cost spike | +15–25% (2023) |

| Outbound volumes under contract | ~60% (2024) |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and entry risks specific to Cameco, highlighting disruptive forces, pricing leverage, and strategic levers that protect its market position.

A concise, one-sheet Porter's Five Forces for Cameco that clarifies uranium market pressures and strategic levers—ideal for rapid boardroom decisions or investor notes.

Customers Bargaining Power

Concentration of Nuclear Utilities

The global uranium customer base is dominated by a few large nuclear utilities—Top 10 utilities account for roughly 55% of reactor demand—giving buyers concentrated leverage in contract talks. These utilities often buy in bulk (annual purchases per utility can exceed 3–10 Mlb U3O8 equivalent), pressuring suppliers on price and delivery terms. By late 2025, consolidation in markets like China, Europe, and the US centralized buying among fewer decision-makers, raising Cameco’s negotiation risk.

Long-term Contractual Structures

Most of Cameco’s revenue—about 70% in 2024—comes from long-term contracts that stabilize prices for both the producer and utilities, shielding the company from spot uranium volatility; here’s the quick math: 2024 sales C$2.4bn, ~C$1.68bn tied to LT deals. These contracts limit Cameco’s exposure but also lock in terms that are hard to renegotiate if market prices rise. Customers leverage these commitments to demand high reliability and security of supply, often with penalty clauses and delivery guarantees.

Utility Inventory Management

Nuclear utilities keep strategic uranium stockpiles, letting them defer purchases when prices spike; buyers used this to time entries and cap spot-market exposure. By end-2025, global civil uranium inventories fell ~18% from 2020 levels to roughly 1.6 million tU (tetravalent uranium equivalent), slightly reducing that waiting power as utilities now face tighter refill needs.

Availability of Alternative Suppliers

Buyers can source uranium from Kazatomprom or the spot market, so Cameco must stay price-competitive and stress its role as a reliable Western supplier; Kazatomprom produced ~22,000 tU in 2024 vs Cameco ~13,000 tU, keeping downward price pressure.

The push for energy security after 2022 lifted demand for Western partners, reducing some switching to lower-cost state firms and supporting Cameco’s long-term contract premiums.

- Kazatomprom ~22,000 tU (2024)

- Cameco ~13,000 tU (2024)

- Spot/contract mix shifts buyer leverage

- Energy security raises Western-supplier premium

Sensitivity to Nuclear Operating Costs

While uranium is a small share of nuclear operating costs (roughly 5–10% in 2024), utilities face price pressure from cheaper renewables and gas, so a sharp uranium price rise prompts customer pushback on fuel costs and demand for more efficient fabrication.

That pressure ripples to suppliers: Cameco must price to protect utilities’ long-term viability—2024 spot uranium volatility (price range US$50–70/lb) raised contract negotiation leverage for buyers.

- Uranium ≈5–10% of plant OPEX (2024)

- Spot price 2024 range US$50–70/lb

- Utilities can demand better fabrication or push contract timing

- Cameco needs customer-aligned pricing to sustain long-term demand

Concentrated buyers boost bargaining power as inventories tighten and producers diverge

Buyers are concentrated—Top 10 utilities ≈55% reactor demand—and buy large volumes (3–10 Mlb U3O8 each), giving strong negotiation leverage versus Cameco; long-term contracts provided ~70% of Cameco’s 2024 revenue (C$2.4bn sales, ~C$1.68bn LT), reducing spot exposure but limiting upside when prices rise. Global inventories fell ~18% from 2020 to ~1.6M tU by end-2025, tightening supply; Kazatomprom 22,000 tU vs Cameco 13,000 tU (2024).

| Metric | 2024/2025 |

|---|---|

| Top-10 utility share | ≈55% |

| Cameco revenue from LT contracts | ≈70% of C$2.4bn |

| Global civil inventories | ~1.6M tU (−18% vs 2020) |

| Production (2024) | Kazatomprom 22,000 tU; Cameco 13,000 tU |

What You See Is What You Get

Cameco Porter's Five Forces Analysis

This preview shows the exact Cameco Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use. The file displayed is the finished document, containing the same strategic insights, force-by-force evaluation, and concise conclusions included in the downloadable deliverable. Purchase grants instant access to this identical report for your decision-making needs.