Camellia Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

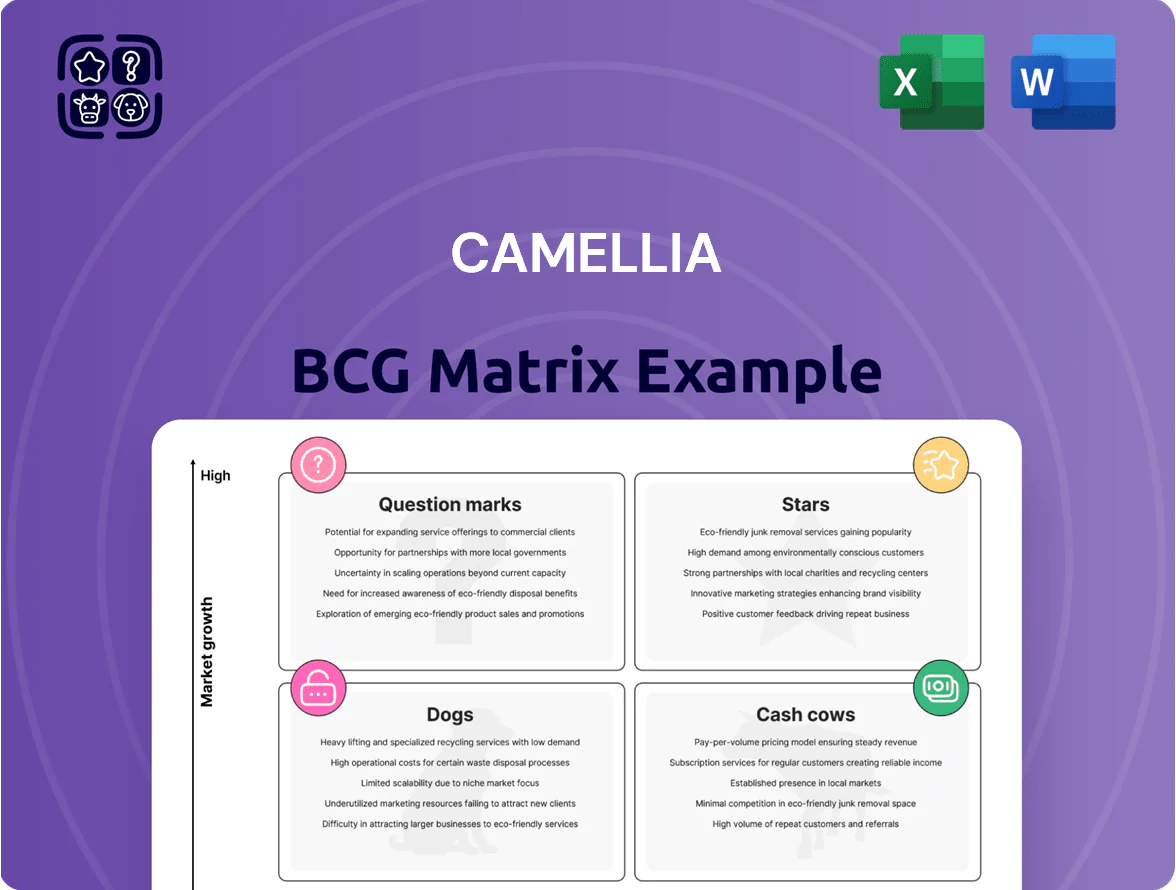

The Camellia BCG Matrix snapshot highlights how its product lines map across growth and market share—revealing potential Stars driving future growth, Cash Cows funding operations, Question Marks needing investment decisions, and Dogs that may warrant divestment. This concise view helps prioritize portfolio moves and spot strategic risks in a changing market. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word and Excel reports to turn insights into action.

Stars

Avocado Production

Avocado Production is a Star for Camellia: its 51% stake in Kenyan-listed Kakuzi and expanding Tanzanian operations give it leadership in a fast-growing market; global avocado demand rose ~6–8% annually to 2025, driven by Europe and Asia. Camellia raised its Tanzanian avocado area to 448 ha in 2025, targeting 650 ha, and is investing heavily in irrigation and orchard maturation. High growth sustains strong market share but keeps cash burn elevated due to capex and multi-year crop gestation.

Macadamia Nuts

Macadamia nuts are a Star for Camellia: high-growth segment with prices up 77% in early 2025, boosting EBITDA margins as unit realization rose from $4.10/kg in 2023 to ~$7.27/kg in Q1 2025.

Large-scale orchards in Malawi and South Africa are maturing—tree yields climbing ~18% YoY—raising Camellia’s exportable volumes by ~22% in 2025.

Australia’s 2025 shortfall tightened global supply, letting Camellia gain share and command premiums ~15–25% above world averages.

Ongoing CAPEX in processing and precision irrigation (~$12m committed through 2026) is needed to protect margins and fend off rivals.

Specialty and Branded Tea

While the global tea market is broadly mature, Camellia’s specialty and branded tea units—notably Darjeeling estates and Jing Tea—act as Stars, targeting premium/luxury segments that grew ~6–8% CAGR vs 1–2% for commodity tea (2021–25); Jing Tea posted a 13% revenue rise in mid-2025. The company uses tea tourism and high-margin retail to differentiate from bulk production, but sustaining estate prestige needs ongoing promotion and strict quality control.

Brazilian Arable Crops

The Brazilian arable crops unit is a Star: 2025 soy and maize output rose 12% to 1.8 million tonnes, driven by awards for operational excellence and a program to irrigate 60% of land, boosting yields by ~15%.

Brazil’s role as a top-3 global exporter gives Camellia high market share amid continued volume growth; mechanization and water-resilience capex of $48m in 2025 shows reinvestment to secure dominance.

- 2025 production 1.8M t (+12%)

- Irrigation coverage 60% (project)

- Yield uplift ~15%

- 2025 capex $48m

- High market share in top-3 exporting country

Precision Engineering Services

AJT Engineering, Camellia’s UK precision-services arm, is a high-growth star: revenues rose 22% in 2025 with improved margins, driven by specialist work for energy and industrial clients amid a green-infrastructure shift.

Camellia’s 2025 capex on horizontal borers and precision kit targets niche share gains; AJT now acts as a non-agricultural growth engine smoothing crop-cycle volatility.

- 2025 revenue +22%

- Higher profitability vs 2024

- Focus: energy, industrial green transition

- Capex on horizontal borers to expand niche share

- Balances cyclical crop portfolio

High-growth agri portfolio: avocados, macadamia, Brazil output up; $60M capex shields margins

Stars: avocados, macadamia, Brazil arable, specialty tea, AJT — high growth and share with 2025 metrics: avocado area 448 ha (target 650), macadamia price ~$7.27/kg (Q1 2025), Brazil output 1.8M t (+12%), capex $60m total (2025–26), AJT rev +22% (2025), irrigation 60% proj.; capex protects margins but keeps cash burn high.

| Unit | 2025 | Note |

|---|---|---|

| Avocado area | 448 ha | target 650 ha |

| Macadamia price | $7.27/kg | Q1 2025 |

| Brazil output | 1.8M t | +12% YoY |

| Capex | $60m | 2025–26 committed |

| AJT rev | +22% | 2025 vs 2024 |

What is included in the product

Comprehensive BCG Matrix review of Camellia’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing each Camellia unit in a quadrant for clear portfolio decisions

Cash Cows

Commodity Black Tea

Kenya and Malawi standard black tea production remains Camellia’s volume driver in a mature market; 2025 estate output ~78,000 tonnes (group share), keeping global market share high despite ~1% CAGR demand.

Operations run industrial-scale, low-cost platforms with 2025 EBITDA margin ~22%, funding dividends and new-crop capex; maintenance capex ~3% of revenue, low versus cash generation.

Indian Tea Operations

Camellia’s Indian tea gardens in Dooars and Assam, operating 100+ years, are Cash Cows: in FY2024 they produced ~42k tonnes of tea and delivered ~18% operating margin, despite periodic weather-related yield dips.

2025 strategy emphasizes milking via mechanization to cut plucking costs by an estimated 12–15%, not aggressive acreage growth.

Cash flows from India fund the Value Enhancement Plan and higher-growth African ventures; India operations contributed ~£28m free cash flow in FY2024.

Bangladesh Tea Estates

Bangladesh Tea Estates hold a leading domestic market share ~28% in 2025 and benefited from a government-backed minimum price introduced Jan 2025 that lifted average realized prices 12% y/y, stabilizing revenue to ~BDT 2.3bn (US$21m) for Camellia’s estates. The local tea market is mature with steady annual volume growth ~2–3% and robust, predictable demand. Camellia’s reputational premium yields higher blend prices and consistent local-currency cashflow; capex shifts to factory efficiency rather than marketing to maximize cash take.

Investment Property Portfolio

Camellia’s Investment Property Portfolio acts as a cash cow: significant non-core land and investment properties generate passive liquidity without needing operational growth.

Under the 2025 Value Enhancement Plan the group sold assets, lifting cash reserves to over 80 million pounds by mid-2025 to fund strategic transition.

These low-growth, high-value assets stabilize the balance sheet and provide predictable funding for reinvestment and debt reduction.

- Cash reserves: >80 million pounds (mid-2025)

- Role: passive liquidity source, not operational growth

- Use: fund transition, reinvestment, and debt paydown

- Segment: low growth, high value; balance-sheet stabilizer

Instant Tea Manufacturing

The Instant Tea Manufacturing unit in India is a mature, low-growth cash cow supplying bulk ingredients to global beverage brands; Camellia holds a secure market position and volumes are projected to stabilize by Q4 2025, with FY2024 revenue ~USD 38m and EBITDA margin ~18% (company filings, 2024).

It delivers steady free cash flow used to service corporate debt and fund agronomy R&D for new crop trials; capital expenditure remains low (~2% of sales), and no major consumer marketing or radical product innovation is required.

- FY2024 revenue ~USD 38m

- EBITDA margin ~18%

- CapEx ~2% of sales

- Volumes stable by Q4 2025

- Cash flows service debt + fund crop R&D

Camellia's Tea Powerhouses: Kenya/Malawi, India, Bangladesh & Instant Tea Profits

Camellia’s Cash Cows: Kenya/Malawi tea (2025 group output ~78,000t; ~22% EBITDA), India gardens (FY2024 ~42,000t; ~18% op margin; ~£28m FCF), Bangladesh estates (2025 market share ~28%; revenue ~BDT2.3bn/US$21m), Instant Tea (FY2024 revenue ~USD38m; EBITDA ~18%).

| Asset | Key 2024/25 |

|---|---|

| Kenya/Malawi | 78,000t; 22% EBITDA |

| India gardens | 42,000t; £28m FCF; 18% margin |

| Bangladesh | 28% share; BDT2.3bn |

| Instant Tea | USD38m; 18% EBITDA |

What You See Is What You Get

Camellia BCG Matrix

The file you're previewing on this page is the exact Camellia BCG Matrix report you'll receive after purchase—no watermarks, no placeholder content—just a fully formatted, strategy-ready document tailored for portfolio assessment and resource allocation.

This preview mirrors the final deliverable: a market-informed, professionally designed BCG Matrix that arrives in your inbox immediately after payment, ready for editing, printing, or sharing with stakeholders.

What you see is the authentic Camellia BCG Matrix file included with your one-time purchase, crafted by strategy professionals to support clear decision-making and prioritization across products or business units.

There are no surprises—this preview is the final product, formatted for presentation and integration into planning, pitches, or executive reviews right away.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

The Camellia BCG Matrix snapshot highlights how its product lines map across growth and market share—revealing potential Stars driving future growth, Cash Cows funding operations, Question Marks needing investment decisions, and Dogs that may warrant divestment. This concise view helps prioritize portfolio moves and spot strategic risks in a changing market. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word and Excel reports to turn insights into action.

Stars

Avocado Production

Avocado Production is a Star for Camellia: its 51% stake in Kenyan-listed Kakuzi and expanding Tanzanian operations give it leadership in a fast-growing market; global avocado demand rose ~6–8% annually to 2025, driven by Europe and Asia. Camellia raised its Tanzanian avocado area to 448 ha in 2025, targeting 650 ha, and is investing heavily in irrigation and orchard maturation. High growth sustains strong market share but keeps cash burn elevated due to capex and multi-year crop gestation.

Macadamia Nuts

Macadamia nuts are a Star for Camellia: high-growth segment with prices up 77% in early 2025, boosting EBITDA margins as unit realization rose from $4.10/kg in 2023 to ~$7.27/kg in Q1 2025.

Large-scale orchards in Malawi and South Africa are maturing—tree yields climbing ~18% YoY—raising Camellia’s exportable volumes by ~22% in 2025.

Australia’s 2025 shortfall tightened global supply, letting Camellia gain share and command premiums ~15–25% above world averages.

Ongoing CAPEX in processing and precision irrigation (~$12m committed through 2026) is needed to protect margins and fend off rivals.

Specialty and Branded Tea

While the global tea market is broadly mature, Camellia’s specialty and branded tea units—notably Darjeeling estates and Jing Tea—act as Stars, targeting premium/luxury segments that grew ~6–8% CAGR vs 1–2% for commodity tea (2021–25); Jing Tea posted a 13% revenue rise in mid-2025. The company uses tea tourism and high-margin retail to differentiate from bulk production, but sustaining estate prestige needs ongoing promotion and strict quality control.

Brazilian Arable Crops

The Brazilian arable crops unit is a Star: 2025 soy and maize output rose 12% to 1.8 million tonnes, driven by awards for operational excellence and a program to irrigate 60% of land, boosting yields by ~15%.

Brazil’s role as a top-3 global exporter gives Camellia high market share amid continued volume growth; mechanization and water-resilience capex of $48m in 2025 shows reinvestment to secure dominance.

- 2025 production 1.8M t (+12%)

- Irrigation coverage 60% (project)

- Yield uplift ~15%

- 2025 capex $48m

- High market share in top-3 exporting country

Precision Engineering Services

AJT Engineering, Camellia’s UK precision-services arm, is a high-growth star: revenues rose 22% in 2025 with improved margins, driven by specialist work for energy and industrial clients amid a green-infrastructure shift.

Camellia’s 2025 capex on horizontal borers and precision kit targets niche share gains; AJT now acts as a non-agricultural growth engine smoothing crop-cycle volatility.

- 2025 revenue +22%

- Higher profitability vs 2024

- Focus: energy, industrial green transition

- Capex on horizontal borers to expand niche share

- Balances cyclical crop portfolio

High-growth agri portfolio: avocados, macadamia, Brazil output up; $60M capex shields margins

Stars: avocados, macadamia, Brazil arable, specialty tea, AJT — high growth and share with 2025 metrics: avocado area 448 ha (target 650), macadamia price ~$7.27/kg (Q1 2025), Brazil output 1.8M t (+12%), capex $60m total (2025–26), AJT rev +22% (2025), irrigation 60% proj.; capex protects margins but keeps cash burn high.

| Unit | 2025 | Note |

|---|---|---|

| Avocado area | 448 ha | target 650 ha |

| Macadamia price | $7.27/kg | Q1 2025 |

| Brazil output | 1.8M t | +12% YoY |

| Capex | $60m | 2025–26 committed |

| AJT rev | +22% | 2025 vs 2024 |

What is included in the product

Comprehensive BCG Matrix review of Camellia’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing each Camellia unit in a quadrant for clear portfolio decisions

Cash Cows

Commodity Black Tea

Kenya and Malawi standard black tea production remains Camellia’s volume driver in a mature market; 2025 estate output ~78,000 tonnes (group share), keeping global market share high despite ~1% CAGR demand.

Operations run industrial-scale, low-cost platforms with 2025 EBITDA margin ~22%, funding dividends and new-crop capex; maintenance capex ~3% of revenue, low versus cash generation.

Indian Tea Operations

Camellia’s Indian tea gardens in Dooars and Assam, operating 100+ years, are Cash Cows: in FY2024 they produced ~42k tonnes of tea and delivered ~18% operating margin, despite periodic weather-related yield dips.

2025 strategy emphasizes milking via mechanization to cut plucking costs by an estimated 12–15%, not aggressive acreage growth.

Cash flows from India fund the Value Enhancement Plan and higher-growth African ventures; India operations contributed ~£28m free cash flow in FY2024.

Bangladesh Tea Estates

Bangladesh Tea Estates hold a leading domestic market share ~28% in 2025 and benefited from a government-backed minimum price introduced Jan 2025 that lifted average realized prices 12% y/y, stabilizing revenue to ~BDT 2.3bn (US$21m) for Camellia’s estates. The local tea market is mature with steady annual volume growth ~2–3% and robust, predictable demand. Camellia’s reputational premium yields higher blend prices and consistent local-currency cashflow; capex shifts to factory efficiency rather than marketing to maximize cash take.

Investment Property Portfolio

Camellia’s Investment Property Portfolio acts as a cash cow: significant non-core land and investment properties generate passive liquidity without needing operational growth.

Under the 2025 Value Enhancement Plan the group sold assets, lifting cash reserves to over 80 million pounds by mid-2025 to fund strategic transition.

These low-growth, high-value assets stabilize the balance sheet and provide predictable funding for reinvestment and debt reduction.

- Cash reserves: >80 million pounds (mid-2025)

- Role: passive liquidity source, not operational growth

- Use: fund transition, reinvestment, and debt paydown

- Segment: low growth, high value; balance-sheet stabilizer

Instant Tea Manufacturing

The Instant Tea Manufacturing unit in India is a mature, low-growth cash cow supplying bulk ingredients to global beverage brands; Camellia holds a secure market position and volumes are projected to stabilize by Q4 2025, with FY2024 revenue ~USD 38m and EBITDA margin ~18% (company filings, 2024).

It delivers steady free cash flow used to service corporate debt and fund agronomy R&D for new crop trials; capital expenditure remains low (~2% of sales), and no major consumer marketing or radical product innovation is required.

- FY2024 revenue ~USD 38m

- EBITDA margin ~18%

- CapEx ~2% of sales

- Volumes stable by Q4 2025

- Cash flows service debt + fund crop R&D

Camellia's Tea Powerhouses: Kenya/Malawi, India, Bangladesh & Instant Tea Profits

Camellia’s Cash Cows: Kenya/Malawi tea (2025 group output ~78,000t; ~22% EBITDA), India gardens (FY2024 ~42,000t; ~18% op margin; ~£28m FCF), Bangladesh estates (2025 market share ~28%; revenue ~BDT2.3bn/US$21m), Instant Tea (FY2024 revenue ~USD38m; EBITDA ~18%).

| Asset | Key 2024/25 |

|---|---|

| Kenya/Malawi | 78,000t; 22% EBITDA |

| India gardens | 42,000t; £28m FCF; 18% margin |

| Bangladesh | 28% share; BDT2.3bn |

| Instant Tea | USD38m; 18% EBITDA |

What You See Is What You Get

Camellia BCG Matrix

The file you're previewing on this page is the exact Camellia BCG Matrix report you'll receive after purchase—no watermarks, no placeholder content—just a fully formatted, strategy-ready document tailored for portfolio assessment and resource allocation.

This preview mirrors the final deliverable: a market-informed, professionally designed BCG Matrix that arrives in your inbox immediately after payment, ready for editing, printing, or sharing with stakeholders.

What you see is the authentic Camellia BCG Matrix file included with your one-time purchase, crafted by strategy professionals to support clear decision-making and prioritization across products or business units.

There are no surprises—this preview is the final product, formatted for presentation and integration into planning, pitches, or executive reviews right away.