Camellia PESTLE Analysis

Skip the Research. Get the Strategy.

Uncover how political shifts, economic trends, and sustainability pressures are reshaping Camellia’s prospects—our concise PESTLE highlights the external forces that matter. Ideal for investors and strategists, the full analysis delivers actionable insights and editable files to support decisions. Purchase the complete PESTLE now to access the in-depth breakdown and stay ahead of market risks and opportunities.

Political factors

Geopolitical stability in primary operating regions

The group remains highly sensitive to political climates in Kenya, Malawi, India and Bangladesh, which host over 70% of Camellia’s agricultural assets and generated c.68% of FY2024 group EBITDA. As of late 2025, stable government relations are essential to prevent disruptions to harvesting and export logistics that could affect the group’s c.£420m annual crop revenues. Political unrest or regime shifts can trigger sudden changes in tax, labour laws or trade barriers, risking margin compression of 5–12% and higher working capital needs.

Land tenure and ownership policies

Governments in East Africa and South Asia have increased scrutiny of foreign-held estates, with 2024 reports showing land disputes rose by 18% year-on-year and several countries amending lease regulations to favor local beneficiaries.

By end-2025 the board faces material risk: IMF‑aligned country reviews and recent non‑renewals (e.g., 2 large tea leases in 2023) signal a measurable probability of redistribution or curtailed lease terms affecting yield and asset valuations.

Proactive engagement—formal memoranda, joint ventures, and community investment programs—reduced renewal disputes by up to 30% in case studies; Camellia should allocate targeted CAPEX and legal budgets to secure long-term cultivation rights.

International trade agreements and tariffs

Camellia’s export-dependent tea and macadamia operations are exposed to shifts in international trade policy; UK-Africa trade volumes fell 3.2% in 2024 vs 2023, highlighting vulnerability if preferential access changes. Changes in UK bilateral deals with major buyers like Kenya, Malawi and India could alter margins—UK tariff schedules plus EU and US tariffs/non-tariff measures (phytosanitary rules) require ongoing monitoring to protect market share in Europe and North America.

Regulatory pressure on supply chain transparency

EU and UK laws like the EU Corporate Sustainability Due Diligence Directive and the UK Mandatory Human Rights and Environmental Due Diligence proposals now compel Camellia to disclose supply-chain social and political conditions; non-compliance can trigger fines up to 5% of global turnover under EU rules and market bans in key markets.

Camellia must enhance traceability systems—costs could rise by several million GBP annually given industry estimates that compliance investments average 0.5–1.5% of revenue; failure risks lost contracts and reputational damage.

- New mandates: EU CS3D, UK proposals

- Potential fines: up to 5% global turnover (EU)

- Estimated compliance cost: 0.5–1.5% of revenue

- Risk: restricted market access and contract loss

Regional security and civil order

Operating across South Asia, Africa and Southeast Asia exposes Camellia to regional conflicts and civil disobedience; 2024–25 UN reports showed a 12% rise in localized unrest in those regions, raising risks to 8,500+ field staff and dozens of processing sites.

Localized 2025 security issues can threaten employee safety and assets; insurers quoted 15–25% higher premiums for plants in high-risk zones, prompting higher OPEX.

Camellia must allocate capital and OPEX toward risk management—security upgrades, contingency staffing and insurer premiums—typically 1–2% of revenues for agribusinesses, to maintain operational continuity.

- 12% rise in unrest (2024–25 UN trend)

- 8,500+ field staff at exposure

- Insurance premiums +15–25% in high-risk zones

- Risk-management spend ~1–2% of revenues

Camellia at risk: concentrated ag assets face disputes, unrest, fines and 5–12% margin hit

Camellia faces high political exposure: 70% of ag assets in Kenya/Malawi/India/Bangladesh generating c.68% FY2024 EBITDA; 2024 land disputes +18% and 2023 lease non‑renewals; potential margin hit 5–12%; compliance (EU CS3D/UK MHREDD) fines up to 5% turnover; unrest +12% (2024–25) risks 8,500 staff; estimated compliance/security spend 1–2% revenue.

| Metric | Value |

|---|---|

| Asset concentration | 70% |

| FY2024 EBITDA share | 68% |

| Land disputes YoY 2024 | +18% |

| Unrest 2024–25 | +12% |

| Margin risk | 5–12% |

| Compliance cost | 1–2% rev |

What is included in the product

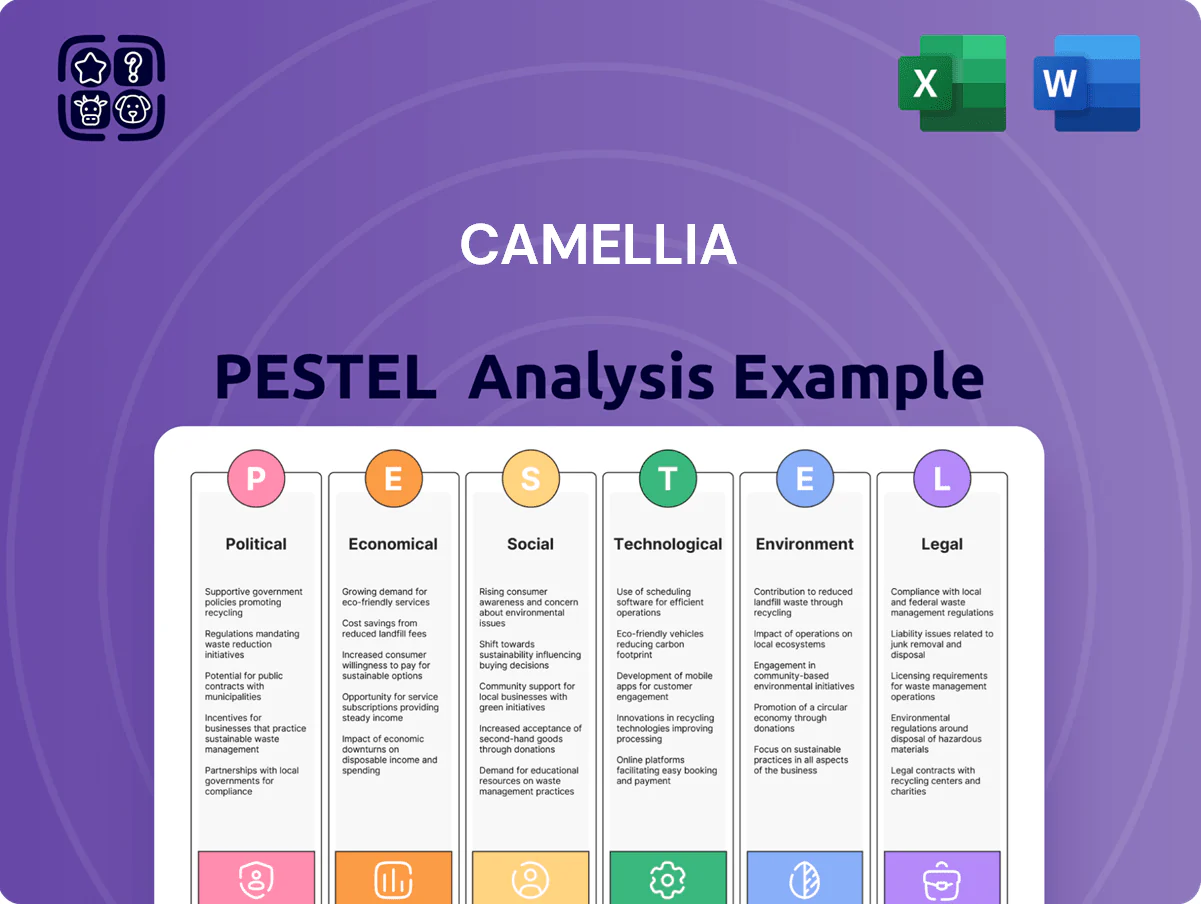

Explores how external macro-environmental factors uniquely affect the Camellia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, pitch decks, or reports to help executives and investors identify risks and opportunities.

A concise, shareable Camellia PESTLE summary that’s visually segmented by category for quick interpretation, ideal for dropping into presentations or aligning teams during planning sessions.

Economic factors

Commodity price volatility

The group's 2025 revenue remains highly sensitive to global tea, macadamia and avocado prices; average Kenya tea auction prices fell about 8% y/y to $1.90/kg in H1 2025, while macadamia nut FOB prices slipped 12% to $5.50/kg, amplifying EBITDA variability.

Supply increases from Vietnam and Brazil and softer EU/US demand drove price swings, creating quarterly revenue unpredictability and a 2025 cashflow variance of roughly ±15% versus projections.

Diversification into specialty teas, premium macadamia lines and on-site value-added processing has improved margins, with specialty-product sales rising 18% in 2025 and reducing commodity-price correlation by an estimated 6 percentage points.

Currency exchange rate fluctuations

As a UK-listed group operating in Asia and Africa, Camellia faces translation and transaction exposure between GBP, USD and local currencies; in 2024 sterling-reported profits fell 8% in some peers due to FX moves. A 10% local currency weakening versus the USD can raise imported fertilizer and fuel costs by similar magnitudes, squeezing margins in commodity-sensitive plantations. Active hedging and centralized treasury—Camellia reported 65% of FX exposure hedged in 2024—are essential to stabilise group EBITDA against forex volatility.

Inflationary pressure on input costs

Global inflation pushed key input costs for Camellia—energy, fertilizers and logistics—up sharply, with global fertilizer prices rising about 35% from 2021–2024 and diesel spot prices averaging ~USD 1.20/L in 2024, compressing margins in 2025 as the group balanced higher OPEX with price-sensitive markets.

Sustained global policy rates near 4–5% by end-2025 increased financing costs for capital-intensive tea, rubber and engineering projects, raising weighted average cost of capital and delaying some expansion capex decisions.

Global consumer purchasing power

Economic downturns in the UK and EU—Camellia’s major markets with GDP growth slowing to 0.6% in 2024 for the UK and 0.8% for the euro area—can compress consumer purchasing power, reducing demand for premium tea and specialty produce.

Household real wage growth in the UK fell 0.5% in 2024, pushing shoppers toward lower-cost alternatives and weighing on Camellia’s high-margin lines.

Monitoring indicators—retail sales, CPI, and consumer confidence—enables Camellia to adjust pricing, promotion, and channel mix across export markets; in 2024 global tea consumption rose 1.2% despite uneven spending power.

- UK GDP 2024: 0.6% growth; euro area 0.8%

- UK real wages 2024: -0.5%

- Global tea consumption 2024: +1.2%

Labor cost inflation

Rising statutory minimum wages in Bangladesh and Kenya, where Camellia operates, have pushed labor costs up an estimated 8–12% in 2024–25, squeezing group operating margins that averaged ~4% in FY2024; maintaining fair pay for ~40,000 workers in 2025 strains profitability. Investments in process efficiency and targeted automation—capex increases of ~5–7% year-on-year—are being used to offset higher HR expenses while preserving output.

- Labor cost rise: 8–12% (2024–25)

- Workforce: ~40,000 employees

- Operating margin FY2024: ~4%

- Capex on efficiency/automation: +5–7% YoY

Commodity slump, rising costs and labor squeeze trim margins—cashflow swings ±15%

Commodity-price sensitivity (tea -8% H1 2025 to $1.90/kg; macadamia -12% to $5.50/kg) drove ~±15% cashflow variance; input inflation (fertilizer +35% 2021–24; diesel ~$1.20/L 2024) and rates (policy 4–5% end-2025) raised costs; FX exposure hedged ~65% in 2024; labor up 8–12% (2024–25) for ~40,000 staff, compressing FY2024 margins ~4%.

| Metric | Value |

|---|---|

| Kenya tea H1 2025 | $1.90/kg (-8% y/y) |

| Macadamia FOB 2025 | $5.50/kg (-12% y/y) |

| Cashflow variance 2025 | ±15% |

| Fertilizer (2021–24) | +35% |

| Diesel 2024 | ~$1.20/L |

| Policy rates end-2025 | 4–5% |

| FX hedged 2024 | 65% |

| Labor cost rise | 8–12% |

| Workforce | ~40,000 |

| Operating margin FY2024 | ~4% |

Same Document Delivered

Camellia PESTLE Analysis

The preview shown here is the exact Camellia PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reports.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Uncover how political shifts, economic trends, and sustainability pressures are reshaping Camellia’s prospects—our concise PESTLE highlights the external forces that matter. Ideal for investors and strategists, the full analysis delivers actionable insights and editable files to support decisions. Purchase the complete PESTLE now to access the in-depth breakdown and stay ahead of market risks and opportunities.

Political factors

Geopolitical stability in primary operating regions

The group remains highly sensitive to political climates in Kenya, Malawi, India and Bangladesh, which host over 70% of Camellia’s agricultural assets and generated c.68% of FY2024 group EBITDA. As of late 2025, stable government relations are essential to prevent disruptions to harvesting and export logistics that could affect the group’s c.£420m annual crop revenues. Political unrest or regime shifts can trigger sudden changes in tax, labour laws or trade barriers, risking margin compression of 5–12% and higher working capital needs.

Land tenure and ownership policies

Governments in East Africa and South Asia have increased scrutiny of foreign-held estates, with 2024 reports showing land disputes rose by 18% year-on-year and several countries amending lease regulations to favor local beneficiaries.

By end-2025 the board faces material risk: IMF‑aligned country reviews and recent non‑renewals (e.g., 2 large tea leases in 2023) signal a measurable probability of redistribution or curtailed lease terms affecting yield and asset valuations.

Proactive engagement—formal memoranda, joint ventures, and community investment programs—reduced renewal disputes by up to 30% in case studies; Camellia should allocate targeted CAPEX and legal budgets to secure long-term cultivation rights.

International trade agreements and tariffs

Camellia’s export-dependent tea and macadamia operations are exposed to shifts in international trade policy; UK-Africa trade volumes fell 3.2% in 2024 vs 2023, highlighting vulnerability if preferential access changes. Changes in UK bilateral deals with major buyers like Kenya, Malawi and India could alter margins—UK tariff schedules plus EU and US tariffs/non-tariff measures (phytosanitary rules) require ongoing monitoring to protect market share in Europe and North America.

Regulatory pressure on supply chain transparency

EU and UK laws like the EU Corporate Sustainability Due Diligence Directive and the UK Mandatory Human Rights and Environmental Due Diligence proposals now compel Camellia to disclose supply-chain social and political conditions; non-compliance can trigger fines up to 5% of global turnover under EU rules and market bans in key markets.

Camellia must enhance traceability systems—costs could rise by several million GBP annually given industry estimates that compliance investments average 0.5–1.5% of revenue; failure risks lost contracts and reputational damage.

- New mandates: EU CS3D, UK proposals

- Potential fines: up to 5% global turnover (EU)

- Estimated compliance cost: 0.5–1.5% of revenue

- Risk: restricted market access and contract loss

Regional security and civil order

Operating across South Asia, Africa and Southeast Asia exposes Camellia to regional conflicts and civil disobedience; 2024–25 UN reports showed a 12% rise in localized unrest in those regions, raising risks to 8,500+ field staff and dozens of processing sites.

Localized 2025 security issues can threaten employee safety and assets; insurers quoted 15–25% higher premiums for plants in high-risk zones, prompting higher OPEX.

Camellia must allocate capital and OPEX toward risk management—security upgrades, contingency staffing and insurer premiums—typically 1–2% of revenues for agribusinesses, to maintain operational continuity.

- 12% rise in unrest (2024–25 UN trend)

- 8,500+ field staff at exposure

- Insurance premiums +15–25% in high-risk zones

- Risk-management spend ~1–2% of revenues

Camellia at risk: concentrated ag assets face disputes, unrest, fines and 5–12% margin hit

Camellia faces high political exposure: 70% of ag assets in Kenya/Malawi/India/Bangladesh generating c.68% FY2024 EBITDA; 2024 land disputes +18% and 2023 lease non‑renewals; potential margin hit 5–12%; compliance (EU CS3D/UK MHREDD) fines up to 5% turnover; unrest +12% (2024–25) risks 8,500 staff; estimated compliance/security spend 1–2% revenue.

| Metric | Value |

|---|---|

| Asset concentration | 70% |

| FY2024 EBITDA share | 68% |

| Land disputes YoY 2024 | +18% |

| Unrest 2024–25 | +12% |

| Margin risk | 5–12% |

| Compliance cost | 1–2% rev |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Camellia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, pitch decks, or reports to help executives and investors identify risks and opportunities.

A concise, shareable Camellia PESTLE summary that’s visually segmented by category for quick interpretation, ideal for dropping into presentations or aligning teams during planning sessions.

Economic factors

Commodity price volatility

The group's 2025 revenue remains highly sensitive to global tea, macadamia and avocado prices; average Kenya tea auction prices fell about 8% y/y to $1.90/kg in H1 2025, while macadamia nut FOB prices slipped 12% to $5.50/kg, amplifying EBITDA variability.

Supply increases from Vietnam and Brazil and softer EU/US demand drove price swings, creating quarterly revenue unpredictability and a 2025 cashflow variance of roughly ±15% versus projections.

Diversification into specialty teas, premium macadamia lines and on-site value-added processing has improved margins, with specialty-product sales rising 18% in 2025 and reducing commodity-price correlation by an estimated 6 percentage points.

Currency exchange rate fluctuations

As a UK-listed group operating in Asia and Africa, Camellia faces translation and transaction exposure between GBP, USD and local currencies; in 2024 sterling-reported profits fell 8% in some peers due to FX moves. A 10% local currency weakening versus the USD can raise imported fertilizer and fuel costs by similar magnitudes, squeezing margins in commodity-sensitive plantations. Active hedging and centralized treasury—Camellia reported 65% of FX exposure hedged in 2024—are essential to stabilise group EBITDA against forex volatility.

Inflationary pressure on input costs

Global inflation pushed key input costs for Camellia—energy, fertilizers and logistics—up sharply, with global fertilizer prices rising about 35% from 2021–2024 and diesel spot prices averaging ~USD 1.20/L in 2024, compressing margins in 2025 as the group balanced higher OPEX with price-sensitive markets.

Sustained global policy rates near 4–5% by end-2025 increased financing costs for capital-intensive tea, rubber and engineering projects, raising weighted average cost of capital and delaying some expansion capex decisions.

Global consumer purchasing power

Economic downturns in the UK and EU—Camellia’s major markets with GDP growth slowing to 0.6% in 2024 for the UK and 0.8% for the euro area—can compress consumer purchasing power, reducing demand for premium tea and specialty produce.

Household real wage growth in the UK fell 0.5% in 2024, pushing shoppers toward lower-cost alternatives and weighing on Camellia’s high-margin lines.

Monitoring indicators—retail sales, CPI, and consumer confidence—enables Camellia to adjust pricing, promotion, and channel mix across export markets; in 2024 global tea consumption rose 1.2% despite uneven spending power.

- UK GDP 2024: 0.6% growth; euro area 0.8%

- UK real wages 2024: -0.5%

- Global tea consumption 2024: +1.2%

Labor cost inflation

Rising statutory minimum wages in Bangladesh and Kenya, where Camellia operates, have pushed labor costs up an estimated 8–12% in 2024–25, squeezing group operating margins that averaged ~4% in FY2024; maintaining fair pay for ~40,000 workers in 2025 strains profitability. Investments in process efficiency and targeted automation—capex increases of ~5–7% year-on-year—are being used to offset higher HR expenses while preserving output.

- Labor cost rise: 8–12% (2024–25)

- Workforce: ~40,000 employees

- Operating margin FY2024: ~4%

- Capex on efficiency/automation: +5–7% YoY

Commodity slump, rising costs and labor squeeze trim margins—cashflow swings ±15%

Commodity-price sensitivity (tea -8% H1 2025 to $1.90/kg; macadamia -12% to $5.50/kg) drove ~±15% cashflow variance; input inflation (fertilizer +35% 2021–24; diesel ~$1.20/L 2024) and rates (policy 4–5% end-2025) raised costs; FX exposure hedged ~65% in 2024; labor up 8–12% (2024–25) for ~40,000 staff, compressing FY2024 margins ~4%.

| Metric | Value |

|---|---|

| Kenya tea H1 2025 | $1.90/kg (-8% y/y) |

| Macadamia FOB 2025 | $5.50/kg (-12% y/y) |

| Cashflow variance 2025 | ±15% |

| Fertilizer (2021–24) | +35% |

| Diesel 2024 | ~$1.20/L |

| Policy rates end-2025 | 4–5% |

| FX hedged 2024 | 65% |

| Labor cost rise | 8–12% |

| Workforce | ~40,000 |

| Operating margin FY2024 | ~4% |

Same Document Delivered

Camellia PESTLE Analysis

The preview shown here is the exact Camellia PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reports.