Computer Age Management Services Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

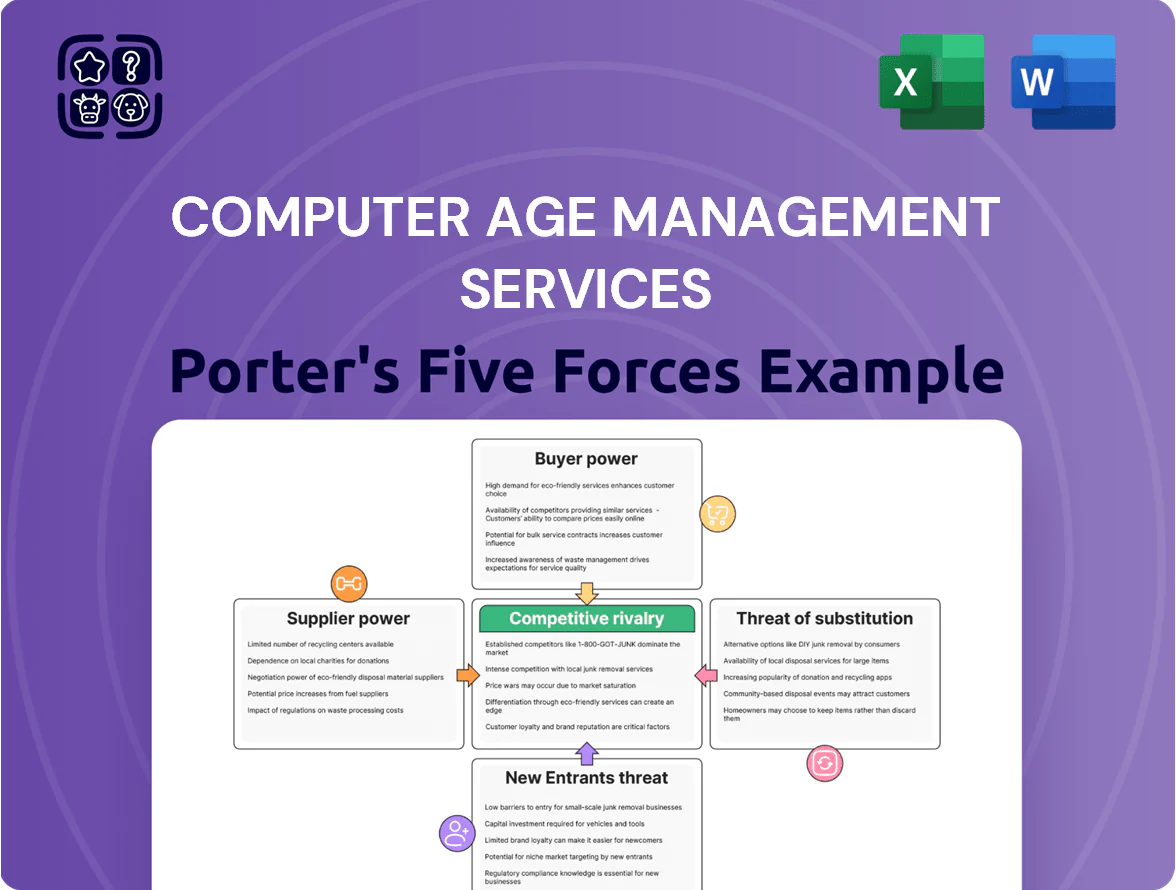

Computer Age Management Services faces moderate supplier leverage, rising buyer expectations, and meaningful competitive rivalry from fintech and legacy players, while regulatory shifts and technological change shape entry barriers and substitute threats; this snapshot highlights critical tensions in its market position. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy tailored to Computer Age Management Services.

Suppliers Bargaining Power

Specialized IT Talent Availability

CAMS depends on fintech and proprietary-software talent to run its platform, and by late 2025 India’s fintech hiring premium rose ~18% year-over-year, giving specialists clear salary leverage.

That supplier power pressures margins, but CAMS reduces risk by investing in internal training programs and a retention-focused culture, keeping turnover below industry average—about 12% vs fintech sector ~20% in 2024.

Cloud and Infrastructure Providers

CAMS (Computer Age Management Services) relies on global cloud providers (AWS, Azure, GCP) for storage and compute, creating moderate vendor dependence; in FY2024 CAMS processed over 1 billion mutual fund transactions, so uptime and scale matter.

The firm’s size gives leverage to win discounts—enterprise cloud deals often cut list prices 30–50%—but migrating petabytes of sensitive financial data is complex and costly, limiting rapid switches.

This technical lock-in and regulatory data residency needs keep cloud vendors in a stable, moderately strong supplier position for CAMS.

Cybersecurity and Compliance Vendors

With India’s RBI and SEBI tightening data rules—RBI’s 2023 operational resilience guidelines and SEBI’s 2024 cyber norms—CAMS must buy certified security stacks (SIEM, EDR, encryption) from specialist vendors to keep licenses; noncompliance fines can exceed ₹100 crore for systemic breaches.

Financial Data Feed Providers

- Essential input: low-latency feeds

- Top vendors: Bloomberg, Refinitiv, major exchanges

- Market share: >70% top-3 (2024)

- Impact: high supplier power → higher costs

Hardware and Networking Equipment Suppliers

Maintaining CAMS’ physical data centers and disaster-recovery sites needs continuous supply of high-performance servers and networking gear; global market size for enterprise servers was $92.5B in 2024, but certified vendors for financial-grade reliability are few.

CAMS reduces supplier power by holding multi-vendor contracts and spares, keeping procurement lead times under 12 weeks and avoiding single-vendor concentration above 25% of spend.

- Enterprise server market: $92.5B (2024)

- Target max single-vendor spend: 25%

- Procurement lead time: ≤12 weeks

- Multiple certified vendors: reduces downtime risk

Supplier power high: talent costs up, market‑data concentrated, CAMS caps risk

Supplier power is moderate-to-high: talent costs rose ~18% YoY (2025), cloud discounts 30–50% offset lock-in, top-3 market-data vendors control >70% (2024), servers market $92.5B (2024); CAMS limits risk with retention (turnover ~12% vs fintech ~20% in 2024), multi-vendor caps (max 25% spend) and ≤12-week lead times.

| Item | Metric |

|---|---|

| Fintech hiring premium | +18% YoY (2025) |

| Market-data share | >70% top‑3 (2024) |

| Server market | $92.5B (2024) |

| Turnover | 12% (CAMS) vs 20% fintech (2024) |

| Cloud discounts | 30–50% enterprise deals |

What is included in the product

Tailored Porter's Five Forces analysis for Computer Age Management Services that uncovers key drivers of competition, buyer and supplier influence, entry barriers, and substitution risks impacting its pricing power and profitability.

One-sheet Porter's Five Forces for CAMS—quickly spot regulatory, competitive, supplier, buyer, and substitute pressures to streamline strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of Asset Management Companies

The Indian mutual fund market is top-heavy: the top 10 AMCs held about 86% of AUM (assets under management) as of Dec 2025, and these clients account for roughly 70% of CAMS's FY2025 revenue, giving them strong fee-negotiation leverage.

Large-volume AMCs push for lower basis-point fees across transfer-agent and transaction services; CAMS needs continuous tech upgrades and SLA improvements to protect gross margins and avoid fee compression.

High Switching Costs for Clients

The migration of decades of investor records and workflows to a new registrar and transfer agent (RTA) can take 6–24 months and cost ₹5–20 crore for a single asset management company (AMC), creating strong operational stickiness that cuts customer bargaining power once onboarded to CAMS.

Risk of data loss or service disruption—seen in industry transition failure rates near 10% in 2023—further deters switching, so retained clients face high effective switching costs and reduced leverage.

Demand for Digital Transformation Tools

Modern customers—distributors and investors—demand sophisticated digital interfaces and real-time reporting, pushing CAMS to boost front-end tech spend; CAMS reported capital expenditure of INR 250–300 crore in FY2024 for technology upgrades.

This pressure compels CAMS to tailor solutions for AMCs aiming to improve end-user experience, increasing switching costs and deepening integration, which offsets some customer bargaining power.

Regulatory Influence on Fee Structures

SEBI's 2024 cap on average total expense ratios (TER) tightened margins: average equity TER fell to 1.75% from 1.95% in 2022, pushing AMCs to demand lower processing fees from RTAs like CAMS during renewals.

Mandated investor-cost cuts give AMCs a formal lever to renegotiate contracts, strengthening buyer power and pressuring CAMS' fee income; in 2024 CAMS reported 6% margin compression in RTA services versus 2022.

- SEBI TER cut: equity funds 1.95%→1.75% (2022→2024)

- AMCs pass savings to RTAs at renewals

- CAMS RTA margin compression ~6% (2024 vs 2022)

- Regulation = legitimized bargaining leverage

Deep Operational Integration

CAMS embeds into an AMC’s operations—handling KYC, SIPs, dividend processing and investor servicing for over 40 of the top 50 mutual funds, linking CAMS uptime and process speed directly to an AMC’s NAV operations and investor flows.

This deep integration creates mutual dependency: AMCs rely on CAMS’ tech and scale while CAMS depends on multi-year service contracts (often 3–5 years) and high switching costs, so power tilts toward cooperative, long-term pricing rather than short-term bargaining.

- Handles KYC, SIP, dividend for 40/50 top funds

- High switching cost: tech, compliance, data migration

- Typical contract: 3–5 years, renewals common

Top AMCs' fee power squeezes RTAs—stickiness offsets TER cuts, margins down ~6%

Buyers (top AMCs) hold strong fee leverage—top 10 AMCs = ~86% AUM (Dec 2025) and ~70% of CAMS FY2025 revenue—pushing lower bps; high switching costs (6–24 months, ₹5–20 crore) and 3–5 year contracts create stickiness that limits bargaining; SEBI TER cut (1.95%→1.75%, 2022→2024) legitimized renegotiation, causing ~6% RTA margin compression (2024 vs 2022).

| Metric | Value |

|---|---|

| Top-10 AMC AUM share (Dec 2025) | 86% |

| CAMS FY2025 rev from top AMCs | ~70% |

| Switch cost per AMC | ₹5–20 crore |

| Switch time | 6–24 months |

| Contract length | 3–5 yrs |

| TER cut (equity) | 1.95%→1.75% (2022→2024) |

| RTA margin change | -6% (2024 vs 2022) |

Same Document Delivered

Computer Age Management Services Porter's Five Forces Analysis

This preview shows the exact Computer Age Management Services Porter's Five Forces Analysis you'll receive—no placeholders or mockups; the full, professionally formatted document is available for instant download after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Computer Age Management Services faces moderate supplier leverage, rising buyer expectations, and meaningful competitive rivalry from fintech and legacy players, while regulatory shifts and technological change shape entry barriers and substitute threats; this snapshot highlights critical tensions in its market position. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy tailored to Computer Age Management Services.

Suppliers Bargaining Power

Specialized IT Talent Availability

CAMS depends on fintech and proprietary-software talent to run its platform, and by late 2025 India’s fintech hiring premium rose ~18% year-over-year, giving specialists clear salary leverage.

That supplier power pressures margins, but CAMS reduces risk by investing in internal training programs and a retention-focused culture, keeping turnover below industry average—about 12% vs fintech sector ~20% in 2024.

Cloud and Infrastructure Providers

CAMS (Computer Age Management Services) relies on global cloud providers (AWS, Azure, GCP) for storage and compute, creating moderate vendor dependence; in FY2024 CAMS processed over 1 billion mutual fund transactions, so uptime and scale matter.

The firm’s size gives leverage to win discounts—enterprise cloud deals often cut list prices 30–50%—but migrating petabytes of sensitive financial data is complex and costly, limiting rapid switches.

This technical lock-in and regulatory data residency needs keep cloud vendors in a stable, moderately strong supplier position for CAMS.

Cybersecurity and Compliance Vendors

With India’s RBI and SEBI tightening data rules—RBI’s 2023 operational resilience guidelines and SEBI’s 2024 cyber norms—CAMS must buy certified security stacks (SIEM, EDR, encryption) from specialist vendors to keep licenses; noncompliance fines can exceed ₹100 crore for systemic breaches.

Financial Data Feed Providers

- Essential input: low-latency feeds

- Top vendors: Bloomberg, Refinitiv, major exchanges

- Market share: >70% top-3 (2024)

- Impact: high supplier power → higher costs

Hardware and Networking Equipment Suppliers

Maintaining CAMS’ physical data centers and disaster-recovery sites needs continuous supply of high-performance servers and networking gear; global market size for enterprise servers was $92.5B in 2024, but certified vendors for financial-grade reliability are few.

CAMS reduces supplier power by holding multi-vendor contracts and spares, keeping procurement lead times under 12 weeks and avoiding single-vendor concentration above 25% of spend.

- Enterprise server market: $92.5B (2024)

- Target max single-vendor spend: 25%

- Procurement lead time: ≤12 weeks

- Multiple certified vendors: reduces downtime risk

Supplier power high: talent costs up, market‑data concentrated, CAMS caps risk

Supplier power is moderate-to-high: talent costs rose ~18% YoY (2025), cloud discounts 30–50% offset lock-in, top-3 market-data vendors control >70% (2024), servers market $92.5B (2024); CAMS limits risk with retention (turnover ~12% vs fintech ~20% in 2024), multi-vendor caps (max 25% spend) and ≤12-week lead times.

| Item | Metric |

|---|---|

| Fintech hiring premium | +18% YoY (2025) |

| Market-data share | >70% top‑3 (2024) |

| Server market | $92.5B (2024) |

| Turnover | 12% (CAMS) vs 20% fintech (2024) |

| Cloud discounts | 30–50% enterprise deals |

What is included in the product

Tailored Porter's Five Forces analysis for Computer Age Management Services that uncovers key drivers of competition, buyer and supplier influence, entry barriers, and substitution risks impacting its pricing power and profitability.

One-sheet Porter's Five Forces for CAMS—quickly spot regulatory, competitive, supplier, buyer, and substitute pressures to streamline strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of Asset Management Companies

The Indian mutual fund market is top-heavy: the top 10 AMCs held about 86% of AUM (assets under management) as of Dec 2025, and these clients account for roughly 70% of CAMS's FY2025 revenue, giving them strong fee-negotiation leverage.

Large-volume AMCs push for lower basis-point fees across transfer-agent and transaction services; CAMS needs continuous tech upgrades and SLA improvements to protect gross margins and avoid fee compression.

High Switching Costs for Clients

The migration of decades of investor records and workflows to a new registrar and transfer agent (RTA) can take 6–24 months and cost ₹5–20 crore for a single asset management company (AMC), creating strong operational stickiness that cuts customer bargaining power once onboarded to CAMS.

Risk of data loss or service disruption—seen in industry transition failure rates near 10% in 2023—further deters switching, so retained clients face high effective switching costs and reduced leverage.

Demand for Digital Transformation Tools

Modern customers—distributors and investors—demand sophisticated digital interfaces and real-time reporting, pushing CAMS to boost front-end tech spend; CAMS reported capital expenditure of INR 250–300 crore in FY2024 for technology upgrades.

This pressure compels CAMS to tailor solutions for AMCs aiming to improve end-user experience, increasing switching costs and deepening integration, which offsets some customer bargaining power.

Regulatory Influence on Fee Structures

SEBI's 2024 cap on average total expense ratios (TER) tightened margins: average equity TER fell to 1.75% from 1.95% in 2022, pushing AMCs to demand lower processing fees from RTAs like CAMS during renewals.

Mandated investor-cost cuts give AMCs a formal lever to renegotiate contracts, strengthening buyer power and pressuring CAMS' fee income; in 2024 CAMS reported 6% margin compression in RTA services versus 2022.

- SEBI TER cut: equity funds 1.95%→1.75% (2022→2024)

- AMCs pass savings to RTAs at renewals

- CAMS RTA margin compression ~6% (2024 vs 2022)

- Regulation = legitimized bargaining leverage

Deep Operational Integration

CAMS embeds into an AMC’s operations—handling KYC, SIPs, dividend processing and investor servicing for over 40 of the top 50 mutual funds, linking CAMS uptime and process speed directly to an AMC’s NAV operations and investor flows.

This deep integration creates mutual dependency: AMCs rely on CAMS’ tech and scale while CAMS depends on multi-year service contracts (often 3–5 years) and high switching costs, so power tilts toward cooperative, long-term pricing rather than short-term bargaining.

- Handles KYC, SIP, dividend for 40/50 top funds

- High switching cost: tech, compliance, data migration

- Typical contract: 3–5 years, renewals common

Top AMCs' fee power squeezes RTAs—stickiness offsets TER cuts, margins down ~6%

Buyers (top AMCs) hold strong fee leverage—top 10 AMCs = ~86% AUM (Dec 2025) and ~70% of CAMS FY2025 revenue—pushing lower bps; high switching costs (6–24 months, ₹5–20 crore) and 3–5 year contracts create stickiness that limits bargaining; SEBI TER cut (1.95%→1.75%, 2022→2024) legitimized renegotiation, causing ~6% RTA margin compression (2024 vs 2022).

| Metric | Value |

|---|---|

| Top-10 AMC AUM share (Dec 2025) | 86% |

| CAMS FY2025 rev from top AMCs | ~70% |

| Switch cost per AMC | ₹5–20 crore |

| Switch time | 6–24 months |

| Contract length | 3–5 yrs |

| TER cut (equity) | 1.95%→1.75% (2022→2024) |

| RTA margin change | -6% (2024 vs 2022) |

Same Document Delivered

Computer Age Management Services Porter's Five Forces Analysis

This preview shows the exact Computer Age Management Services Porter's Five Forces Analysis you'll receive—no placeholders or mockups; the full, professionally formatted document is available for instant download after purchase.