Canadian Solar PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our PESTLE Analysis for Canadian Solar reveals how shifting policies, supply-chain economics, and rapid tech advances are reshaping the company’s growth trajectory—insights that investors and strategists can act on immediately. Purchase the full report to access detailed political, economic, social, technological, legal, and environmental implications plus ready-to-use recommendations. Buy now for instant strategic clarity.

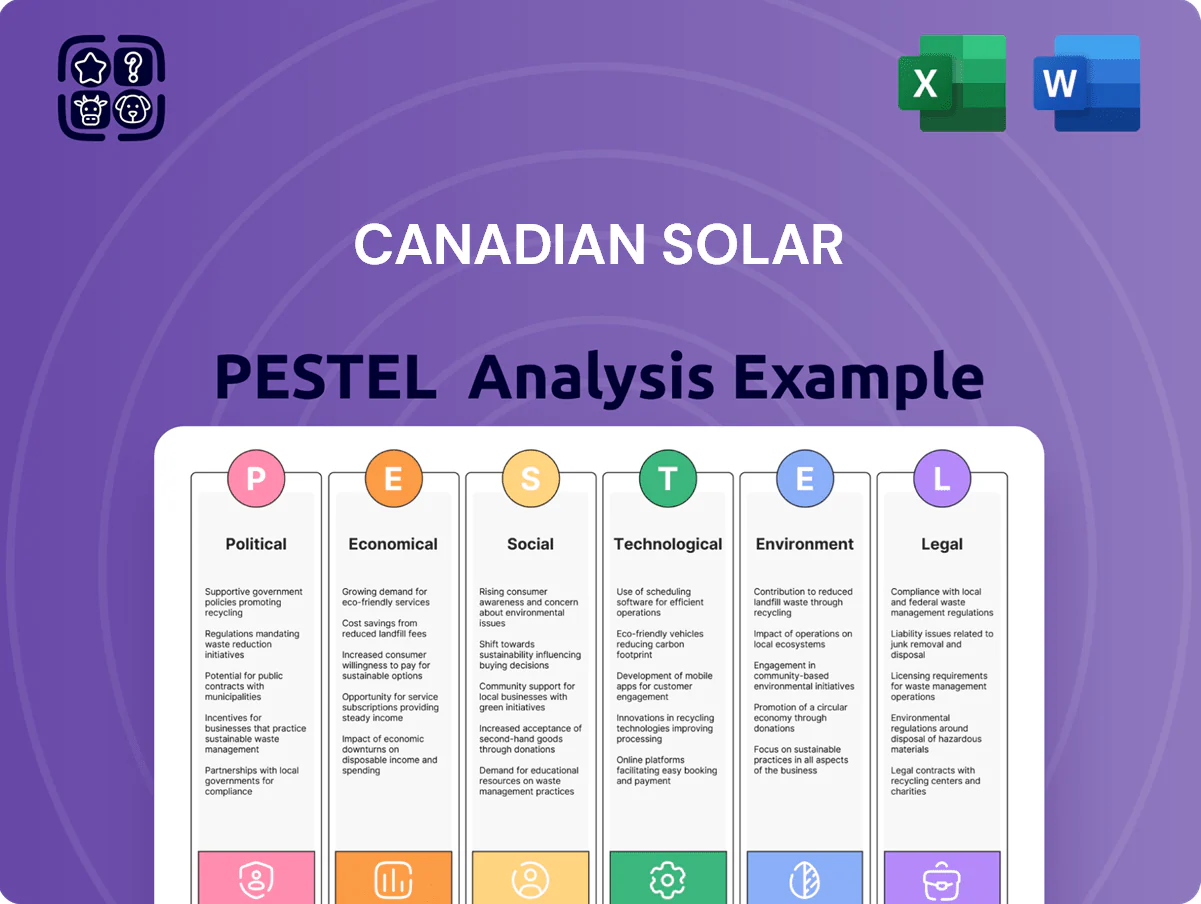

Political factors

Geopolitical Trade Tensions

Ongoing Western-China trade disputes have raised tariffs on imported solar cells/modules up to 250% in some US antidumping/countervailing cases, pressuring Canadian Solar's supply chain and gross margins (Q4 2025 guidance noted margin compression industry-wide).

Higher duties push Canadian Solar toward localized manufacturing: US & SE Asia expansions (e.g., planned US module capacity expansions announced 2024–25) to mitigate tariffs and FX risks.

Navigating protectionist policies is vital to protect share in high-value democratic markets where ~60–70% of global project tender value is concentrated, affecting revenue mix and pricing strategy.

Incentive Programs and Subsidies

The US Inflation Reduction Act continues to provide up to 30% investment tax credits and production incentives that supported over US$62bn in clean energy tax credits in 2024, bolstering Canadian Solar’s project development pipeline; EU green subsidy schemes (eg. REPowerEU) and Southeast Asian auctions—Philippines 2024 solar tenders reaching 2.5 GW—similarly drive utility-scale demand. Canadian Solar must map expansion to these fiscal regimes to retain competitiveness and leverage projected regional CAPEX flows.

Energy Security Priorities

Global shifts toward energy independence have elevated solar to national security: 64% of G20 countries now list renewables in energy strategy documents (IEA 2024), boosting demand for suppliers like Canadian Solar. Governments prioritizing domestic generation to cut reliance on fossil imports — global fossil fuel price volatility rose 38% in 2022–24 — favors long-term public tenders. This political climate supports Canadian Solar securing multi-year government and utility contracts, contributing to its FY2024 revenue mix where project sales grew 22% year-over-year.

Localization of Manufacturing Mandates

Many countries now require local content to access solar incentives, pushing suppliers to build domestic factories; Canadian Solar opened a 1.2 GW module plant in Texas (operational 2024) and other regional facilities to meet such mandates and qualify for US and EU support.

Domestic production raises unit costs—US cell/module manufacturing can be 10–20% higher than Asian supply chains—but secures tariff exemptions, tax credits and project eligibility that protect revenue and market access.

Balancing ~USD 50–150 million in capex per large plant versus long-term contract wins and incentives is a core strategic trade-off for Canadian Solar as political localization spreads.

- 2024: 1.2 GW Texas plant operational

- Domestic costs ~10–20% above Asia

- Capex per large plant ~USD 50–150M

- Local content enables tariff/exemption access and incentive eligibility

Global Climate Commitments

The reinforcement of agreements like the Paris Accord drives national net-zero targets; as of 2025, over 140 countries have net-zero pledges covering 88% of global emissions, sustaining demand for renewables.

Such mandates underpin regular renewable auctions and procurement programs—Canada, EU and India held >$60B combined utility-scale solar tenders in 2024–25—favoring global suppliers like Canadian Solar.

Canadian Solar depends on policy stability to justify heavy R&D and capex; the company invested ≈$120M in R&D in 2024 and announced multi-year manufacturing expansions tied to long-term offtake signals.

- 140+ countries with net-zero pledges (covers 88% of emissions)

- $60B+ utility-scale solar tenders in 2024–25 (Canada, EU, India)

- Canadian Solar R&D ≈$120M in 2024; capex linked to policy stability

Tariffs Drive Canadian Solar to Texas: Local Builds, Higher Costs, IRA-Driven Demand

Tariffs and protectionism (US antidumping up to 250%) force Canadian Solar into localized manufacturing (1.2 GW Texas plant operational 2024) to secure IRA credits (up to 30%) and tender eligibility; domestic costs rise ~10–20% vs Asia, capex per plant ~$50–150M, but policy-driven tenders and net-zero commitments (140+ countries) sustain long-term demand.

| Metric | Value |

|---|---|

| US tariff peak | 250% |

| Texas plant | 1.2 GW (2024) |

| Domestic cost premium | 10–20% |

| Capex/plant | USD 50–150M |

What is included in the product

Explores how macro-environmental forces uniquely affect Canadian Solar across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

Condenses Canadian Solar's PESTLE into a sharp, easily shareable summary that teams can drop into presentations or planning sessions to quickly align on regulatory, economic, and technological risks and opportunities.

Economic factors

Interest Rate Environment

Persistent high interest rates through 2025 pushed Canada and US policy rates above 4.5–5%, raising weighted average cost of capital for utility-scale solar; finance costs for projects increased by an estimated 150–250 bps versus 2021 levels, squeezing IRRs. Higher borrowing costs have led to reported postponements of projects industry-wide, with some developers delaying >20% of pipelines when IRRs fell below target thresholds. Canadian Solar must deploy hedging, mezzanine debt, tax equity and captive financing to protect margins and sustain its ~8–12% project IRR targets.

Raw Material Price Volatility

Fluctuations in polysilicon, silver and solar glass prices directly squeeze Canadian Solar’s module margins; polysilicon rose ~15% in 2024 vs 2023 and silver averaged ~28 USD/oz in 2024, increasing input costs. Supply-chain bottlenecks have eased since 2022, but a sudden commodity spike could cut EBITDA margins materially. Vertical integration and multi-year supply contracts remain critical to stabilize costs and protect 2025 guidance.

Currency Exchange Fluctuations

Operating across 20+ countries, Canadian Solar faces material FX exposure to USD/CNY and EUR/USD; in 2025 FX movements contributed roughly a $45m non-cash loss recognized in FY2024, illustrating how swings can distort EBITDA comparability.

The company reported hedging coverage of over 60% of near-term receivables in 2024, using forwards and options to mitigate translation and transaction risk.

Global Energy Demand Cycles

Economic growth in China and India drives demand for new generation; China added about 85 GW of solar in 2023 and India targeted 500 GW renewables by 2030, shaping capacity needs for Canadian Solar.

Economic slowdowns cut industrial power use and can delay renewables investment—global GDP growth fell to ~3.0% in 2023, pressuring project development pipelines.

Rapid urbanization in emerging markets (urban population in India rising to ~35% by 2030) supports long-term solar adoption and revenue growth potential.

- China 85 GW solar added in 2023

- India 500 GW renewables target by 2030

- Global GDP ~3.0% in 2023

Cost Competitiveness of Solar

Falling LCOE for utility-scale solar reached roughly US$28–35/MWh in 2024 globally, making solar the cheapest source of new power in many regions and enabling Canadian Solar to outcompete coal and gas on price without relying solely on subsidies.

Canadian Solar’s margin and project economics benefit from this cost edge, but sustaining leadership requires continuing module efficiency gains and BOS cost reductions as gas and coal decarbonization technologies and storage costs also improve.

- Global utility-scale solar LCOE ~US$28–35/MWh (2024)

- Allows competitive bidding vs coal/gas without subsidies

- Ongoing tech and BOS improvements needed to preserve price lead

Rising rates, material costs and FX dent solar margins — LCOE still competitive

High policy rates (US/CAN ~4.5–5% in 2025) raised project financing costs ~150–250 bps vs 2021, pressuring IRRs; polysilicon +15% in 2024 and silver ~28 USD/oz raised module costs; FX volatility caused a ~$45m FY2024 non‑cash loss; global solar LCOE ~US$28–35/MWh (2024) preserves competitiveness but margins need vertical integration and hedging to sustain.

| Metric | Value |

|---|---|

| Policy rates (US/CAN 2025) | 4.5–5% |

| Financing cost rise vs 2021 | +150–250 bps |

| Polysilicon (2024 vs 2023) | +15% |

| Silver (2024 avg) | ~28 USD/oz |

| FX non‑cash loss (FY2024) | ~$45m |

| Global utility LCOE (2024) | US$28–35/MWh |

Full Version Awaits

Canadian Solar PESTLE Analysis

The preview shown here is the exact Canadian Solar PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Our PESTLE Analysis for Canadian Solar reveals how shifting policies, supply-chain economics, and rapid tech advances are reshaping the company’s growth trajectory—insights that investors and strategists can act on immediately. Purchase the full report to access detailed political, economic, social, technological, legal, and environmental implications plus ready-to-use recommendations. Buy now for instant strategic clarity.

Political factors

Geopolitical Trade Tensions

Ongoing Western-China trade disputes have raised tariffs on imported solar cells/modules up to 250% in some US antidumping/countervailing cases, pressuring Canadian Solar's supply chain and gross margins (Q4 2025 guidance noted margin compression industry-wide).

Higher duties push Canadian Solar toward localized manufacturing: US & SE Asia expansions (e.g., planned US module capacity expansions announced 2024–25) to mitigate tariffs and FX risks.

Navigating protectionist policies is vital to protect share in high-value democratic markets where ~60–70% of global project tender value is concentrated, affecting revenue mix and pricing strategy.

Incentive Programs and Subsidies

The US Inflation Reduction Act continues to provide up to 30% investment tax credits and production incentives that supported over US$62bn in clean energy tax credits in 2024, bolstering Canadian Solar’s project development pipeline; EU green subsidy schemes (eg. REPowerEU) and Southeast Asian auctions—Philippines 2024 solar tenders reaching 2.5 GW—similarly drive utility-scale demand. Canadian Solar must map expansion to these fiscal regimes to retain competitiveness and leverage projected regional CAPEX flows.

Energy Security Priorities

Global shifts toward energy independence have elevated solar to national security: 64% of G20 countries now list renewables in energy strategy documents (IEA 2024), boosting demand for suppliers like Canadian Solar. Governments prioritizing domestic generation to cut reliance on fossil imports — global fossil fuel price volatility rose 38% in 2022–24 — favors long-term public tenders. This political climate supports Canadian Solar securing multi-year government and utility contracts, contributing to its FY2024 revenue mix where project sales grew 22% year-over-year.

Localization of Manufacturing Mandates

Many countries now require local content to access solar incentives, pushing suppliers to build domestic factories; Canadian Solar opened a 1.2 GW module plant in Texas (operational 2024) and other regional facilities to meet such mandates and qualify for US and EU support.

Domestic production raises unit costs—US cell/module manufacturing can be 10–20% higher than Asian supply chains—but secures tariff exemptions, tax credits and project eligibility that protect revenue and market access.

Balancing ~USD 50–150 million in capex per large plant versus long-term contract wins and incentives is a core strategic trade-off for Canadian Solar as political localization spreads.

- 2024: 1.2 GW Texas plant operational

- Domestic costs ~10–20% above Asia

- Capex per large plant ~USD 50–150M

- Local content enables tariff/exemption access and incentive eligibility

Global Climate Commitments

The reinforcement of agreements like the Paris Accord drives national net-zero targets; as of 2025, over 140 countries have net-zero pledges covering 88% of global emissions, sustaining demand for renewables.

Such mandates underpin regular renewable auctions and procurement programs—Canada, EU and India held >$60B combined utility-scale solar tenders in 2024–25—favoring global suppliers like Canadian Solar.

Canadian Solar depends on policy stability to justify heavy R&D and capex; the company invested ≈$120M in R&D in 2024 and announced multi-year manufacturing expansions tied to long-term offtake signals.

- 140+ countries with net-zero pledges (covers 88% of emissions)

- $60B+ utility-scale solar tenders in 2024–25 (Canada, EU, India)

- Canadian Solar R&D ≈$120M in 2024; capex linked to policy stability

Tariffs Drive Canadian Solar to Texas: Local Builds, Higher Costs, IRA-Driven Demand

Tariffs and protectionism (US antidumping up to 250%) force Canadian Solar into localized manufacturing (1.2 GW Texas plant operational 2024) to secure IRA credits (up to 30%) and tender eligibility; domestic costs rise ~10–20% vs Asia, capex per plant ~$50–150M, but policy-driven tenders and net-zero commitments (140+ countries) sustain long-term demand.

| Metric | Value |

|---|---|

| US tariff peak | 250% |

| Texas plant | 1.2 GW (2024) |

| Domestic cost premium | 10–20% |

| Capex/plant | USD 50–150M |

What is included in the product

Explores how macro-environmental forces uniquely affect Canadian Solar across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

Condenses Canadian Solar's PESTLE into a sharp, easily shareable summary that teams can drop into presentations or planning sessions to quickly align on regulatory, economic, and technological risks and opportunities.

Economic factors

Interest Rate Environment

Persistent high interest rates through 2025 pushed Canada and US policy rates above 4.5–5%, raising weighted average cost of capital for utility-scale solar; finance costs for projects increased by an estimated 150–250 bps versus 2021 levels, squeezing IRRs. Higher borrowing costs have led to reported postponements of projects industry-wide, with some developers delaying >20% of pipelines when IRRs fell below target thresholds. Canadian Solar must deploy hedging, mezzanine debt, tax equity and captive financing to protect margins and sustain its ~8–12% project IRR targets.

Raw Material Price Volatility

Fluctuations in polysilicon, silver and solar glass prices directly squeeze Canadian Solar’s module margins; polysilicon rose ~15% in 2024 vs 2023 and silver averaged ~28 USD/oz in 2024, increasing input costs. Supply-chain bottlenecks have eased since 2022, but a sudden commodity spike could cut EBITDA margins materially. Vertical integration and multi-year supply contracts remain critical to stabilize costs and protect 2025 guidance.

Currency Exchange Fluctuations

Operating across 20+ countries, Canadian Solar faces material FX exposure to USD/CNY and EUR/USD; in 2025 FX movements contributed roughly a $45m non-cash loss recognized in FY2024, illustrating how swings can distort EBITDA comparability.

The company reported hedging coverage of over 60% of near-term receivables in 2024, using forwards and options to mitigate translation and transaction risk.

Global Energy Demand Cycles

Economic growth in China and India drives demand for new generation; China added about 85 GW of solar in 2023 and India targeted 500 GW renewables by 2030, shaping capacity needs for Canadian Solar.

Economic slowdowns cut industrial power use and can delay renewables investment—global GDP growth fell to ~3.0% in 2023, pressuring project development pipelines.

Rapid urbanization in emerging markets (urban population in India rising to ~35% by 2030) supports long-term solar adoption and revenue growth potential.

- China 85 GW solar added in 2023

- India 500 GW renewables target by 2030

- Global GDP ~3.0% in 2023

Cost Competitiveness of Solar

Falling LCOE for utility-scale solar reached roughly US$28–35/MWh in 2024 globally, making solar the cheapest source of new power in many regions and enabling Canadian Solar to outcompete coal and gas on price without relying solely on subsidies.

Canadian Solar’s margin and project economics benefit from this cost edge, but sustaining leadership requires continuing module efficiency gains and BOS cost reductions as gas and coal decarbonization technologies and storage costs also improve.

- Global utility-scale solar LCOE ~US$28–35/MWh (2024)

- Allows competitive bidding vs coal/gas without subsidies

- Ongoing tech and BOS improvements needed to preserve price lead

Rising rates, material costs and FX dent solar margins — LCOE still competitive

High policy rates (US/CAN ~4.5–5% in 2025) raised project financing costs ~150–250 bps vs 2021, pressuring IRRs; polysilicon +15% in 2024 and silver ~28 USD/oz raised module costs; FX volatility caused a ~$45m FY2024 non‑cash loss; global solar LCOE ~US$28–35/MWh (2024) preserves competitiveness but margins need vertical integration and hedging to sustain.

| Metric | Value |

|---|---|

| Policy rates (US/CAN 2025) | 4.5–5% |

| Financing cost rise vs 2021 | +150–250 bps |

| Polysilicon (2024 vs 2023) | +15% |

| Silver (2024 avg) | ~28 USD/oz |

| FX non‑cash loss (FY2024) | ~$45m |

| Global utility LCOE (2024) | US$28–35/MWh |

Full Version Awaits

Canadian Solar PESTLE Analysis

The preview shown here is the exact Canadian Solar PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for decision-making.