Canadian Tire Corporation PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our PESTLE Analysis of Canadian Tire Corporation reveals how political regulation, shifting consumer spending, tech-driven retail trends, environmental obligations, and competitive legal pressures converge to shape its strategic outlook—essential reading for investors and strategists. Purchase the full report for a complete, actionable breakdown in editable formats and make smarter, faster decisions.

Political factors

Trade Policy and Cross-Border Tariffs

As of late 2025, Canada’s trade ties—notably with the US (goods trade CA$1.1 trillion in 2024) and China (CA$119 billion in 2024)—directly shape Canadian Tire’s procurement strategy, prompting focus on tariff exposure across automotive and hardware lines.

Potential tariff changes or renegotiated regional deals could raise landed costs by an estimated 2–6%, forcing agile supply-chain shifts to preserve retail margins (gross margin 2024: 24.1%).

Canadian Tire closely monitors geopolitical developments, sourcing alternatives and inventory buffers to limit disruptions from international manufacturers and protect EBITDA, which was CA$1.2 billion in FY2024.

Federal Carbon Pricing and Climate Policy

The federal plan to raise the carbon price to CAD 170/tonne by 2030, with stepped increases through 2025, raises fuel and transport costs for Canadian Tire’s logistics and gasoline retailing, potentially adding millions to operating expenses given the company sold ~2.1 billion litres of fuel in 2024. This accelerates capital allocation toward fleet electrification and efficiency; Canadian Tire’s FY2024 capex of CAD 1.1 billion may increasingly target low-carbon vehicles and station upgrades. Aligning with national targets reduces regulatory risk and supports brand reputation amid rising consumer demand for greener retailers.

Labor and Minimum Wage Regulations

Provincial minimum wage hikes—Ontario to C$16.55/hr and Alberta to C$15.00/hr in 2025—along with strengthened labor protections raised Canadian Tire’s labor cost pressure; labor expense represented about 24% of retail operating costs in 2024 for comparable retailers. Canadian Tire must balance competitive pay across banners (retail, automotive, financial services) while preserving operating margin—net margin was ~3.1% in FY2024. Ongoing employment-standards updates require continuous compliance monitoring to avoid fines and manage staffing efficiency in a high-service model.

Supply Chain Geopolitics

Geopolitical instability in hubs like China and Southeast Asia has pushed Canadian Tire to diversify suppliers; by 2024 the retailer increased non-China sourced imports by ~15% to reduce stockout risk after 2021–22 disruptions.

Federal and provincial incentives for domestic production and friend-shoring—including CEBA-linked grants and Ontario's manufacturing tax credits—are steering capital expenditures toward local tooling and warehousing investments.

Maintaining resilient supply chains is a political priority: Canadian Tire targets inventory-improvement metrics, aiming to cut stockout-related lost sales from an estimated CAD 200–300 million in 2021–22 through higher safety stock and regional distribution capacity.

- Diversified sourcing: +15% non-China imports (2024)

- Policy drivers: federal/provincial incentives, manufacturing tax credits

- Financial impact: CAD 200–300m estimated lost sales (2021–22)

- Actions: increased safety stock, regional warehousing investments

Government Infrastructure and Transit Spending

Federal and provincial investments in transportation—Canada’s 2024 Investing in Canada Plan commitments of over CAD 120 billion through 2031—boost demand for automotive products and services, supporting Canadian Tire’s core auto segment.

Improved road networks and a national push to add 50,000+ EV chargers by 2027 create opportunities for Canadian Tire to expand EV charging, maintenance, and parts offerings.

Canadian Tire partners with governments and municipalities to integrate stores into community transit and service hubs, enhancing foot traffic and service revenue; company Q3 2025 retail segment sales rose 6.2% year-over-year, reflecting infrastructure-driven demand.

- Federal/provincial transport capex: CAD 120B+ (2024–2031)

- Target EV chargers: 50,000+ by 2027

- Canadian Tire retail sales growth Q3 2025: +6.2% YoY

Trade shifts, carbon costs & capex reshape Canadian supply chains and logistics

Political factors—trade exposure to US (goods trade CA$1.1T 2024) and China (CA$119B 2024), carbon price rise to CAD170/tonne by 2030, provincial minimum wages (Ontario C$16.55, Alberta C$15.00 in 2025), increased non-China sourcing (+15% 2024), federal transport capex CAD120B+ (2024–31)—drive sourcing shifts, higher logistics/labor costs, capex for electrification and regional warehousing.

| Metric | Value |

|---|---|

| US goods trade 2024 | CA$1.1T |

| China goods trade 2024 | CA$119B |

| Carbon price target 2030 | CAD170/tonne |

| Non-China sourcing increase 2024 | +15% |

| Federal transport capex | CAD120B+ |

What is included in the product

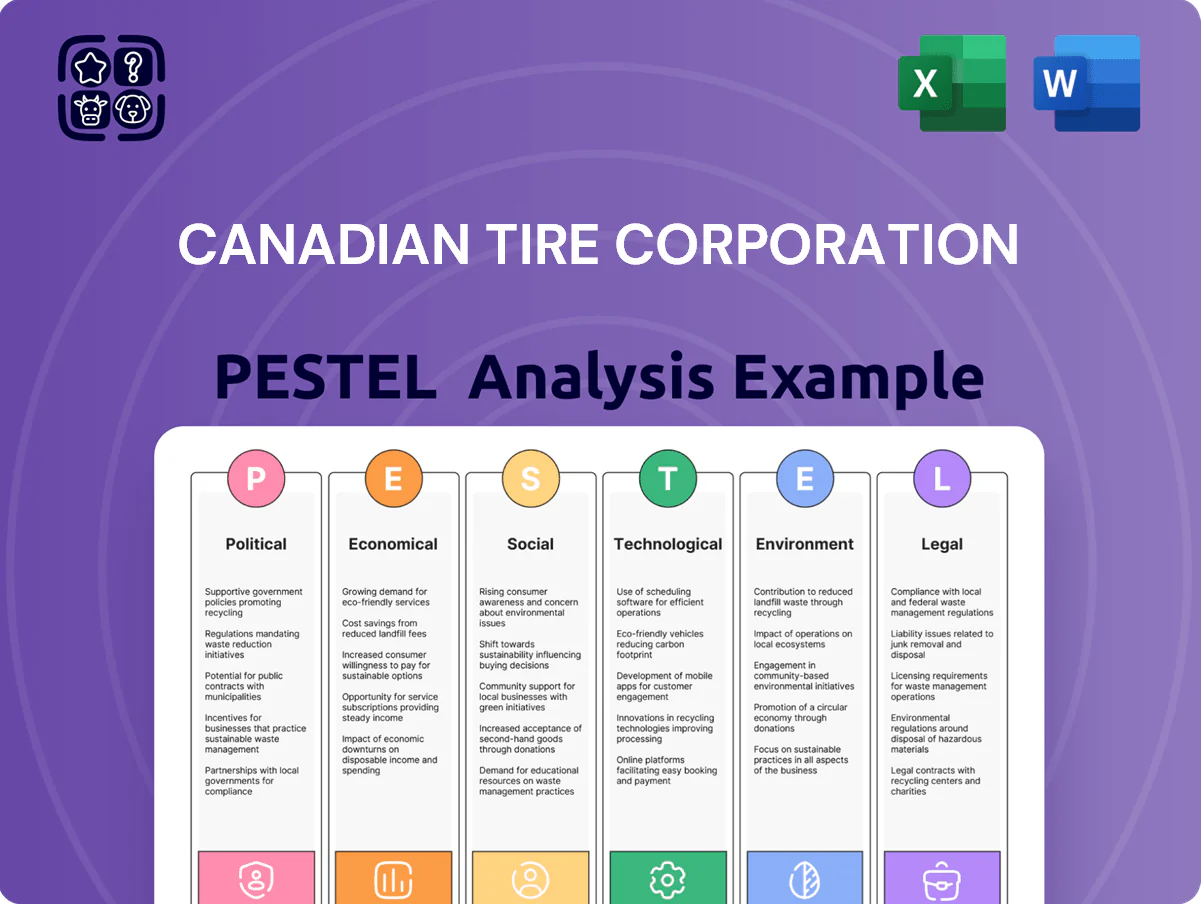

Explores how external macro-environmental factors uniquely affect Canadian Tire Corporation across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE snapshot for Canadian Tire that highlights external risks and opportunities—ready to drop into presentations, shared across teams, and annotated with region- or business-line notes to streamline planning and decision-making.

Economic factors

Monetary Policy and Interest Rate Environment

The lagged impact of mortgage resets—roughly 25% of outstanding mortgages repricing through 2024–25—compresses disposable income for middle-class households, the retailer's core customer base.

Management must fine-tune promotional financing and credit terms to sustain sales while keeping provisions for credit losses in check; Canadian Tire Bank reported a 2024 provision ratio near 0.9%.)

Inflationary Pressures on Operating Costs

Persistent inflation in raw materials and global shipping—container rates up ~30% from 2020 levels and Canada CPI averaging 3.4% in 2024—pressures Canadian Tire’s ability to keep low price points, raising input and logistics costs across retail and auto segments.

Canadian Tire leverages scale and private-label brands like MotoMaster and Canvas, which drove private-label penetration gains to ~18% of merchandise sales in FY2024, to offer value options for consumers facing higher living costs.

Effective price optimization, category-level markdown management and cost-containment across supply chain and SG&A are critical to protect consolidated adjusted EBITDA margins, which were 9.8% in FY2024 and vulnerable to sustained inflationary shocks.

Canadian Dollar Currency Volatility

Fluctuations in the Canadian dollar versus the US dollar materially affect Canadian Tire’s import costs, with the loonie sliding ~6% in 2024 vs USD, raising landed costs across retail banners. The company uses hedging programs—forward contracts and options—to offset exposure; Canadian Tire reported FX-linked gross margin variability in FY2024. Analysts track FX moves closely since a 1% CAD weakening can raise COGS materially and compress retail margins.

Household Debt and Credit Risk

High household debt in Canada—household debt-to-disposable-income ratio ~176% in Q3 2025—threatens Canadian Tire’s retail sales as consumers cut discretionary spend on items like seasonal decor and premium sporting goods.

Elevated debt raises credit risk for Canadian Tire Bank; maintaining strict credit scoring and higher provisioning is critical as household insolvency filings rose 8% year-over-year in 2024.

Housing Market Trends and DIY Demand

As of 2025 the Canadian housing market shows stronger renovation activity versus new builds, with Statistics Canada reporting renovation spending up ~4.5% YoY in 2024 and CMHC noting a slower new-home starts recovery; this shifts demand toward hardware and home categories that benefit Canadian Tire.

Housing affordability pressures persist—median house prices remained ~6% above pre-2020 levels in 2024—prompting homeowners to upgrade existing properties and sustaining steady DIY purchases for tools, fixtures and seasonal products.

This renovation-driven demand underpins Canadian Tire’s Living and Fixing pillars, reflected in FY2024 retail sales growth in home and automotive categories, helping stabilize margins amid retail headwinds.

- Renovation spending +4.5% YoY in 2024 (Statistics Canada)

- Median house prices ~6% above 2019 levels (2024)

- FY2024 home/automotive sales growth supported Living and Fixing

Rising rates squeeze spending but boost Canadian Tire Bank; renovations and private label shore sales

Interest rates ~4.5–5.0% (end-2025) squeeze discretionary spend and boost Canadian Tire Bank NIMs; mortgage resets (~25% through 2024–25) lower household disposable income. Inflation (CPI ~3.4% in 2024) and +30% container rates since 2020 raise input/logistics costs, while private-label penetration ~18% (FY2024) and renovation spending +4.5% (2024) support core categories.

| Metric | Value |

|---|---|

| Policy rate (end-2025) | 4.5–5.0% |

| CPI (2024) | 3.4% |

| Private-label share (FY2024) | ~18% |

| Renovation spend (2024) | +4.5% YoY |

Same Document Delivered

Canadian Tire Corporation PESTLE Analysis

The preview shown here is the exact Canadian Tire Corporation PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and insights visible in this sample are the final file you’ll download instantly after checkout, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Our PESTLE Analysis of Canadian Tire Corporation reveals how political regulation, shifting consumer spending, tech-driven retail trends, environmental obligations, and competitive legal pressures converge to shape its strategic outlook—essential reading for investors and strategists. Purchase the full report for a complete, actionable breakdown in editable formats and make smarter, faster decisions.

Political factors

Trade Policy and Cross-Border Tariffs

As of late 2025, Canada’s trade ties—notably with the US (goods trade CA$1.1 trillion in 2024) and China (CA$119 billion in 2024)—directly shape Canadian Tire’s procurement strategy, prompting focus on tariff exposure across automotive and hardware lines.

Potential tariff changes or renegotiated regional deals could raise landed costs by an estimated 2–6%, forcing agile supply-chain shifts to preserve retail margins (gross margin 2024: 24.1%).

Canadian Tire closely monitors geopolitical developments, sourcing alternatives and inventory buffers to limit disruptions from international manufacturers and protect EBITDA, which was CA$1.2 billion in FY2024.

Federal Carbon Pricing and Climate Policy

The federal plan to raise the carbon price to CAD 170/tonne by 2030, with stepped increases through 2025, raises fuel and transport costs for Canadian Tire’s logistics and gasoline retailing, potentially adding millions to operating expenses given the company sold ~2.1 billion litres of fuel in 2024. This accelerates capital allocation toward fleet electrification and efficiency; Canadian Tire’s FY2024 capex of CAD 1.1 billion may increasingly target low-carbon vehicles and station upgrades. Aligning with national targets reduces regulatory risk and supports brand reputation amid rising consumer demand for greener retailers.

Labor and Minimum Wage Regulations

Provincial minimum wage hikes—Ontario to C$16.55/hr and Alberta to C$15.00/hr in 2025—along with strengthened labor protections raised Canadian Tire’s labor cost pressure; labor expense represented about 24% of retail operating costs in 2024 for comparable retailers. Canadian Tire must balance competitive pay across banners (retail, automotive, financial services) while preserving operating margin—net margin was ~3.1% in FY2024. Ongoing employment-standards updates require continuous compliance monitoring to avoid fines and manage staffing efficiency in a high-service model.

Supply Chain Geopolitics

Geopolitical instability in hubs like China and Southeast Asia has pushed Canadian Tire to diversify suppliers; by 2024 the retailer increased non-China sourced imports by ~15% to reduce stockout risk after 2021–22 disruptions.

Federal and provincial incentives for domestic production and friend-shoring—including CEBA-linked grants and Ontario's manufacturing tax credits—are steering capital expenditures toward local tooling and warehousing investments.

Maintaining resilient supply chains is a political priority: Canadian Tire targets inventory-improvement metrics, aiming to cut stockout-related lost sales from an estimated CAD 200–300 million in 2021–22 through higher safety stock and regional distribution capacity.

- Diversified sourcing: +15% non-China imports (2024)

- Policy drivers: federal/provincial incentives, manufacturing tax credits

- Financial impact: CAD 200–300m estimated lost sales (2021–22)

- Actions: increased safety stock, regional warehousing investments

Government Infrastructure and Transit Spending

Federal and provincial investments in transportation—Canada’s 2024 Investing in Canada Plan commitments of over CAD 120 billion through 2031—boost demand for automotive products and services, supporting Canadian Tire’s core auto segment.

Improved road networks and a national push to add 50,000+ EV chargers by 2027 create opportunities for Canadian Tire to expand EV charging, maintenance, and parts offerings.

Canadian Tire partners with governments and municipalities to integrate stores into community transit and service hubs, enhancing foot traffic and service revenue; company Q3 2025 retail segment sales rose 6.2% year-over-year, reflecting infrastructure-driven demand.

- Federal/provincial transport capex: CAD 120B+ (2024–2031)

- Target EV chargers: 50,000+ by 2027

- Canadian Tire retail sales growth Q3 2025: +6.2% YoY

Trade shifts, carbon costs & capex reshape Canadian supply chains and logistics

Political factors—trade exposure to US (goods trade CA$1.1T 2024) and China (CA$119B 2024), carbon price rise to CAD170/tonne by 2030, provincial minimum wages (Ontario C$16.55, Alberta C$15.00 in 2025), increased non-China sourcing (+15% 2024), federal transport capex CAD120B+ (2024–31)—drive sourcing shifts, higher logistics/labor costs, capex for electrification and regional warehousing.

| Metric | Value |

|---|---|

| US goods trade 2024 | CA$1.1T |

| China goods trade 2024 | CA$119B |

| Carbon price target 2030 | CAD170/tonne |

| Non-China sourcing increase 2024 | +15% |

| Federal transport capex | CAD120B+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Canadian Tire Corporation across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE snapshot for Canadian Tire that highlights external risks and opportunities—ready to drop into presentations, shared across teams, and annotated with region- or business-line notes to streamline planning and decision-making.

Economic factors

Monetary Policy and Interest Rate Environment

The lagged impact of mortgage resets—roughly 25% of outstanding mortgages repricing through 2024–25—compresses disposable income for middle-class households, the retailer's core customer base.

Management must fine-tune promotional financing and credit terms to sustain sales while keeping provisions for credit losses in check; Canadian Tire Bank reported a 2024 provision ratio near 0.9%.)

Inflationary Pressures on Operating Costs

Persistent inflation in raw materials and global shipping—container rates up ~30% from 2020 levels and Canada CPI averaging 3.4% in 2024—pressures Canadian Tire’s ability to keep low price points, raising input and logistics costs across retail and auto segments.

Canadian Tire leverages scale and private-label brands like MotoMaster and Canvas, which drove private-label penetration gains to ~18% of merchandise sales in FY2024, to offer value options for consumers facing higher living costs.

Effective price optimization, category-level markdown management and cost-containment across supply chain and SG&A are critical to protect consolidated adjusted EBITDA margins, which were 9.8% in FY2024 and vulnerable to sustained inflationary shocks.

Canadian Dollar Currency Volatility

Fluctuations in the Canadian dollar versus the US dollar materially affect Canadian Tire’s import costs, with the loonie sliding ~6% in 2024 vs USD, raising landed costs across retail banners. The company uses hedging programs—forward contracts and options—to offset exposure; Canadian Tire reported FX-linked gross margin variability in FY2024. Analysts track FX moves closely since a 1% CAD weakening can raise COGS materially and compress retail margins.

Household Debt and Credit Risk

High household debt in Canada—household debt-to-disposable-income ratio ~176% in Q3 2025—threatens Canadian Tire’s retail sales as consumers cut discretionary spend on items like seasonal decor and premium sporting goods.

Elevated debt raises credit risk for Canadian Tire Bank; maintaining strict credit scoring and higher provisioning is critical as household insolvency filings rose 8% year-over-year in 2024.

Housing Market Trends and DIY Demand

As of 2025 the Canadian housing market shows stronger renovation activity versus new builds, with Statistics Canada reporting renovation spending up ~4.5% YoY in 2024 and CMHC noting a slower new-home starts recovery; this shifts demand toward hardware and home categories that benefit Canadian Tire.

Housing affordability pressures persist—median house prices remained ~6% above pre-2020 levels in 2024—prompting homeowners to upgrade existing properties and sustaining steady DIY purchases for tools, fixtures and seasonal products.

This renovation-driven demand underpins Canadian Tire’s Living and Fixing pillars, reflected in FY2024 retail sales growth in home and automotive categories, helping stabilize margins amid retail headwinds.

- Renovation spending +4.5% YoY in 2024 (Statistics Canada)

- Median house prices ~6% above 2019 levels (2024)

- FY2024 home/automotive sales growth supported Living and Fixing

Rising rates squeeze spending but boost Canadian Tire Bank; renovations and private label shore sales

Interest rates ~4.5–5.0% (end-2025) squeeze discretionary spend and boost Canadian Tire Bank NIMs; mortgage resets (~25% through 2024–25) lower household disposable income. Inflation (CPI ~3.4% in 2024) and +30% container rates since 2020 raise input/logistics costs, while private-label penetration ~18% (FY2024) and renovation spending +4.5% (2024) support core categories.

| Metric | Value |

|---|---|

| Policy rate (end-2025) | 4.5–5.0% |

| CPI (2024) | 3.4% |

| Private-label share (FY2024) | ~18% |

| Renovation spend (2024) | +4.5% YoY |

Same Document Delivered

Canadian Tire Corporation PESTLE Analysis

The preview shown here is the exact Canadian Tire Corporation PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and insights visible in this sample are the final file you’ll download instantly after checkout, with no placeholders or surprises.