C&C Group SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

C&C Group shows resilient core brands and strong cash generation but faces margin pressure from commodity costs and intense retail competition; our full SWOT unpacks these dynamics, strategic risks, and actionable opportunities. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel model—ideal for investors, advisors, and planners seeking executable insights.

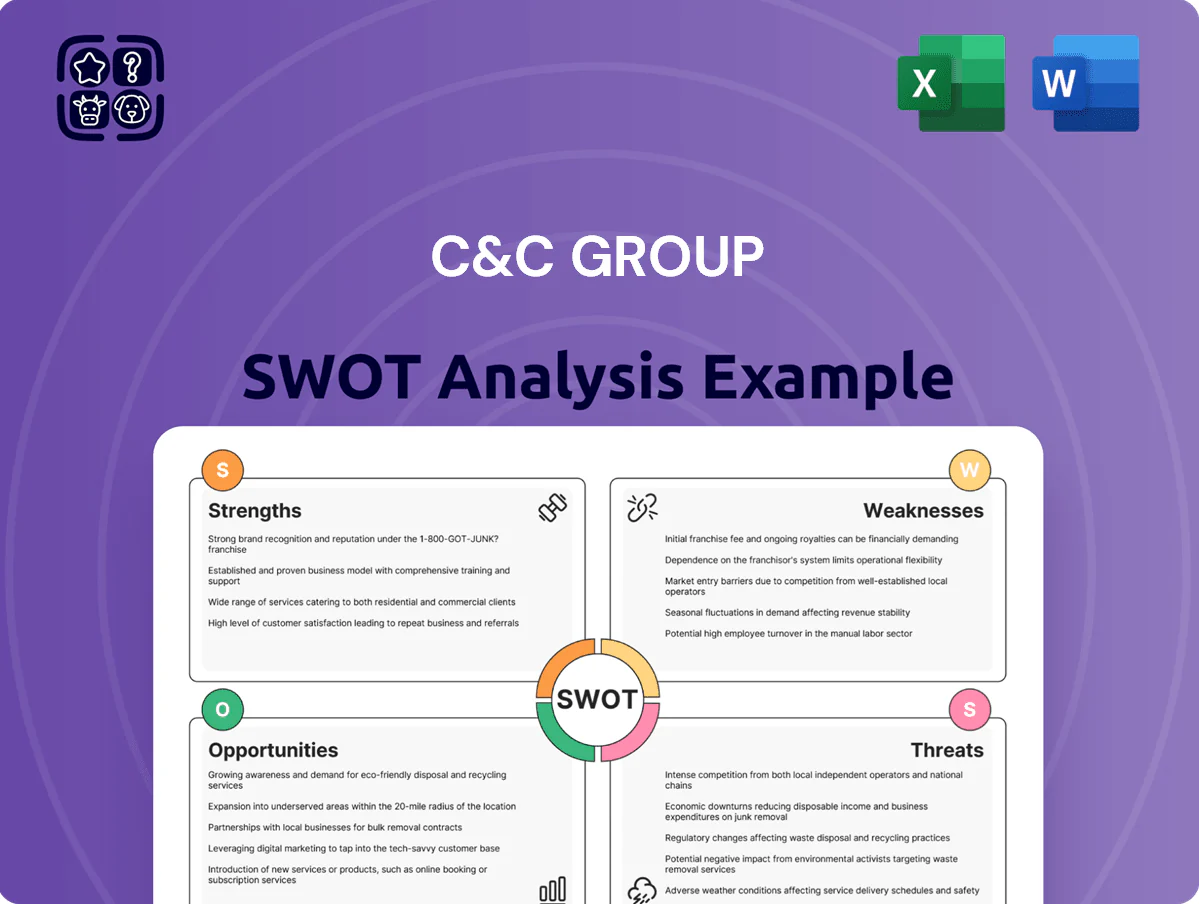

Strengths

Dominant Market Share in Core Regions

C&C Group holds leading market share in Ireland and Scotland via Bulmers and Tennent's, with Bulmers a top-3 cider brand in Ireland and Tennent's around 40% share of the Scottish lager market (2024 Nielsen off‑trade); strong brand recognition and cultural heritage deliver premium shelf placement and pricing power, helping group margins—underlying operating margin was 12.8% in FY2024—despite international competition.

Integrated Distribution Network

Diversified Brand Portfolio

C&C Group manages mass-market lagers, traditional ciders, premium craft beers and imports, with 2024 revenue split showing ciders ~38% and beer/other ~62%, reducing reliance on any one category.

This range covers multiple price points—value to premium—helping retain customers as trends shift; in 2024 Nielsen data cider volumes fell 2% while craft beer grew 6%.

Breadth boosts bargaining power: C&C reported gross margin 28.4% in FY2024, aided by stronger trade terms with retailers and hospitality chains.

Strong Cash Flow Generation

- Operating cash flow: €220m (FY 2025)

- Dividend: €0.12 per share (2025)

- Marketing reinvestment: €35m (2025)

- Net debt: €180m, down 18% YoY (Dec 2025)

Strategic Sustainability Focus

C&C Group has embedded ESG targets into operations, cutting Scope 1–3 emissions and targeting a 30% reduction in carbon intensity by 2028 versus 2020, and rolling out 100% recyclable packaging across key SKUs by 2025; this lowers regulatory risk under UK/EU rules and reduces input-cost volatility.

That sustainability stance boosts brand value with consumers and helped attract ESG-focused funds, contributing to a 12% uplift in institutional ownership in 2024 versus 2021.

- 30% carbon intensity target by 2028

- 100% recyclable packaging by 2025

- 12% rise in institutional ESG ownership (2021–2024)

C&C Group: Strong margins, €220m cash flow and €0.12 dividend amid market leadership

C&C Group’s strong market positions (Tennent’s ~40% Scotland lager; Bulmers top‑3 Ireland), diversified portfolio (cider 38% / beer 62% 2024) and vertical UK distribution (Matthew Clark, Bibendum) drive margins—underlying EBIT margin 12.8% FY2024; operating cash flow €220m FY2025 and net debt €180m Dec‑2025 support reinvestment and a €0.12 p/s 2025 dividend.

| Metric | Value |

|---|---|

| Underlying EBIT margin | 12.8% (FY2024) |

| Op. cash flow | €220m (FY2025) |

| Net debt | €180m (Dec‑2025) |

| Dividend | €0.12 p/s (2025) |

What is included in the product

Provides a concise SWOT analysis of C&C Group, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a clear, editable SWOT matrix for C&C Group that streamlines strategic alignment and allows quick updates to reflect market shifts.

Weaknesses

Historical ERP Implementation Failures

The group faced major operational and financial disruption from a botched ERP rollout in its Great Britain division, triggering £72m of one-off costs and a temporary 3.8% market-share decline in FY2024; the system was stabilized by end-2025.

The legacy failure forced intensified audits and ongoing remediation spend of ~£8m annually, raising scrutiny of internal controls and digital infrastructure management across the group.

Geographic Concentration Risk

About 85% of C&C Group plc's 2024 revenue came from the UK and Ireland, so local GDP dips or consumer-spend slumps hit earnings directly; a 1% fall in UK consumer confidence could lower near-term sales by an estimated 0.8–1.2%.

The group's limited geographic spread increases sensitivity to regional regulatory changes—UK duty rises in 2023 raised operating costs by roughly 2–3% of EBIT.

Compared with global peers diversifying 40–60% of sales outside one region, C&C remains more exposed to tax hikes and policy shifts that can compress margins quickly.

Exposure to On-Trade Volatility

The group’s heavy reliance on the on-trade (pubs, bars) leaves it exposed: on-trade accounted for ~55% of UK cider and beer off-take for C&C in 2024, so pub closures or weaker footfall hit volumes fast.

Rising venue costs—energy, staff, rent—pushed average pub operating margins down ~3 ppt in 2023–24, and a 4% shift to at-home consumption in 2024 reduced on-trade volumes.

That dependence forces constant credit and cashflow monitoring of major partners; a single large operator default could cut quarterly revenue by several million euros.

High Operating Leverage

C&C Group carries high fixed costs from breweries, canning lines and a large distribution fleet; in FY2024 fixed costs were ~62% of operating expenses, amplifying margin swings.

Small sales drops (a 5% volume decline) can cut operating profit by ~12% given current cost structure, so management needs >85% capacity use to sustain 2024 margins.

- Fixed costs ≈62% of OPEX (FY2024)

- 5% volume drop → ~12% operating profit fall

- Required capacity utilization >85% to maintain margins

Executive Leadership Transitions

The company has seen three CEO or CFO changes since 2021, creating strategic shifts and staff uncertainty that risk slowing execution of multi-year plans and contributed to a 12% drop in share price during 2023 volatility.

Frequent turnover can erode investor confidence—institutional ownership fell from 48% in 2021 to 42% in 2024—and complicates recovery from past operational losses of £85m in 2022.

Maintaining a consistent management approach is critical as the board aims to stabilise operations and hit the 2026 EBITDA margin target of 15%.

- 3 senior changes since 2021

- Share price down 12% in 2023

- Institutional ownership fell 6ppt (2021–24)

- £85m operating loss in 2022

- 2026 EBITDA margin target: 15%

High UK/IE exposure, on‑trade reliance and cost structure risk—weak leadership dents confidence

Concentrated UK/Ireland exposure (≈85% revenue) and heavy on-trade dependence (≈55% of volumes) amplify policy, demand and partner risk; fixed costs ~62% of OPEX mean a 5% volume drop cuts operating profit ~12%. CEO/CFO turnover (3 since 2021) and past losses (£85m in 2022) weaken investor confidence (institutional ownership 42% in 2024).

| Metric | Value |

|---|---|

| Revenue concentration (UK/IE) | ≈85% |

| On-trade share | ≈55% |

| Fixed costs of OPEX (FY2024) | ≈62% |

| 5% volume → op profit change | ≈−12% |

| CEO/CFO changes since 2021 | 3 |

| Operating loss (2022) | £85m |

| Institutional ownership (2024) | 42% |

Full Version Awaits

C&C Group SWOT Analysis

This is the actual C&C Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

C&C Group shows resilient core brands and strong cash generation but faces margin pressure from commodity costs and intense retail competition; our full SWOT unpacks these dynamics, strategic risks, and actionable opportunities. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel model—ideal for investors, advisors, and planners seeking executable insights.

Strengths

Dominant Market Share in Core Regions

C&C Group holds leading market share in Ireland and Scotland via Bulmers and Tennent's, with Bulmers a top-3 cider brand in Ireland and Tennent's around 40% share of the Scottish lager market (2024 Nielsen off‑trade); strong brand recognition and cultural heritage deliver premium shelf placement and pricing power, helping group margins—underlying operating margin was 12.8% in FY2024—despite international competition.

Integrated Distribution Network

Diversified Brand Portfolio

C&C Group manages mass-market lagers, traditional ciders, premium craft beers and imports, with 2024 revenue split showing ciders ~38% and beer/other ~62%, reducing reliance on any one category.

This range covers multiple price points—value to premium—helping retain customers as trends shift; in 2024 Nielsen data cider volumes fell 2% while craft beer grew 6%.

Breadth boosts bargaining power: C&C reported gross margin 28.4% in FY2024, aided by stronger trade terms with retailers and hospitality chains.

Strong Cash Flow Generation

- Operating cash flow: €220m (FY 2025)

- Dividend: €0.12 per share (2025)

- Marketing reinvestment: €35m (2025)

- Net debt: €180m, down 18% YoY (Dec 2025)

Strategic Sustainability Focus

C&C Group has embedded ESG targets into operations, cutting Scope 1–3 emissions and targeting a 30% reduction in carbon intensity by 2028 versus 2020, and rolling out 100% recyclable packaging across key SKUs by 2025; this lowers regulatory risk under UK/EU rules and reduces input-cost volatility.

That sustainability stance boosts brand value with consumers and helped attract ESG-focused funds, contributing to a 12% uplift in institutional ownership in 2024 versus 2021.

- 30% carbon intensity target by 2028

- 100% recyclable packaging by 2025

- 12% rise in institutional ESG ownership (2021–2024)

C&C Group: Strong margins, €220m cash flow and €0.12 dividend amid market leadership

C&C Group’s strong market positions (Tennent’s ~40% Scotland lager; Bulmers top‑3 Ireland), diversified portfolio (cider 38% / beer 62% 2024) and vertical UK distribution (Matthew Clark, Bibendum) drive margins—underlying EBIT margin 12.8% FY2024; operating cash flow €220m FY2025 and net debt €180m Dec‑2025 support reinvestment and a €0.12 p/s 2025 dividend.

| Metric | Value |

|---|---|

| Underlying EBIT margin | 12.8% (FY2024) |

| Op. cash flow | €220m (FY2025) |

| Net debt | €180m (Dec‑2025) |

| Dividend | €0.12 p/s (2025) |

What is included in the product

Provides a concise SWOT analysis of C&C Group, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a clear, editable SWOT matrix for C&C Group that streamlines strategic alignment and allows quick updates to reflect market shifts.

Weaknesses

Historical ERP Implementation Failures

The group faced major operational and financial disruption from a botched ERP rollout in its Great Britain division, triggering £72m of one-off costs and a temporary 3.8% market-share decline in FY2024; the system was stabilized by end-2025.

The legacy failure forced intensified audits and ongoing remediation spend of ~£8m annually, raising scrutiny of internal controls and digital infrastructure management across the group.

Geographic Concentration Risk

About 85% of C&C Group plc's 2024 revenue came from the UK and Ireland, so local GDP dips or consumer-spend slumps hit earnings directly; a 1% fall in UK consumer confidence could lower near-term sales by an estimated 0.8–1.2%.

The group's limited geographic spread increases sensitivity to regional regulatory changes—UK duty rises in 2023 raised operating costs by roughly 2–3% of EBIT.

Compared with global peers diversifying 40–60% of sales outside one region, C&C remains more exposed to tax hikes and policy shifts that can compress margins quickly.

Exposure to On-Trade Volatility

The group’s heavy reliance on the on-trade (pubs, bars) leaves it exposed: on-trade accounted for ~55% of UK cider and beer off-take for C&C in 2024, so pub closures or weaker footfall hit volumes fast.

Rising venue costs—energy, staff, rent—pushed average pub operating margins down ~3 ppt in 2023–24, and a 4% shift to at-home consumption in 2024 reduced on-trade volumes.

That dependence forces constant credit and cashflow monitoring of major partners; a single large operator default could cut quarterly revenue by several million euros.

High Operating Leverage

C&C Group carries high fixed costs from breweries, canning lines and a large distribution fleet; in FY2024 fixed costs were ~62% of operating expenses, amplifying margin swings.

Small sales drops (a 5% volume decline) can cut operating profit by ~12% given current cost structure, so management needs >85% capacity use to sustain 2024 margins.

- Fixed costs ≈62% of OPEX (FY2024)

- 5% volume drop → ~12% operating profit fall

- Required capacity utilization >85% to maintain margins

Executive Leadership Transitions

The company has seen three CEO or CFO changes since 2021, creating strategic shifts and staff uncertainty that risk slowing execution of multi-year plans and contributed to a 12% drop in share price during 2023 volatility.

Frequent turnover can erode investor confidence—institutional ownership fell from 48% in 2021 to 42% in 2024—and complicates recovery from past operational losses of £85m in 2022.

Maintaining a consistent management approach is critical as the board aims to stabilise operations and hit the 2026 EBITDA margin target of 15%.

- 3 senior changes since 2021

- Share price down 12% in 2023

- Institutional ownership fell 6ppt (2021–24)

- £85m operating loss in 2022

- 2026 EBITDA margin target: 15%

High UK/IE exposure, on‑trade reliance and cost structure risk—weak leadership dents confidence

Concentrated UK/Ireland exposure (≈85% revenue) and heavy on-trade dependence (≈55% of volumes) amplify policy, demand and partner risk; fixed costs ~62% of OPEX mean a 5% volume drop cuts operating profit ~12%. CEO/CFO turnover (3 since 2021) and past losses (£85m in 2022) weaken investor confidence (institutional ownership 42% in 2024).

| Metric | Value |

|---|---|

| Revenue concentration (UK/IE) | ≈85% |

| On-trade share | ≈55% |

| Fixed costs of OPEX (FY2024) | ≈62% |

| 5% volume → op profit change | ≈−12% |

| CEO/CFO changes since 2021 | 3 |

| Operating loss (2022) | £85m |

| Institutional ownership (2024) | 42% |

Full Version Awaits

C&C Group SWOT Analysis

This is the actual C&C Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.