Canfor PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our targeted PESTLE Analysis of Canfor—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its market position and growth prospects; buy the full report for an actionable, ready-to-use breakdown that investors, consultants, and strategists rely on.

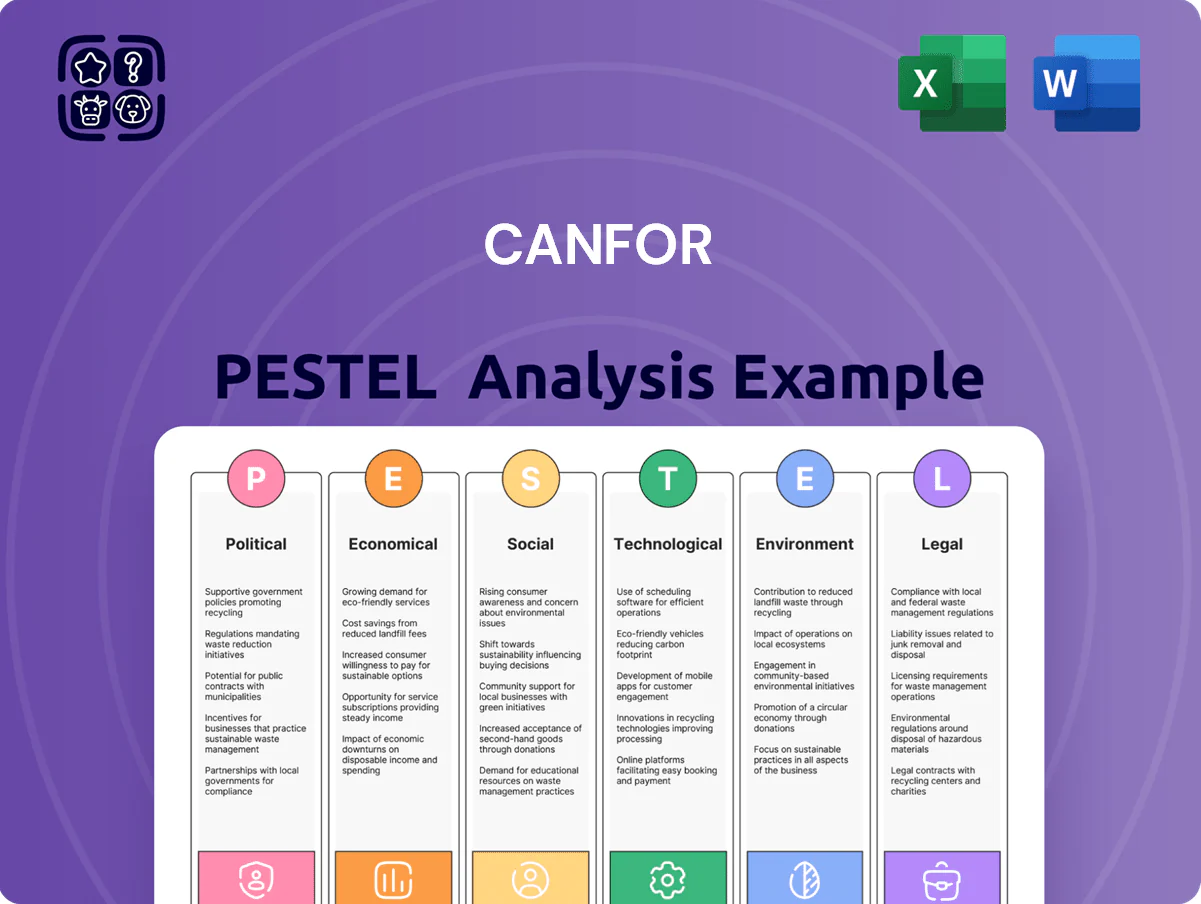

Political factors

Softwood Lumber Trade Dispute

The ongoing softwood lumber dispute with the United States remained a major political risk for Canfor into late 2025, with U.S. countervailing and anti-dumping duties averaging about 17–21% on Canadian shipments, squeezing 2024–25 gross margins by an estimated 150–300 basis points. Canfor accelerated geographic diversification, increasing U.S. manufacturing capacity to roughly 30% of production and expanding European sales, lowering exposure to duties. Continued lobbying and bilateral negotiations have directly influenced cross-border cost structure, with trade remedies adding approximately C$120–200 million in annual cash tax-like charges industry-wide.

British Columbia Forestry Policy

The BC government’s stricter land‑use rules prioritizing old‑growth and ecosystem health have cut provincial AAC by about 16% since 2019, pressuring Canfor to optimize harvests and boost procurement from residuals and third‑party mills; in 2024 Canfor reported fiber substitution costs rising ~12% YoY and capital investments of CAD 120m into mill modifications and biomass sourcing to shore up long‑term fiber security in Western Canada.

Federal Carbon Pricing Framework

The federal carbon pricing framework, rising from CAD 50/tCO2e in 2022 to CAD 65/tCO2e in 2024 and scheduled to reach CAD 170/tCO2e by 2030, raises Canfor’s manufacturing and transport costs—estimated to add CAD 15–25/ODT on fuel-intensive mills and trucking. Political pressure to hit Canada’s 2030 and net-zero 2050 targets has driven Canfor to invest hundreds of millions in electrification, biomass boilers and carbon reduction projects, creating both near-term margin compression and capex-led transformation.

International Trade Agreements

Expansion into Asian and European markets for Canfor is shaped by bilateral trade agreements and geopolitical stability; for example, Canada-EU CETA reduces tariffs for Canadian wood products, while China imported 1.8 million m3 of softwood lumber from Canada in 2024, making access sensitive to agreement terms.

Political shifts in importers like China or Japan can trigger abrupt tariff or phytosanitary rule changes; in 2023-24 regional disputes led to temporary certification delays affecting shipment timings and prices.

Canfor needs a flexible global sales strategy—diversifying channels and using short-term contracts—to limit exposure to localized political volatility and protect ~15–20% of export revenue tied to a single region.

- Rely on trade agreements (CETA) to lower tariff risk

- Monitor geopolitical indicators in China, Japan, EU

- Diversify buyers to reduce single-region revenue >15%

- Use flexible contracts and contingency logistics

Government Innovation Subsidies

Political support for a circular bio-economy gives Canfor access to grants and tax credits—Canada budget 2024 allocated CAD 1.5 billion to clean bio-industrial projects, and B.C. provincial programs offered CAD 120 million in 2023–24, enabling funding for wood-waste-to-biofuel/biochemical pilots.

Federal and provincial grants can offset high capex for modernization; recent green recovery funding reduced project financing gaps by up to 30%, improving IRR for conversion projects and lowering payback periods.

- Canada federal bioeconomy funding: CAD 1.5B (2024)

- B.C. provincial support: CAD 120M (2023–24)

- Typical capex offset: up to 30% via grants/tax credits

- Targets: wood-waste conversion to biofuels/biochemicals

Margins squeezed by duties, AAC cuts & carbon; diversification and grants mitigate risks

Softwood duties (17–21%) and BC AAC cuts (~16%) compressed 2024–25 margins; carbon price rose to CAD65/t in 2024 (CAD170/t by 2030) raising costs; diversification to US (≈30% capacity) and Europe plus bioeconomy grants (CAD1.5B federal, CAD120M BC) partly offset risks; exports concentrated ~15–20% per region—necessitating flexible contracts and capex for electrification/biomass.

| Metric | Value |

|---|---|

| US duties | 17–21% |

| BC AAC change | −16% since 2019 |

| US capacity | ≈30% |

| Carbon price (2024) | CAD65/t |

| Bio grants (2024) | CAD1.5B fed, CAD120M BC |

What is included in the product

Explores how macro-environmental factors uniquely affect Canfor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities.

A concise, visually segmented Canfor PESTLE summary that’s easily dropped into presentations or shared across teams to support quick alignment, risk discussions, and decision-making during planning sessions.

Economic factors

Global Interest Rate Cycles

By end-2025, stabilization of global interest rates—with the US Fed funds rate near 5.25–5.50% and Canada’s policy rate around 4.50%—directly moderates North American housing activity, a key driver of lumber demand; higher borrowing costs have cut US housing starts ~12% y/y in 2024 and Canada’s starts fell ~8% y/y, pressuring Canfor’s cyclical revenue. Canfor closely tracks central bank signals to forecast demand swings in its core markets.

North American Housing Starts

The demand for softwood lumber is tightly tied to U.S. and Canadian housing markets; U.S. housing starts rose to an annualized 1.46 million units in 2025 Q4, supporting mill volumes, while Canadian starts were about 219,000 units in 2025, keeping regional demand elevated. Persistent shortages in major urban centers—metro vacancy rates under 3% in 2024—create a demand floor despite rate-driven slowdowns. Canfor’s EBITDA swings with permit activity; a 10% change in North American starts historically alters lumber volumes by ~6-8%.

Commodity Price Volatility

Fluctuations in lumber and pulp prices drive earnings volatility for Canfor; lumber futures swung roughly 25-40% year-over-year in 2023-2024, pushing Canfor’s adjusted EBITDA from CAD 1.1bn in 2021 to CAD 0.4bn in 2023.

Global supply chain disruptions and inventory shifts at big-box retailers have caused rapid price swings, with North American softwood lumber stocks varying by over 30% across 2022-2024 leading to volatile realized prices.

Canfor uses hedging—locking futures contracts covering a material portion of production—and diversified lines (sawn lumber, pulp, paper) to mitigate cycles; pulp sales helped stabilize revenue, contributing over 20% of 2024 sales.

Operational Inflationary Pressures

Rising labor, energy and transportation costs have pressured Canfor’s margins, with Canadian average hourly wood product wages up ~6% y/y and industrial electricity prices rising about 4% in 2024–25, constraining EBITDA recovery heading into 2026.

Chemical input inflation—pulp bleaching agents rose roughly 12% from 2023–25—and diesel fuel averaging CAD 1.80–2.10/L in 2024–25 has increased logging operational spend, forcing efficiency and capital allocation shifts.

Canfor must weigh these input cost trends against market tolerance for price increases; SPF lumber and pulp markets showed volatile realized prices in 2024–25, limiting pass-through without demand erosion.

- Labor +6% y/y (wood products sector, 2024–25)

- Chemicals +12% (pulp inputs, 2023–25)

- Diesel CAD 1.80–2.10/L (2024–25)

- Industrial electricity +4% (2024–25)

Currency Exchange Volatility

As a Canadian company with substantial U.S. dollar sales, Canfor is exposed to CAD/USD volatility; a 10% CAD appreciation vs USD would cut translated U.S. revenue materially—Canfor reported 2024 US dollar sales representing about 40% of consolidated revenue.

A weaker CAD boosts export competitiveness and lifted 2024 adjusted operating earnings by an estimated CAD 60–80 million versus a neutral FX scenario; conversely, CAD strength compresses margins on U.S. sales.

- ~40% of revenue USD-denominated (2024)

- CAD appreciation of 10% materially reduces translated revenue

- FX tailwind in 2024 added ~CAD 60–80m to adjusted operating earnings

Housing starts, lumber swings and input inflation squeeze margins despite FX tailwind

Key economics: housing starts (US 1.46M 2025, CA 219k 2025) drive lumber demand; lumber price volatility 25–40% y/y (2023–24) swings EBITDA (CAD 1.1bn in 2021 to CAD 0.4bn in 2023); input inflation—wages +6% (2024–25), chemicals +12% (2023–25), diesel CAD1.80–2.10/L—pressures margins; FX: ~40% revenue USD, 2024 FX tailwind ≈ CAD60–80m.

| Metric | Value |

|---|---|

| US housing starts | 1.46M (2025) |

| CA housing starts | 219k (2025) |

| Revenue USD share | ~40% (2024) |

| FX tailwind | CAD60–80m (2024) |

Preview the Actual Deliverable

Canfor PESTLE Analysis

The preview shown here is the exact Canfor PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our targeted PESTLE Analysis of Canfor—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its market position and growth prospects; buy the full report for an actionable, ready-to-use breakdown that investors, consultants, and strategists rely on.

Political factors

Softwood Lumber Trade Dispute

The ongoing softwood lumber dispute with the United States remained a major political risk for Canfor into late 2025, with U.S. countervailing and anti-dumping duties averaging about 17–21% on Canadian shipments, squeezing 2024–25 gross margins by an estimated 150–300 basis points. Canfor accelerated geographic diversification, increasing U.S. manufacturing capacity to roughly 30% of production and expanding European sales, lowering exposure to duties. Continued lobbying and bilateral negotiations have directly influenced cross-border cost structure, with trade remedies adding approximately C$120–200 million in annual cash tax-like charges industry-wide.

British Columbia Forestry Policy

The BC government’s stricter land‑use rules prioritizing old‑growth and ecosystem health have cut provincial AAC by about 16% since 2019, pressuring Canfor to optimize harvests and boost procurement from residuals and third‑party mills; in 2024 Canfor reported fiber substitution costs rising ~12% YoY and capital investments of CAD 120m into mill modifications and biomass sourcing to shore up long‑term fiber security in Western Canada.

Federal Carbon Pricing Framework

The federal carbon pricing framework, rising from CAD 50/tCO2e in 2022 to CAD 65/tCO2e in 2024 and scheduled to reach CAD 170/tCO2e by 2030, raises Canfor’s manufacturing and transport costs—estimated to add CAD 15–25/ODT on fuel-intensive mills and trucking. Political pressure to hit Canada’s 2030 and net-zero 2050 targets has driven Canfor to invest hundreds of millions in electrification, biomass boilers and carbon reduction projects, creating both near-term margin compression and capex-led transformation.

International Trade Agreements

Expansion into Asian and European markets for Canfor is shaped by bilateral trade agreements and geopolitical stability; for example, Canada-EU CETA reduces tariffs for Canadian wood products, while China imported 1.8 million m3 of softwood lumber from Canada in 2024, making access sensitive to agreement terms.

Political shifts in importers like China or Japan can trigger abrupt tariff or phytosanitary rule changes; in 2023-24 regional disputes led to temporary certification delays affecting shipment timings and prices.

Canfor needs a flexible global sales strategy—diversifying channels and using short-term contracts—to limit exposure to localized political volatility and protect ~15–20% of export revenue tied to a single region.

- Rely on trade agreements (CETA) to lower tariff risk

- Monitor geopolitical indicators in China, Japan, EU

- Diversify buyers to reduce single-region revenue >15%

- Use flexible contracts and contingency logistics

Government Innovation Subsidies

Political support for a circular bio-economy gives Canfor access to grants and tax credits—Canada budget 2024 allocated CAD 1.5 billion to clean bio-industrial projects, and B.C. provincial programs offered CAD 120 million in 2023–24, enabling funding for wood-waste-to-biofuel/biochemical pilots.

Federal and provincial grants can offset high capex for modernization; recent green recovery funding reduced project financing gaps by up to 30%, improving IRR for conversion projects and lowering payback periods.

- Canada federal bioeconomy funding: CAD 1.5B (2024)

- B.C. provincial support: CAD 120M (2023–24)

- Typical capex offset: up to 30% via grants/tax credits

- Targets: wood-waste conversion to biofuels/biochemicals

Margins squeezed by duties, AAC cuts & carbon; diversification and grants mitigate risks

Softwood duties (17–21%) and BC AAC cuts (~16%) compressed 2024–25 margins; carbon price rose to CAD65/t in 2024 (CAD170/t by 2030) raising costs; diversification to US (≈30% capacity) and Europe plus bioeconomy grants (CAD1.5B federal, CAD120M BC) partly offset risks; exports concentrated ~15–20% per region—necessitating flexible contracts and capex for electrification/biomass.

| Metric | Value |

|---|---|

| US duties | 17–21% |

| BC AAC change | −16% since 2019 |

| US capacity | ≈30% |

| Carbon price (2024) | CAD65/t |

| Bio grants (2024) | CAD1.5B fed, CAD120M BC |

What is included in the product

Explores how macro-environmental factors uniquely affect Canfor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities.

A concise, visually segmented Canfor PESTLE summary that’s easily dropped into presentations or shared across teams to support quick alignment, risk discussions, and decision-making during planning sessions.

Economic factors

Global Interest Rate Cycles

By end-2025, stabilization of global interest rates—with the US Fed funds rate near 5.25–5.50% and Canada’s policy rate around 4.50%—directly moderates North American housing activity, a key driver of lumber demand; higher borrowing costs have cut US housing starts ~12% y/y in 2024 and Canada’s starts fell ~8% y/y, pressuring Canfor’s cyclical revenue. Canfor closely tracks central bank signals to forecast demand swings in its core markets.

North American Housing Starts

The demand for softwood lumber is tightly tied to U.S. and Canadian housing markets; U.S. housing starts rose to an annualized 1.46 million units in 2025 Q4, supporting mill volumes, while Canadian starts were about 219,000 units in 2025, keeping regional demand elevated. Persistent shortages in major urban centers—metro vacancy rates under 3% in 2024—create a demand floor despite rate-driven slowdowns. Canfor’s EBITDA swings with permit activity; a 10% change in North American starts historically alters lumber volumes by ~6-8%.

Commodity Price Volatility

Fluctuations in lumber and pulp prices drive earnings volatility for Canfor; lumber futures swung roughly 25-40% year-over-year in 2023-2024, pushing Canfor’s adjusted EBITDA from CAD 1.1bn in 2021 to CAD 0.4bn in 2023.

Global supply chain disruptions and inventory shifts at big-box retailers have caused rapid price swings, with North American softwood lumber stocks varying by over 30% across 2022-2024 leading to volatile realized prices.

Canfor uses hedging—locking futures contracts covering a material portion of production—and diversified lines (sawn lumber, pulp, paper) to mitigate cycles; pulp sales helped stabilize revenue, contributing over 20% of 2024 sales.

Operational Inflationary Pressures

Rising labor, energy and transportation costs have pressured Canfor’s margins, with Canadian average hourly wood product wages up ~6% y/y and industrial electricity prices rising about 4% in 2024–25, constraining EBITDA recovery heading into 2026.

Chemical input inflation—pulp bleaching agents rose roughly 12% from 2023–25—and diesel fuel averaging CAD 1.80–2.10/L in 2024–25 has increased logging operational spend, forcing efficiency and capital allocation shifts.

Canfor must weigh these input cost trends against market tolerance for price increases; SPF lumber and pulp markets showed volatile realized prices in 2024–25, limiting pass-through without demand erosion.

- Labor +6% y/y (wood products sector, 2024–25)

- Chemicals +12% (pulp inputs, 2023–25)

- Diesel CAD 1.80–2.10/L (2024–25)

- Industrial electricity +4% (2024–25)

Currency Exchange Volatility

As a Canadian company with substantial U.S. dollar sales, Canfor is exposed to CAD/USD volatility; a 10% CAD appreciation vs USD would cut translated U.S. revenue materially—Canfor reported 2024 US dollar sales representing about 40% of consolidated revenue.

A weaker CAD boosts export competitiveness and lifted 2024 adjusted operating earnings by an estimated CAD 60–80 million versus a neutral FX scenario; conversely, CAD strength compresses margins on U.S. sales.

- ~40% of revenue USD-denominated (2024)

- CAD appreciation of 10% materially reduces translated revenue

- FX tailwind in 2024 added ~CAD 60–80m to adjusted operating earnings

Housing starts, lumber swings and input inflation squeeze margins despite FX tailwind

Key economics: housing starts (US 1.46M 2025, CA 219k 2025) drive lumber demand; lumber price volatility 25–40% y/y (2023–24) swings EBITDA (CAD 1.1bn in 2021 to CAD 0.4bn in 2023); input inflation—wages +6% (2024–25), chemicals +12% (2023–25), diesel CAD1.80–2.10/L—pressures margins; FX: ~40% revenue USD, 2024 FX tailwind ≈ CAD60–80m.

| Metric | Value |

|---|---|

| US housing starts | 1.46M (2025) |

| CA housing starts | 219k (2025) |

| Revenue USD share | ~40% (2024) |

| FX tailwind | CAD60–80m (2024) |

Preview the Actual Deliverable

Canfor PESTLE Analysis

The preview shown here is the exact Canfor PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.