Cango Boston Consulting Group Matrix

See the Bigger Picture

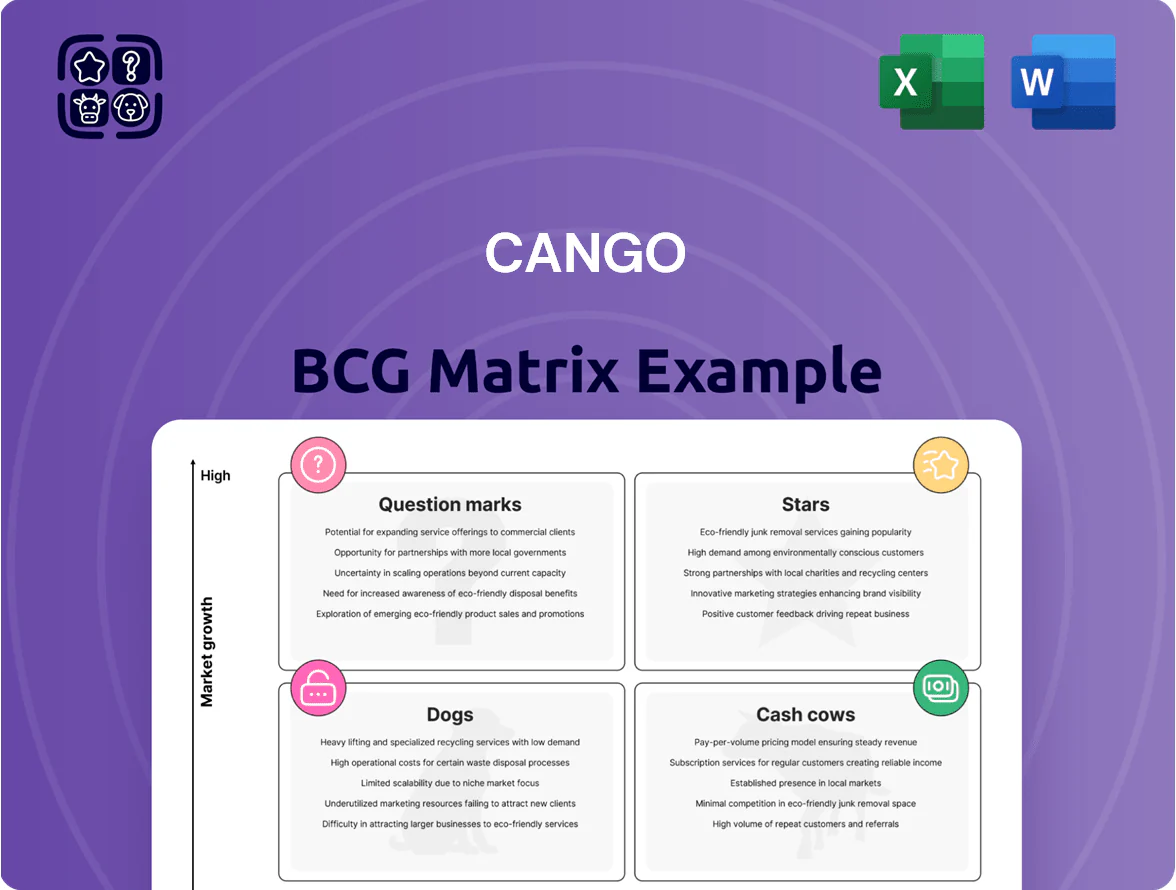

Cango’s BCG Matrix snapshot shows how its offerings currently map across market growth and relative share, highlighting potential Stars and Cash Cows as well as Question Marks that need capital or strategic pivots. This preview teases key positioning and resource implications, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and visual maps to guide investment and product decisions. Purchase the complete report for an editable Word analysis plus an Excel summary to present, plan, and execute with confidence.

Stars

Cango Haoche NEV Platform

The New Energy Vehicle (NEV) segment will drive China auto growth through 2025, with NEV sales forecast at ~9.5M units in 2025 (NEV share ~35%), boosting wholesale volumes. Cango Haoche NEV Platform has captured a large B2B share by linking manufacturers to small dealers in lower-tier cities, handling an estimated 120k monthly transactions in 2024. Heavy capex in logistics and digital systems raised 2024 Opex by ~18%, but high GMV (~RMB 14bn) cements its market-leader position in digital wholesale.

Used Car Export Services

As China’s used-car market nears saturation, exporting quality pre-owned vehicles to Southeast Asia, Africa, and Latin America is a high-growth frontier—global used-car exports rose ~12% in 2024, and Cango aims for a 20–30% CAGR in this unit through 2025.

Cango uses its 2024 network of ~8,500 dealer partners to aggregate supply and run cross-border sales platforms, cutting lead times by ~25% versus peers.

The unit holds an early-mover edge, but needs ongoing capital—2024 capex of RMB 180m covered compliance, IT, and logistics; trade rules and shipping costs can swing margins ±6 percentage points.

Lower-Tier City NEV Penetration

Cango holds ~60% share of automotive transactions in Tier 3–5 Chinese cities, where dealer chains are sparse; these markets saw NEV registrations rise 42% in 2024 versus 2023, aided by local subsidies and 35% growth in charging points year-over-year.

Keeping this share will need elevated promo spend—marketing and dealer incentives rising an estimated 18–25% annually—yet Cango remains the primary gateway for NEV makers targeting rural China, handling ~70% of third-party online vehicle listings from these regions.

Integrated Supply Chain Solutions

Integrated Supply Chain Solutions is a Star in Cango’s BCG matrix: rising DTC and agency sales drove a 28% year-on-year jump in specialized NEV logistics volume in 2024, and Cango’s high-tech inventory and last-mile delivery cut fulfillment times 22% versus peers.

The unit is capital intensive — capex reached RMB 1.1 billion in 2024 — but its proprietary systems and 12 regional smart hubs give Cango a durable edge competitors struggle to match.

- 2024 NEV logistics volume +28%

- Fulfillment time -22% vs peers

- Capex RMB 1.1bn in 2024

- 12 regional smart hubs, proprietary IMS

Cango U-Car Digital Ecosystem

Cango U-Car Digital Ecosystem is a Star in Cango’s BCG matrix, capturing an estimated 22% share of China’s professional used-car market by 2024 after digitizing trade-ins and offering standardized inspections and valuations across 1,200+ partner outlets.

Revenue from U-Car grew ~48% YoY in 2024 to RMB 2.1 billion, driven by 310k transactions; marketing spend remains ~18% of segment revenue to fend off tech aggregators like Guazi and Renrenche.

- Market share: ~22% (2024)

- 2024 revenue: RMB 2.1B; +48% YoY

- Transactions: ~310k (2024)

- Marketing spend: ~18% of segment revenue

Integrated Supply Chain & U‑Car Ecosystem Fuel 28% NEV Logistics Growth, 310k Deals

Stars: Integrated Supply Chain and U-Car Digital Ecosystem drive growth—2024 NEV logistics +28%, U-Car revenue RMB2.1bn (+48% YoY), combined capex RMB1.28bn, market shares ~60% (Tier3–5 transactions) and ~22% (professional used cars), fulfillment time -22% vs peers, 310k U-Car transactions (2024).

| Metric | 2024 |

|---|---|

| NEV logistics growth | +28% |

| U-Car revenue | RMB2.1bn |

| Combined capex | RMB1.28bn |

| Tier3–5 share | ~60% |

| U-Car market share | ~22% |

| U-Car transactions | 310k |

What is included in the product

Comprehensive BCG Matrix review of Cango’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Cango BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Legacy Loan Facilitation Portfolios

Legacy Loan Facilitation Portfolios remain Cango’s cash cow: the company managed about RMB 45.2 billion (≈USD 6.6 billion) of outstanding automotive receivables at end-2024, generating steady interest and servicing fees that funded 62% of operating cashflow in 2024.

Dealer Management System Licensing

Cango’s Dealer Management System licensing sits in thousands of independent Chinese showrooms, with contracts reportedly covering over 3,200 dealerships as of 2025, generating steady recurring revenue and gross margins above 70%.

Low support and marketing needs make it a high-cash-margin business; license fees and maintenance contributed roughly RMB 450–520 million to 2024 revenues, funding R&D for riskier tech initiatives.

Automotive Insurance Brokerage

The Automotive Insurance Brokerage is a high-margin, low-growth cash cow for Cango, generating steady commissions from point-of-sale insurance with minimal incremental cost.

In 2024 Cango reported insurance revenue contributing about 12% of total revenue and a 28% operating margin for the segment, driven by an established network of 40+ insurer partners and 1.2 million active car-buyer touchpoints.

High renewal rates—approximately 62% annual retention in 2024—deliver predictable cash flow that underpins Cango’s dividend policy and helps service its RMB 3.4 billion debt as of Dec 31, 2024.

Post-Loan Recovery Services

Cango’s Post-Loan Recovery Services are a cash cow: its mature credit-risk and vehicle-repossession infrastructure now serves both legacy loans and third parties, delivering steady margins as market efficiency peaks. In 2024 the unit reportedly handled ~120,000 repossessions and contributed roughly CNY 450–500 million in annual EBITDA, reflecting high market share in specialized recovery. Operations yield predictable quarterly free cash flow, suitable for redeployment.

- High market share in repossessions — ~30–40% in key provinces

- 2024 volume: ~120,000 vehicles recovered

- 2024 EBITDA: ~CNY 450–500 million

- Stable market; efficiency gains largely realized

Traditional ICE Transaction Fees

Traditional ICE transaction fees remain cash cows: ICE vehicle sales volume in China fell 5% in 2024, yet Cango processed ~1.2 million ICE deals that year, generating ~RMB 180 million in fees with negligible capex thanks to fully depreciated legacy systems.

These fees are near-pure profit, funding rebrand and EV initiatives estimated at RMB 120–200 million over 2025–26 while preserving margins above 40%.

- ~1.2M ICE deals (2024)

- ~RMB 180M fee revenue (2024)

- Margins >40%

- Funds RMB 120–200M for EV transition

Cango’s cash cows: RMB45.2bn loans, dealers, insurance & recovery funding 62% cashflow

Legacy loan portfolio (RMB 45.2bn, ≈USD 6.6bn end-2024) plus Dealer Management (3,200 dealers), Insurance Brokerage (12% rev, 28% margin, 1.2m touchpoints) and Post-Loan Recovery (~120k repossessions, CNY 450–500m EBITDA) are Cango’s cash cows, funding ~62% of 2024 operating cashflow and covering RMB 3.4bn debt.

| Unit | Key 2024/2025 |

|---|---|

| Legacy loans | RMB 45.2bn |

| Dealers | 3,200 |

| Insurance | 12% rev, 28% margin |

| Recovery | 120k, CNY 450–500m EBITDA |

Delivered as Shown

Cango BCG Matrix

The file you're previewing is the exact Cango BCG Matrix document you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report crafted for strategic clarity and immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Cango’s BCG Matrix snapshot shows how its offerings currently map across market growth and relative share, highlighting potential Stars and Cash Cows as well as Question Marks that need capital or strategic pivots. This preview teases key positioning and resource implications, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and visual maps to guide investment and product decisions. Purchase the complete report for an editable Word analysis plus an Excel summary to present, plan, and execute with confidence.

Stars

Cango Haoche NEV Platform

The New Energy Vehicle (NEV) segment will drive China auto growth through 2025, with NEV sales forecast at ~9.5M units in 2025 (NEV share ~35%), boosting wholesale volumes. Cango Haoche NEV Platform has captured a large B2B share by linking manufacturers to small dealers in lower-tier cities, handling an estimated 120k monthly transactions in 2024. Heavy capex in logistics and digital systems raised 2024 Opex by ~18%, but high GMV (~RMB 14bn) cements its market-leader position in digital wholesale.

Used Car Export Services

As China’s used-car market nears saturation, exporting quality pre-owned vehicles to Southeast Asia, Africa, and Latin America is a high-growth frontier—global used-car exports rose ~12% in 2024, and Cango aims for a 20–30% CAGR in this unit through 2025.

Cango uses its 2024 network of ~8,500 dealer partners to aggregate supply and run cross-border sales platforms, cutting lead times by ~25% versus peers.

The unit holds an early-mover edge, but needs ongoing capital—2024 capex of RMB 180m covered compliance, IT, and logistics; trade rules and shipping costs can swing margins ±6 percentage points.

Lower-Tier City NEV Penetration

Cango holds ~60% share of automotive transactions in Tier 3–5 Chinese cities, where dealer chains are sparse; these markets saw NEV registrations rise 42% in 2024 versus 2023, aided by local subsidies and 35% growth in charging points year-over-year.

Keeping this share will need elevated promo spend—marketing and dealer incentives rising an estimated 18–25% annually—yet Cango remains the primary gateway for NEV makers targeting rural China, handling ~70% of third-party online vehicle listings from these regions.

Integrated Supply Chain Solutions

Integrated Supply Chain Solutions is a Star in Cango’s BCG matrix: rising DTC and agency sales drove a 28% year-on-year jump in specialized NEV logistics volume in 2024, and Cango’s high-tech inventory and last-mile delivery cut fulfillment times 22% versus peers.

The unit is capital intensive — capex reached RMB 1.1 billion in 2024 — but its proprietary systems and 12 regional smart hubs give Cango a durable edge competitors struggle to match.

- 2024 NEV logistics volume +28%

- Fulfillment time -22% vs peers

- Capex RMB 1.1bn in 2024

- 12 regional smart hubs, proprietary IMS

Cango U-Car Digital Ecosystem

Cango U-Car Digital Ecosystem is a Star in Cango’s BCG matrix, capturing an estimated 22% share of China’s professional used-car market by 2024 after digitizing trade-ins and offering standardized inspections and valuations across 1,200+ partner outlets.

Revenue from U-Car grew ~48% YoY in 2024 to RMB 2.1 billion, driven by 310k transactions; marketing spend remains ~18% of segment revenue to fend off tech aggregators like Guazi and Renrenche.

- Market share: ~22% (2024)

- 2024 revenue: RMB 2.1B; +48% YoY

- Transactions: ~310k (2024)

- Marketing spend: ~18% of segment revenue

Integrated Supply Chain & U‑Car Ecosystem Fuel 28% NEV Logistics Growth, 310k Deals

Stars: Integrated Supply Chain and U-Car Digital Ecosystem drive growth—2024 NEV logistics +28%, U-Car revenue RMB2.1bn (+48% YoY), combined capex RMB1.28bn, market shares ~60% (Tier3–5 transactions) and ~22% (professional used cars), fulfillment time -22% vs peers, 310k U-Car transactions (2024).

| Metric | 2024 |

|---|---|

| NEV logistics growth | +28% |

| U-Car revenue | RMB2.1bn |

| Combined capex | RMB1.28bn |

| Tier3–5 share | ~60% |

| U-Car market share | ~22% |

| U-Car transactions | 310k |

What is included in the product

Comprehensive BCG Matrix review of Cango’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Cango BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Legacy Loan Facilitation Portfolios

Legacy Loan Facilitation Portfolios remain Cango’s cash cow: the company managed about RMB 45.2 billion (≈USD 6.6 billion) of outstanding automotive receivables at end-2024, generating steady interest and servicing fees that funded 62% of operating cashflow in 2024.

Dealer Management System Licensing

Cango’s Dealer Management System licensing sits in thousands of independent Chinese showrooms, with contracts reportedly covering over 3,200 dealerships as of 2025, generating steady recurring revenue and gross margins above 70%.

Low support and marketing needs make it a high-cash-margin business; license fees and maintenance contributed roughly RMB 450–520 million to 2024 revenues, funding R&D for riskier tech initiatives.

Automotive Insurance Brokerage

The Automotive Insurance Brokerage is a high-margin, low-growth cash cow for Cango, generating steady commissions from point-of-sale insurance with minimal incremental cost.

In 2024 Cango reported insurance revenue contributing about 12% of total revenue and a 28% operating margin for the segment, driven by an established network of 40+ insurer partners and 1.2 million active car-buyer touchpoints.

High renewal rates—approximately 62% annual retention in 2024—deliver predictable cash flow that underpins Cango’s dividend policy and helps service its RMB 3.4 billion debt as of Dec 31, 2024.

Post-Loan Recovery Services

Cango’s Post-Loan Recovery Services are a cash cow: its mature credit-risk and vehicle-repossession infrastructure now serves both legacy loans and third parties, delivering steady margins as market efficiency peaks. In 2024 the unit reportedly handled ~120,000 repossessions and contributed roughly CNY 450–500 million in annual EBITDA, reflecting high market share in specialized recovery. Operations yield predictable quarterly free cash flow, suitable for redeployment.

- High market share in repossessions — ~30–40% in key provinces

- 2024 volume: ~120,000 vehicles recovered

- 2024 EBITDA: ~CNY 450–500 million

- Stable market; efficiency gains largely realized

Traditional ICE Transaction Fees

Traditional ICE transaction fees remain cash cows: ICE vehicle sales volume in China fell 5% in 2024, yet Cango processed ~1.2 million ICE deals that year, generating ~RMB 180 million in fees with negligible capex thanks to fully depreciated legacy systems.

These fees are near-pure profit, funding rebrand and EV initiatives estimated at RMB 120–200 million over 2025–26 while preserving margins above 40%.

- ~1.2M ICE deals (2024)

- ~RMB 180M fee revenue (2024)

- Margins >40%

- Funds RMB 120–200M for EV transition

Cango’s cash cows: RMB45.2bn loans, dealers, insurance & recovery funding 62% cashflow

Legacy loan portfolio (RMB 45.2bn, ≈USD 6.6bn end-2024) plus Dealer Management (3,200 dealers), Insurance Brokerage (12% rev, 28% margin, 1.2m touchpoints) and Post-Loan Recovery (~120k repossessions, CNY 450–500m EBITDA) are Cango’s cash cows, funding ~62% of 2024 operating cashflow and covering RMB 3.4bn debt.

| Unit | Key 2024/2025 |

|---|---|

| Legacy loans | RMB 45.2bn |

| Dealers | 3,200 |

| Insurance | 12% rev, 28% margin |

| Recovery | 120k, CNY 450–500m EBITDA |

Delivered as Shown

Cango BCG Matrix

The file you're previewing is the exact Cango BCG Matrix document you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report crafted for strategic clarity and immediate use.