Cango Business Model Canvas

Unlock Cango’s Business Model Canvas: Ready Insights for Investors & Founders

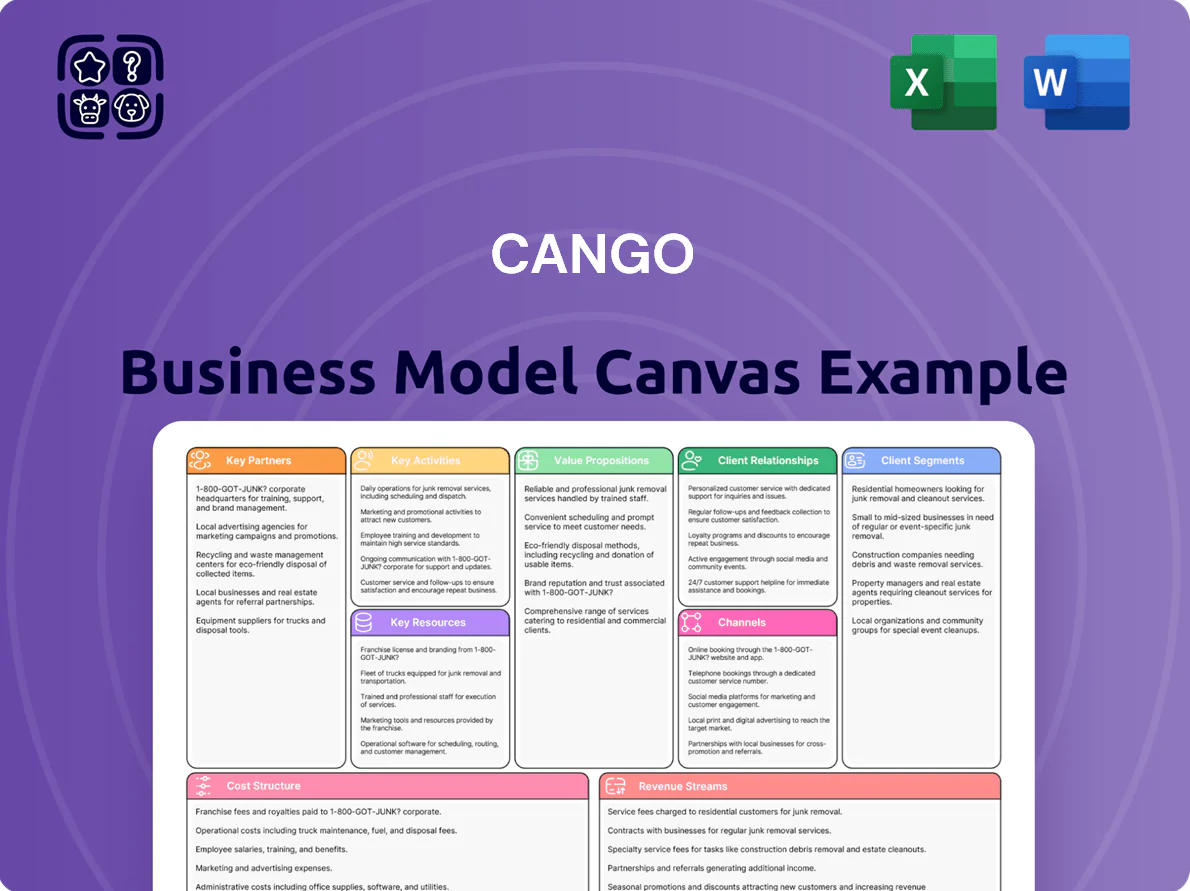

Unlock Cango’s strategic playbook with our Business Model Canvas—concise, actionable, and tailored for investors, advisors, and founders seeking competitive edge; download the full Word/Excel canvas to examine customer segments, revenue streams, partnerships, and growth levers with ready-to-use insights for benchmarking and strategy execution.

Partnerships

Commercial Banking Institutions

Cango partners with major Chinese commercial banks (e.g., ICBC, CMB) to unlock liquidity for auto loans, channeling over RMB 30 billion in bank funding in 2024 to underbanked buyers in lower-tier cities. Banks use Cango’s proprietary credit models to approve higher-risk borrowers; integrated APIs ensure capital flows directly to dealers while Cango earns facilitation fees ~1.2–2.5% per loan.

Extensive Registered Dealer Network

Cango works with over 8,000 small and mid-sized automotive dealers across China who act as the primary points of sale, giving Cango local reach in fragmented regional markets; these dealers supply showrooms, sales staff, and on-the-ground customer access. Cango equips them with digital sales platforms, inventory-management tools, and access to loan and leasing products—supporting roughly RMB 120 billion in financed vehicle transactions through its network in 2024.

Insurance and Aftermarket Providers

Cango partners with over 30 insurance and aftermarket providers to sell vehicle insurance and extended warranties at point of purchase, creating a one-stop experience that raised attach rates to ~28% in 2024 and boosted average transaction value by about CNY 4,800 (≈USD 700). The cross-sell drives commission revenue—roughly 12% of Cango’s 2024 service revenues—and improves consumer protection through bundled coverage and longer warranty terms.

Technology and Data Partners

Collaborations with cloud providers and data vendors let Cango refine credit models and scale analytics; by 2025 partnerships cut model retraining time 30% and supported processing of 50+ TB monthly to score thin-file buyers.

That tech backbone lowers delinquency—Cango reported subprime 30-day delinquency near 2.8% in 2024—and speeds approvals, trimming median decision time to under 2 hours.

- 50+ TB/month data ingested

- 30% faster model retraining (2025)

- Median approval <2 hours

- 30-day delinquency ~2.8% (2024)

Used Car Auction Platforms and Logistics

Partnerships with national auction platforms and logistics providers let Cango Haoche move cars across China efficiently; in 2024 Cango reported Haoche processed ~120,000 used-car listings with turnover target under 30 days, so transport links cut regional stock imbalances and carrying cost.

- Logistics cut transfer time: 3–7 days between provinces

- Supports 120k listings (2024) and sub-30 day turnover

- Reduces regional stock shortfalls by ~15%

Cango lands RMB30–35bn bank backing; 120k listings, sub‑2hr approvals, 2.8% delinquency

Cango secures RMB 30–35bn bank funding (2024) via ICBC/CMB partnerships, earning 1.2–2.5% fees; its 8,000+ dealer network supported ~RMB 120bn financed transactions and 120k Haoche listings (2024). Tech/data partners processed 50+ TB/month, cut model retraining 30% (2025), yielding <2‑hour approvals and 2.8% 30‑day delinquency (2024).

| Metric | Value (year) |

|---|---|

| Bank funding | RMB 30–35bn (2024) |

| Dealers | 8,000+ (2024) |

| Financed volume | RMB 120bn (2024) |

| Haoche listings | 120k (2024) |

| Data ingested | 50+ TB/month (2025) |

| Model retrain speed | 30% faster (2025) |

| Median approval time | <2 hours (2024) |

| 30-day delinquency | 2.8% (2024) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Cango detailing nine BMC blocks—customer segments, channels, value propositions, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—aligned with the company’s real-world operations and strategy, including competitive advantage analysis, SWOT-linked insights, and a polished format for presentations, funding discussions, and decision-making.

Condenses Cango’s complex auto-fintech model into a one-page, editable snapshot that saves hours of structuring while enabling quick comparison, team collaboration, and boardroom-ready presentations.

Activities

Automotive Loan Facilitation

Cango matches car buyers with partner-bank loans, handling applications end-to-end—data intake, credit checks, approval and disbursement—serving over 1.2 million retail loan applications and facilitating RMB 150 billion in auto finance throughput in 2024. This requires continual coordination among buyer, dealer, and lender to meet regulatory requirements and average a 48-hour approval cycle for standard loans.

Platform Development and Maintenance

Cango spends heavily on its digital backbone—notably the Cango Haoche app and dealer management systems—with R&D and IT ops accounting for about 12–15% of FY2024 revenue (~RMB 1.1–1.3 billion on a RMB 9.2 billion top line) to fund continuous UI updates, new product integrations, and data‑security measures; this supports peak loads of tens of thousands of concurrent transactions across China’s 31 provinces.

Dealer Network Management and Training

The company recruits, onboards, and trains dealers to use the Cango platform, with field agents visiting 2,300+ partner dealerships in 2024 to provide hands-on tech support and update sales teams on financing and insurance products; this raised dealer NPS to 42 and cut platform-related errors by 28% year-over-year. This activity strengthens brand loyalty and maintains consistent service quality for end consumers.

Risk Management and Credit Assessment

Risk management centers on refining credit-scoring models with machine learning applied to Cango’s historical loan and transaction dataset (over 12m loans through 2024), improving default prediction and pricing.

Cango monitors portfolio KPIs—90+ DPD, NPL ratio (~2.8% in 2024), recovery rates—and uses real-time repayment signals to trigger proactive collections, protecting bank partner trust and limiting losses.

- 12m loans analyzed through 2024

- NPL ~2.8% (2024)

- Real-time repayment monitoring

- ML-driven credit score updates

- Proactive collections to preserve partner trust

Used Car Transaction Facilitation

Cango: AI-driven auto-finance platform — RMB150B throughput, 1.2M apps, 2.8% NPL

Cango runs end-to-end auto-finance origination (1.2m apps; RMB150B throughput 2024), R&D/IT ~12–15% revenue (~RMB1.1–1.3B on RMB9.2B), dealer onboarding (2,300+ sites), ML credit models on 12m loans, NPL ~2.8% (2024), and used-car ops (200k listings; China used-car market ~28m transactions 2024).

| Metric | 2024 Value |

|---|---|

| Loan apps | 1.2m |

| Throughput | RMB150B |

| Revenue | RMB9.2B |

| R&D/IT spend | 12–15% (~RMB1.1–1.3B) |

| Loans analyzed | 12m |

| NPL | ~2.8% |

| Dealers visited | 2,300+ |

| Used listings | 200k |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact Cango Business Model Canvas you will receive after purchase—no mockups or samples. When you complete your order, you'll download this same professionally formatted file, ready to edit and present in Word and Excel. What you see is the final deliverable, fully structured and complete—no hidden content or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Cango’s Business Model Canvas: Ready Insights for Investors & Founders

Unlock Cango’s strategic playbook with our Business Model Canvas—concise, actionable, and tailored for investors, advisors, and founders seeking competitive edge; download the full Word/Excel canvas to examine customer segments, revenue streams, partnerships, and growth levers with ready-to-use insights for benchmarking and strategy execution.

Partnerships

Commercial Banking Institutions

Cango partners with major Chinese commercial banks (e.g., ICBC, CMB) to unlock liquidity for auto loans, channeling over RMB 30 billion in bank funding in 2024 to underbanked buyers in lower-tier cities. Banks use Cango’s proprietary credit models to approve higher-risk borrowers; integrated APIs ensure capital flows directly to dealers while Cango earns facilitation fees ~1.2–2.5% per loan.

Extensive Registered Dealer Network

Cango works with over 8,000 small and mid-sized automotive dealers across China who act as the primary points of sale, giving Cango local reach in fragmented regional markets; these dealers supply showrooms, sales staff, and on-the-ground customer access. Cango equips them with digital sales platforms, inventory-management tools, and access to loan and leasing products—supporting roughly RMB 120 billion in financed vehicle transactions through its network in 2024.

Insurance and Aftermarket Providers

Cango partners with over 30 insurance and aftermarket providers to sell vehicle insurance and extended warranties at point of purchase, creating a one-stop experience that raised attach rates to ~28% in 2024 and boosted average transaction value by about CNY 4,800 (≈USD 700). The cross-sell drives commission revenue—roughly 12% of Cango’s 2024 service revenues—and improves consumer protection through bundled coverage and longer warranty terms.

Technology and Data Partners

Collaborations with cloud providers and data vendors let Cango refine credit models and scale analytics; by 2025 partnerships cut model retraining time 30% and supported processing of 50+ TB monthly to score thin-file buyers.

That tech backbone lowers delinquency—Cango reported subprime 30-day delinquency near 2.8% in 2024—and speeds approvals, trimming median decision time to under 2 hours.

- 50+ TB/month data ingested

- 30% faster model retraining (2025)

- Median approval <2 hours

- 30-day delinquency ~2.8% (2024)

Used Car Auction Platforms and Logistics

Partnerships with national auction platforms and logistics providers let Cango Haoche move cars across China efficiently; in 2024 Cango reported Haoche processed ~120,000 used-car listings with turnover target under 30 days, so transport links cut regional stock imbalances and carrying cost.

- Logistics cut transfer time: 3–7 days between provinces

- Supports 120k listings (2024) and sub-30 day turnover

- Reduces regional stock shortfalls by ~15%

Cango lands RMB30–35bn bank backing; 120k listings, sub‑2hr approvals, 2.8% delinquency

Cango secures RMB 30–35bn bank funding (2024) via ICBC/CMB partnerships, earning 1.2–2.5% fees; its 8,000+ dealer network supported ~RMB 120bn financed transactions and 120k Haoche listings (2024). Tech/data partners processed 50+ TB/month, cut model retraining 30% (2025), yielding <2‑hour approvals and 2.8% 30‑day delinquency (2024).

| Metric | Value (year) |

|---|---|

| Bank funding | RMB 30–35bn (2024) |

| Dealers | 8,000+ (2024) |

| Financed volume | RMB 120bn (2024) |

| Haoche listings | 120k (2024) |

| Data ingested | 50+ TB/month (2025) |

| Model retrain speed | 30% faster (2025) |

| Median approval time | <2 hours (2024) |

| 30-day delinquency | 2.8% (2024) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Cango detailing nine BMC blocks—customer segments, channels, value propositions, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—aligned with the company’s real-world operations and strategy, including competitive advantage analysis, SWOT-linked insights, and a polished format for presentations, funding discussions, and decision-making.

Condenses Cango’s complex auto-fintech model into a one-page, editable snapshot that saves hours of structuring while enabling quick comparison, team collaboration, and boardroom-ready presentations.

Activities

Automotive Loan Facilitation

Cango matches car buyers with partner-bank loans, handling applications end-to-end—data intake, credit checks, approval and disbursement—serving over 1.2 million retail loan applications and facilitating RMB 150 billion in auto finance throughput in 2024. This requires continual coordination among buyer, dealer, and lender to meet regulatory requirements and average a 48-hour approval cycle for standard loans.

Platform Development and Maintenance

Cango spends heavily on its digital backbone—notably the Cango Haoche app and dealer management systems—with R&D and IT ops accounting for about 12–15% of FY2024 revenue (~RMB 1.1–1.3 billion on a RMB 9.2 billion top line) to fund continuous UI updates, new product integrations, and data‑security measures; this supports peak loads of tens of thousands of concurrent transactions across China’s 31 provinces.

Dealer Network Management and Training

The company recruits, onboards, and trains dealers to use the Cango platform, with field agents visiting 2,300+ partner dealerships in 2024 to provide hands-on tech support and update sales teams on financing and insurance products; this raised dealer NPS to 42 and cut platform-related errors by 28% year-over-year. This activity strengthens brand loyalty and maintains consistent service quality for end consumers.

Risk Management and Credit Assessment

Risk management centers on refining credit-scoring models with machine learning applied to Cango’s historical loan and transaction dataset (over 12m loans through 2024), improving default prediction and pricing.

Cango monitors portfolio KPIs—90+ DPD, NPL ratio (~2.8% in 2024), recovery rates—and uses real-time repayment signals to trigger proactive collections, protecting bank partner trust and limiting losses.

- 12m loans analyzed through 2024

- NPL ~2.8% (2024)

- Real-time repayment monitoring

- ML-driven credit score updates

- Proactive collections to preserve partner trust

Used Car Transaction Facilitation

Cango: AI-driven auto-finance platform — RMB150B throughput, 1.2M apps, 2.8% NPL

Cango runs end-to-end auto-finance origination (1.2m apps; RMB150B throughput 2024), R&D/IT ~12–15% revenue (~RMB1.1–1.3B on RMB9.2B), dealer onboarding (2,300+ sites), ML credit models on 12m loans, NPL ~2.8% (2024), and used-car ops (200k listings; China used-car market ~28m transactions 2024).

| Metric | 2024 Value |

|---|---|

| Loan apps | 1.2m |

| Throughput | RMB150B |

| Revenue | RMB9.2B |

| R&D/IT spend | 12–15% (~RMB1.1–1.3B) |

| Loans analyzed | 12m |

| NPL | ~2.8% |

| Dealers visited | 2,300+ |

| Used listings | 200k |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact Cango Business Model Canvas you will receive after purchase—no mockups or samples. When you complete your order, you'll download this same professionally formatted file, ready to edit and present in Word and Excel. What you see is the final deliverable, fully structured and complete—no hidden content or surprises.