Cango SWOT Analysis

Make Insightful Decisions Backed by Expert Research

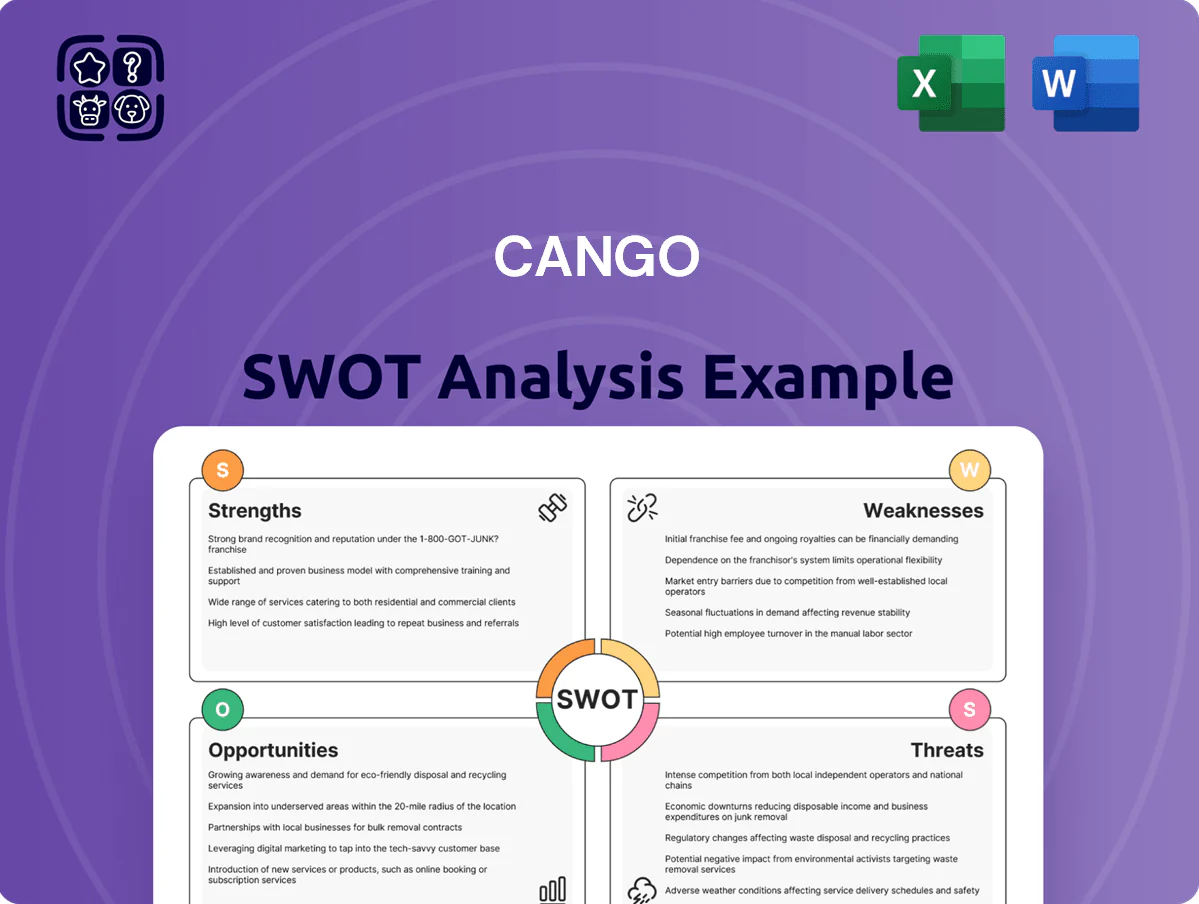

Cango’s SWOT snapshot highlights robust digital lending capabilities and strategic partnerships, counterbalanced by regulatory volatility and competitive pressure; for a full, research-backed breakdown with financial context and actionable recommendations, purchase the complete SWOT analysis—includes editable Word and Excel files to support investment decisions and strategic planning.

Strengths

Extensive Dealer Network

Cango maintains a robust presence across China, especially in Tier 3–4 cities where car ownership grew 6.8% in 2024 and remains above urban average; this reach covers roughly 12,000 small dealers as of Dec 2025. By linking these dealers to centralized financing and supply-chain tools, Cango creates a durable competitive moat that cut acquisition costs and raised loan origination volumes to RMB 38.5 billion in 2025. The dealer network is a vital gateway for OEMs: Cango-enabled sales accounted for an estimated 9% of regional passenger-vehicle volume in 2025, easing manufacturers’ access to fragmented markets.

Platform-Centric Business Model

The Cango Haoche platform shifted Cango from a pure finance intermediary to a transaction facilitator, integrating vehicle sourcing, logistics and financing into one digital ecosystem that handled over RMB 120 billion gross transaction value in 2024.

Advanced Data Analytics

Cango uses a proprietary credit-assessment engine trained on 10+ years and ~15 million auto-loan records to score borrowers, enabling decisioning in minutes versus days at regional banks.

That tech drove a reported 2024 net default rate near 2.1%, roughly half typical regional-bank auto portfolios, boosting origination velocity and margins.

These analytics attracted institutional funding: by Q4 2024 Cango had >¥20 billion in third-party loan commitments from banks and asset managers seeking stable, risk-adjusted auto returns.

Strategic NEV Partnerships

Efficient Cost Structure

Cango: 12K dealers, RMB38.5B loans, 2.1% defaults, 35% NEV share, ¥20B+ funding

Cango’s strengths: 12,000-dealer reach in Tier 3–4 China; RMB 38.5B loan originations and RMB 120B GTV (2024–25); proprietary credit engine on ~15M records yielding ~2.1% net default (2024); >¥20B third-party funding (Q4 2024); 35% NEV share capture and tailored battery loans; SG&A down 18% (2022–24), cash burn $12M Q4 2024.

| Metric | Value |

|---|---|

| Dealers (Dec 2025) | 12,000 |

| Loan originations (2025) | RMB 38.5B |

| GTV (2024) | RMB 120B |

| Credit records | ~15M |

| Net default (2024) | ~2.1% |

| Third-party funding (Q4 2024) | ¥20B+ |

| NEV share (2024) | 35% |

| SG&A change (2022–24) | -18% |

| Cash burn (Q4 2024) | $12M |

What is included in the product

Provides a concise SWOT overview of Cango, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a compact SWOT snapshot of Cango for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Revenue Concentration Risks

Declining Legacy Finance Income

The traditional loan-facilitation arm has shrunk: finance income fell 37% year-on-year to RMB 1.2 billion in 2024, as OEMs (manufacturers) moved to direct financing, cutting Cango’s high-margin legacy share.

As that segment declines, Cango must scale platform services fast — platform revenue rose just 8% in 2024, highlighting a profitability gap versus legacy margins.

The transition squeezed net margin to -4.3% in 2024 and pressured investor confidence, reflected in a 46% drop in market cap since 2022.

Limited Brand Awareness

In China’s crowded auto internet market, Cango (NYSE: CANG) lacks consumer brand reach comparable to Autohome (Autohome Inc.) and Dongchedi, with Autohome reporting 2024 monthly active users of ~60 million vs Cango’s consumer touchpoints mainly via 10,000+ dealer partners; most buyers find Cango through dealers, not direct search.

This weak direct-to-consumer equity prevents Cango from bypassing intermediaries and likely trims retail margin capture; Cango’s 2024 gross margin on retail services was ~18%, below pure consumer platforms that can exceed 25%.

Exposure to Credit Volatility

- Model sophistication helps, but macro risk persists.

- GDP 5.2% (2024) and 3.1% credit costs signal sensitivity.

- ~40% funding from banks/trusts increases counterparty exposure.

Heavy Dependence on Third-Party Dealers

Cango relies heavily on ~12,000 independent dealers nationwide; dealer-originated loans made up about 68% of loan volume in 2024, so any shift to rivals or OEM (original equipment manufacturer) consolidation could cut core distribution quickly.

That dependence reduces Cango’s control over end-customer service and dealer pricing, raising reputational and quality risks and pressuring margins if Cango must incentivize loyalty.

- 12,000 dealers; 68% loan volume (2024)

- High churn risk if dealers defect

- Limited control over customer experience

- OEM consolidation could close primary channel

Transaction slump drags margin into negative as finance income, market cap plunge

| Metric | 2024 |

|---|---|

| Transaction share | 62% |

| Transactions H2 YoY | -14% |

| Finance income | RMB1.2bn (-37%) |

| Net margin | -4.3% |

| Dealers / loan vol | 12,000 / 68% |

| Credit costs | 3.1% |

| Bank/trust funding | ~40% |

| China GDP | 5.2% |

What You See Is What You Get

Cango SWOT Analysis

This is the actual Cango SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live preview of the real analysis file, structured and ready to use for decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Cango’s SWOT snapshot highlights robust digital lending capabilities and strategic partnerships, counterbalanced by regulatory volatility and competitive pressure; for a full, research-backed breakdown with financial context and actionable recommendations, purchase the complete SWOT analysis—includes editable Word and Excel files to support investment decisions and strategic planning.

Strengths

Extensive Dealer Network

Cango maintains a robust presence across China, especially in Tier 3–4 cities where car ownership grew 6.8% in 2024 and remains above urban average; this reach covers roughly 12,000 small dealers as of Dec 2025. By linking these dealers to centralized financing and supply-chain tools, Cango creates a durable competitive moat that cut acquisition costs and raised loan origination volumes to RMB 38.5 billion in 2025. The dealer network is a vital gateway for OEMs: Cango-enabled sales accounted for an estimated 9% of regional passenger-vehicle volume in 2025, easing manufacturers’ access to fragmented markets.

Platform-Centric Business Model

The Cango Haoche platform shifted Cango from a pure finance intermediary to a transaction facilitator, integrating vehicle sourcing, logistics and financing into one digital ecosystem that handled over RMB 120 billion gross transaction value in 2024.

Advanced Data Analytics

Cango uses a proprietary credit-assessment engine trained on 10+ years and ~15 million auto-loan records to score borrowers, enabling decisioning in minutes versus days at regional banks.

That tech drove a reported 2024 net default rate near 2.1%, roughly half typical regional-bank auto portfolios, boosting origination velocity and margins.

These analytics attracted institutional funding: by Q4 2024 Cango had >¥20 billion in third-party loan commitments from banks and asset managers seeking stable, risk-adjusted auto returns.

Strategic NEV Partnerships

Efficient Cost Structure

Cango: 12K dealers, RMB38.5B loans, 2.1% defaults, 35% NEV share, ¥20B+ funding

Cango’s strengths: 12,000-dealer reach in Tier 3–4 China; RMB 38.5B loan originations and RMB 120B GTV (2024–25); proprietary credit engine on ~15M records yielding ~2.1% net default (2024); >¥20B third-party funding (Q4 2024); 35% NEV share capture and tailored battery loans; SG&A down 18% (2022–24), cash burn $12M Q4 2024.

| Metric | Value |

|---|---|

| Dealers (Dec 2025) | 12,000 |

| Loan originations (2025) | RMB 38.5B |

| GTV (2024) | RMB 120B |

| Credit records | ~15M |

| Net default (2024) | ~2.1% |

| Third-party funding (Q4 2024) | ¥20B+ |

| NEV share (2024) | 35% |

| SG&A change (2022–24) | -18% |

| Cash burn (Q4 2024) | $12M |

What is included in the product

Provides a concise SWOT overview of Cango, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a compact SWOT snapshot of Cango for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Revenue Concentration Risks

Declining Legacy Finance Income

The traditional loan-facilitation arm has shrunk: finance income fell 37% year-on-year to RMB 1.2 billion in 2024, as OEMs (manufacturers) moved to direct financing, cutting Cango’s high-margin legacy share.

As that segment declines, Cango must scale platform services fast — platform revenue rose just 8% in 2024, highlighting a profitability gap versus legacy margins.

The transition squeezed net margin to -4.3% in 2024 and pressured investor confidence, reflected in a 46% drop in market cap since 2022.

Limited Brand Awareness

In China’s crowded auto internet market, Cango (NYSE: CANG) lacks consumer brand reach comparable to Autohome (Autohome Inc.) and Dongchedi, with Autohome reporting 2024 monthly active users of ~60 million vs Cango’s consumer touchpoints mainly via 10,000+ dealer partners; most buyers find Cango through dealers, not direct search.

This weak direct-to-consumer equity prevents Cango from bypassing intermediaries and likely trims retail margin capture; Cango’s 2024 gross margin on retail services was ~18%, below pure consumer platforms that can exceed 25%.

Exposure to Credit Volatility

- Model sophistication helps, but macro risk persists.

- GDP 5.2% (2024) and 3.1% credit costs signal sensitivity.

- ~40% funding from banks/trusts increases counterparty exposure.

Heavy Dependence on Third-Party Dealers

Cango relies heavily on ~12,000 independent dealers nationwide; dealer-originated loans made up about 68% of loan volume in 2024, so any shift to rivals or OEM (original equipment manufacturer) consolidation could cut core distribution quickly.

That dependence reduces Cango’s control over end-customer service and dealer pricing, raising reputational and quality risks and pressuring margins if Cango must incentivize loyalty.

- 12,000 dealers; 68% loan volume (2024)

- High churn risk if dealers defect

- Limited control over customer experience

- OEM consolidation could close primary channel

Transaction slump drags margin into negative as finance income, market cap plunge

| Metric | 2024 |

|---|---|

| Transaction share | 62% |

| Transactions H2 YoY | -14% |

| Finance income | RMB1.2bn (-37%) |

| Net margin | -4.3% |

| Dealers / loan vol | 12,000 / 68% |

| Credit costs | 3.1% |

| Bank/trust funding | ~40% |

| China GDP | 5.2% |

What You See Is What You Get

Cango SWOT Analysis

This is the actual Cango SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live preview of the real analysis file, structured and ready to use for decision-making.