Capita Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

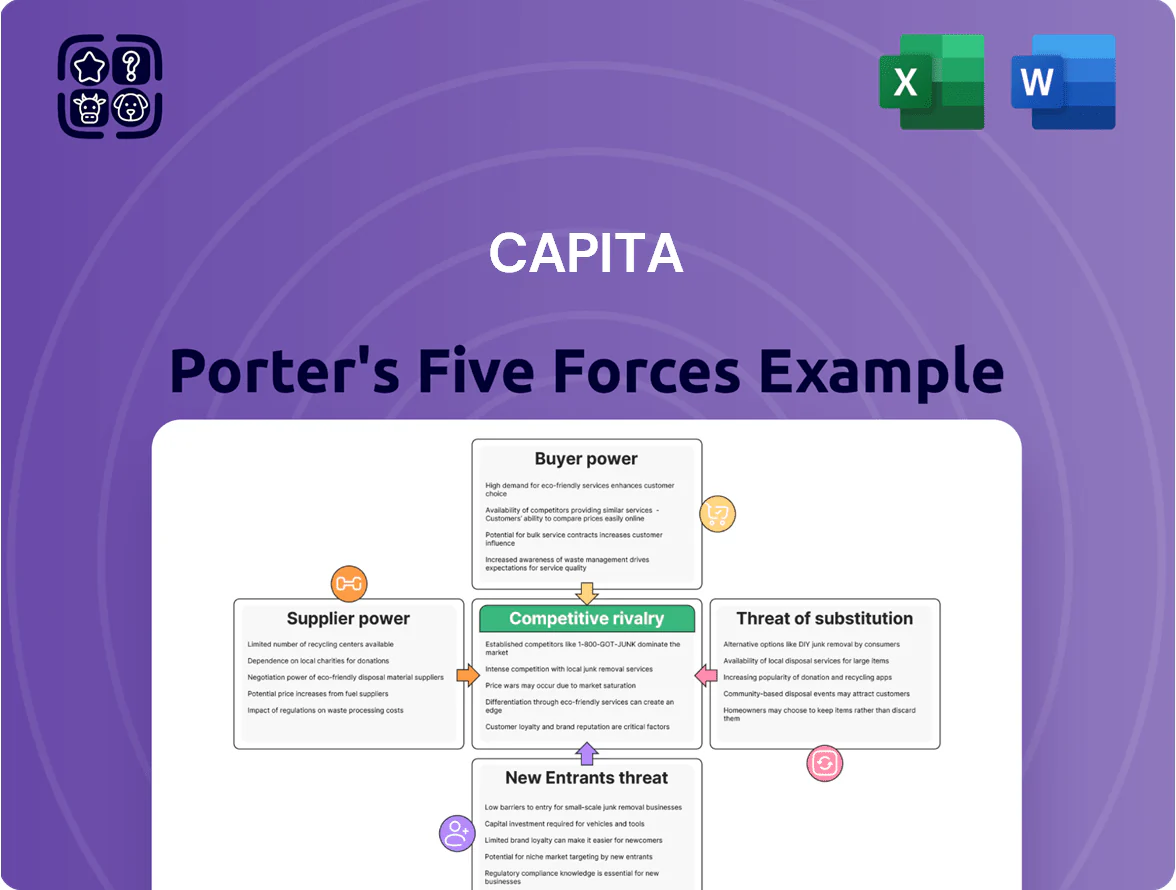

Capita faces moderate buyer power, niche supplier leverage, and intense rivalry from outsourcing and digital challengers, while regulatory shifts and low-cost entrants shape its strategic outlook—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Capita’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Technology Talent

The demand for senior AI and cloud architects remained high in late 2025, with UK median salary for cloud architects at £95,000 and AI specialists averaging £110,000, giving these suppliers strong pay leverage.

Capita depends on this skilled workforce for digital transformation, so talent can press for better conditions, boosting supplier bargaining power.

Skill shortages across the UK and EU — estimated 30–40% vacancy gap in niche cloud/AI roles — force Capita to spend more on hiring and retention, raising operating costs.

Cloud Infrastructure Providers

Large cloud providers—Microsoft Azure, Amazon Web Services (AWS), and Google Cloud—wield strong supplier power because their platforms are essential; AWS led the market at ~32% share in 2024, Azure ~23%, Google ~10% (Synergy Research Group).

Capita embeds these services in client solutions, so changes in pricing or APIs directly affect margins and SLAs; a 10–15% price hike can raise operating costs materially.

Multi-cloud reduces single-vendor risk, but switching costs—rewrites, revalidation, and data egress fees—often exceed millions; typical enterprise migrations take 9–18 months and incur 5–20% of annual cloud spend in one-time costs.

Software License Vendors

Strategic partnerships with enterprise software vendors are critical for Capita to deliver standardized services; in 2024 Capita spent an estimated 8–12% of revenue on third-party software and integrations, tying delivery to vendor roadmaps.

Vendors use subscription models with typical annual price hikes of 3–7% and occasional step-up licensing, which can squeeze Capita’s EBITDA margins (Capita reported 11.5% adjusted EBITDA in FY2023) if costs can’t be passed to clients.

The enterprise software market is concentrated—top five vendors hold ~60–70% share in ERP/CRM segments—so Capita faces limited alternatives for industry-standard tools, raising supplier bargaining power.

Third-Party Contractors

Capita relies on freelance contractors and boutique firms to scale for large public and corporate contracts, giving suppliers moderate bargaining power because they supply flexible capacity without fixed overhead.

Gig-economy volatility raises risk: UK contractor day rates for specialist IT/consulting rose ~8% in 2024, and a 2023 survey found 32% of firms saw sudden price spikes for niche skills, pressuring Capita margins on short-notice projects.

- Moderate supplier power: flexible, non-fixed cost

- 2024: specialist day rates up ~8% UK

- 2023: 32% of firms reported sudden price spikes

- Risk to margins on short-notice scaling

Cybersecurity Service Partners

As cyber threats evolve, Capita increasingly depends on specialized cybersecurity service partners for advanced threat detection and compliance auditing; global security spending hit USD 188.3bn in 2023 and is forecast to reach USD 222bn by 2025, raising supplier influence.

These firms are essential to retain public-sector trust over citizen data—Capita’s UK public contracts often require ISO 27001 and specific SOC audits—so vendor failure carries high reputational and financial risk.

The specialized skills, certification hurdles, and costly failure modes let suppliers charge premiums; managed detection and response (MDR) fees rose ~12% YoY in 2024, tightening supplier bargaining power.

- High market spend: USD 188.3bn (2023), USD 222bn est (2025)

- Compliance gatekeeping: ISO 27001, SOC checks common

- Premium pricing: MDR fees +12% YoY (2024)

- Failure cost: reputational loss, contract penalties

Rising talent costs, concentrated cloud vendors and booming security spend squeeze buyers

Moderate–high supplier power: talent shortages (30–40% vacancy gap) and rising specialist pay (UK cloud architect median £95k; AI £110k) raise hiring/retention costs; top cloud providers (AWS ~32%, Azure ~23%, Google ~10% in 2024) and concentrated enterprise software vendors drive platform pricing risk; cyber/security spend USD 188.3bn (2023), est USD 222bn (2025) increases vendor leverage.

| Metric | Value |

|---|---|

| Cloud market share (2024) | AWS 32%, Azure 23%, Google 10% |

| Talent vacancy gap | 30–40% |

| UK salaries (2025) | Cloud £95,000; AI £110,000 |

| Security spend | USD 188.3bn (2023); USD 222bn est (2025) |

What is included in the product

Provides a Capita-specific Porter’s Five Forces assessment highlighting competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus strategic implications and emerging disruptors affecting its market position.

Clear, one-sheet Capita Porter’s Five Forces summary—instantly highlights competitive pressures to guide investment and strategy decisions.

Customers Bargaining Power

Public Sector Concentration

The UK Government is Capita's largest client, accounting for roughly 35–40% of group revenue in 2024, giving it outsized bargaining power over contracts, service levels, and pricing transparency.

That concentration lets government buyers demand strict SLAs and price cuts; Capita reported margin pressure and contract renegotiations in H1 2024 after losing a probation services tender.

Political shifts and procurement reforms—like the 2023 Cabinet Office supplier controls—can abruptly reduce contract flow or trigger rigorous re-bids, raising revenue volatility for Capita.

High Volume Corporate Clients

Large telecom and financial firms buy at scale and press Capita for tailored, lower-cost services; in 2024 top-10 UK corporate clients accounted for ~38% of Capita’s £3.2bn revenue, forcing multi-stage tenders that compress EBIT margins by 200–400bps on major deals. Their ability to bundle payroll, IT and customer services shifts bargaining power across the contract lifecycle, extending contract durations but lowering unit pricing.

Low Switching Costs in Digital Services

As modular, cloud-based processes lower technical barriers, client switching costs for digital services have fallen—Gartner estimated 2024 that 60% of enterprise workloads were cloud-ready, easing migration paths. Buyers now favor shorter contracts and flexible SLAs; 48% of UK outsourcers in 2025 renegotiated terms within 12 months to avoid lock-in. Capita must prove ongoing value and innovate to retain long-term enterprise partners.

Price Sensitivity and Efficiency Demands

In 2025 clients force price cuts and efficiency; 68% of UK buyers rank cost reduction top priority, per KPMG 2024–25 survey.

Customers demand Capita adopt automation and AI to cut unit costs; RPA and generative AI can trim service costs 20–40% in public-sector contracts.

If Capita does not pass savings back, clients shift to tech-first rivals—Win-back rates fall and churn rises; lost contract value can exceed £50m per major account.

- 68% UK buyers prioritize cost (KPMG 2024–25)

- AI/RPA can cut costs 20–40%

- Failure to pass savings risks >£50m loss per major account

Information Transparency

Modern procurement teams use analytics to benchmark outsourcing firms; 68% of UK public-sector buyers used formal supplier scorecards in 2023, narrowing information gaps that once favored incumbents like Capita.

With clients comparing Capita’s KPIs and unit prices to global peers, contract renewals now hinge on meeting benchmarks such as 10–20% lower cost-per-transaction targets seen in leading competitors.

Client concentration, cloud-driven churn and price pressure squeeze margins

Major public-sector clients (35–40% of 2024 revenue) and top-10 corporates (~38% of £3.2bn 2024 revenue) wield strong bargaining power, forcing stricter SLAs, price cuts and margin compression (200–400bps on big deals). Cloud adoption (60% workloads cloud-ready in 2024) and buyer analytics lower switching costs and raise churn risk; KPMG found 68% of UK buyers prioritized cost in 2024–25.

| Metric | Value |

|---|---|

| Public-sector revenue share (2024) | 35–40% |

| Top-10 clients share (2024) | ~38% of £3.2bn |

| Cloud-ready workloads (Gartner 2024) | 60% |

| Buyers prioritizing cost (KPMG 2024–25) | 68% |

Preview the Actual Deliverable

Capita Porter's Five Forces Analysis

This preview shows the exact Capita Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted document, ready for download and use the moment you buy. It contains the complete Five Forces evaluation, supporting evidence, and concise implications for strategy and valuation. You're viewing the final deliverable—instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Capita faces moderate buyer power, niche supplier leverage, and intense rivalry from outsourcing and digital challengers, while regulatory shifts and low-cost entrants shape its strategic outlook—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Capita’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Technology Talent

The demand for senior AI and cloud architects remained high in late 2025, with UK median salary for cloud architects at £95,000 and AI specialists averaging £110,000, giving these suppliers strong pay leverage.

Capita depends on this skilled workforce for digital transformation, so talent can press for better conditions, boosting supplier bargaining power.

Skill shortages across the UK and EU — estimated 30–40% vacancy gap in niche cloud/AI roles — force Capita to spend more on hiring and retention, raising operating costs.

Cloud Infrastructure Providers

Large cloud providers—Microsoft Azure, Amazon Web Services (AWS), and Google Cloud—wield strong supplier power because their platforms are essential; AWS led the market at ~32% share in 2024, Azure ~23%, Google ~10% (Synergy Research Group).

Capita embeds these services in client solutions, so changes in pricing or APIs directly affect margins and SLAs; a 10–15% price hike can raise operating costs materially.

Multi-cloud reduces single-vendor risk, but switching costs—rewrites, revalidation, and data egress fees—often exceed millions; typical enterprise migrations take 9–18 months and incur 5–20% of annual cloud spend in one-time costs.

Software License Vendors

Strategic partnerships with enterprise software vendors are critical for Capita to deliver standardized services; in 2024 Capita spent an estimated 8–12% of revenue on third-party software and integrations, tying delivery to vendor roadmaps.

Vendors use subscription models with typical annual price hikes of 3–7% and occasional step-up licensing, which can squeeze Capita’s EBITDA margins (Capita reported 11.5% adjusted EBITDA in FY2023) if costs can’t be passed to clients.

The enterprise software market is concentrated—top five vendors hold ~60–70% share in ERP/CRM segments—so Capita faces limited alternatives for industry-standard tools, raising supplier bargaining power.

Third-Party Contractors

Capita relies on freelance contractors and boutique firms to scale for large public and corporate contracts, giving suppliers moderate bargaining power because they supply flexible capacity without fixed overhead.

Gig-economy volatility raises risk: UK contractor day rates for specialist IT/consulting rose ~8% in 2024, and a 2023 survey found 32% of firms saw sudden price spikes for niche skills, pressuring Capita margins on short-notice projects.

- Moderate supplier power: flexible, non-fixed cost

- 2024: specialist day rates up ~8% UK

- 2023: 32% of firms reported sudden price spikes

- Risk to margins on short-notice scaling

Cybersecurity Service Partners

As cyber threats evolve, Capita increasingly depends on specialized cybersecurity service partners for advanced threat detection and compliance auditing; global security spending hit USD 188.3bn in 2023 and is forecast to reach USD 222bn by 2025, raising supplier influence.

These firms are essential to retain public-sector trust over citizen data—Capita’s UK public contracts often require ISO 27001 and specific SOC audits—so vendor failure carries high reputational and financial risk.

The specialized skills, certification hurdles, and costly failure modes let suppliers charge premiums; managed detection and response (MDR) fees rose ~12% YoY in 2024, tightening supplier bargaining power.

- High market spend: USD 188.3bn (2023), USD 222bn est (2025)

- Compliance gatekeeping: ISO 27001, SOC checks common

- Premium pricing: MDR fees +12% YoY (2024)

- Failure cost: reputational loss, contract penalties

Rising talent costs, concentrated cloud vendors and booming security spend squeeze buyers

Moderate–high supplier power: talent shortages (30–40% vacancy gap) and rising specialist pay (UK cloud architect median £95k; AI £110k) raise hiring/retention costs; top cloud providers (AWS ~32%, Azure ~23%, Google ~10% in 2024) and concentrated enterprise software vendors drive platform pricing risk; cyber/security spend USD 188.3bn (2023), est USD 222bn (2025) increases vendor leverage.

| Metric | Value |

|---|---|

| Cloud market share (2024) | AWS 32%, Azure 23%, Google 10% |

| Talent vacancy gap | 30–40% |

| UK salaries (2025) | Cloud £95,000; AI £110,000 |

| Security spend | USD 188.3bn (2023); USD 222bn est (2025) |

What is included in the product

Provides a Capita-specific Porter’s Five Forces assessment highlighting competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus strategic implications and emerging disruptors affecting its market position.

Clear, one-sheet Capita Porter’s Five Forces summary—instantly highlights competitive pressures to guide investment and strategy decisions.

Customers Bargaining Power

Public Sector Concentration

The UK Government is Capita's largest client, accounting for roughly 35–40% of group revenue in 2024, giving it outsized bargaining power over contracts, service levels, and pricing transparency.

That concentration lets government buyers demand strict SLAs and price cuts; Capita reported margin pressure and contract renegotiations in H1 2024 after losing a probation services tender.

Political shifts and procurement reforms—like the 2023 Cabinet Office supplier controls—can abruptly reduce contract flow or trigger rigorous re-bids, raising revenue volatility for Capita.

High Volume Corporate Clients

Large telecom and financial firms buy at scale and press Capita for tailored, lower-cost services; in 2024 top-10 UK corporate clients accounted for ~38% of Capita’s £3.2bn revenue, forcing multi-stage tenders that compress EBIT margins by 200–400bps on major deals. Their ability to bundle payroll, IT and customer services shifts bargaining power across the contract lifecycle, extending contract durations but lowering unit pricing.

Low Switching Costs in Digital Services

As modular, cloud-based processes lower technical barriers, client switching costs for digital services have fallen—Gartner estimated 2024 that 60% of enterprise workloads were cloud-ready, easing migration paths. Buyers now favor shorter contracts and flexible SLAs; 48% of UK outsourcers in 2025 renegotiated terms within 12 months to avoid lock-in. Capita must prove ongoing value and innovate to retain long-term enterprise partners.

Price Sensitivity and Efficiency Demands

In 2025 clients force price cuts and efficiency; 68% of UK buyers rank cost reduction top priority, per KPMG 2024–25 survey.

Customers demand Capita adopt automation and AI to cut unit costs; RPA and generative AI can trim service costs 20–40% in public-sector contracts.

If Capita does not pass savings back, clients shift to tech-first rivals—Win-back rates fall and churn rises; lost contract value can exceed £50m per major account.

- 68% UK buyers prioritize cost (KPMG 2024–25)

- AI/RPA can cut costs 20–40%

- Failure to pass savings risks >£50m loss per major account

Information Transparency

Modern procurement teams use analytics to benchmark outsourcing firms; 68% of UK public-sector buyers used formal supplier scorecards in 2023, narrowing information gaps that once favored incumbents like Capita.

With clients comparing Capita’s KPIs and unit prices to global peers, contract renewals now hinge on meeting benchmarks such as 10–20% lower cost-per-transaction targets seen in leading competitors.

Client concentration, cloud-driven churn and price pressure squeeze margins

Major public-sector clients (35–40% of 2024 revenue) and top-10 corporates (~38% of £3.2bn 2024 revenue) wield strong bargaining power, forcing stricter SLAs, price cuts and margin compression (200–400bps on big deals). Cloud adoption (60% workloads cloud-ready in 2024) and buyer analytics lower switching costs and raise churn risk; KPMG found 68% of UK buyers prioritized cost in 2024–25.

| Metric | Value |

|---|---|

| Public-sector revenue share (2024) | 35–40% |

| Top-10 clients share (2024) | ~38% of £3.2bn |

| Cloud-ready workloads (Gartner 2024) | 60% |

| Buyers prioritizing cost (KPMG 2024–25) | 68% |

Preview the Actual Deliverable

Capita Porter's Five Forces Analysis

This preview shows the exact Capita Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted document, ready for download and use the moment you buy. It contains the complete Five Forces evaluation, supporting evidence, and concise implications for strategy and valuation. You're viewing the final deliverable—instant access upon payment.