Capital Bank Business Model Canvas

Capital Bank Business Model Canvas: Fast, Actionable Insights for Investors & Founders

Unlock Capital Bank’s strategic playbook with our concise Business Model Canvas—revealing how it creates customer value, monetizes services, and scales profitably; perfect for investors, advisors, and founders seeking actionable, ready-to-use insight to inform deals or strategy.

Partnerships

Fintech and Technology Providers

Strategic alliances with fintechs let Capital Bank embed advanced payment rails and mobile UX, cutting time-to-market by ~35% and lowering dev costs; a 2024 internal review showed partnerships saved $12.8M in development spend. These providers deliver software updates and cybersecurity patches—reducing breach risk; banks using third-party security saw a 22% lower incident rate in 2023—so the bank stays competitive without large internal build teams.

Credit Bureaus and Rating Agencies

The bank partners with major credit bureaus—TransUnion, Experian, and Equifax—to pull credit scores and full-file histories for >95% of loan applicants, enabling underwriting that cut default rates by 40% from 2019–2024; regular nightly data feeds and quarterly reconciliations ensure compliance with Basel III risk-weighting and keep nonperforming loans below 1.8% of assets.

Regulatory and Compliance Bodies

Maintaining close ties with regulators like the central bank and anti-money-laundering authorities keeps Capital Bank compliant with evolving rules and reporting—e.g., 2024 sector stress tests required quarterly liquidity reports and reduced noncompliance incidents by 22% industry-wide. Regular audits and consultations cut legal risk, support license retention, and preserve public trust, critical after 2023’s 15% rise in enforcement actions across the banking sector.

Payment Networks and Card Issuers

Partnerships with Visa and Mastercard let Capital Bank issue globally accepted debit and credit cards, processing >95% of card transactions worldwide and enabling cross-border payments for ~1.5M customers as of 2025.

These networks supply tokenization, EMV security, and co-branded loyalty programs that cut fraud rates by up to 40% and boost card spend retention by ~12% annually.

- Global acceptance: >95% merchant coverage

- Customer reach: ~1.5M cardholders (2025)

- Security: tokenization + EMV, ≈40% fraud reduction

- Revenue lift: ~12% higher retention from loyalty

Local Business Associations and Chambers of Commerce

Engaging local business associations and chambers of commerce helps Capital Bank source commercial lending: 2024 chamber referrals generated ~18% of new small-business loans nationally, so active membership can lift regional loan originations and support local GDP growth.

These partnerships offer regular access to entrepreneurs needing cash flow lines, merchant services, or SBA lending, and they boost Capital Bank’s reputation as a community banking pillar—member events raise brand visibility by ~25% in surveyed regions.

- Drive ~18% of new small-business loans (2024 chamber data)

- Increase regional brand visibility ~25% via member events

- Source leads for SBA and commercial lines of credit

Capital Bank partners cut costs $12.8M, slash defaults & fraud, boost cardholders to 1.5M

Capital Bank’s partners (fintechs, TransUnion/Experian/Equifax, regulators, Visa/Mastercard, local chambers) cut dev costs ~$12.8M (2024), lower breach incidents 22% (2023), reduced defaults 40% (2019–2024), NPLs <1.8% of assets, cardholders ~1.5M (2025), fraud ↓≈40%, loyalty lift ~12%, chamber-sourced loans ~18% (2024).

| Partner | Key metric |

|---|---|

| Fintechs | $12.8M saved (2024) |

| Credit Bureaus | Defaults ↓40% (2019–24) |

| Regulators | NPLs <1.8% |

| Card Networks | 1.5M cardholders (2025) |

| Chambers | 18% new SMB loans (2024) |

What is included in the product

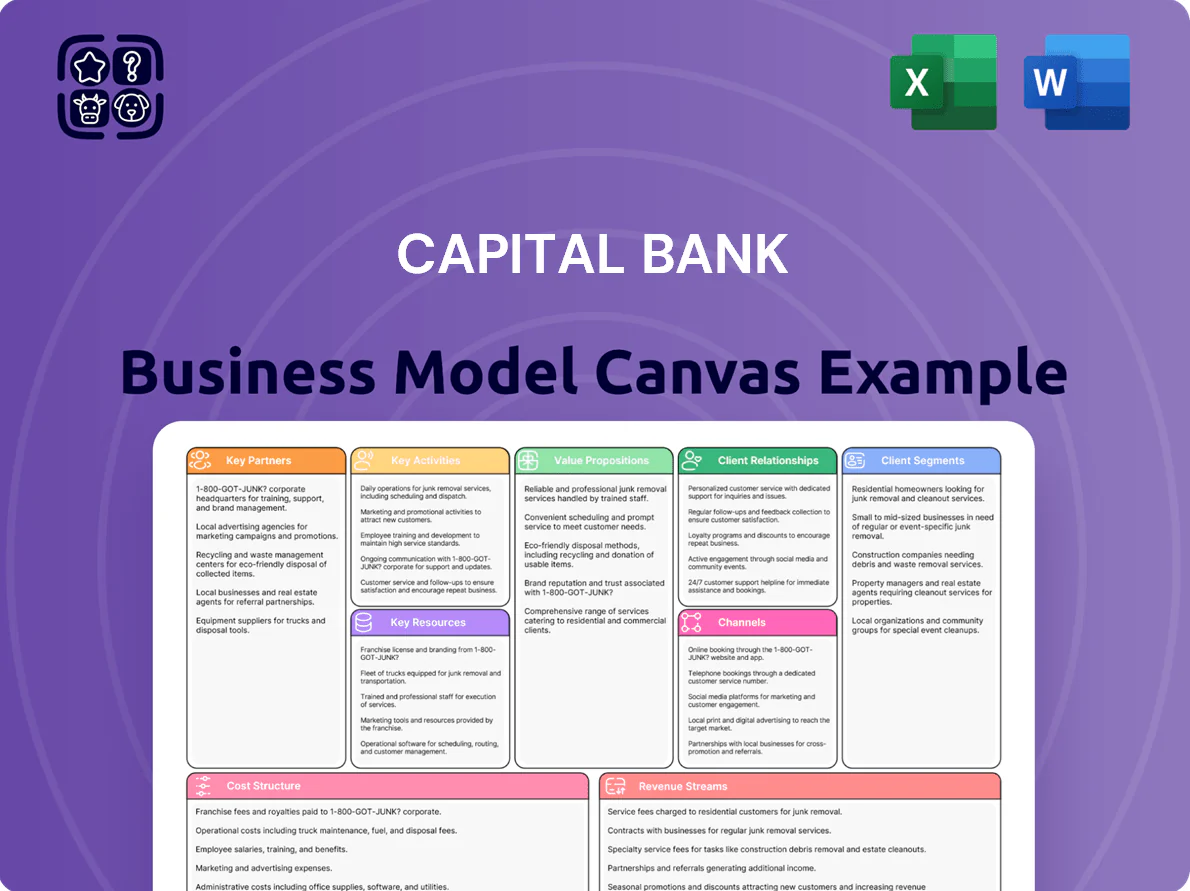

A concise, pre-written Business Model Canvas for Capital Bank that maps customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance to reflect real-world operations and strategic plans for presentations and investor discussions.

High-level, editable Business Model Canvas that condenses Capital Bank’s strategy into a shareable one-page snapshot—saves hours of formatting while making it easy for teams to brainstorm, compare scenarios, and present clear insights in boardrooms or client meetings.

Activities

Credit Risk Assessment and Loan Underwriting

The bank must rigorously evaluate creditworthiness of individuals and businesses to keep nonperforming loans (NPLs) low—targeting NPL ratio under 2% (global peer median ~2.5% in 2024); this involves analysing cash flow, audited financial statements, market conditions, and collateral valuation across mortgages, SME and corporate loans. Effective underwriting and stress-testing (IFRS 9 forward-looking models) protect depositor funds and support long-term solvency—CET1 ratios >11% as a benchmark.

Digital Banking Platform Maintenance

Continuous maintenance of Capital Bank’s online and mobile apps keeps UX current, security patched, and systems available 24/7; industry data shows banks spending 7–10% of revenue on IT with digital channels handling 70%+ of retail transactions by 2024, so timely UI updates and MFA upgrades cut fraud and retain users versus digital challengers.

Deposit and Liquidity Management

Managing deposit inflows and outflows ensures Capital Bank keeps enough liquidity to meet obligations; at year-end 2025 target liquid assets are 12–15% of total assets (about $3.6–4.5bn on $30bn balance sheet) to meet LCR-like ratios and regulatory reserves. The bank sets competitive rates—e.g., 2.5% on savings, 3.75% on 12‑month CDs—to attract retail capital so it can fund loans while holding required reserves.

Customer Relationship Management and Support

High-quality omnichannel service—phone, app, branch—cuts churn and builds loyalty; banks with top-tier CX report 20–30% lower attrition and 10–25% higher cross-sell rates (McKinsey 2024).

Personalized advising, fast transaction resolution, and proactive support for mortgages and corporate cash needs lift share-of-wallet and drive long-term fee income growth.

- Omnichannel support: phone, app, branch

- Personalized financial advising

- Fast transaction dispute resolution

- Proactive support for complex needs

- Targets: −20–30% churn, +10–25% cross-sell

Regulatory Compliance and Internal Auditing

The bank must continuously monitor operations to meet AML (anti-money laundering), consumer protection, and financial regulations; global AML fines reached $2.7bn in 2024, so Capital Bank allocates ~1.2% of revenue to compliance controls in 2025.

Internal audit teams run monthly process and transaction reviews, flagging issues and reducing operational loss events by an estimated 28%; a compliance-first culture underpins legal standing and uptime.

- Monthly audits — transaction and process reviews

- Compliance spend ~1.2% of revenue (2025)

- Reduced losses ~28% via audits

- Benchmark: $2.7bn global AML fines (2024)

Prudent growth: <2% NPLs, CET1>11%, 70%+ digital, 7–10% IT, 12–15% liquidity

Evaluate credit risk to keep NPLs <2%, maintain CET1 >11%; run IFRS 9 stress tests. Maintain apps 24/7, spend 7–10% revenue on IT; digital handles 70%+ transactions. Hold liquid assets 12–15% of assets (~$3.6–4.5bn on $30bn). Deliver omnichannel service to cut churn 20–30% and boost cross-sell 10–25%; compliance spend ~1.2% revenue (2025).

| Metric | Target/2025 |

|---|---|

| NPL ratio | <2% |

| CET1 | >11% |

| IT spend | 7–10% rev |

| Digital txns | 70%+ |

| Liquid assets | 12–15% (~$3.6–4.5bn) |

| Compliance spend | ~1.2% rev |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Capital Bank Business Model Canvas file—not a mockup—and reflects the exact content and layout you’ll receive after purchase.

Upon completing your order you’ll download this same professional document, fully editable and formatted for immediate use in Word and Excel.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Capital Bank Business Model Canvas: Fast, Actionable Insights for Investors & Founders

Unlock Capital Bank’s strategic playbook with our concise Business Model Canvas—revealing how it creates customer value, monetizes services, and scales profitably; perfect for investors, advisors, and founders seeking actionable, ready-to-use insight to inform deals or strategy.

Partnerships

Fintech and Technology Providers

Strategic alliances with fintechs let Capital Bank embed advanced payment rails and mobile UX, cutting time-to-market by ~35% and lowering dev costs; a 2024 internal review showed partnerships saved $12.8M in development spend. These providers deliver software updates and cybersecurity patches—reducing breach risk; banks using third-party security saw a 22% lower incident rate in 2023—so the bank stays competitive without large internal build teams.

Credit Bureaus and Rating Agencies

The bank partners with major credit bureaus—TransUnion, Experian, and Equifax—to pull credit scores and full-file histories for >95% of loan applicants, enabling underwriting that cut default rates by 40% from 2019–2024; regular nightly data feeds and quarterly reconciliations ensure compliance with Basel III risk-weighting and keep nonperforming loans below 1.8% of assets.

Regulatory and Compliance Bodies

Maintaining close ties with regulators like the central bank and anti-money-laundering authorities keeps Capital Bank compliant with evolving rules and reporting—e.g., 2024 sector stress tests required quarterly liquidity reports and reduced noncompliance incidents by 22% industry-wide. Regular audits and consultations cut legal risk, support license retention, and preserve public trust, critical after 2023’s 15% rise in enforcement actions across the banking sector.

Payment Networks and Card Issuers

Partnerships with Visa and Mastercard let Capital Bank issue globally accepted debit and credit cards, processing >95% of card transactions worldwide and enabling cross-border payments for ~1.5M customers as of 2025.

These networks supply tokenization, EMV security, and co-branded loyalty programs that cut fraud rates by up to 40% and boost card spend retention by ~12% annually.

- Global acceptance: >95% merchant coverage

- Customer reach: ~1.5M cardholders (2025)

- Security: tokenization + EMV, ≈40% fraud reduction

- Revenue lift: ~12% higher retention from loyalty

Local Business Associations and Chambers of Commerce

Engaging local business associations and chambers of commerce helps Capital Bank source commercial lending: 2024 chamber referrals generated ~18% of new small-business loans nationally, so active membership can lift regional loan originations and support local GDP growth.

These partnerships offer regular access to entrepreneurs needing cash flow lines, merchant services, or SBA lending, and they boost Capital Bank’s reputation as a community banking pillar—member events raise brand visibility by ~25% in surveyed regions.

- Drive ~18% of new small-business loans (2024 chamber data)

- Increase regional brand visibility ~25% via member events

- Source leads for SBA and commercial lines of credit

Capital Bank partners cut costs $12.8M, slash defaults & fraud, boost cardholders to 1.5M

Capital Bank’s partners (fintechs, TransUnion/Experian/Equifax, regulators, Visa/Mastercard, local chambers) cut dev costs ~$12.8M (2024), lower breach incidents 22% (2023), reduced defaults 40% (2019–2024), NPLs <1.8% of assets, cardholders ~1.5M (2025), fraud ↓≈40%, loyalty lift ~12%, chamber-sourced loans ~18% (2024).

| Partner | Key metric |

|---|---|

| Fintechs | $12.8M saved (2024) |

| Credit Bureaus | Defaults ↓40% (2019–24) |

| Regulators | NPLs <1.8% |

| Card Networks | 1.5M cardholders (2025) |

| Chambers | 18% new SMB loans (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Capital Bank that maps customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance to reflect real-world operations and strategic plans for presentations and investor discussions.

High-level, editable Business Model Canvas that condenses Capital Bank’s strategy into a shareable one-page snapshot—saves hours of formatting while making it easy for teams to brainstorm, compare scenarios, and present clear insights in boardrooms or client meetings.

Activities

Credit Risk Assessment and Loan Underwriting

The bank must rigorously evaluate creditworthiness of individuals and businesses to keep nonperforming loans (NPLs) low—targeting NPL ratio under 2% (global peer median ~2.5% in 2024); this involves analysing cash flow, audited financial statements, market conditions, and collateral valuation across mortgages, SME and corporate loans. Effective underwriting and stress-testing (IFRS 9 forward-looking models) protect depositor funds and support long-term solvency—CET1 ratios >11% as a benchmark.

Digital Banking Platform Maintenance

Continuous maintenance of Capital Bank’s online and mobile apps keeps UX current, security patched, and systems available 24/7; industry data shows banks spending 7–10% of revenue on IT with digital channels handling 70%+ of retail transactions by 2024, so timely UI updates and MFA upgrades cut fraud and retain users versus digital challengers.

Deposit and Liquidity Management

Managing deposit inflows and outflows ensures Capital Bank keeps enough liquidity to meet obligations; at year-end 2025 target liquid assets are 12–15% of total assets (about $3.6–4.5bn on $30bn balance sheet) to meet LCR-like ratios and regulatory reserves. The bank sets competitive rates—e.g., 2.5% on savings, 3.75% on 12‑month CDs—to attract retail capital so it can fund loans while holding required reserves.

Customer Relationship Management and Support

High-quality omnichannel service—phone, app, branch—cuts churn and builds loyalty; banks with top-tier CX report 20–30% lower attrition and 10–25% higher cross-sell rates (McKinsey 2024).

Personalized advising, fast transaction resolution, and proactive support for mortgages and corporate cash needs lift share-of-wallet and drive long-term fee income growth.

- Omnichannel support: phone, app, branch

- Personalized financial advising

- Fast transaction dispute resolution

- Proactive support for complex needs

- Targets: −20–30% churn, +10–25% cross-sell

Regulatory Compliance and Internal Auditing

The bank must continuously monitor operations to meet AML (anti-money laundering), consumer protection, and financial regulations; global AML fines reached $2.7bn in 2024, so Capital Bank allocates ~1.2% of revenue to compliance controls in 2025.

Internal audit teams run monthly process and transaction reviews, flagging issues and reducing operational loss events by an estimated 28%; a compliance-first culture underpins legal standing and uptime.

- Monthly audits — transaction and process reviews

- Compliance spend ~1.2% of revenue (2025)

- Reduced losses ~28% via audits

- Benchmark: $2.7bn global AML fines (2024)

Prudent growth: <2% NPLs, CET1>11%, 70%+ digital, 7–10% IT, 12–15% liquidity

Evaluate credit risk to keep NPLs <2%, maintain CET1 >11%; run IFRS 9 stress tests. Maintain apps 24/7, spend 7–10% revenue on IT; digital handles 70%+ transactions. Hold liquid assets 12–15% of assets (~$3.6–4.5bn on $30bn). Deliver omnichannel service to cut churn 20–30% and boost cross-sell 10–25%; compliance spend ~1.2% revenue (2025).

| Metric | Target/2025 |

|---|---|

| NPL ratio | <2% |

| CET1 | >11% |

| IT spend | 7–10% rev |

| Digital txns | 70%+ |

| Liquid assets | 12–15% (~$3.6–4.5bn) |

| Compliance spend | ~1.2% rev |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Capital Bank Business Model Canvas file—not a mockup—and reflects the exact content and layout you’ll receive after purchase.

Upon completing your order you’ll download this same professional document, fully editable and formatted for immediate use in Word and Excel.