Capital Senior Living PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, demographic trends, and regulatory pressures are shaping Capital Senior Living’s outlook in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access detailed risk assessments, scenario-driven insights, and ready-to-use recommendations that sharpen your competitive and investment decisions.

Political factors

Medicare and Medicaid reimbursement policies

Federal and state funding levels for senior care, including Medicare/Medicaid covering roughly 70% of long-term care spending nationally, directly affect Capital Senior Living’s assisted living and memory care revenue streams.

Changes in reimbursement rates or Medicaid eligibility in late 2025—where several states proposed 3–6% rate adjustments—can render some community locations financially unviable.

Investors track legislative shifts closely; a 1% reimbursement cut can compress operating margins by an estimated 50–150 basis points for facilities with high Medicaid mix.

Governmental healthcare reform initiatives

Ongoing debates over national healthcare infrastructure and senior support systems create regulatory uncertainty for Capital Senior Living; CMS rule changes and potential Medicaid/Medicare expansions could affect reimbursement rates for skilled care, while 2024 proposals targeting staffing ratios (e.g., bills in Congress and state-level mandates in 12 states) raise compliance costs. Legislative shifts in Washington directly influence private-pay occupancy stability—U.S. senior population 65+ reached 59.2M in 2023, up 3.5% YoY—requiring agile strategic planning.

State-level licensing and certification requirements

Each US state enforces distinct licensing and certification rules for senior living, creating a complex compliance patchwork that Capital Senior Living must manage across its ~100 leased/operated communities; noncompliance risks fines or closures—e.g., average state inspection frequencies rose ~12% from 2019–2023. Political pressure to tighten safety standards has driven stricter protocols and more frequent inspections, increasing compliance costs by an estimated 3–5% of operating expenses in recent years. Navigating regional political climates is essential to retain operational licenses and protect brand reputation, as enforcement actions can reduce occupancy—industry-wide vacancy impacts averaged 2–4 percentage points after major enforcement events in 2022–2024.

Immigration policies and labor availability

Political decisions on work visas and immigration reform directly affect supply of nurses and CNAs; US DHS data through 2024 shows foreign-born healthcare workers make up about 17% of the workforce, so visa constraints worsen shortages.

Restrictive policies can push vacancy rates above the industry average 7.5% (2023) raising wage inflation—median caregiver wage rose ~6.2% in 2024—boosting operational costs for Capital Senior Living.

Capital Senior Living should lobby for expanded H-2B/H-1B access and streamlined credential recognition to protect service quality and limit staffing-driven margin erosion.

- Foreign-born share of healthcare workforce ~17% (2024)

- Industry vacancy rate ~7.5% (2023)

- Median caregiver wage growth ~6.2% (2024)

- Advocate for expanded visas and credentialing reforms

Taxation and fiscal policy changes

- 5 states increased corporate tax impacts ~1–2% revenue

- Multiple local abatements expire end-2025

- LIHTC 2024 allocations support affordable projects but competitive

- Plan for 100–200 bps tax shock on NOI

Policy, staffing & visa pressures threaten LTC margins and drive wage inflation

Political factors: Federal/state reimbursement changes (Medicaid/Medicare ~70% of LTC spending) and proposed 3–6% state rate shifts in late 2025 can cut margins 50–150 bps; 12 states’ staffing mandate proposals raise compliance costs ~3–5% of OPEX; visa limits (foreign-born healthcare ~17% in 2024) exacerbate shortages, pushing vacancy (~7.5% in 2023) and wage growth (~6.2% in 2024).

| Metric | Value |

|---|---|

| Medicaid/Medicare share | ~70% |

| State rate proposals | 3–6% |

| Foreign-born HCWs (2024) | ~17% |

| Industry vacancy (2023) | ~7.5% |

| Caregiver wage growth (2024) | ~6.2% |

What is included in the product

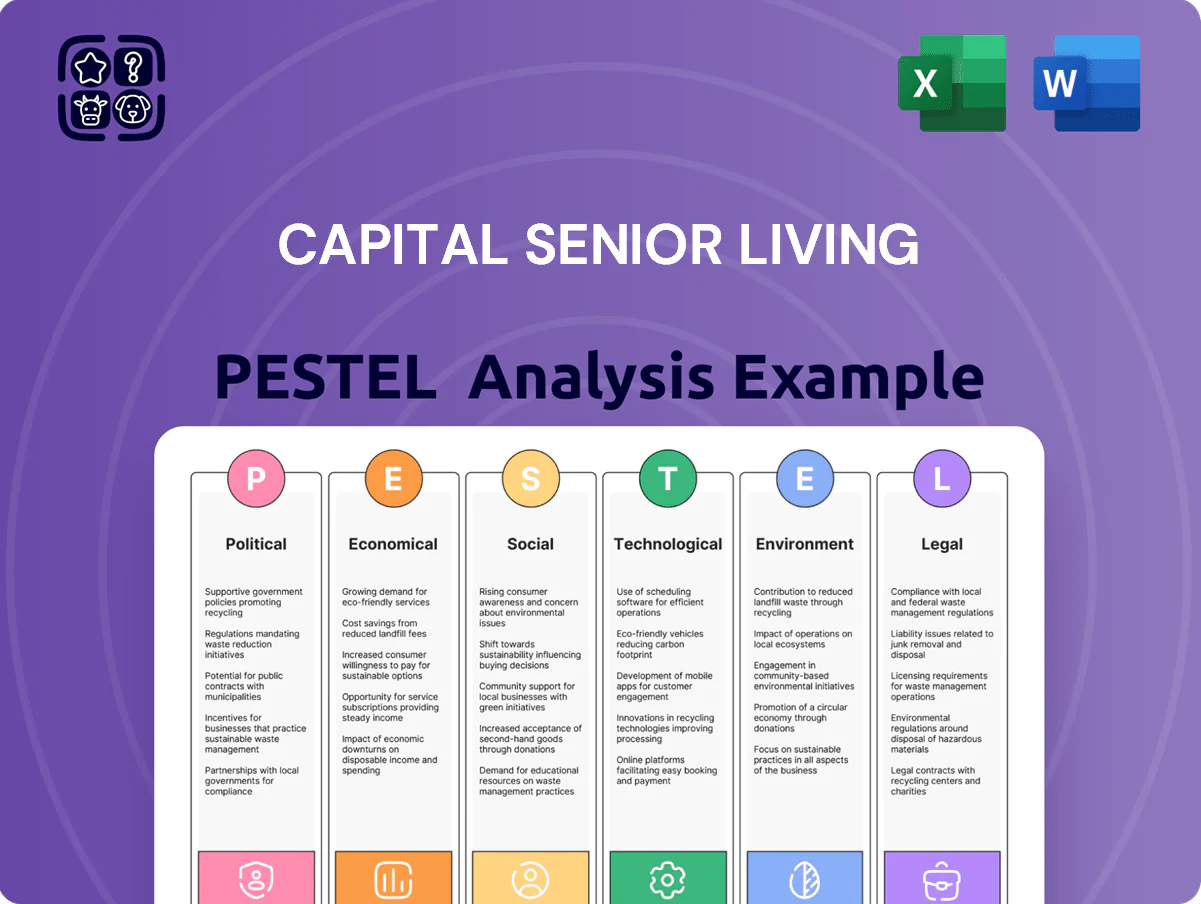

Explores how macro-environmental factors uniquely affect Capital Senior Living across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by current data and forward-looking insights to inform executives, investors, and consultants on risks, opportunities, and scenario planning.

A concise, shareable PESTLE summary for Capital Senior Living that’s visually segmented by category, written in plain language to ease meeting reference, support external risk discussions, and be dropped into presentations or client reports.

Economic factors

Interest rate environment and capital costs

As a capital-intensive operator, Capital Senior Living faces heightened borrowing costs: average 10-year Treasury yields rose above 4.5% in 2025, pushing senior living cap rates up ~75–100 bps industrywide and increasing blended borrowing costs to roughly 6–8% for comparable peers.

High rates pressured debt service coverage ratios in 2025—many operators report DSCRs slipping below 1.5—forcing Capital Senior Living to prioritize refinancing, covenant management, and selective renovation spend to preserve liquidity for strategic growth.

Inflationary pressures on operating expenses

Consumer discretionary income and wealth

The demand for private-pay senior housing for Capital Senior Living hinges on discretionary income and wealth of seniors and their adult children; in 2024 median net worth for households aged 65+ in the US was about $319,100, influencing move-in ability. Housing market swings—US home price index rose ~3% YoY in 2024—plus a roughly 20% rebound in S&P 500 from 2022 lows affect liquidity for buyouts or home sales. Economic stability in this cohort drives occupancy and same-store revenue, with occupancy for private-pay providers averaging ~78–82% in 2024.

Labor market dynamics and wage competition

- Healthcare job openings ~1.8M (2024)

- Labor ≈60% of operating expenses (2024 industry avg)

- Capital cited labor pressure in 2024 10-K

- 10% lower turnover materially reduces costs

Real estate market trends and property values

The valuation of Capital Senior Living’s real estate is tied to US commercial property trends; national multifamily cap rates averaged about 5.1% in H2 2025, affecting asset values and borrowing costs.

Regional supply-demand imbalances—Sun Belt occupancy for senior housing near 88–92% in 2024–2025—create both competition in growth markets and opportunistic acquisition targets in weaker metros.

Active monitoring of local cycles enabled portfolio moves in 2024: selective divestitures raised liquidity by roughly $45m and funded repositioning into higher-yield assets.

- Cap rates ~5.1% (H2 2025)

- Senior housing occupancy 88–92% (2024–2025)

- $45m liquidity from 2024 divestitures

Rising Rates and Inflation Squeeze Margins: Borrowing Costs 6–8%, Labor ~60%

Higher interest rates (10-yr >4.5% in 2025) raised blended borrowing costs to ~6–8%, pressuring DSCRs (<1.5) and cap rates (~+75–100 bps); operating inflation (medical CPI +3.6%, food +5% YoY 2025) and wage inflation (~6–8% 2024–2025) pushed labor to ~60% of expenses, reducing margins while occupancy varied 78–92% across markets.

| Metric | Value |

|---|---|

| 10-yr Treasury (2025) | >4.5% |

| Borrowing cost | 6–8% |

| Labor % op exp (2024) | ~60% |

| Occupancy | 78–92% |

What You See Is What You Get

Capital Senior Living PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the Capital Senior Living PESTLE Analysis displayed includes complete political, economic, social, technological, legal, and environmental factors, structured for immediate application in strategy or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, demographic trends, and regulatory pressures are shaping Capital Senior Living’s outlook in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access detailed risk assessments, scenario-driven insights, and ready-to-use recommendations that sharpen your competitive and investment decisions.

Political factors

Medicare and Medicaid reimbursement policies

Federal and state funding levels for senior care, including Medicare/Medicaid covering roughly 70% of long-term care spending nationally, directly affect Capital Senior Living’s assisted living and memory care revenue streams.

Changes in reimbursement rates or Medicaid eligibility in late 2025—where several states proposed 3–6% rate adjustments—can render some community locations financially unviable.

Investors track legislative shifts closely; a 1% reimbursement cut can compress operating margins by an estimated 50–150 basis points for facilities with high Medicaid mix.

Governmental healthcare reform initiatives

Ongoing debates over national healthcare infrastructure and senior support systems create regulatory uncertainty for Capital Senior Living; CMS rule changes and potential Medicaid/Medicare expansions could affect reimbursement rates for skilled care, while 2024 proposals targeting staffing ratios (e.g., bills in Congress and state-level mandates in 12 states) raise compliance costs. Legislative shifts in Washington directly influence private-pay occupancy stability—U.S. senior population 65+ reached 59.2M in 2023, up 3.5% YoY—requiring agile strategic planning.

State-level licensing and certification requirements

Each US state enforces distinct licensing and certification rules for senior living, creating a complex compliance patchwork that Capital Senior Living must manage across its ~100 leased/operated communities; noncompliance risks fines or closures—e.g., average state inspection frequencies rose ~12% from 2019–2023. Political pressure to tighten safety standards has driven stricter protocols and more frequent inspections, increasing compliance costs by an estimated 3–5% of operating expenses in recent years. Navigating regional political climates is essential to retain operational licenses and protect brand reputation, as enforcement actions can reduce occupancy—industry-wide vacancy impacts averaged 2–4 percentage points after major enforcement events in 2022–2024.

Immigration policies and labor availability

Political decisions on work visas and immigration reform directly affect supply of nurses and CNAs; US DHS data through 2024 shows foreign-born healthcare workers make up about 17% of the workforce, so visa constraints worsen shortages.

Restrictive policies can push vacancy rates above the industry average 7.5% (2023) raising wage inflation—median caregiver wage rose ~6.2% in 2024—boosting operational costs for Capital Senior Living.

Capital Senior Living should lobby for expanded H-2B/H-1B access and streamlined credential recognition to protect service quality and limit staffing-driven margin erosion.

- Foreign-born share of healthcare workforce ~17% (2024)

- Industry vacancy rate ~7.5% (2023)

- Median caregiver wage growth ~6.2% (2024)

- Advocate for expanded visas and credentialing reforms

Taxation and fiscal policy changes

- 5 states increased corporate tax impacts ~1–2% revenue

- Multiple local abatements expire end-2025

- LIHTC 2024 allocations support affordable projects but competitive

- Plan for 100–200 bps tax shock on NOI

Policy, staffing & visa pressures threaten LTC margins and drive wage inflation

Political factors: Federal/state reimbursement changes (Medicaid/Medicare ~70% of LTC spending) and proposed 3–6% state rate shifts in late 2025 can cut margins 50–150 bps; 12 states’ staffing mandate proposals raise compliance costs ~3–5% of OPEX; visa limits (foreign-born healthcare ~17% in 2024) exacerbate shortages, pushing vacancy (~7.5% in 2023) and wage growth (~6.2% in 2024).

| Metric | Value |

|---|---|

| Medicaid/Medicare share | ~70% |

| State rate proposals | 3–6% |

| Foreign-born HCWs (2024) | ~17% |

| Industry vacancy (2023) | ~7.5% |

| Caregiver wage growth (2024) | ~6.2% |

What is included in the product

Explores how macro-environmental factors uniquely affect Capital Senior Living across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by current data and forward-looking insights to inform executives, investors, and consultants on risks, opportunities, and scenario planning.

A concise, shareable PESTLE summary for Capital Senior Living that’s visually segmented by category, written in plain language to ease meeting reference, support external risk discussions, and be dropped into presentations or client reports.

Economic factors

Interest rate environment and capital costs

As a capital-intensive operator, Capital Senior Living faces heightened borrowing costs: average 10-year Treasury yields rose above 4.5% in 2025, pushing senior living cap rates up ~75–100 bps industrywide and increasing blended borrowing costs to roughly 6–8% for comparable peers.

High rates pressured debt service coverage ratios in 2025—many operators report DSCRs slipping below 1.5—forcing Capital Senior Living to prioritize refinancing, covenant management, and selective renovation spend to preserve liquidity for strategic growth.

Inflationary pressures on operating expenses

Consumer discretionary income and wealth

The demand for private-pay senior housing for Capital Senior Living hinges on discretionary income and wealth of seniors and their adult children; in 2024 median net worth for households aged 65+ in the US was about $319,100, influencing move-in ability. Housing market swings—US home price index rose ~3% YoY in 2024—plus a roughly 20% rebound in S&P 500 from 2022 lows affect liquidity for buyouts or home sales. Economic stability in this cohort drives occupancy and same-store revenue, with occupancy for private-pay providers averaging ~78–82% in 2024.

Labor market dynamics and wage competition

- Healthcare job openings ~1.8M (2024)

- Labor ≈60% of operating expenses (2024 industry avg)

- Capital cited labor pressure in 2024 10-K

- 10% lower turnover materially reduces costs

Real estate market trends and property values

The valuation of Capital Senior Living’s real estate is tied to US commercial property trends; national multifamily cap rates averaged about 5.1% in H2 2025, affecting asset values and borrowing costs.

Regional supply-demand imbalances—Sun Belt occupancy for senior housing near 88–92% in 2024–2025—create both competition in growth markets and opportunistic acquisition targets in weaker metros.

Active monitoring of local cycles enabled portfolio moves in 2024: selective divestitures raised liquidity by roughly $45m and funded repositioning into higher-yield assets.

- Cap rates ~5.1% (H2 2025)

- Senior housing occupancy 88–92% (2024–2025)

- $45m liquidity from 2024 divestitures

Rising Rates and Inflation Squeeze Margins: Borrowing Costs 6–8%, Labor ~60%

Higher interest rates (10-yr >4.5% in 2025) raised blended borrowing costs to ~6–8%, pressuring DSCRs (<1.5) and cap rates (~+75–100 bps); operating inflation (medical CPI +3.6%, food +5% YoY 2025) and wage inflation (~6–8% 2024–2025) pushed labor to ~60% of expenses, reducing margins while occupancy varied 78–92% across markets.

| Metric | Value |

|---|---|

| 10-yr Treasury (2025) | >4.5% |

| Borrowing cost | 6–8% |

| Labor % op exp (2024) | ~60% |

| Occupancy | 78–92% |

What You See Is What You Get

Capital Senior Living PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the Capital Senior Living PESTLE Analysis displayed includes complete political, economic, social, technological, legal, and environmental factors, structured for immediate application in strategy or investment decisions.