Cairn Energy Boston Consulting Group Matrix

Unlock Strategic Clarity

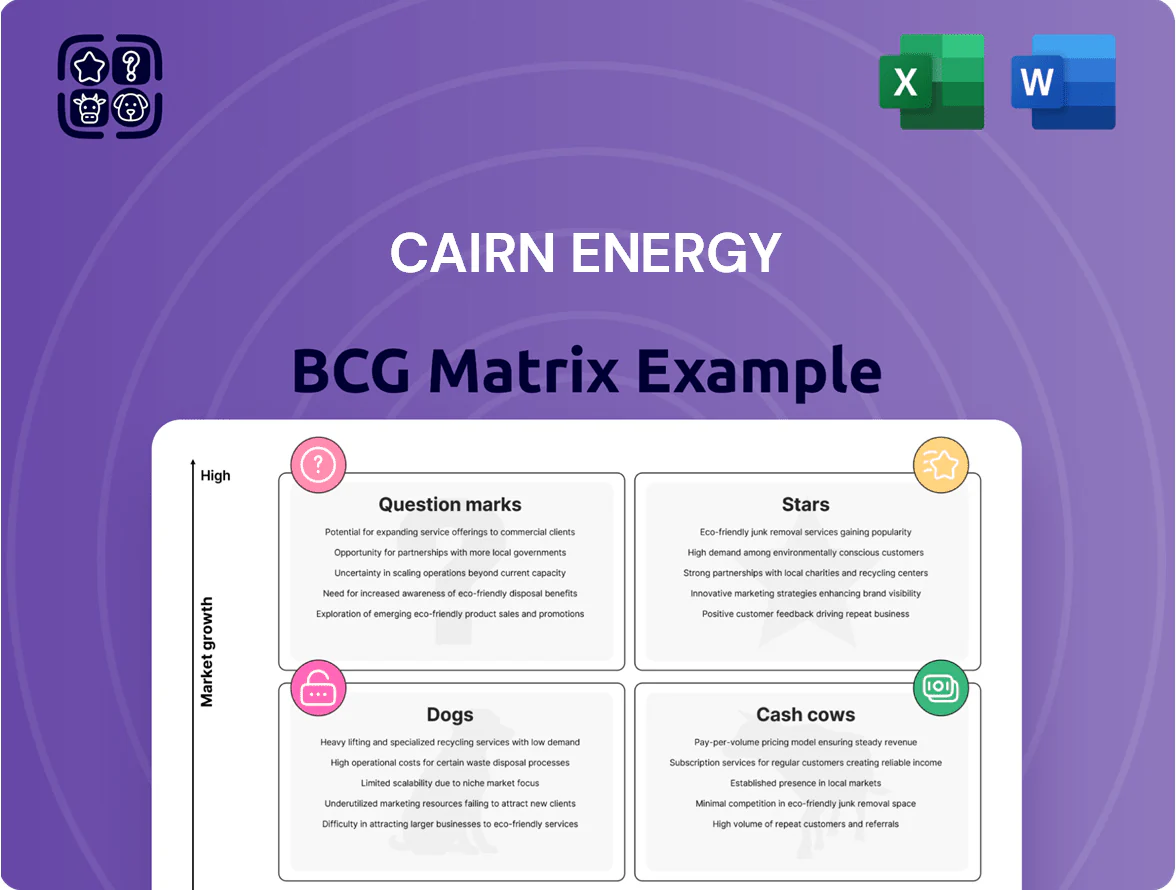

Cairn Energy’s BCG Matrix preview highlights where its exploration and production assets likely fall across Stars, Cash Cows, Question Marks, and Dogs amid volatile oil markets and shifting capital allocation — revealing early signals about which projects drive growth and which consume cash. This sneak peek is strategic but limited; purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files so you can act quickly with clarity.

Stars

Badr El Din Integrated Concession Development

Following the 2025 ratification of the integrated concession agreement, Badr El Din Integrated Concession Development (BED) became Cairn Energy’s high-growth engine, holding ~38% of the company’s effective production portfolio by year‑end 2025.

Consolidating eight concessions unlocked ~120 million boe contingent resources, enabling aggressive appraisal and development drilling that achieved an exit rate >21,000 boepd by 31 Dec 2025.

BED requires ongoing capital reinvestment—capex of approximately $280m in 2025—to sustain >20% year‑on‑year production growth and transition from growth asset to long‑term cash generator.

Liquid-Focused Drilling Program

The strategic shift toward liquids, which reached about 43% of Cairn Energy’s production by Q4 2025, targets a higher-growth, high-demand segment and boosts portfolio resilience.

Deploying a four-rig fleet on liquids-rich targets in Egypt strengthened market position versus the prior gas-heavy mix and lifted FY2025 realized liquids prices to roughly $74/bbl.

Drilling plus waterflood capex ran at ~US$220m H2 2025, consuming cash but delivering the portfolio’s highest margins—EBITDA margin for liquids wells near 58% in 2025.

Near-Field Exploration Successes

Successful exploration in North Um Baraka and South East Horus has elevated these Egyptian Western Desert licenses to BCG Matrix stars, driven by stacked hydrocarbon shows and contingent resources of ~120–180 MMboe combined as of Q4 2025.

Proximity to existing pipelines and the Abu Roash processing hub cuts tie-in time to 6–12 months, enabling faster cash flow and potential 35–45% market share gains locally.

Management targets converting encounters to 2P reserves by end-2026, budgeting $90–120m capex for appraisal and appraisal drilling across both licenses.

Modernized Fiscal Terms and Concession Extensions

The new single integrated agreement adopts improved fiscal terms—reductions in royalty rates and blended tax relief—that enable Cairn Energy to redirect an estimated $120–150 million annually into capex and exploration, catalyzing high-growth reinvestment across legacy blocks.

By refreshing primary development periods, the company effectively resets mature-asset lifecycles, converting declining fields into multi-year growth projects with projected production uplifts of 10–25% over five years.

This framework strengthens Cairn’s capital-competition position versus MENA peers by lowering breakeven unit costs to under $30/boe and improving project IRRs by 4–6 percentage points.

- Annual reinvestment potential: $120–150M

- Projected production uplift: 10–25% (5 years)

- Breakeven: < $30 per boe

- IRR improvement: +4–6 pp

Enhanced Waterflood and Recovery Projects

Enhanced waterflood programs boosted Cairn Energy’s onshore Egyptian output, surpassing year-end 2025 guidance by ~18%, raising average production to about 62 kbopd versus 52 kbopd guidance; capex for these secondary recovery projects reached ~USD 220m in 2025.

These projects are high-growth within the BCG matrix: they use advanced injection tech in mature fields where Cairn keeps >85% operating control; capital intensity is high but crucial to retain market leadership in Egypt.

- +18% production vs guidance (end-2025)

- ~62 kbopd realized output

- USD 220m 2025 capex on waterfloods

- Operational control >85%

BED & Western Desert: Liquids-rich BCG Stars—>21k boepd, <$30/boe breakeven, 120–180 MMboe

BED and Western Desert liquids-rich projects are BCG Stars: ~38% portfolio share, exit rate >21,000 boepd (Dec 31, 2025), 2025 capex ~$280m (BED) + $220m waterfloods, contingent resources ~120–180 MMboe, FY2025 liquids ~43% at ~$74/bbl, breakeven < $30/boe, annual reinvestment $120–150m; targets 2P conversion by end‑2026 with $90–120m appraisal capex.

| Metric | Value |

|---|---|

| Portfolio share | ~38% |

| Exit rate | >21,000 boepd |

| 2025 capex | $280m + $220m |

| Contingent | 120–180 MMboe |

| Liquids % | ~43% |

| Breakeven | < $30/boe |

What is included in the product

BCG Matrix for Cairn Energy: quadrant-by-quadrant strategic review identifying Stars, Cash Cows, Question Marks, Dogs and recommended invest/hold/divest actions.

One-page Cairn Energy BCG Matrix placing each business unit in a quadrant for rapid portfolio clarity.

Cash Cows

Western Desert Producing Assets

The Western Desert producing blocks in Egypt remain Cairn Energy’s primary cash cows, delivering steady production of ~18,000 boe/d in 2025 and reliable free cash flow. These assets generated significant net cash, helping Cairn reach an approximate net cash position of $103 million by 31 Dec 2025. Cash from these fields funded 2025 exploration spend of ~$45 million and covered remaining junior debt of roughly $28 million. They underpin near-term liquidity for growth.

Egyptian Gas Operational Performance

Gas from established wells such as BED15-31 delivers steady revenue—Egyptian domestic gas sales averaged about 7.8 mcm/d in 2024, with fixed-price contracts near $2.5/MMBtu, giving Cairn predictable cash inflows.

In Egypt’s mature market these assets need minimal promotion and mainly target uptime and cost cuts; operating expenses for similar fields run ~$3–5/boe equivalent, keeping margins healthy.

Reliable cash flow funds group admin costs and ongoing technical studies, covering roughly 40–50% of corporate G&A in 2024 and financing reservoir appraisal campaigns.

UK North Sea Non-Operated Interests

Cairn Energy’s remaining UK North Sea non-operated interests act as cash cows: mature, low-growth fields generating steady free cash flow with minimal capex, contributing roughly $120–150m annually to group operating cash flow in 2024–25.

As a non-operator, Cairn milks these inflows to bolster liquidity and redeploy capital, and those cash returns enabled full repayment of its $400m senior debt facility ahead of schedule in late 2025.

EGPC Receivables Collection Plan

The structured payment plan with the Egyptian General Petroleum Corporation (EGPC) converted legacy receivables into a steady cash stream; by end-2025 Cairn Energy collected over $150 million in one year, cutting receivables and stabilising cash flow.

This consistent monthly collection of back-pay functions as a synthetic cash cow, delivering non-dilutive funding for exploration and appraisal, and reducing short-term financing needs and interest expense.

Here’s the quick math: $150m collected in 12 months ≈ $12.5m/month, freeing capital for operations and M&A without issuing equity.

- Over $150m collected in 2025

- ≈ $12.5m monthly inflow

- Receivables materially reduced by year-end 2025

- Non-dilutive funding for growth and lower interest costs

Consolidated Infrastructure and Midstream Access

Consolidated Infrastructure and Midstream Access: Cairn Energy’s ownership of Western Desert processing plants and pipelines delivers a high-share, low-growth cash cow—handling ~120 kbpd capacity with ~80% utilization in 2025, cutting unit operating cost to ~$8–10/boe and boosting EBITDA margins by ~15–20% versus standalone fields.

- ~120 kbpd capacity

- 80% utilization (2025)

- $8–10 per boe operating cost

- +15–20% EBITDA margin lift

Cairn’s Western Desert & UK North Sea: $120–150M cash flow, 18k boe/d fuel debt paydown

The Western Desert and UK North Sea assets are Cairn’s cash cows, yielding ~18,000 boe/d (2025) and $120–150m pa (2024–25), funding $45m exploration and repaying $400m debt; EGPC receipts added ~$150m in 2025 (~$12.5m/mo). Operating costs ~ $3–10/boe; infrastructure 120 kbpd capacity at 80% util.

| Metric | Value (2025) |

|---|---|

| Production | ~18,000 boe/d |

| UK cash flow | $120–150m |

| EGPC receipts | $150m (~$12.5m/mo) |

| Opex | $3–10/boe |

| Infra cap | 120 kbpd, 80% util |

What You’re Viewing Is Included

Cairn Energy BCG Matrix

The file you're previewing is the exact Cairn Energy BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready document tailored for professional use and stakeholder presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Cairn Energy’s BCG Matrix preview highlights where its exploration and production assets likely fall across Stars, Cash Cows, Question Marks, and Dogs amid volatile oil markets and shifting capital allocation — revealing early signals about which projects drive growth and which consume cash. This sneak peek is strategic but limited; purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files so you can act quickly with clarity.

Stars

Badr El Din Integrated Concession Development

Following the 2025 ratification of the integrated concession agreement, Badr El Din Integrated Concession Development (BED) became Cairn Energy’s high-growth engine, holding ~38% of the company’s effective production portfolio by year‑end 2025.

Consolidating eight concessions unlocked ~120 million boe contingent resources, enabling aggressive appraisal and development drilling that achieved an exit rate >21,000 boepd by 31 Dec 2025.

BED requires ongoing capital reinvestment—capex of approximately $280m in 2025—to sustain >20% year‑on‑year production growth and transition from growth asset to long‑term cash generator.

Liquid-Focused Drilling Program

The strategic shift toward liquids, which reached about 43% of Cairn Energy’s production by Q4 2025, targets a higher-growth, high-demand segment and boosts portfolio resilience.

Deploying a four-rig fleet on liquids-rich targets in Egypt strengthened market position versus the prior gas-heavy mix and lifted FY2025 realized liquids prices to roughly $74/bbl.

Drilling plus waterflood capex ran at ~US$220m H2 2025, consuming cash but delivering the portfolio’s highest margins—EBITDA margin for liquids wells near 58% in 2025.

Near-Field Exploration Successes

Successful exploration in North Um Baraka and South East Horus has elevated these Egyptian Western Desert licenses to BCG Matrix stars, driven by stacked hydrocarbon shows and contingent resources of ~120–180 MMboe combined as of Q4 2025.

Proximity to existing pipelines and the Abu Roash processing hub cuts tie-in time to 6–12 months, enabling faster cash flow and potential 35–45% market share gains locally.

Management targets converting encounters to 2P reserves by end-2026, budgeting $90–120m capex for appraisal and appraisal drilling across both licenses.

Modernized Fiscal Terms and Concession Extensions

The new single integrated agreement adopts improved fiscal terms—reductions in royalty rates and blended tax relief—that enable Cairn Energy to redirect an estimated $120–150 million annually into capex and exploration, catalyzing high-growth reinvestment across legacy blocks.

By refreshing primary development periods, the company effectively resets mature-asset lifecycles, converting declining fields into multi-year growth projects with projected production uplifts of 10–25% over five years.

This framework strengthens Cairn’s capital-competition position versus MENA peers by lowering breakeven unit costs to under $30/boe and improving project IRRs by 4–6 percentage points.

- Annual reinvestment potential: $120–150M

- Projected production uplift: 10–25% (5 years)

- Breakeven: < $30 per boe

- IRR improvement: +4–6 pp

Enhanced Waterflood and Recovery Projects

Enhanced waterflood programs boosted Cairn Energy’s onshore Egyptian output, surpassing year-end 2025 guidance by ~18%, raising average production to about 62 kbopd versus 52 kbopd guidance; capex for these secondary recovery projects reached ~USD 220m in 2025.

These projects are high-growth within the BCG matrix: they use advanced injection tech in mature fields where Cairn keeps >85% operating control; capital intensity is high but crucial to retain market leadership in Egypt.

- +18% production vs guidance (end-2025)

- ~62 kbopd realized output

- USD 220m 2025 capex on waterfloods

- Operational control >85%

BED & Western Desert: Liquids-rich BCG Stars—>21k boepd, <$30/boe breakeven, 120–180 MMboe

BED and Western Desert liquids-rich projects are BCG Stars: ~38% portfolio share, exit rate >21,000 boepd (Dec 31, 2025), 2025 capex ~$280m (BED) + $220m waterfloods, contingent resources ~120–180 MMboe, FY2025 liquids ~43% at ~$74/bbl, breakeven < $30/boe, annual reinvestment $120–150m; targets 2P conversion by end‑2026 with $90–120m appraisal capex.

| Metric | Value |

|---|---|

| Portfolio share | ~38% |

| Exit rate | >21,000 boepd |

| 2025 capex | $280m + $220m |

| Contingent | 120–180 MMboe |

| Liquids % | ~43% |

| Breakeven | < $30/boe |

What is included in the product

BCG Matrix for Cairn Energy: quadrant-by-quadrant strategic review identifying Stars, Cash Cows, Question Marks, Dogs and recommended invest/hold/divest actions.

One-page Cairn Energy BCG Matrix placing each business unit in a quadrant for rapid portfolio clarity.

Cash Cows

Western Desert Producing Assets

The Western Desert producing blocks in Egypt remain Cairn Energy’s primary cash cows, delivering steady production of ~18,000 boe/d in 2025 and reliable free cash flow. These assets generated significant net cash, helping Cairn reach an approximate net cash position of $103 million by 31 Dec 2025. Cash from these fields funded 2025 exploration spend of ~$45 million and covered remaining junior debt of roughly $28 million. They underpin near-term liquidity for growth.

Egyptian Gas Operational Performance

Gas from established wells such as BED15-31 delivers steady revenue—Egyptian domestic gas sales averaged about 7.8 mcm/d in 2024, with fixed-price contracts near $2.5/MMBtu, giving Cairn predictable cash inflows.

In Egypt’s mature market these assets need minimal promotion and mainly target uptime and cost cuts; operating expenses for similar fields run ~$3–5/boe equivalent, keeping margins healthy.

Reliable cash flow funds group admin costs and ongoing technical studies, covering roughly 40–50% of corporate G&A in 2024 and financing reservoir appraisal campaigns.

UK North Sea Non-Operated Interests

Cairn Energy’s remaining UK North Sea non-operated interests act as cash cows: mature, low-growth fields generating steady free cash flow with minimal capex, contributing roughly $120–150m annually to group operating cash flow in 2024–25.

As a non-operator, Cairn milks these inflows to bolster liquidity and redeploy capital, and those cash returns enabled full repayment of its $400m senior debt facility ahead of schedule in late 2025.

EGPC Receivables Collection Plan

The structured payment plan with the Egyptian General Petroleum Corporation (EGPC) converted legacy receivables into a steady cash stream; by end-2025 Cairn Energy collected over $150 million in one year, cutting receivables and stabilising cash flow.

This consistent monthly collection of back-pay functions as a synthetic cash cow, delivering non-dilutive funding for exploration and appraisal, and reducing short-term financing needs and interest expense.

Here’s the quick math: $150m collected in 12 months ≈ $12.5m/month, freeing capital for operations and M&A without issuing equity.

- Over $150m collected in 2025

- ≈ $12.5m monthly inflow

- Receivables materially reduced by year-end 2025

- Non-dilutive funding for growth and lower interest costs

Consolidated Infrastructure and Midstream Access

Consolidated Infrastructure and Midstream Access: Cairn Energy’s ownership of Western Desert processing plants and pipelines delivers a high-share, low-growth cash cow—handling ~120 kbpd capacity with ~80% utilization in 2025, cutting unit operating cost to ~$8–10/boe and boosting EBITDA margins by ~15–20% versus standalone fields.

- ~120 kbpd capacity

- 80% utilization (2025)

- $8–10 per boe operating cost

- +15–20% EBITDA margin lift

Cairn’s Western Desert & UK North Sea: $120–150M cash flow, 18k boe/d fuel debt paydown

The Western Desert and UK North Sea assets are Cairn’s cash cows, yielding ~18,000 boe/d (2025) and $120–150m pa (2024–25), funding $45m exploration and repaying $400m debt; EGPC receipts added ~$150m in 2025 (~$12.5m/mo). Operating costs ~ $3–10/boe; infrastructure 120 kbpd capacity at 80% util.

| Metric | Value (2025) |

|---|---|

| Production | ~18,000 boe/d |

| UK cash flow | $120–150m |

| EGPC receipts | $150m (~$12.5m/mo) |

| Opex | $3–10/boe |

| Infra cap | 120 kbpd, 80% util |

What You’re Viewing Is Included

Cairn Energy BCG Matrix

The file you're previewing is the exact Cairn Energy BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready document tailored for professional use and stakeholder presentations.