Cairn Energy PESTLE Analysis

Skip the Research. Get the Strategy.

Cairn Energy faces a dynamic external landscape—from shifting North Sea regulations and volatile oil prices to evolving ESG expectations and rapid exploration technology advances; our PESTLE distils these forces into clear implications for strategy and risk. Purchase the full PESTLE to get the complete, actionable analysis and ready-to-use insights for investment or planning.

Political factors

Geopolitical Stability in Egypt

Cairn Energy remains heavily exposed to Egypt, where its primary producing assets generated about 60% of group production in 2024 and contributed roughly $220m of EBITDA through FY2024, making political stability crucial.

Although the Egyptian government pledged $7bn in upstream investment incentives in 2023–24, regional Middle East tensions have periodically tightened security measures and increased country risk premia for operators.

Close strategic alignment with state-owned partners such as EGPC and EGAS is essential to maintain operational continuity, access export infrastructure, and secure future concessions amid shifting regulatory priorities.

UK North Sea Policy Shifts

Political decisions on UK North Sea licensing and decommissioning materially affect Cairn Energy’s non-operated stakes; the 2024 UK oil & gas licensing round awarded 101 blocks, shifting valuation assumptions for assets tied to future development cashflows worth an estimated £200–£400m across similar portfolios. Fluctuating ministerial signals on new licensing and a 50% UK 2030 emissions reduction target complicate capital planning for projects with long payback periods. Cairn must balance short-term energy security demands—UK production met ~45% of domestic oil in 2023—with policy-driven decline scenarios when modelling reserves and impairment risk.

Resource Nationalism Trends

Resource nationalism remains elevated in emerging markets: from 2018–2024 renegotiation incidents rose 22%, and governments captured an average 6–10% higher fiscal take after contract revisions; a 2023 IEA/World Bank review found 18% of upstream projects faced mid‑life fiscal changes. With Brent volatility (2024 average ~US$86/bbl) fueling domestic pressure, Capricorn must sustain diplomatic and commercial ties to limit exposure to renegotiation and protect projected cash flows.

International Trade and Sanctions

Global political tensions reshape energy flows and access to specialized oilfield services; in 2024, sanctions linked to Russia and Iran tightened supply of tubulars and drilling rigs, raising spot rig rates by ~18% in MENA versus 2022 levels.

Trade restrictions on regional partners can disrupt supply chains and raise operating costs for mature-field workovers in Egypt, where Cairn’s 2024 capex guidance of ~$140–160m is sensitive to equipment price swings.

Continuous geopolitical monitoring is essential to secure equipment and expertise for Egyptian operations and to hedge against potential 10–20% cost overruns from logistic bottlenecks.

- Sanctions increased rig/parts scarcity; spot rig rates +18% (MENA, 2024)

- Cairn 2024 capex sensitivity: ~$140–160m

- Potential 10–20% cost overruns from supply-chain disruptions

- Geo-monitoring crucial to secure equipment/expertise for Egypt

Government Payment Reliability

- Estimated Egyptian arrears to IOCs ~ $2.5bn (2024)

- Previous systemic delays: 2014–2016, 2020–2023

- 2024 MOUs and quarterly recovery targets aim to improve predictability

Cairn’s Egypt reliance, $2.5bn arrears & rising MENA costs threaten FY24 EBITDA and capex

Cairn’s Egypt exposure (≈60% production, ~$220m FY2024 EBITDA) makes political stability, state partnerships, and receivable clearance (~$2.5bn arrears 2024) critical; regional tensions, sanctions (rig rates +18% MENA 2024) and renegotiation trends (+22% incidents 2018–24) raise fiscal and cost risks, impacting capex ($140–160m 2024) and potential 10–20% overruns.

| Metric | Value |

|---|---|

| Egypt share of production | ~60% |

| FY2024 EBITDA from Egypt | $220m |

| Estimated Egyptian arrears | $2.5bn (2024) |

| 2024 capex guidance | $140–160m |

| MENA spot rig rate change (2024 vs 2022) | +18% |

| Renegotiation incidents change (2018–24) | +22% |

| Potential cost overrun | 10–20% |

What is included in the product

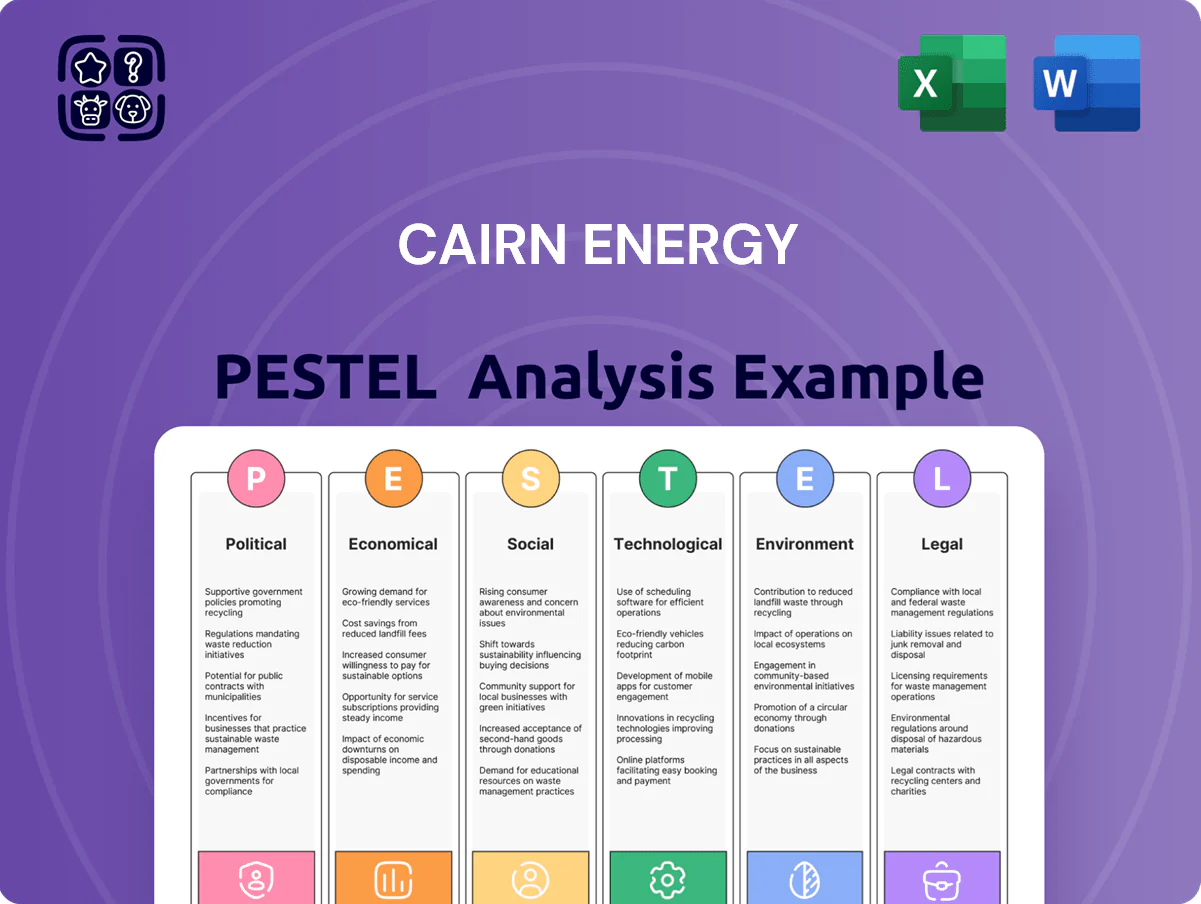

Explores how external macro-environmental factors uniquely affect Cairn Energy across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to reveal risks and opportunities specific to its upstream oil & gas operations and jurisdictions.

A concise, PESTLE-segmented summary of Cairn Energy’s external risks and opportunities, formatted for easy insertion into presentations or strategy packs to streamline team discussions and decision-making.

Economic factors

Global Hydrocarbon Price Volatility

Revenue and profitability at Cairn Energy move in lockstep with Brent and gas prices; Brent averaged about 95 USD/bbl in 2024 while UK gas NBP averaged ~45 p/therm, directly affecting 2024 EBITDA swings. Demand shifts in China, India and OPEC+ quotas caused 2024 price volatility that constrained capital spending, reducing 2024 CAPEX guidance vs 2023 by ~15%. Cairn uses hedging programs and fixed-price offtakes to smooth cash flow and protect shareholder returns.

Inflationary Pressure on Operating Costs

Rising global inflation lifted input costs for Cairn Energy, with UK CPI at 4.0% and Egypt inflation near 30% in 2024, driving higher labor, materials and technical-service bills for North Sea maintenance and Egyptian expansion.

Maintaining aging North Sea infrastructure raised operating expenditures, contributing to group opex pressure as Cairn reported cash opex increases in 2024 versus 2023.

Cost escalation risks squeezing margins and raising the crude price needed to break even on existing projects, making tight cost control and contract hedging essential to preserve project viability.

Currency Exchange Rate Fluctuations

As a UK-listed international operator, Cairn Energy faces FX risk across USD, GBP and EGP; with Brent priced in USD, a 10% GBP depreciation vs USD in 2024 would have increased reported revenue in GBP but raised local cost pressures in Egypt where EGP weakened ~18% vs USD in 2023–24. Financial teams use hedging and natural offsets; Cairn reported FX translation losses of £45m in 2024 related to USD/GBP moves, underscoring active management needs.

Access to Capital Markets

The shift to green energy and tighter ESG lending has constrained bank financing for mid-sized oil firms; in 2024 banks reduced fossil-fuel project exposure by about 12%, pressuring Cairn to preserve liquidity.

Higher global policy rates (ECB peak ~4.5% in 2024) and stricter credit terms mean Cairn must show strong free cash flow—2023 pro forma FCF margins in the UKCS averaged ~18% for viable projects.

Funding new developments will hinge on disciplined capital allocation and demonstrable FCF, with a target net cash/EBITDA ratio under 1.0 to access capital markets on reasonable terms.

- 2024: banks cut fossil exposure ~12%

- Policy rates ~4–4.5% (2024)

- Target: net cash/EBITDA <1.0

- FCF margins ~18% benchmark (UKCS projects)

Egyptian Economic Recovery

Egypts GDP grew 3.7% in FY2023/24 and IMF-backed reforms plus a $3 billion 2024 IMF arrangement have improved fiscal buffers, supporting public investment in energy infrastructure and boosting domestic demand for gas and power.

Continued structural reforms—subsidy rationalization and tax measures—alongside $20+ billion in pledged GCC and multilateral financing reduce sovereign funding gaps and signal a firmer macro outlook for Cairn Energy projects.

A more stable Egyptian pound and narrowing inflation from 38% in 2023 to ~20% by late 2024 lower currency-devaluation risk, improving project economics and foreign-investor returns.

- GDP growth 3.7% (FY2023/24)

- $3bn IMF deal + $20bn+ external pledges

- Inflation ~20% late-2024 (from 38% in 2023)

Commodity swings, inflation and FX squeeze margins — CAPEX cut and tighter finance

Commodity prices (Brent ~95 USD/bbl, NBP ~45 p/therm in 2024) drove 2024 EBITDA swings and cut CAPEX guidance ~15% vs 2023; hedging and fixed offtakes smooth cash flow.

Inflation and ageing UKCS assets pushed opex up (UK CPI ~4.0%, Egypt inflation ~20% late‑2024), squeezing margins and raising break‑even prices.

FX and financing risks—GBP down ~10% vs USD, EGP weaker ~18% in 2023–24—caused £45m translation losses; banks cut fossil exposure ~12% in 2024, forcing tight capital discipline.

| Metric | 2024/2023 |

|---|---|

| Brent | ~95 USD/bbl (2024) |

| NBP | ~45 p/therm (2024) |

| UK CPI | 4.0% (2024) |

| Egypt inflation | ~20% late‑2024 |

| Banks fossil exposure cut | ~12% (2024) |

| FX translation loss | £45m (2024) |

Preview the Actual Deliverable

Cairn Energy PESTLE Analysis

The preview shown here is the exact Cairn Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Cairn Energy faces a dynamic external landscape—from shifting North Sea regulations and volatile oil prices to evolving ESG expectations and rapid exploration technology advances; our PESTLE distils these forces into clear implications for strategy and risk. Purchase the full PESTLE to get the complete, actionable analysis and ready-to-use insights for investment or planning.

Political factors

Geopolitical Stability in Egypt

Cairn Energy remains heavily exposed to Egypt, where its primary producing assets generated about 60% of group production in 2024 and contributed roughly $220m of EBITDA through FY2024, making political stability crucial.

Although the Egyptian government pledged $7bn in upstream investment incentives in 2023–24, regional Middle East tensions have periodically tightened security measures and increased country risk premia for operators.

Close strategic alignment with state-owned partners such as EGPC and EGAS is essential to maintain operational continuity, access export infrastructure, and secure future concessions amid shifting regulatory priorities.

UK North Sea Policy Shifts

Political decisions on UK North Sea licensing and decommissioning materially affect Cairn Energy’s non-operated stakes; the 2024 UK oil & gas licensing round awarded 101 blocks, shifting valuation assumptions for assets tied to future development cashflows worth an estimated £200–£400m across similar portfolios. Fluctuating ministerial signals on new licensing and a 50% UK 2030 emissions reduction target complicate capital planning for projects with long payback periods. Cairn must balance short-term energy security demands—UK production met ~45% of domestic oil in 2023—with policy-driven decline scenarios when modelling reserves and impairment risk.

Resource Nationalism Trends

Resource nationalism remains elevated in emerging markets: from 2018–2024 renegotiation incidents rose 22%, and governments captured an average 6–10% higher fiscal take after contract revisions; a 2023 IEA/World Bank review found 18% of upstream projects faced mid‑life fiscal changes. With Brent volatility (2024 average ~US$86/bbl) fueling domestic pressure, Capricorn must sustain diplomatic and commercial ties to limit exposure to renegotiation and protect projected cash flows.

International Trade and Sanctions

Global political tensions reshape energy flows and access to specialized oilfield services; in 2024, sanctions linked to Russia and Iran tightened supply of tubulars and drilling rigs, raising spot rig rates by ~18% in MENA versus 2022 levels.

Trade restrictions on regional partners can disrupt supply chains and raise operating costs for mature-field workovers in Egypt, where Cairn’s 2024 capex guidance of ~$140–160m is sensitive to equipment price swings.

Continuous geopolitical monitoring is essential to secure equipment and expertise for Egyptian operations and to hedge against potential 10–20% cost overruns from logistic bottlenecks.

- Sanctions increased rig/parts scarcity; spot rig rates +18% (MENA, 2024)

- Cairn 2024 capex sensitivity: ~$140–160m

- Potential 10–20% cost overruns from supply-chain disruptions

- Geo-monitoring crucial to secure equipment/expertise for Egypt

Government Payment Reliability

- Estimated Egyptian arrears to IOCs ~ $2.5bn (2024)

- Previous systemic delays: 2014–2016, 2020–2023

- 2024 MOUs and quarterly recovery targets aim to improve predictability

Cairn’s Egypt reliance, $2.5bn arrears & rising MENA costs threaten FY24 EBITDA and capex

Cairn’s Egypt exposure (≈60% production, ~$220m FY2024 EBITDA) makes political stability, state partnerships, and receivable clearance (~$2.5bn arrears 2024) critical; regional tensions, sanctions (rig rates +18% MENA 2024) and renegotiation trends (+22% incidents 2018–24) raise fiscal and cost risks, impacting capex ($140–160m 2024) and potential 10–20% overruns.

| Metric | Value |

|---|---|

| Egypt share of production | ~60% |

| FY2024 EBITDA from Egypt | $220m |

| Estimated Egyptian arrears | $2.5bn (2024) |

| 2024 capex guidance | $140–160m |

| MENA spot rig rate change (2024 vs 2022) | +18% |

| Renegotiation incidents change (2018–24) | +22% |

| Potential cost overrun | 10–20% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Cairn Energy across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to reveal risks and opportunities specific to its upstream oil & gas operations and jurisdictions.

A concise, PESTLE-segmented summary of Cairn Energy’s external risks and opportunities, formatted for easy insertion into presentations or strategy packs to streamline team discussions and decision-making.

Economic factors

Global Hydrocarbon Price Volatility

Revenue and profitability at Cairn Energy move in lockstep with Brent and gas prices; Brent averaged about 95 USD/bbl in 2024 while UK gas NBP averaged ~45 p/therm, directly affecting 2024 EBITDA swings. Demand shifts in China, India and OPEC+ quotas caused 2024 price volatility that constrained capital spending, reducing 2024 CAPEX guidance vs 2023 by ~15%. Cairn uses hedging programs and fixed-price offtakes to smooth cash flow and protect shareholder returns.

Inflationary Pressure on Operating Costs

Rising global inflation lifted input costs for Cairn Energy, with UK CPI at 4.0% and Egypt inflation near 30% in 2024, driving higher labor, materials and technical-service bills for North Sea maintenance and Egyptian expansion.

Maintaining aging North Sea infrastructure raised operating expenditures, contributing to group opex pressure as Cairn reported cash opex increases in 2024 versus 2023.

Cost escalation risks squeezing margins and raising the crude price needed to break even on existing projects, making tight cost control and contract hedging essential to preserve project viability.

Currency Exchange Rate Fluctuations

As a UK-listed international operator, Cairn Energy faces FX risk across USD, GBP and EGP; with Brent priced in USD, a 10% GBP depreciation vs USD in 2024 would have increased reported revenue in GBP but raised local cost pressures in Egypt where EGP weakened ~18% vs USD in 2023–24. Financial teams use hedging and natural offsets; Cairn reported FX translation losses of £45m in 2024 related to USD/GBP moves, underscoring active management needs.

Access to Capital Markets

The shift to green energy and tighter ESG lending has constrained bank financing for mid-sized oil firms; in 2024 banks reduced fossil-fuel project exposure by about 12%, pressuring Cairn to preserve liquidity.

Higher global policy rates (ECB peak ~4.5% in 2024) and stricter credit terms mean Cairn must show strong free cash flow—2023 pro forma FCF margins in the UKCS averaged ~18% for viable projects.

Funding new developments will hinge on disciplined capital allocation and demonstrable FCF, with a target net cash/EBITDA ratio under 1.0 to access capital markets on reasonable terms.

- 2024: banks cut fossil exposure ~12%

- Policy rates ~4–4.5% (2024)

- Target: net cash/EBITDA <1.0

- FCF margins ~18% benchmark (UKCS projects)

Egyptian Economic Recovery

Egypts GDP grew 3.7% in FY2023/24 and IMF-backed reforms plus a $3 billion 2024 IMF arrangement have improved fiscal buffers, supporting public investment in energy infrastructure and boosting domestic demand for gas and power.

Continued structural reforms—subsidy rationalization and tax measures—alongside $20+ billion in pledged GCC and multilateral financing reduce sovereign funding gaps and signal a firmer macro outlook for Cairn Energy projects.

A more stable Egyptian pound and narrowing inflation from 38% in 2023 to ~20% by late 2024 lower currency-devaluation risk, improving project economics and foreign-investor returns.

- GDP growth 3.7% (FY2023/24)

- $3bn IMF deal + $20bn+ external pledges

- Inflation ~20% late-2024 (from 38% in 2023)

Commodity swings, inflation and FX squeeze margins — CAPEX cut and tighter finance

Commodity prices (Brent ~95 USD/bbl, NBP ~45 p/therm in 2024) drove 2024 EBITDA swings and cut CAPEX guidance ~15% vs 2023; hedging and fixed offtakes smooth cash flow.

Inflation and ageing UKCS assets pushed opex up (UK CPI ~4.0%, Egypt inflation ~20% late‑2024), squeezing margins and raising break‑even prices.

FX and financing risks—GBP down ~10% vs USD, EGP weaker ~18% in 2023–24—caused £45m translation losses; banks cut fossil exposure ~12% in 2024, forcing tight capital discipline.

| Metric | 2024/2023 |

|---|---|

| Brent | ~95 USD/bbl (2024) |

| NBP | ~45 p/therm (2024) |

| UK CPI | 4.0% (2024) |

| Egypt inflation | ~20% late‑2024 |

| Banks fossil exposure cut | ~12% (2024) |

| FX translation loss | £45m (2024) |

Preview the Actual Deliverable

Cairn Energy PESTLE Analysis

The preview shown here is the exact Cairn Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.