Card Factory Plc Boston Consulting Group Matrix

See the Bigger Picture

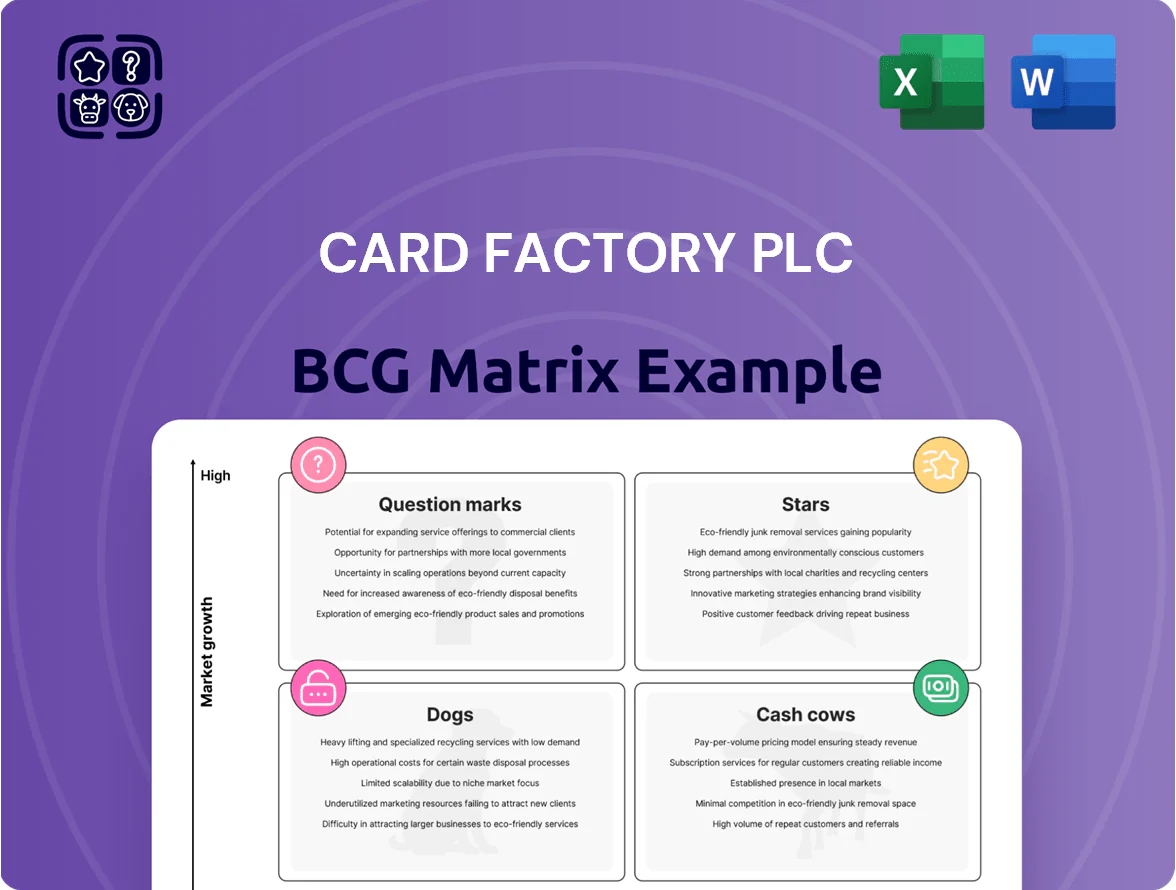

Card Factory’s BCG Matrix preview highlights likely Cash Cow segments in mature retail categories and potential Question Marks where online and gift-card growth could be accelerated—this snapshot shows where sales generate steady cash and where strategic investment might unlock future Stars. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and actionable steps to optimize portfolio allocation and boost shareholder value.

Stars

Gifts and Celebration Essentials

This segment became a primary growth engine in 2025, posting double-digit like-for-like revenue gains—about +12–18%—in confectionery and soft toys, driving a ~4–6% uplift in group LFL sales to H1 2025.

Card Factory leverages a 30–40% share in celebrations to capture more of the £1.2bn UK non-card gift market, lifting average basket values by ~£1.50–£2.50.

These ranges demand higher inventory (stock days up ~10–15%) and more floor space, but boost gross margin contribution and customer frequency.

As categories mature over 3–5 years, they’re forecast to stabilize and become high-margin cash generators, supporting store-level profitability and free cash flow.

International Partnerships and Wholesale

Card Factory expanded internationally via a capital-light wholesale model, landing major partners in the US, Australia and South Africa and targeting scale beyond the saturated UK high street.

The international/wholesale segment grew over 20% in 2025, helped by acquisition of Garlanna and Garven which opened North American and Irish routes to market.

Integration and initial logistics absorbed cash in 2025—management reported ~£18m one-off set-up costs—but the segment sits in a high-growth niche with sizable untapped demand.

The stated goal is to scale global wholesale to diversify revenue; management targets international sales contributing 25% of group revenue by 2028.

Funky Pigeon Digital Platform

Following Card Factory’s late-2025 acquisition, Funky Pigeon anchors the group in the high-growth online personalised cards and gifting market, with UK digital sales growing ~12% CAGR 2022–25 and Funky Pigeon holding ~22% share as the sector’s #2.

It supplies the platform, tech stack and brand reach to rival pure-play retailers; Card Factory is investing £35m through 2026 to integrate Bristol and Guernsey teams into its vertical manufacturing model.

Integration aims to cut fulfilment lead times by ~25% and lift digital gross margin from ~38% to a target ~44% by FY2027; this unit is therefore a classic BCG star needing continued innovation.

Omnichannel Retail Integration

Omnichannel Retail Integration lets Card Factory convert 24 million unique annual in-store customers into digital revenue by linking in-store convenience with online personalization, targeting tech-savvy value shoppers and boosting ARPU.

The rollout requires ~£25–35m upfront for POS upgrades and digital marketing, raising short-term capex but protecting share versus online-only rivals; success could drive mid-single-digit CAGR in sales over 2026–2035.

- 24M unique in-store customers

- £25–35m estimated upfront cost

- Targets tech-savvy value segment

- Potential mid-single-digit CAGR 2026–2035

Seasonal and Licensed Ranges

Card Factory’s seasonal and licensed ranges are Stars: Mother’s Day and Valentine’s Day 2024 drove record sales, with Q1 seasonal uplifts up ~18% year-on-year and licensed products contributing ~22% of seasonal revenue.

High-growth peaks face fierce competition but give Card Factory strong market share among value retailers, capturing an estimated 28% of UK seasonal card spend in key windows.

The group invested ~£6.5m in design and creative IP in FY2024 to refresh licences and exclusives, keeping ranges top choice for UK shoppers.

These ranges boost footfall and brand dominance during critical trading weeks, representing the Stars in the BCG matrix for Card Factory.

- Q1 seasonal sales +18% YoY (2024)

- Licensed products ≈22% of seasonal revenue

- Estimated 28% market share in peak windows

- £6.5m design/IP investment in FY2024

Stars' omnichannel push fuels double-digit growth—seasonal +18%, intl +20%, capex £25–35m

Stars: seasonal/licensed and omnichannel gifts drove double-digit growth—Q1 seasonal +18% YoY (2024); licensed = 22% seasonal revenue; seasonal market share ~28%; confectionery/soft toys LFL +12–18% in H1 2025; international/wholesale +20% in 2025; Funky Pigeon digital gross margin target ~44% by FY2027; upfront omnichannel spend £25–35m.

| Metric | Value |

|---|---|

| Q1 seasonal YoY | +18% |

| Licensed share | 22% |

| Seasonal market share | 28% |

| Confectionery LFL | +12–18% |

| Intl growth 2025 | +20% |

| Omnichannel capex | £25–35m |

What is included in the product

BCG Matrix review of Card Factory: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest recommendations per unit.

One-page BCG Matrix placing Card Factory units in quadrants for quick strategic clarity and decision-making

Cash Cows

Core UK Greeting Cards

The Core UK greeting cards business is the group's cash cow, holding roughly 30%–35% UK market share in a mature, low-growth sector (industry growth ~1% in 2024) and delivering modest like-for-like sales growth of ~2%–3%.

It supplies most operating cash flow—Card Factory reported £62m adjusted operating cash flow in H1 2025—thanks to vertical integration: in-house design and manufacturing keeps gross margins near 60% and trims third-party costs.

Management uses this steady cash "milk" to fund international roll-out (20+ store openings since 2023) and a multi-year digital transformation programme with c.£25m committed through 2025.

UK Physical Store Estate

With 1,100+ UK stores, Card Factory’s physical estate is a classic cash cow: high visibility, low category growth, yet same-store sales outperformed UK retail by ~2.5ppt in FY 2024 (like-for-like sales +1.8% vs UK retail -0.7%).

These locations convert footfall into steady cash with low incremental marketing spend; space-optimization has been capex-light, boosting sales per sqm by ~6% since 2022.

Operating cash flow from stores funds a progressive dividend (2024 payout 6.0p per share) and helps service net debt (~£120m at Dec 2024).

Everyday Value Ranges

Everyday Value Ranges deliver steady cash flow for Card Factory Plc, with value lines accounting for about 45% of store sales in FY2024 and maintaining market share among price-sensitive shoppers during downturns.

These low-price SKUs need minimal promotion since Card Factory is widely seen as the high-street lowest-price option, cutting marketing spend by an estimated 12% versus premium ranges.

Predictable weekly demand for basic cards and party basics enables optimized inventory and a 6–8x annual stock turnover, supporting margins despite lower unit prices.

Reliable margins from this segment funded 60% of FY2024 investment in higher-growth product testing and seasonal innovation pilots.

Vertical Manufacturing (Printcraft)

Printcraft, Card Factory Plc’s in-house manufacturing arm, produces ~70% of the group’s card stock, cutting per-unit costs by an estimated 30% versus third-party suppliers and capturing the manufacturer’s margin to lift group gross margin by ~150–200 basis points in FY2024 (year to 26 March 2024).

It operates in a mature, low-growth internal market where capacity matches retail demand; capital spend was £8.5m in FY2024 to sustain efficiency, and volume-driven cost savings are a key source of Card Factory’s everyday-low-pricing strategy.

- Produces ~70% of card stock

- ~30% lower unit cost vs external suppliers

- Adds ~150–200 bps to group gross margin (FY2024)

- £8.5m capex in FY2024 to maintain capacity

Established Third-Party Partnerships

Established wholesale agreements with retailers such as Aldi and The Reject Shop deliver steady, low-maintenance revenue—Card Factory Plc reported wholesale sales of £45m in FY 2024, roughly 12% of group revenue.

These deals use existing product lines and logistics, needing minimal capex to retain high channel market share and ~18% gross margins, so they act as mature, high-margin cash generators.

This reliable cash flow funds aggressive international expansion efforts without diluting core operations.

- Wholesale sales £45m FY2024

- ~12% of group revenue

- ~18% gross margin

- Low capex, high cash conversion

Card Factory: UK cash cow powering margin gains, £62m OCF H1 and £25m growth spend

Card Factory’s UK core is the cash cow: ~1,100 stores, 30–35% market share, like-for-like sales +1.8% FY2024, and it produced £62m adjusted operating cash flow H1 2025; Printcraft supplies ~70% of stock, cutting unit costs ~30% and adding ~150–200bps to gross margin; wholesale ¥45m FY2024 (~12% revenue) and value ranges (45% of sales) sustain steady cash for digital and international rollout (c.£25m through 2025).

| Metric | Value |

|---|---|

| Stores | 1,100+ |

| Market share | 30–35% |

| Adj OCF | £62m H1 2025 |

| Printcraft % | ~70% |

| Wholesale | £45m FY2024 |

| Capex committed | £25m to 2025 |

What You’re Viewing Is Included

Card Factory Plc BCG Matrix

The file you're previewing is the exact Card Factory Plc BCG Matrix report you'll receive after purchase—no watermarks, placeholders, or demo content—just a fully formatted, analysis-ready document crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Card Factory’s BCG Matrix preview highlights likely Cash Cow segments in mature retail categories and potential Question Marks where online and gift-card growth could be accelerated—this snapshot shows where sales generate steady cash and where strategic investment might unlock future Stars. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and actionable steps to optimize portfolio allocation and boost shareholder value.

Stars

Gifts and Celebration Essentials

This segment became a primary growth engine in 2025, posting double-digit like-for-like revenue gains—about +12–18%—in confectionery and soft toys, driving a ~4–6% uplift in group LFL sales to H1 2025.

Card Factory leverages a 30–40% share in celebrations to capture more of the £1.2bn UK non-card gift market, lifting average basket values by ~£1.50–£2.50.

These ranges demand higher inventory (stock days up ~10–15%) and more floor space, but boost gross margin contribution and customer frequency.

As categories mature over 3–5 years, they’re forecast to stabilize and become high-margin cash generators, supporting store-level profitability and free cash flow.

International Partnerships and Wholesale

Card Factory expanded internationally via a capital-light wholesale model, landing major partners in the US, Australia and South Africa and targeting scale beyond the saturated UK high street.

The international/wholesale segment grew over 20% in 2025, helped by acquisition of Garlanna and Garven which opened North American and Irish routes to market.

Integration and initial logistics absorbed cash in 2025—management reported ~£18m one-off set-up costs—but the segment sits in a high-growth niche with sizable untapped demand.

The stated goal is to scale global wholesale to diversify revenue; management targets international sales contributing 25% of group revenue by 2028.

Funky Pigeon Digital Platform

Following Card Factory’s late-2025 acquisition, Funky Pigeon anchors the group in the high-growth online personalised cards and gifting market, with UK digital sales growing ~12% CAGR 2022–25 and Funky Pigeon holding ~22% share as the sector’s #2.

It supplies the platform, tech stack and brand reach to rival pure-play retailers; Card Factory is investing £35m through 2026 to integrate Bristol and Guernsey teams into its vertical manufacturing model.

Integration aims to cut fulfilment lead times by ~25% and lift digital gross margin from ~38% to a target ~44% by FY2027; this unit is therefore a classic BCG star needing continued innovation.

Omnichannel Retail Integration

Omnichannel Retail Integration lets Card Factory convert 24 million unique annual in-store customers into digital revenue by linking in-store convenience with online personalization, targeting tech-savvy value shoppers and boosting ARPU.

The rollout requires ~£25–35m upfront for POS upgrades and digital marketing, raising short-term capex but protecting share versus online-only rivals; success could drive mid-single-digit CAGR in sales over 2026–2035.

- 24M unique in-store customers

- £25–35m estimated upfront cost

- Targets tech-savvy value segment

- Potential mid-single-digit CAGR 2026–2035

Seasonal and Licensed Ranges

Card Factory’s seasonal and licensed ranges are Stars: Mother’s Day and Valentine’s Day 2024 drove record sales, with Q1 seasonal uplifts up ~18% year-on-year and licensed products contributing ~22% of seasonal revenue.

High-growth peaks face fierce competition but give Card Factory strong market share among value retailers, capturing an estimated 28% of UK seasonal card spend in key windows.

The group invested ~£6.5m in design and creative IP in FY2024 to refresh licences and exclusives, keeping ranges top choice for UK shoppers.

These ranges boost footfall and brand dominance during critical trading weeks, representing the Stars in the BCG matrix for Card Factory.

- Q1 seasonal sales +18% YoY (2024)

- Licensed products ≈22% of seasonal revenue

- Estimated 28% market share in peak windows

- £6.5m design/IP investment in FY2024

Stars' omnichannel push fuels double-digit growth—seasonal +18%, intl +20%, capex £25–35m

Stars: seasonal/licensed and omnichannel gifts drove double-digit growth—Q1 seasonal +18% YoY (2024); licensed = 22% seasonal revenue; seasonal market share ~28%; confectionery/soft toys LFL +12–18% in H1 2025; international/wholesale +20% in 2025; Funky Pigeon digital gross margin target ~44% by FY2027; upfront omnichannel spend £25–35m.

| Metric | Value |

|---|---|

| Q1 seasonal YoY | +18% |

| Licensed share | 22% |

| Seasonal market share | 28% |

| Confectionery LFL | +12–18% |

| Intl growth 2025 | +20% |

| Omnichannel capex | £25–35m |

What is included in the product

BCG Matrix review of Card Factory: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest recommendations per unit.

One-page BCG Matrix placing Card Factory units in quadrants for quick strategic clarity and decision-making

Cash Cows

Core UK Greeting Cards

The Core UK greeting cards business is the group's cash cow, holding roughly 30%–35% UK market share in a mature, low-growth sector (industry growth ~1% in 2024) and delivering modest like-for-like sales growth of ~2%–3%.

It supplies most operating cash flow—Card Factory reported £62m adjusted operating cash flow in H1 2025—thanks to vertical integration: in-house design and manufacturing keeps gross margins near 60% and trims third-party costs.

Management uses this steady cash "milk" to fund international roll-out (20+ store openings since 2023) and a multi-year digital transformation programme with c.£25m committed through 2025.

UK Physical Store Estate

With 1,100+ UK stores, Card Factory’s physical estate is a classic cash cow: high visibility, low category growth, yet same-store sales outperformed UK retail by ~2.5ppt in FY 2024 (like-for-like sales +1.8% vs UK retail -0.7%).

These locations convert footfall into steady cash with low incremental marketing spend; space-optimization has been capex-light, boosting sales per sqm by ~6% since 2022.

Operating cash flow from stores funds a progressive dividend (2024 payout 6.0p per share) and helps service net debt (~£120m at Dec 2024).

Everyday Value Ranges

Everyday Value Ranges deliver steady cash flow for Card Factory Plc, with value lines accounting for about 45% of store sales in FY2024 and maintaining market share among price-sensitive shoppers during downturns.

These low-price SKUs need minimal promotion since Card Factory is widely seen as the high-street lowest-price option, cutting marketing spend by an estimated 12% versus premium ranges.

Predictable weekly demand for basic cards and party basics enables optimized inventory and a 6–8x annual stock turnover, supporting margins despite lower unit prices.

Reliable margins from this segment funded 60% of FY2024 investment in higher-growth product testing and seasonal innovation pilots.

Vertical Manufacturing (Printcraft)

Printcraft, Card Factory Plc’s in-house manufacturing arm, produces ~70% of the group’s card stock, cutting per-unit costs by an estimated 30% versus third-party suppliers and capturing the manufacturer’s margin to lift group gross margin by ~150–200 basis points in FY2024 (year to 26 March 2024).

It operates in a mature, low-growth internal market where capacity matches retail demand; capital spend was £8.5m in FY2024 to sustain efficiency, and volume-driven cost savings are a key source of Card Factory’s everyday-low-pricing strategy.

- Produces ~70% of card stock

- ~30% lower unit cost vs external suppliers

- Adds ~150–200 bps to group gross margin (FY2024)

- £8.5m capex in FY2024 to maintain capacity

Established Third-Party Partnerships

Established wholesale agreements with retailers such as Aldi and The Reject Shop deliver steady, low-maintenance revenue—Card Factory Plc reported wholesale sales of £45m in FY 2024, roughly 12% of group revenue.

These deals use existing product lines and logistics, needing minimal capex to retain high channel market share and ~18% gross margins, so they act as mature, high-margin cash generators.

This reliable cash flow funds aggressive international expansion efforts without diluting core operations.

- Wholesale sales £45m FY2024

- ~12% of group revenue

- ~18% gross margin

- Low capex, high cash conversion

Card Factory: UK cash cow powering margin gains, £62m OCF H1 and £25m growth spend

Card Factory’s UK core is the cash cow: ~1,100 stores, 30–35% market share, like-for-like sales +1.8% FY2024, and it produced £62m adjusted operating cash flow H1 2025; Printcraft supplies ~70% of stock, cutting unit costs ~30% and adding ~150–200bps to gross margin; wholesale ¥45m FY2024 (~12% revenue) and value ranges (45% of sales) sustain steady cash for digital and international rollout (c.£25m through 2025).

| Metric | Value |

|---|---|

| Stores | 1,100+ |

| Market share | 30–35% |

| Adj OCF | £62m H1 2025 |

| Printcraft % | ~70% |

| Wholesale | £45m FY2024 |

| Capex committed | £25m to 2025 |

What You’re Viewing Is Included

Card Factory Plc BCG Matrix

The file you're previewing is the exact Card Factory Plc BCG Matrix report you'll receive after purchase—no watermarks, placeholders, or demo content—just a fully formatted, analysis-ready document crafted for strategic clarity and professional use.