Card Factory Plc Porter's Five Forces Analysis

Don't Miss the Bigger Picture

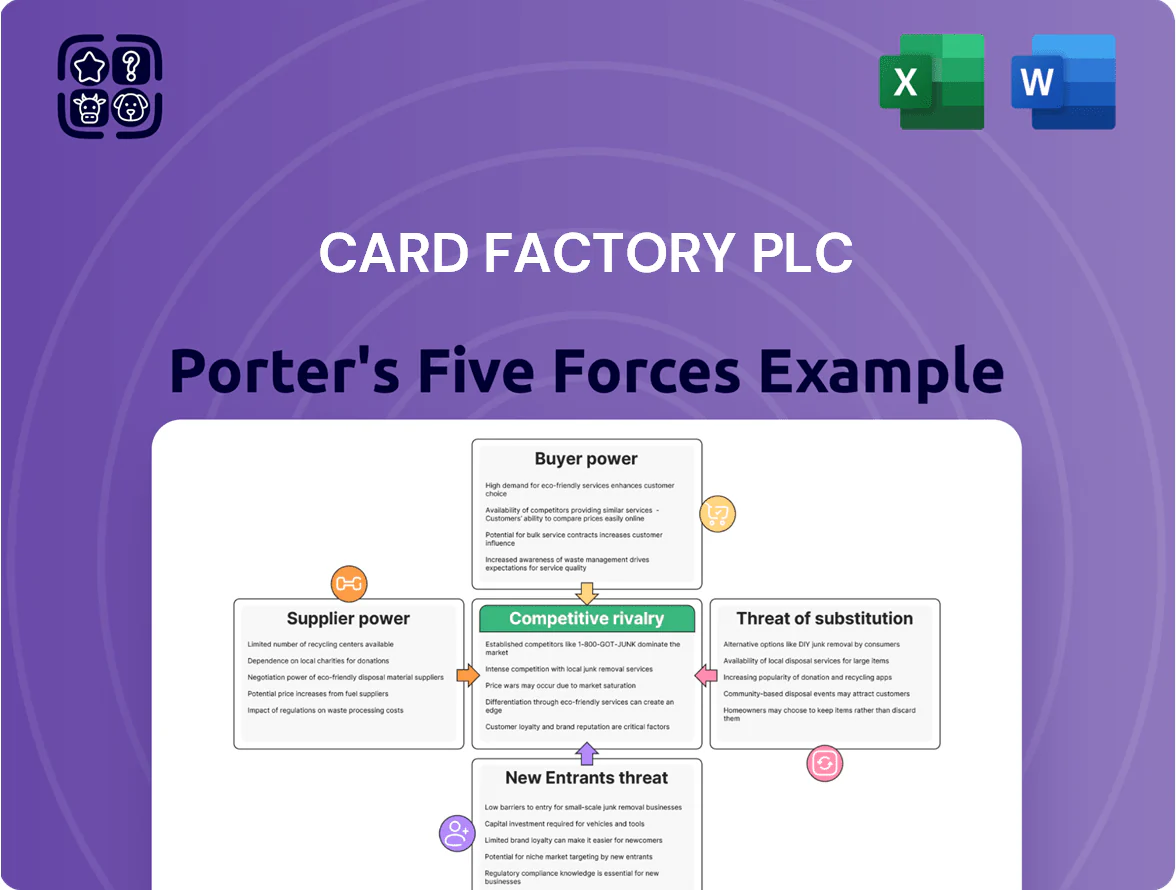

Card Factory faces moderate buyer power, intense rivalry in mass-market gifting, and subdued supplier leverage—while online substitutes and occasional new entrants pressure margins and growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Card Factory Plc’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration and Self Manufacturing

Card Factory prints about 70% of its greeting cards in-house, cutting supplier dependence and lowering unit production costs by an estimated 8–12% versus outsourced peers (FY 2024 internal cost analysis).

This vertical integration gives Card Factory stronger pricing control and faster SKU turnover, reducing lead times from weeks to days and shrinkage in supplier bargaining power.

By bypassing wholesalers, the retailer preserves gross margin—Group gross margin was 44.1% in FY 2024—limiting supplier leverage in negotiations.

Volume Driven Procurement Leverage

Card Factory Plc buys huge volumes of paper, ink and envelopes—retail value revenues were £515m in FY2024—letting it secure supplier discounts of 5–15% on commodities and long-term supply contracts. Suppliers view Card Factory as a trophy client, so bargaining power shifts to Card Factory through volume rebates, priority fulfilment and tighter price collars. This scale reduces input-cost volatility and raises competitors’ procurement costs.

Diversification of Third Party Vendors

Card Factory manufactures cards in-house but sources gifts and partyware from multiple external suppliers, mainly in Asia; in FY2024 about 60% of non-card SKU value came from Asian vendors, per company trading updates.

Maintaining a broad, non-exclusive supplier base prevents over-reliance on any single manufacturer, so supplier-switching is operationally simple and keeps bargaining power low.

Exposure to Global Commodity Prices

Despite internal manufacturing strengths, Card Factory remains exposed to global paper pulp and energy prices; paper accounted for roughly 35% of COGS in 2024 and UK wholesale power rose ~18% year-on-year in 2023–24, so suppliers gain leverage during shortages or inflationary spikes.

Hedging covers short-term swings, but sustained raw material price rises compress gross margin—Card Factory’s 2024 gross margin fell to ~44.5% from 46.8% in 2022—showing supplier-driven cost pressure.

- Paper pulp + energy key inputs

- Paper ~35% of COGS (2024)

- UK wholesale power +18% (2023–24)

- Gross margin 46.8% → 44.5% (2022→2024)

Logistics and Freight Dependency

Card Factory depends on international shipping and UK logistics to move goods to ~900 stores; in 2024 global container rates averaged about $1,200 per FEU, and fuel surcharges rose 18% in 2023–24, boosting input costs.

Because a few major carriers control primary shipping lanes, Card Factory has limited leverage; supply-chain disruptions or freight spikes force acceptance of higher landed costs to keep shelves stocked.

- ~900 stores; global container avg $1,200/FEU (2024)

- Fuel surcharges +18% (2023–24)

- Concentration of major carriers = higher supplier leverage

- Disruptions → must absorb or pass on costs

Card Factory’s 70% in-house production & 44% margin: supplier leverage vs paper/energy risks

Card Factory’s 70% in-house card production, £515m retail revenue (FY2024) and 900 stores give it strong supplier leverage, securing 5–15% commodity discounts and protecting a 44.1% gross margin; paper (~35% of COGS) and energy/freight spikes (UK power +18%, container ~$1,200/FEU in 2024) remain risk points that can temporarily boost supplier power.

| Metric | Value (2024) |

|---|---|

| In-house card production | 70% |

| Retail revenue | £515m |

| Gross margin | 44.1% |

| Paper share of COGS | ~35% |

| UK power change (2023–24) | +18% |

| Avg container rate | $1,200/FEU |

What is included in the product

Tailored Porter's Five Forces analysis for Card Factory Plc, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers affecting its pricing, margins, and market positioning.

A concise Porter's Five Forces snapshot for Card Factory Plc—quickly identify competitive threats and bargaining pressures to support faster strategic decisions.

Customers Bargaining Power

Low Switching Costs for Consumers

Shoppers face virtually no financial or psychological barrier to switch from Card Factory; typical greeting cards cost £1–£5, so a few pence difference drives switching. The UK retail mix—26,000 convenience stores, 7,000 supermarkets, plus online options—gives plentiful alternatives and easy walk-away behavior. Low friction means Card Factory must compete on price and shelf availability; in FY2024 like-for-like sales were volatile, so stock and discounting strategies are critical to limit churn.

High Price Sensitivity in the Value Segment

The core Card Factory customer is drawn by low prices; 2024 sales mix shows private-label and value lines drove 68% of UK in-store revenue, so shoppers compare prices with Aldi, Lidl and Poundland ranges.

These buyers are highly price-sensitive: a 1% price rise risks a 1.5–2% volume drop (retail elasticity estimate), limiting pricing power and margin expansion.

Availability of Convenient Alternatives

Supermarkets like Tesco and Sainsbury’s erode Card Factory Plc customer loyalty by bundling cards with grocery trips, with UK supermarket card sales estimated at ~£300m annually in 2024, so shoppers save time by buying cards during weekly shops rather than making a separate trip; this convenience strengthens buyers’ power since they can switch to one-stop retailers without depending on specialty chains, pressuring Card Factory’s footfall and margin.

Impact of Online Transparency

The rise of e-commerce makes price and design comparison instant, with Moonpig reporting a 2024 digital revenue of £142m and Etsy showing 2024 GMV up 14% year-on-year, so Card Factory faces well-informed customers who can shop alternatives on mobile in seconds.

This online transparency narrows Card Factory’s pricing power, forces continuous digital promotions and UX investment, and limits control of the market narrative as customers easily switch to competitors.

- Mobile search speeds comparison

- Moonpig £142m digital revenue (2024)

- Etsy GMV +14% (2024)

- Higher promotion and UX spend required

Discretionary Nature of Spending

- Non-essential: high opt-out risk in downturns

- Digital substitutes rising: lower per-unit spend

- Need value: price, exclusives, experience

High buyer power, fierce competition — price sensitivity (-1.5 to -2.0) squeezes margins

Buyers have strong bargaining power: low switch costs, many retail alternatives (26,000 convenience stores, 7,000 supermarkets), and online rivals (Moonpig digital revenue £142m in 2024) make price the key driver; estimated price elasticity ~-1.5 to -2.0 limits Card Factory’s pricing power and forces higher promo and UX spend to retain footfall and margin.

| Metric | Value (2024) |

|---|---|

| Convenience stores | 26,000 |

| Supermarkets | 7,000 |

| Moonpig digital revenue | £142m |

| Estimated price elasticity | -1.5 to -2.0 |

Full Version Awaits

Card Factory Plc Porter's Five Forces Analysis

This preview shows the exact Card Factory Plc Porter’s Five Forces analysis you’ll receive immediately after purchase—no samples or placeholders—fully formatted and ready for download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Card Factory faces moderate buyer power, intense rivalry in mass-market gifting, and subdued supplier leverage—while online substitutes and occasional new entrants pressure margins and growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Card Factory Plc’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration and Self Manufacturing

Card Factory prints about 70% of its greeting cards in-house, cutting supplier dependence and lowering unit production costs by an estimated 8–12% versus outsourced peers (FY 2024 internal cost analysis).

This vertical integration gives Card Factory stronger pricing control and faster SKU turnover, reducing lead times from weeks to days and shrinkage in supplier bargaining power.

By bypassing wholesalers, the retailer preserves gross margin—Group gross margin was 44.1% in FY 2024—limiting supplier leverage in negotiations.

Volume Driven Procurement Leverage

Card Factory Plc buys huge volumes of paper, ink and envelopes—retail value revenues were £515m in FY2024—letting it secure supplier discounts of 5–15% on commodities and long-term supply contracts. Suppliers view Card Factory as a trophy client, so bargaining power shifts to Card Factory through volume rebates, priority fulfilment and tighter price collars. This scale reduces input-cost volatility and raises competitors’ procurement costs.

Diversification of Third Party Vendors

Card Factory manufactures cards in-house but sources gifts and partyware from multiple external suppliers, mainly in Asia; in FY2024 about 60% of non-card SKU value came from Asian vendors, per company trading updates.

Maintaining a broad, non-exclusive supplier base prevents over-reliance on any single manufacturer, so supplier-switching is operationally simple and keeps bargaining power low.

Exposure to Global Commodity Prices

Despite internal manufacturing strengths, Card Factory remains exposed to global paper pulp and energy prices; paper accounted for roughly 35% of COGS in 2024 and UK wholesale power rose ~18% year-on-year in 2023–24, so suppliers gain leverage during shortages or inflationary spikes.

Hedging covers short-term swings, but sustained raw material price rises compress gross margin—Card Factory’s 2024 gross margin fell to ~44.5% from 46.8% in 2022—showing supplier-driven cost pressure.

- Paper pulp + energy key inputs

- Paper ~35% of COGS (2024)

- UK wholesale power +18% (2023–24)

- Gross margin 46.8% → 44.5% (2022→2024)

Logistics and Freight Dependency

Card Factory depends on international shipping and UK logistics to move goods to ~900 stores; in 2024 global container rates averaged about $1,200 per FEU, and fuel surcharges rose 18% in 2023–24, boosting input costs.

Because a few major carriers control primary shipping lanes, Card Factory has limited leverage; supply-chain disruptions or freight spikes force acceptance of higher landed costs to keep shelves stocked.

- ~900 stores; global container avg $1,200/FEU (2024)

- Fuel surcharges +18% (2023–24)

- Concentration of major carriers = higher supplier leverage

- Disruptions → must absorb or pass on costs

Card Factory’s 70% in-house production & 44% margin: supplier leverage vs paper/energy risks

Card Factory’s 70% in-house card production, £515m retail revenue (FY2024) and 900 stores give it strong supplier leverage, securing 5–15% commodity discounts and protecting a 44.1% gross margin; paper (~35% of COGS) and energy/freight spikes (UK power +18%, container ~$1,200/FEU in 2024) remain risk points that can temporarily boost supplier power.

| Metric | Value (2024) |

|---|---|

| In-house card production | 70% |

| Retail revenue | £515m |

| Gross margin | 44.1% |

| Paper share of COGS | ~35% |

| UK power change (2023–24) | +18% |

| Avg container rate | $1,200/FEU |

What is included in the product

Tailored Porter's Five Forces analysis for Card Factory Plc, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers affecting its pricing, margins, and market positioning.

A concise Porter's Five Forces snapshot for Card Factory Plc—quickly identify competitive threats and bargaining pressures to support faster strategic decisions.

Customers Bargaining Power

Low Switching Costs for Consumers

Shoppers face virtually no financial or psychological barrier to switch from Card Factory; typical greeting cards cost £1–£5, so a few pence difference drives switching. The UK retail mix—26,000 convenience stores, 7,000 supermarkets, plus online options—gives plentiful alternatives and easy walk-away behavior. Low friction means Card Factory must compete on price and shelf availability; in FY2024 like-for-like sales were volatile, so stock and discounting strategies are critical to limit churn.

High Price Sensitivity in the Value Segment

The core Card Factory customer is drawn by low prices; 2024 sales mix shows private-label and value lines drove 68% of UK in-store revenue, so shoppers compare prices with Aldi, Lidl and Poundland ranges.

These buyers are highly price-sensitive: a 1% price rise risks a 1.5–2% volume drop (retail elasticity estimate), limiting pricing power and margin expansion.

Availability of Convenient Alternatives

Supermarkets like Tesco and Sainsbury’s erode Card Factory Plc customer loyalty by bundling cards with grocery trips, with UK supermarket card sales estimated at ~£300m annually in 2024, so shoppers save time by buying cards during weekly shops rather than making a separate trip; this convenience strengthens buyers’ power since they can switch to one-stop retailers without depending on specialty chains, pressuring Card Factory’s footfall and margin.

Impact of Online Transparency

The rise of e-commerce makes price and design comparison instant, with Moonpig reporting a 2024 digital revenue of £142m and Etsy showing 2024 GMV up 14% year-on-year, so Card Factory faces well-informed customers who can shop alternatives on mobile in seconds.

This online transparency narrows Card Factory’s pricing power, forces continuous digital promotions and UX investment, and limits control of the market narrative as customers easily switch to competitors.

- Mobile search speeds comparison

- Moonpig £142m digital revenue (2024)

- Etsy GMV +14% (2024)

- Higher promotion and UX spend required

Discretionary Nature of Spending

- Non-essential: high opt-out risk in downturns

- Digital substitutes rising: lower per-unit spend

- Need value: price, exclusives, experience

High buyer power, fierce competition — price sensitivity (-1.5 to -2.0) squeezes margins

Buyers have strong bargaining power: low switch costs, many retail alternatives (26,000 convenience stores, 7,000 supermarkets), and online rivals (Moonpig digital revenue £142m in 2024) make price the key driver; estimated price elasticity ~-1.5 to -2.0 limits Card Factory’s pricing power and forces higher promo and UX spend to retain footfall and margin.

| Metric | Value (2024) |

|---|---|

| Convenience stores | 26,000 |

| Supermarkets | 7,000 |

| Moonpig digital revenue | £142m |

| Estimated price elasticity | -1.5 to -2.0 |

Full Version Awaits

Card Factory Plc Porter's Five Forces Analysis

This preview shows the exact Card Factory Plc Porter’s Five Forces analysis you’ll receive immediately after purchase—no samples or placeholders—fully formatted and ready for download and use.