Cardlytics Boston Consulting Group Matrix

See the Bigger Picture

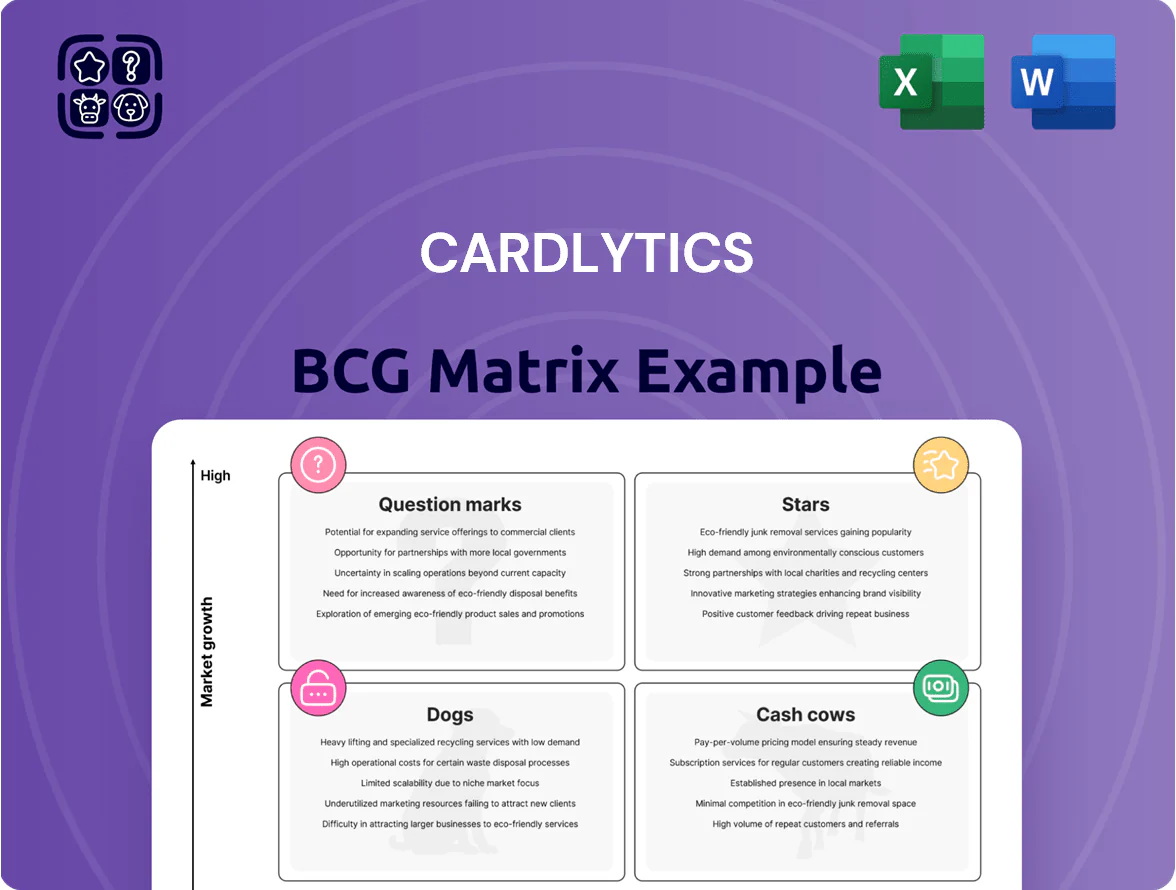

Cardlytics sits at the intersection of ad tech and fintech, with high-growth advertising products showing star potential while legacy partnerships may resemble cash cows needing efficiency improvements; pockets of underperforming offerings could be dogs or question marks pending strategic investment. This preview highlights competitive positioning and market dynamics—purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide smart product and capital decisions.

Stars

U.K. Market Expansion

The U.K. unit is a Star: Cardlytics reported a 22% revenue rise in late 2025 in the U.K., outpacing overall growth as U.S. bank partner limits pressured domestic sales.

The segment capitalized on first-mover advantage in European card-linked offers, capturing key merchants and increasing take rates versus peers.

Sustained growth needs continued investment in local merchant partnerships and sales—expect reinvestment to keep the U.K. as a primary growth engine.

Cardlytics Rewards Platform (CRP)

Launched as a cornerstone of Cardlytics diversification, Cardlytics Rewards Platform (CRP) extends ads beyond bank apps to new digital properties and signed its first major non-bank partners in 2025, including a leading digital sports platform that opens an addressable audience of ~25M monthly users.

As a new product in the $55B global commerce media market (2025 estimate), CRP is a Star: high growth and high investment, requiring elevated promotional spend—Cardlytics signaled ~20–30% incremental marketing allocation—to win share from retail media networks.

Monthly Qualified User (MQU) Growth

Cardlytics grew Monthly Qualified Users 21% YoY to 230.3 million by end-2025, capturing a dominant slice of the addressable digital-banking audience and creating a strong moat via first-party purchase data.

That scale fuels ad product reach in commerce media as advertisers move to privacy-safe channels; sustaining the lead needs ongoing infrastructure capex and data engineering investment.

Self-Service Advertiser Tools

Self-Service Advertiser Tools rolled out in 2024–2025 opened Cardlytics to agencies and SMBs, expanding advertisers from ~120 enterprise clients to over 3,400 advertisers by Q4 2025 and driving a faster growth rate than enterprise revenue (SMB ad bookings grew ~48% YoY vs enterprise ~12%).

This segment diversifies revenue away from top-10 clients that once made ~42% of ad revenue; SMBs now contribute ~27% of total ad revenue, lowering concentration risk and improving ARPU mix.

These tools scale demand-side reach but need continuous engineering investment—Cardlytics increased ad-tech R&D spend by ~22% in 2025—to match programmatic features and reporting offered by competitors.

- Rolled out 2024–2025

- Advertisers grew to ~3,400 by Q4 2025

- SMB bookings +48% YoY (2025)

- SMBs ≈27% of ad revenue

- R&D spend +22% (2025)

Next-Gen Data Insights Portal

The mid-2025 launch of Next-Gen Data Insights Portal (Customer Insights Dashboards) cemented Cardlytics as a leader in closed-loop measurement for offline sales, driving strong adoption among performance marketers and lifting deal win rates by double digits.

With global retail media spend topping $120 billion in 2024 and projected 12% CAGR to 2027, the Portal captures high market share by mapping digital ads to actual in-store spend using aggregated bank-verified transaction data.

Its granular consumer-spend segments and ROI attribution reduce campaign waste and boost measured offline lift, positioning the product as a Star in Cardlytics’ BCG Matrix.

- Launch: mid-2025

- Market: retail media > $120B (2024)

- Growth: ~12% CAGR to 2027

- Benefit: bank-verified transaction attribution

Strong growth: 230.3M MQUs, UK +22%, SMB bookings +48% amid heavy R&D reinvestment

Stars: U.K. unit, Cardlytics Rewards Platform, Self-Service tools, and Next‑Gen Portal drive high growth and require sustained reinvestment; combined MQUs 230.3M (2025), UK rev +22% (late 2025), SMB bookings +48% YoY (2025), ad-tech R&D +22% (2025).

| Metric | Value |

|---|---|

| MQUs | 230.3M (2025) |

| UK rev growth | +22% (late 2025) |

| SMB bookings | +48% YoY (2025) |

| R&D spend | +22% (2025) |

What is included in the product

BCG Matrix analysis of Cardlytics' units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page Cardlytics BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Core U.S. Bank Partnerships

Core U.S. Bank partnerships, led by JPMorgan Chase and Wells Fargo, generate the bulk of Cardlytics’ cash flow, accounting for roughly 60–70% of platform revenue in 2024 per company disclosures.

These mature deals reach millions of customers with low incremental maintenance costs versus new launches, improving margin predictability and free cash flow conversion.

Extending Chase through 2028 secures a reliably milkable asset that funds R&D and higher-growth initiatives; Chase accounted for ~35% of revenue in 2024.

Enterprise Retail Advertising

Enterprise Retail Advertising drives steady cash for Cardlytics: Fortune 500 retail and dining campaigns accounted for roughly 48% of 2025 ad billings, with gross margins near 65% and net retention above 110%, per company disclosures and industry reports.

Card-Linked Offer (CLO) Network

As owner of the largest card-linked offer (CLO) network in the US, Cardlytics held roughly 40% merchant-funded offer share and processed ~\$12.5B in annualized purchase volume in 2024, giving it a mature, low-competition position at scale.

That dominance let Cardlytics report positive adjusted EBITDA in FY2024 despite a ~6% YoY revenue decline, producing free cash flow used to pay down \$140M of corporate debt in 2024 and fund the Cardlytics Rewards Platform pivot.

Anonymized Purchase Data Licensing

Cardlytics monetizes anonymized purchase data from over $5.8 trillion in annual consumer spend, making this a high-margin, low-maintenance cash cow that funds operations during restructuring.

Data licensing yields gross margins above 60% (2024 reported trends) and recurring contracts with major brands, supplying steady EBITDA support while core product pivots pursue growth.

Because the data is a byproduct of account-based offers, incremental cost is low yet demand is high: licensing contributed a material portion of 2024 revenue stability and cash flow.

- Source pool: $5.8 trillion annual spend

- Gross margins: >60% (2024 trends)

- Role: recurring, high-margin cash flow

- Benefit: funds restructuring and product investment

Direct-to-Consumer (DTC) Advertiser Base

A steady cohort of established direct-to-consumer (DTC) brands has made Cardlytics a permanent part of their media mixes, delivering predictable recurring revenue—Cardlytics reported $476M revenue in FY2024, with DTC and retail partnerships a major contributor.

These advertisers favor Cardlytics for measurable incremental sales and lower ROAS volatility than social platforms; Cardlytics’ 2024 average campaign ROI uplift studies showed 10–25% incremental sales per campaign.

Because this mature segment needs minimal new acquisition spend from Cardlytics, it functions as a reliable liquidity source, supporting margins and cash flow while growth investments target other quadrants.

- Recurring revenue from DTC: stabilizes cash flow

- Incremental sales uplift: ~10–25% per campaign (2024)

- Low churn and minimal marketing spend to retain

- Supports margins and reinvestment for growth

Cardlytics: High‑margin bank deals & data driving $476M revenue, $5.8T spend access

Cardlytics’ cash cows: core U.S. bank deals (Chase ~35% of 2024 revenue; banks 60–70% of platform revenue in 2024), Enterprise Retail Advertising (48% of 2025 ad billings; ~65% gross margin), data licensing (>60% gross margins; access to $5.8T spend; processed ~$12.5B purchase volume in 2024), and recurring DTC/retail revenue (FY2024 revenue $476M; campaign uplift 10–25%).

| Metric | Value |

|---|---|

| FY2024 Revenue | $476M |

| Chase share (2024) | ~35% |

| Banks share (2024) | 60–70% |

| Processed volume (2024) | $12.5B |

| Annual spend pool | $5.8T |

| Ad billings (retail, 2025) | 48% |

| Gross margins (data/retail) | ~60–65% |

Preview = Final Product

Cardlytics BCG Matrix

The Cardlytics BCG Matrix you're previewing here is the exact document you'll receive after purchase—fully formatted, watermark-free, and ready for professional use.

This preview mirrors the final BCG Matrix report, blending market-backed insights with clear visuals so you can present, edit, or print immediately after download.

No demo content or placeholders—just a strategy-ready file crafted by experts for seamless integration into your planning or client materials.

Purchase grants instant access to the complete, analysis-ready Cardlytics BCG Matrix for immediate deployment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Cardlytics sits at the intersection of ad tech and fintech, with high-growth advertising products showing star potential while legacy partnerships may resemble cash cows needing efficiency improvements; pockets of underperforming offerings could be dogs or question marks pending strategic investment. This preview highlights competitive positioning and market dynamics—purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide smart product and capital decisions.

Stars

U.K. Market Expansion

The U.K. unit is a Star: Cardlytics reported a 22% revenue rise in late 2025 in the U.K., outpacing overall growth as U.S. bank partner limits pressured domestic sales.

The segment capitalized on first-mover advantage in European card-linked offers, capturing key merchants and increasing take rates versus peers.

Sustained growth needs continued investment in local merchant partnerships and sales—expect reinvestment to keep the U.K. as a primary growth engine.

Cardlytics Rewards Platform (CRP)

Launched as a cornerstone of Cardlytics diversification, Cardlytics Rewards Platform (CRP) extends ads beyond bank apps to new digital properties and signed its first major non-bank partners in 2025, including a leading digital sports platform that opens an addressable audience of ~25M monthly users.

As a new product in the $55B global commerce media market (2025 estimate), CRP is a Star: high growth and high investment, requiring elevated promotional spend—Cardlytics signaled ~20–30% incremental marketing allocation—to win share from retail media networks.

Monthly Qualified User (MQU) Growth

Cardlytics grew Monthly Qualified Users 21% YoY to 230.3 million by end-2025, capturing a dominant slice of the addressable digital-banking audience and creating a strong moat via first-party purchase data.

That scale fuels ad product reach in commerce media as advertisers move to privacy-safe channels; sustaining the lead needs ongoing infrastructure capex and data engineering investment.

Self-Service Advertiser Tools

Self-Service Advertiser Tools rolled out in 2024–2025 opened Cardlytics to agencies and SMBs, expanding advertisers from ~120 enterprise clients to over 3,400 advertisers by Q4 2025 and driving a faster growth rate than enterprise revenue (SMB ad bookings grew ~48% YoY vs enterprise ~12%).

This segment diversifies revenue away from top-10 clients that once made ~42% of ad revenue; SMBs now contribute ~27% of total ad revenue, lowering concentration risk and improving ARPU mix.

These tools scale demand-side reach but need continuous engineering investment—Cardlytics increased ad-tech R&D spend by ~22% in 2025—to match programmatic features and reporting offered by competitors.

- Rolled out 2024–2025

- Advertisers grew to ~3,400 by Q4 2025

- SMB bookings +48% YoY (2025)

- SMBs ≈27% of ad revenue

- R&D spend +22% (2025)

Next-Gen Data Insights Portal

The mid-2025 launch of Next-Gen Data Insights Portal (Customer Insights Dashboards) cemented Cardlytics as a leader in closed-loop measurement for offline sales, driving strong adoption among performance marketers and lifting deal win rates by double digits.

With global retail media spend topping $120 billion in 2024 and projected 12% CAGR to 2027, the Portal captures high market share by mapping digital ads to actual in-store spend using aggregated bank-verified transaction data.

Its granular consumer-spend segments and ROI attribution reduce campaign waste and boost measured offline lift, positioning the product as a Star in Cardlytics’ BCG Matrix.

- Launch: mid-2025

- Market: retail media > $120B (2024)

- Growth: ~12% CAGR to 2027

- Benefit: bank-verified transaction attribution

Strong growth: 230.3M MQUs, UK +22%, SMB bookings +48% amid heavy R&D reinvestment

Stars: U.K. unit, Cardlytics Rewards Platform, Self-Service tools, and Next‑Gen Portal drive high growth and require sustained reinvestment; combined MQUs 230.3M (2025), UK rev +22% (late 2025), SMB bookings +48% YoY (2025), ad-tech R&D +22% (2025).

| Metric | Value |

|---|---|

| MQUs | 230.3M (2025) |

| UK rev growth | +22% (late 2025) |

| SMB bookings | +48% YoY (2025) |

| R&D spend | +22% (2025) |

What is included in the product

BCG Matrix analysis of Cardlytics' units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page Cardlytics BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Core U.S. Bank Partnerships

Core U.S. Bank partnerships, led by JPMorgan Chase and Wells Fargo, generate the bulk of Cardlytics’ cash flow, accounting for roughly 60–70% of platform revenue in 2024 per company disclosures.

These mature deals reach millions of customers with low incremental maintenance costs versus new launches, improving margin predictability and free cash flow conversion.

Extending Chase through 2028 secures a reliably milkable asset that funds R&D and higher-growth initiatives; Chase accounted for ~35% of revenue in 2024.

Enterprise Retail Advertising

Enterprise Retail Advertising drives steady cash for Cardlytics: Fortune 500 retail and dining campaigns accounted for roughly 48% of 2025 ad billings, with gross margins near 65% and net retention above 110%, per company disclosures and industry reports.

Card-Linked Offer (CLO) Network

As owner of the largest card-linked offer (CLO) network in the US, Cardlytics held roughly 40% merchant-funded offer share and processed ~\$12.5B in annualized purchase volume in 2024, giving it a mature, low-competition position at scale.

That dominance let Cardlytics report positive adjusted EBITDA in FY2024 despite a ~6% YoY revenue decline, producing free cash flow used to pay down \$140M of corporate debt in 2024 and fund the Cardlytics Rewards Platform pivot.

Anonymized Purchase Data Licensing

Cardlytics monetizes anonymized purchase data from over $5.8 trillion in annual consumer spend, making this a high-margin, low-maintenance cash cow that funds operations during restructuring.

Data licensing yields gross margins above 60% (2024 reported trends) and recurring contracts with major brands, supplying steady EBITDA support while core product pivots pursue growth.

Because the data is a byproduct of account-based offers, incremental cost is low yet demand is high: licensing contributed a material portion of 2024 revenue stability and cash flow.

- Source pool: $5.8 trillion annual spend

- Gross margins: >60% (2024 trends)

- Role: recurring, high-margin cash flow

- Benefit: funds restructuring and product investment

Direct-to-Consumer (DTC) Advertiser Base

A steady cohort of established direct-to-consumer (DTC) brands has made Cardlytics a permanent part of their media mixes, delivering predictable recurring revenue—Cardlytics reported $476M revenue in FY2024, with DTC and retail partnerships a major contributor.

These advertisers favor Cardlytics for measurable incremental sales and lower ROAS volatility than social platforms; Cardlytics’ 2024 average campaign ROI uplift studies showed 10–25% incremental sales per campaign.

Because this mature segment needs minimal new acquisition spend from Cardlytics, it functions as a reliable liquidity source, supporting margins and cash flow while growth investments target other quadrants.

- Recurring revenue from DTC: stabilizes cash flow

- Incremental sales uplift: ~10–25% per campaign (2024)

- Low churn and minimal marketing spend to retain

- Supports margins and reinvestment for growth

Cardlytics: High‑margin bank deals & data driving $476M revenue, $5.8T spend access

Cardlytics’ cash cows: core U.S. bank deals (Chase ~35% of 2024 revenue; banks 60–70% of platform revenue in 2024), Enterprise Retail Advertising (48% of 2025 ad billings; ~65% gross margin), data licensing (>60% gross margins; access to $5.8T spend; processed ~$12.5B purchase volume in 2024), and recurring DTC/retail revenue (FY2024 revenue $476M; campaign uplift 10–25%).

| Metric | Value |

|---|---|

| FY2024 Revenue | $476M |

| Chase share (2024) | ~35% |

| Banks share (2024) | 60–70% |

| Processed volume (2024) | $12.5B |

| Annual spend pool | $5.8T |

| Ad billings (retail, 2025) | 48% |

| Gross margins (data/retail) | ~60–65% |

Preview = Final Product

Cardlytics BCG Matrix

The Cardlytics BCG Matrix you're previewing here is the exact document you'll receive after purchase—fully formatted, watermark-free, and ready for professional use.

This preview mirrors the final BCG Matrix report, blending market-backed insights with clear visuals so you can present, edit, or print immediately after download.

No demo content or placeholders—just a strategy-ready file crafted by experts for seamless integration into your planning or client materials.

Purchase grants instant access to the complete, analysis-ready Cardlytics BCG Matrix for immediate deployment.