Cardlytics SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Cardlytics leverages unique bank-partnered consumer purchase data and targeted advertising to drive strong merchant ROI, but faces competitive ad tech pressure and regulatory/data-privacy risks; uncover the full strategic implications and financial context in our complete SWOT analysis—purchase the editable Word + Excel report for investor-ready insights and tactical recommendations.

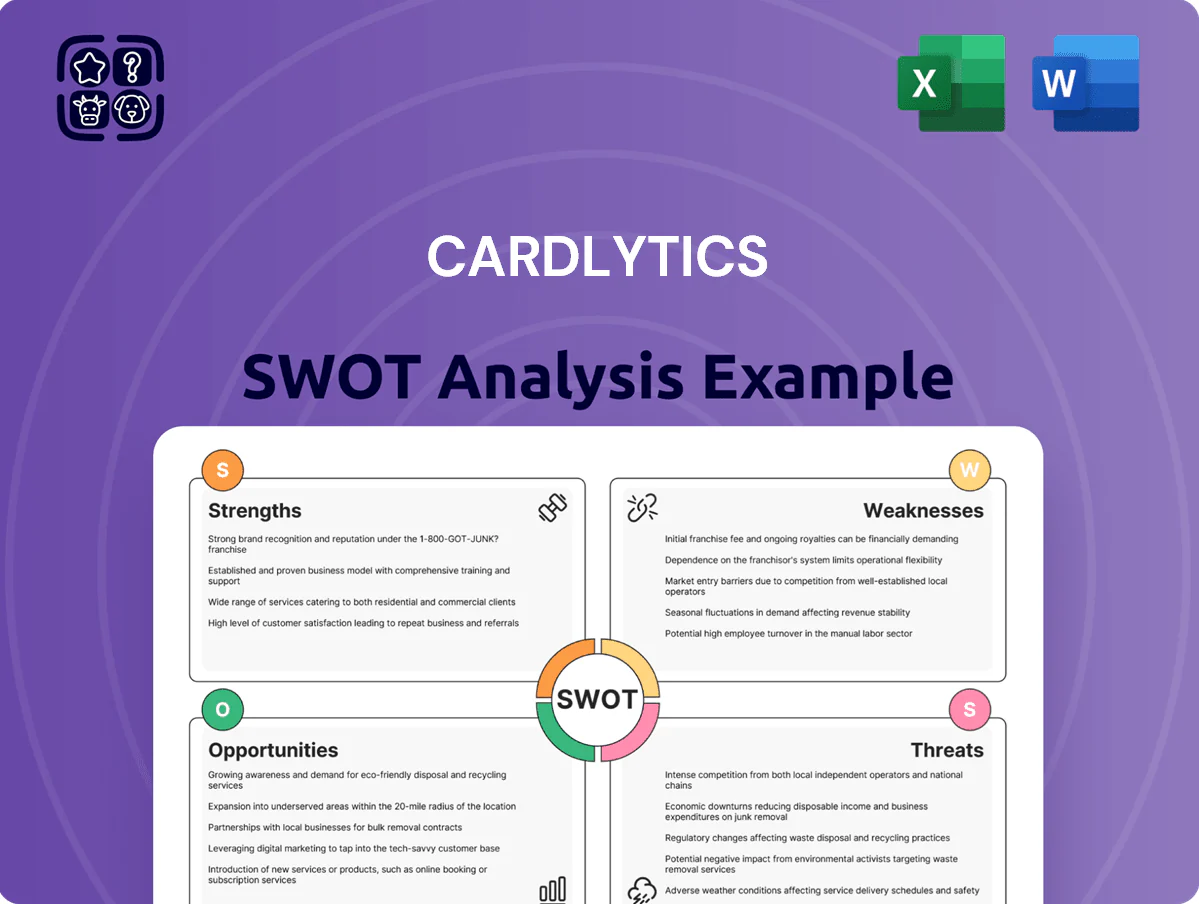

Strengths

Deep Integration with Financial Institutions

Cardlytics holds long-term integrations with banks such as JPMorgan Chase, Bank of America, and Wells Fargo, giving it direct access to over 100 million active online banking users as of 2025. These partnerships create a high-trust, hard-to-replicate ecosystem because of complex API, security, and regulatory requirements in banking software. That scale drives predictable monthly reach and ad spend conversion inside primary financial apps.

Access to Deterministic Purchase Data

Cardlytics uses actual bank transaction data, not inferred browsing signals, giving advertisers precise spend-level targeting and measurement; in 2024 Cardlytics reported processing $100B+ in purchase volume and delivered ROI lifts averaging 3x for top retail clients. This deterministic dataset enables closed-loop attribution—linking ad impressions to real sales—so marketers can prove incremental revenue and justify spend with transaction-backed KPIs like CPA and LTV.

Highly Scaleable Advertising Network

Frictionless User Experience

- Integrated in bank apps — no apps/coupons

- +18% active engagement (2024)

- 4–6% conversion vs 0.5–1% display

- ~12% merchant transaction lift

Privacy-First Architecture

Cardlytics uses anonymized transaction signals and runs analytics inside partner banks' firewalls so no personally identifiable information is shared with advertisers, preserving customer privacy and reducing breach risk.

This privacy-first design complies with 2025 regulations like updated EU GDPR guidance and US state laws, and sidesteps third-party cookie loss—supporting targeted offers while keeping data in-bank.

That security posture helped Cardlytics retain 95% of its major bank partners through 2024 and supports revenue stability tied to $1.2B in 2024 purchase-intent signals processed.

- In-bank processing: no PII shared

- Compliant with 2025 privacy rules

- Resilient to cookie deprecation

- 95% major-bank retention (2024)

- $1.2B in purchase signals processed (2024)

Cardlytics: 100M+ users, $100B purchases, ~28% growth and ~5x ROAS

Cardlytics' bank integrations reach 100M+ online users (2025) and 1,400 banks/CUs (70% U.S. deposits), processing $100B+ purchase volume (2024) and $1.2B purchase-intent signals, driving platform revenue +28% YoY (2025), advertiser ROAS ~5x and conversion 4–6% with ~12% merchant lift; 95% major-bank retention (2024) and privacy-first in-bank processing preserve compliance.

| Metric | Value |

|---|---|

| Online users (2025) | 100M+ |

| Banks/credit unions (2025) | 1,400 |

| % U.S. deposits | 70% |

| Purchase volume (2024) | $100B+ |

| Purchase-intent signals (2024) | $1.2B |

| Revenue growth (2025) | ~28% YoY |

| Advertiser ROAS | ~5x |

| Conversion rate | 4–6% |

| Merchant lift | ~12% |

| Major-bank retention (2024) | 95% |

What is included in the product

Delivers a strategic overview of Cardlytics’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position in the card-linked marketing and advertising ecosystem.

Provides a concise SWOT matrix tailored to Cardlytics for fast, visual alignment of marketing and partnership strategies.

Weaknesses

Heavy Concentration on Top Banking Partners

A large share of Cardlytics' revenue and active-user reach is concentrated in a few banks—JPMorgan Chase and Bank of America alone accounted for roughly 30–40% of tracked deposits and partner-driven ad spend in 2024, per company disclosures and industry reports. If a top partner terminated its deal or built an in-house offers platform, Cardlytics would face a severe revenue shock and user loss. This dependence weakens long-term revenue stability and leaves Cardlytics with limited pricing and contract leverage.

Complexity of the Sales Cycle

User Interface Limitations

Cardlytics’ offers live inside banks’ apps, so the company has limited control over visual placement; poor app navigation or clutter can cut offer visibility by over 30% according to 2024 merchant attribution studies, lowering click-through rates versus feed-based ads.

This restriction on creative control reduces campaign effectiveness: Cardlytics’ average CTRs (~0.3%–0.6% in 2023 reports) lag behind Instagram (1.1%–1.5%) and Google Display (0.5%–1.0%), hurting ROI for advertisers.

Dependence on Discretionary Spending

Cardlytics' revenue tracks consumer transactions, especially dining, travel, and retail; US consumer card spend in these categories fell 3.2% y/y in Q4 2024, hurting commission pools.

High inflation and recession risk make spend-sensitive commission income cyclical; Cardlytics reported 2024 net revenue down 5% y/y, showing sensitivity vs subscription peers.

- Revenue tied to transaction volume

- Q4 2024 US dining/travel spending -3.2% y/y

- 2024 net revenue -5% y/y

- More cyclical than subscription models

Limited Global Footprint

- Regulatory gaps: varied banking rules per country raise integration costs

- Consumer differences: loyalty and payment habits vary by market

- Fragmentation: dozens of local banks needed versus few US partners

- Revenue concentration: ~90%+ NA revenue in FY2024 limits growth runway

Concentrated bank revenue, long onboarding, low CTRs—2024 revs down, NA‑centric

Revenue concentrated in few banks (JPMorgan, BofA ~30–40% of deposits/ad spend 2024), long 18–36 month bank onboarding, limited app placement reduces CTR (Cardlytics 0.3–0.6% vs IG 1.1–1.5%), revenue cyclical (2024 net revenue -5% y/y; US dining/travel spend -3.2% Q4 2024), 90%+ revenue North America exposure.

| Metric | 2024 |

|---|---|

| Top‑bank share | 30–40% |

| Onboard time | 18–36 months |

| CTR | 0.3–0.6% |

| Net rev change | -5% y/y |

| NA revenue | 90%+ |

Preview Before You Purchase

Cardlytics SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Cardlytics leverages unique bank-partnered consumer purchase data and targeted advertising to drive strong merchant ROI, but faces competitive ad tech pressure and regulatory/data-privacy risks; uncover the full strategic implications and financial context in our complete SWOT analysis—purchase the editable Word + Excel report for investor-ready insights and tactical recommendations.

Strengths

Deep Integration with Financial Institutions

Cardlytics holds long-term integrations with banks such as JPMorgan Chase, Bank of America, and Wells Fargo, giving it direct access to over 100 million active online banking users as of 2025. These partnerships create a high-trust, hard-to-replicate ecosystem because of complex API, security, and regulatory requirements in banking software. That scale drives predictable monthly reach and ad spend conversion inside primary financial apps.

Access to Deterministic Purchase Data

Cardlytics uses actual bank transaction data, not inferred browsing signals, giving advertisers precise spend-level targeting and measurement; in 2024 Cardlytics reported processing $100B+ in purchase volume and delivered ROI lifts averaging 3x for top retail clients. This deterministic dataset enables closed-loop attribution—linking ad impressions to real sales—so marketers can prove incremental revenue and justify spend with transaction-backed KPIs like CPA and LTV.

Highly Scaleable Advertising Network

Frictionless User Experience

- Integrated in bank apps — no apps/coupons

- +18% active engagement (2024)

- 4–6% conversion vs 0.5–1% display

- ~12% merchant transaction lift

Privacy-First Architecture

Cardlytics uses anonymized transaction signals and runs analytics inside partner banks' firewalls so no personally identifiable information is shared with advertisers, preserving customer privacy and reducing breach risk.

This privacy-first design complies with 2025 regulations like updated EU GDPR guidance and US state laws, and sidesteps third-party cookie loss—supporting targeted offers while keeping data in-bank.

That security posture helped Cardlytics retain 95% of its major bank partners through 2024 and supports revenue stability tied to $1.2B in 2024 purchase-intent signals processed.

- In-bank processing: no PII shared

- Compliant with 2025 privacy rules

- Resilient to cookie deprecation

- 95% major-bank retention (2024)

- $1.2B in purchase signals processed (2024)

Cardlytics: 100M+ users, $100B purchases, ~28% growth and ~5x ROAS

Cardlytics' bank integrations reach 100M+ online users (2025) and 1,400 banks/CUs (70% U.S. deposits), processing $100B+ purchase volume (2024) and $1.2B purchase-intent signals, driving platform revenue +28% YoY (2025), advertiser ROAS ~5x and conversion 4–6% with ~12% merchant lift; 95% major-bank retention (2024) and privacy-first in-bank processing preserve compliance.

| Metric | Value |

|---|---|

| Online users (2025) | 100M+ |

| Banks/credit unions (2025) | 1,400 |

| % U.S. deposits | 70% |

| Purchase volume (2024) | $100B+ |

| Purchase-intent signals (2024) | $1.2B |

| Revenue growth (2025) | ~28% YoY |

| Advertiser ROAS | ~5x |

| Conversion rate | 4–6% |

| Merchant lift | ~12% |

| Major-bank retention (2024) | 95% |

What is included in the product

Delivers a strategic overview of Cardlytics’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position in the card-linked marketing and advertising ecosystem.

Provides a concise SWOT matrix tailored to Cardlytics for fast, visual alignment of marketing and partnership strategies.

Weaknesses

Heavy Concentration on Top Banking Partners

A large share of Cardlytics' revenue and active-user reach is concentrated in a few banks—JPMorgan Chase and Bank of America alone accounted for roughly 30–40% of tracked deposits and partner-driven ad spend in 2024, per company disclosures and industry reports. If a top partner terminated its deal or built an in-house offers platform, Cardlytics would face a severe revenue shock and user loss. This dependence weakens long-term revenue stability and leaves Cardlytics with limited pricing and contract leverage.

Complexity of the Sales Cycle

User Interface Limitations

Cardlytics’ offers live inside banks’ apps, so the company has limited control over visual placement; poor app navigation or clutter can cut offer visibility by over 30% according to 2024 merchant attribution studies, lowering click-through rates versus feed-based ads.

This restriction on creative control reduces campaign effectiveness: Cardlytics’ average CTRs (~0.3%–0.6% in 2023 reports) lag behind Instagram (1.1%–1.5%) and Google Display (0.5%–1.0%), hurting ROI for advertisers.

Dependence on Discretionary Spending

Cardlytics' revenue tracks consumer transactions, especially dining, travel, and retail; US consumer card spend in these categories fell 3.2% y/y in Q4 2024, hurting commission pools.

High inflation and recession risk make spend-sensitive commission income cyclical; Cardlytics reported 2024 net revenue down 5% y/y, showing sensitivity vs subscription peers.

- Revenue tied to transaction volume

- Q4 2024 US dining/travel spending -3.2% y/y

- 2024 net revenue -5% y/y

- More cyclical than subscription models

Limited Global Footprint

- Regulatory gaps: varied banking rules per country raise integration costs

- Consumer differences: loyalty and payment habits vary by market

- Fragmentation: dozens of local banks needed versus few US partners

- Revenue concentration: ~90%+ NA revenue in FY2024 limits growth runway

Concentrated bank revenue, long onboarding, low CTRs—2024 revs down, NA‑centric

Revenue concentrated in few banks (JPMorgan, BofA ~30–40% of deposits/ad spend 2024), long 18–36 month bank onboarding, limited app placement reduces CTR (Cardlytics 0.3–0.6% vs IG 1.1–1.5%), revenue cyclical (2024 net revenue -5% y/y; US dining/travel spend -3.2% Q4 2024), 90%+ revenue North America exposure.

| Metric | 2024 |

|---|---|

| Top‑bank share | 30–40% |

| Onboard time | 18–36 months |

| CTR | 0.3–0.6% |

| Net rev change | -5% y/y |

| NA revenue | 90%+ |

Preview Before You Purchase

Cardlytics SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.