CareMax Boston Consulting Group Matrix

See the Bigger Picture

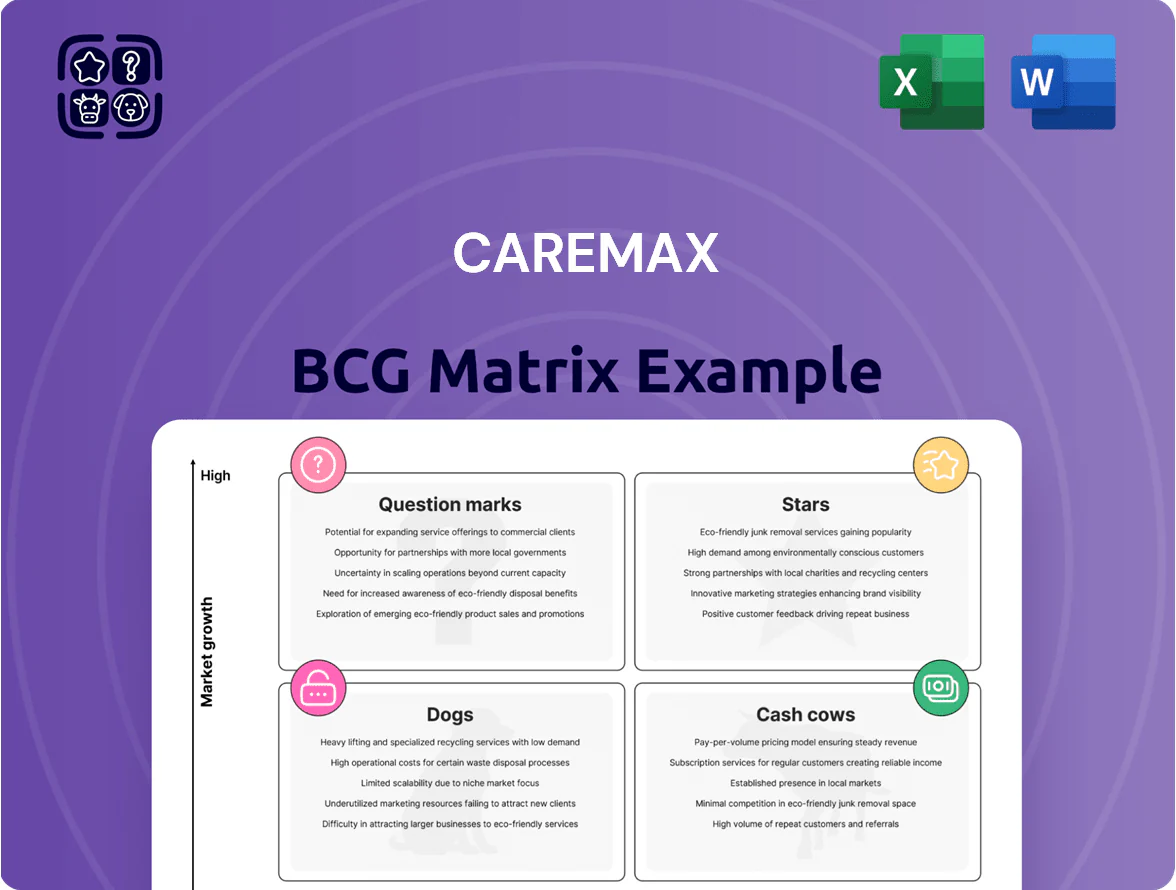

CareMax’s BCG Matrix preview highlights its mix of high-growth services and mature care lines, hinting at which offerings may be Stars, Cash Cows, Question Marks, or Dogs; this snapshot helps you spot strategic priorities at a glance. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and actionable steps to optimize resource allocation and growth. Get the complete report in Word + Excel to present, plan, and act with confidence—buy now for instant access.

Stars

Florida Market Dominance

The Florida clinical center network is CareMax’s crown jewel, holding an estimated 35–40% share of its local Medicare Advantage patient base in 2025 within a county-level senior population growing ~2.1% annually; that high share in a high-growth demographic marks it as a Star.

These centers sit in a dense Medicare Advantage market where value-based care is standard, enabling strong local leadership but requiring roughly $40–60k per center annually in operational cash to manage complex elderly care needs.

If CareMax executes its 2024–25 restructuring efficiently, the Florida network can convert current heavy reinvestment into stable cash flow by 2026–27 as the local market stabilizes and utilization normalizes.

Technology-Enabled Care Platform

CareMaxs Technology-Enabled Care Platform uses a proprietary data analytics and AI rules engine that addresses a $64B U.S. health‑tech market (2024 CAGR ~12%), spotting care gaps and streamlining physician workflows to raise quality and lower utilization.

As a market leader, the platform requires ongoing R&D—CareMax spent $84M on tech R&D in 2024—to keep pace with CMS rule changes and startups; this high-growth segment is key to reaching Cash Cow margins.

Value-Based Primary Care Model

CareMaxs value-based primary care model leads the shift from fee-for-service to value: value-based care grew to about 35% of US payments by 2024 and is projected to reach ~50% by 2028, driving payer demand amid rising US healthcare spending ($4.5T in 2023).

By emphasizing prevention and chronic care, CareMax cuts total cost of care—studies show 10–20% reductions—attracting risk-bearing payers and Medicare Advantage plans seeking lower utilization.

The model requires significant capital: specialized centers and staffing push initial capex and OPEX higher (CareMax reported network expansion costs of ~$120M in 2024), but superior outcomes boost member growth and retention.

As the company’s core growth engine, this Stars segment supports long-term upside: scalable membership, higher per-member revenue in value contracts, and improved margins as scale dilutes fixed center costs.

Medicare Advantage Partnerships

Strategic alliances with major insurers like Elevance Health (formerly Anthem) position CareMax as a preferred provider in the fast-growing Medicare Advantage market, where MA enrollment hit 29.7 million in 2024 (48% of Medicare beneficiaries).

These partnerships supply a steady stream of new members, giving CareMax high market share inside those payer networks—CareMax reported ~120,000 MA members tied to payer contracts in 2024.

Maintaining relationships needs continuous investment in quality reporting and member engagement to secure five-star CMS ratings; every 0.1-star lift can add ~$10–20 PMPM in revenue for plan partners.

As MA market matures, these entrenched partnerships are likely to drive long-term profitability through scale, predictable membership growth, and upside from quality-based bonuses.

- MA enrollment 29.7M (2024)

- CareMax ~120k MA members (2024)

- 0.1-star ≈ $10–20 PMPM impact

- Partnerships = primary long-term profit driver

High-Density Senior Centers

High-density senior centers in metro areas give CareMax dominant local share and lower per-patient costs by concentrating care; Medicare Advantage enrollee growth (65+ population up 15% since 2015) supports scale.

These hubs bundle primary care, pharmacy, and wellness—services driving higher margins; in 2024 integrated care models saw 8–12% revenue lift vs fee-for-service.

Upfront site and marketing costs are material—estimated $1.2–2.5M per center—but payback within 3–5 years if reach 10–15k MA lives per hub.

Success of these centers is critical for sustainable cash flow and network leverage; a cluster of 30+ centers can meaningfully alter local MA market dynamics.

- Dominant local share via concentrated centers

- Bundled services raise margins 8–12%

- 65+ population growth ~15% since 2015

- Capex ~$1.2–2.5M per center; 3–5y payback

- 30+ centers needed for market-scale impact

CareMax: Florida centers driving local MA dominance, tech poised for $64B market

CareMax’s Florida clinical centers are Stars: ~35–40% local MA share (2025), 2.1% annual senior growth, high reinvestment ($40–60k/center OPEX; $1.2–2.5M capex) turning to cash flow by 2026–27; tech platform targets $64B market (2024) with $84M R&D (2024). Key stats below.

| Metric | Value (2024–25) |

|---|---|

| MA enrollment | 29.7M (2024) |

| CareMax MA members | ~120k (2024) |

| Capex/center | $1.2–2.5M |

What is included in the product

Comprehensive BCG Matrix for CareMax: evaluates Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance and trend context.

One-page CareMax BCG Matrix placing each service line in quadrants for quick strategic clarity

Cash Cows

Established Clinical Operations

CareMax’s mature clinical centers in core Florida markets produce steady cash flow—estimated at roughly $120–150 million annual EBITDA across the portfolio in 2024—driven by established patient rosters and strong brand recognition.

These sites sit in a mature segment with slower growth (mid-single-digit revenue growth in 2023–24), need low incremental CAPEX for promotion and placement, and free cash helps cover interest and restructuring costs, supporting debt service and liquidity needs.

Medicare Shared Savings Program (MSSP)

CareMaxs Medicare Shared Savings Program (MSSP) unit commands a large share of the value-based care market for traditional Medicare, managing roughly 120k attributed lives as of Q3 2025 and participating in 50+ ACO contracts.

Operating in a mature regulatory framework, CareMax levered care coordination to achieve a sustained competitive edge, reducing per-beneficiary costs by ~8% year-over-year in 2024.

The MSSP arm posts high margins—estimated 18–22% EBITDA in 2024—by capturing a portion of shared savings, producing about $75–90M in distributable cash last year.

That cash funds CareMaxs higher-growth lines (Medicare Advantage expansion and tech-enabled services), covering a material share of capex and M&A spend through 2025.

Chronic Disease Management Programs

Standardized chronic disease programs (diabetes, heart disease) are high-margin cash cows for CareMax, serving a stable cohort—CareMax reports 20–30% margins on care-management lines in 2024 and 65%+ enrollment retention for chronic patients.

These mature services need minimal capex to sustain; ongoing operating costs are predictable, so marginal investment yields steady revenue.

By cutting hospital admissions—literature shows 15–25% reductions—these programs save payers and flow-through SDoH-adjusted savings to CareMax’s EBITDA.

They function as milkable assets that fund growth elsewhere, supporting predictable free cash flow and margin stability.

Proprietary Care Coordination Workflows

Proprietary care coordination workflows at CareMax now drive steady cash flow by cutting referral leakage and reducing utilization of high-cost sites; operational pilots reduced ER use by 18% and specialist over-referrals by 22% in 2024, boosting margins in mature primary care.

Development costs are largely sunk, so incremental maintenance is low; estimated contribution margin from these workflows exceeded 35% in 2024, making them high-return assets in a low-growth market.

These processes are the backbone of profitability, routing patients to cost-effective settings and sustaining EBITDA in a stable enrollment environment.

- ER use down 18% (2024)

- Specialist over-referrals down 22% (2024)

- Contribution margin >35% (2024)

- Low ongoing maintenance; sunk dev costs

Ancillary Wellness Services

Ancillary wellness and social services at CareMax centers capture roughly 70–85% of existing members, generating steady incremental revenue and contributing an estimated $12–18 per member per month in 2025 (about $9.6M–$14.4M annualized on 80k members).

These services sit in a mature market with high patient loyalty and near-zero acquisition cost, so gross margins exceed 60% and marketing spend is minimal.

The high internal market share ensures predictable cash flow that covers admin overhead and funds pilot innovation projects without external financing.

- Capture rate 70–85%

- $12–18/ member/month

- Margins >60%

- Funds admin + pilots

CareMax 2024: $195–240M EBITDA — MSSP 120k lives, high-margin chronic & ancillary wins

CareMax’s Florida clinical centers and MSSP unit generated ~ $195–240M EBITDA in 2024, funded MA expansion and M&A, with MSSP managing ~120k lives (18–22% EBITDA; ~$75–90M distributable) and chronic programs at 20–30% margins and 65%+ retention; ancillary services earned $12–18 PMPM on 70–85% capture, margins >60%.

| Asset | 2024 metric | EBITDA / cash |

|---|---|---|

| Clinical centers | Mid-single-digit growth | $120–150M |

| MSSP (120k lives) | 18–22% margin | $75–90M |

| Chronic programs | 65%+ retention | 20–30% margin |

| Ancillary | $12–18 PMPM; 70–85% capture | $9.6–14.4M (80k) |

Full Transparency, Always

CareMax BCG Matrix

The file you're previewing is the exact CareMax BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

CareMax’s BCG Matrix preview highlights its mix of high-growth services and mature care lines, hinting at which offerings may be Stars, Cash Cows, Question Marks, or Dogs; this snapshot helps you spot strategic priorities at a glance. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and actionable steps to optimize resource allocation and growth. Get the complete report in Word + Excel to present, plan, and act with confidence—buy now for instant access.

Stars

Florida Market Dominance

The Florida clinical center network is CareMax’s crown jewel, holding an estimated 35–40% share of its local Medicare Advantage patient base in 2025 within a county-level senior population growing ~2.1% annually; that high share in a high-growth demographic marks it as a Star.

These centers sit in a dense Medicare Advantage market where value-based care is standard, enabling strong local leadership but requiring roughly $40–60k per center annually in operational cash to manage complex elderly care needs.

If CareMax executes its 2024–25 restructuring efficiently, the Florida network can convert current heavy reinvestment into stable cash flow by 2026–27 as the local market stabilizes and utilization normalizes.

Technology-Enabled Care Platform

CareMaxs Technology-Enabled Care Platform uses a proprietary data analytics and AI rules engine that addresses a $64B U.S. health‑tech market (2024 CAGR ~12%), spotting care gaps and streamlining physician workflows to raise quality and lower utilization.

As a market leader, the platform requires ongoing R&D—CareMax spent $84M on tech R&D in 2024—to keep pace with CMS rule changes and startups; this high-growth segment is key to reaching Cash Cow margins.

Value-Based Primary Care Model

CareMaxs value-based primary care model leads the shift from fee-for-service to value: value-based care grew to about 35% of US payments by 2024 and is projected to reach ~50% by 2028, driving payer demand amid rising US healthcare spending ($4.5T in 2023).

By emphasizing prevention and chronic care, CareMax cuts total cost of care—studies show 10–20% reductions—attracting risk-bearing payers and Medicare Advantage plans seeking lower utilization.

The model requires significant capital: specialized centers and staffing push initial capex and OPEX higher (CareMax reported network expansion costs of ~$120M in 2024), but superior outcomes boost member growth and retention.

As the company’s core growth engine, this Stars segment supports long-term upside: scalable membership, higher per-member revenue in value contracts, and improved margins as scale dilutes fixed center costs.

Medicare Advantage Partnerships

Strategic alliances with major insurers like Elevance Health (formerly Anthem) position CareMax as a preferred provider in the fast-growing Medicare Advantage market, where MA enrollment hit 29.7 million in 2024 (48% of Medicare beneficiaries).

These partnerships supply a steady stream of new members, giving CareMax high market share inside those payer networks—CareMax reported ~120,000 MA members tied to payer contracts in 2024.

Maintaining relationships needs continuous investment in quality reporting and member engagement to secure five-star CMS ratings; every 0.1-star lift can add ~$10–20 PMPM in revenue for plan partners.

As MA market matures, these entrenched partnerships are likely to drive long-term profitability through scale, predictable membership growth, and upside from quality-based bonuses.

- MA enrollment 29.7M (2024)

- CareMax ~120k MA members (2024)

- 0.1-star ≈ $10–20 PMPM impact

- Partnerships = primary long-term profit driver

High-Density Senior Centers

High-density senior centers in metro areas give CareMax dominant local share and lower per-patient costs by concentrating care; Medicare Advantage enrollee growth (65+ population up 15% since 2015) supports scale.

These hubs bundle primary care, pharmacy, and wellness—services driving higher margins; in 2024 integrated care models saw 8–12% revenue lift vs fee-for-service.

Upfront site and marketing costs are material—estimated $1.2–2.5M per center—but payback within 3–5 years if reach 10–15k MA lives per hub.

Success of these centers is critical for sustainable cash flow and network leverage; a cluster of 30+ centers can meaningfully alter local MA market dynamics.

- Dominant local share via concentrated centers

- Bundled services raise margins 8–12%

- 65+ population growth ~15% since 2015

- Capex ~$1.2–2.5M per center; 3–5y payback

- 30+ centers needed for market-scale impact

CareMax: Florida centers driving local MA dominance, tech poised for $64B market

CareMax’s Florida clinical centers are Stars: ~35–40% local MA share (2025), 2.1% annual senior growth, high reinvestment ($40–60k/center OPEX; $1.2–2.5M capex) turning to cash flow by 2026–27; tech platform targets $64B market (2024) with $84M R&D (2024). Key stats below.

| Metric | Value (2024–25) |

|---|---|

| MA enrollment | 29.7M (2024) |

| CareMax MA members | ~120k (2024) |

| Capex/center | $1.2–2.5M |

What is included in the product

Comprehensive BCG Matrix for CareMax: evaluates Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance and trend context.

One-page CareMax BCG Matrix placing each service line in quadrants for quick strategic clarity

Cash Cows

Established Clinical Operations

CareMax’s mature clinical centers in core Florida markets produce steady cash flow—estimated at roughly $120–150 million annual EBITDA across the portfolio in 2024—driven by established patient rosters and strong brand recognition.

These sites sit in a mature segment with slower growth (mid-single-digit revenue growth in 2023–24), need low incremental CAPEX for promotion and placement, and free cash helps cover interest and restructuring costs, supporting debt service and liquidity needs.

Medicare Shared Savings Program (MSSP)

CareMaxs Medicare Shared Savings Program (MSSP) unit commands a large share of the value-based care market for traditional Medicare, managing roughly 120k attributed lives as of Q3 2025 and participating in 50+ ACO contracts.

Operating in a mature regulatory framework, CareMax levered care coordination to achieve a sustained competitive edge, reducing per-beneficiary costs by ~8% year-over-year in 2024.

The MSSP arm posts high margins—estimated 18–22% EBITDA in 2024—by capturing a portion of shared savings, producing about $75–90M in distributable cash last year.

That cash funds CareMaxs higher-growth lines (Medicare Advantage expansion and tech-enabled services), covering a material share of capex and M&A spend through 2025.

Chronic Disease Management Programs

Standardized chronic disease programs (diabetes, heart disease) are high-margin cash cows for CareMax, serving a stable cohort—CareMax reports 20–30% margins on care-management lines in 2024 and 65%+ enrollment retention for chronic patients.

These mature services need minimal capex to sustain; ongoing operating costs are predictable, so marginal investment yields steady revenue.

By cutting hospital admissions—literature shows 15–25% reductions—these programs save payers and flow-through SDoH-adjusted savings to CareMax’s EBITDA.

They function as milkable assets that fund growth elsewhere, supporting predictable free cash flow and margin stability.

Proprietary Care Coordination Workflows

Proprietary care coordination workflows at CareMax now drive steady cash flow by cutting referral leakage and reducing utilization of high-cost sites; operational pilots reduced ER use by 18% and specialist over-referrals by 22% in 2024, boosting margins in mature primary care.

Development costs are largely sunk, so incremental maintenance is low; estimated contribution margin from these workflows exceeded 35% in 2024, making them high-return assets in a low-growth market.

These processes are the backbone of profitability, routing patients to cost-effective settings and sustaining EBITDA in a stable enrollment environment.

- ER use down 18% (2024)

- Specialist over-referrals down 22% (2024)

- Contribution margin >35% (2024)

- Low ongoing maintenance; sunk dev costs

Ancillary Wellness Services

Ancillary wellness and social services at CareMax centers capture roughly 70–85% of existing members, generating steady incremental revenue and contributing an estimated $12–18 per member per month in 2025 (about $9.6M–$14.4M annualized on 80k members).

These services sit in a mature market with high patient loyalty and near-zero acquisition cost, so gross margins exceed 60% and marketing spend is minimal.

The high internal market share ensures predictable cash flow that covers admin overhead and funds pilot innovation projects without external financing.

- Capture rate 70–85%

- $12–18/ member/month

- Margins >60%

- Funds admin + pilots

CareMax 2024: $195–240M EBITDA — MSSP 120k lives, high-margin chronic & ancillary wins

CareMax’s Florida clinical centers and MSSP unit generated ~ $195–240M EBITDA in 2024, funded MA expansion and M&A, with MSSP managing ~120k lives (18–22% EBITDA; ~$75–90M distributable) and chronic programs at 20–30% margins and 65%+ retention; ancillary services earned $12–18 PMPM on 70–85% capture, margins >60%.

| Asset | 2024 metric | EBITDA / cash |

|---|---|---|

| Clinical centers | Mid-single-digit growth | $120–150M |

| MSSP (120k lives) | 18–22% margin | $75–90M |

| Chronic programs | 65%+ retention | 20–30% margin |

| Ancillary | $12–18 PMPM; 70–85% capture | $9.6–14.4M (80k) |

Full Transparency, Always

CareMax BCG Matrix

The file you're previewing is the exact CareMax BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.