CareMax PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, reimbursement trends, and digital health advances are shaping CareMax’s growth and risks—our concise PESTLE snapshot highlights the external forces that matter most. Ready-made for investors and strategists, the full PESTLE delivers actionable insights, editable charts, and scenario-driven recommendations. Purchase now to download the complete analysis and make smarter, faster decisions.

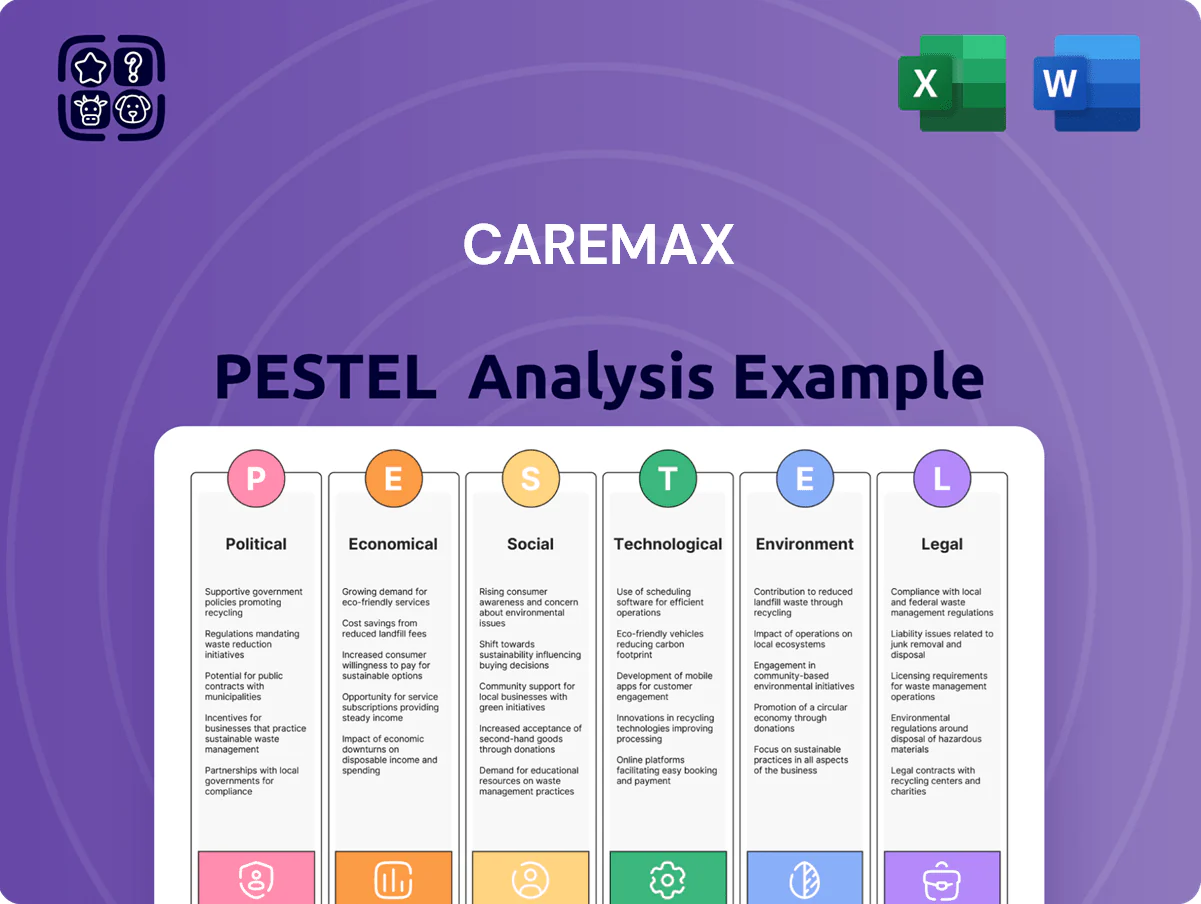

Political factors

Medicare Advantage Regulatory Oversight

As of late 2025 the federal government has tightened Medicare Advantage Star Ratings and risk-adjustment rules, with CMS proposing adjustments that could shift up to 5–8% of plan reimbursements nationwide; CareMax must continually update coding and quality programs to protect revenue tied to ratings. Bipartisan oversight has increased audits and demo projects, pressuring value-based providers to show measurable clinical gains—CareMax reported a 4.2% improvement in HEDIS metrics in 2024 to align with these expectations.

Value-Based Care Legislative Support

Strong bipartisan momentum continues for shifting Medicare and Medicaid toward value-based care; CMS reported 63% of Medicare payments tied to value-based models in 2024, aligning with CareMax’s capitated, outcomes-driven model that targets lower total cost of care and improved metrics.

CareMax benefits from federal incentives and state Medicaid demonstrations expanding integrated primary care, but Congressional turnover can reprioritize funding for community health—federal discretionary public health funding fell 4% real terms in FY2025, posing execution risk.

State-Level Healthcare Regulations

CareMax operates in clustered markets where state healthcare mandates and licensing vary, affecting reimbursement and network requirements; for example Florida tightened MCO reporting by end-2025, raising provider network disclosure and timeliness standards for entities covering ~4.5 million Medicaid beneficiaries.

Public Health Policy Priorities

Federal emphasis on social determinants of health has pushed non-clinical needs into policy; CMS expanded SDOH-related initiatives, with $1.5B in targeted grants in 2024 supporting food, housing, and transport programs for seniors.

CareMax must align services to address food insecurity, transport, and housing to qualify for pilot programs and grants; providers addressing SDOH saw a 12% revenue uplift from value-based contracts in 2023–2024.

- Align services to CMS SDOH grants ($1.5B in 2024)

- Target food, transport, housing for elderly

- Participation in pilots increases grant access

- Addressing SDOH linked to ~12% revenue uplift

Election Cycle Uncertainty

The post-2024 election landscape raises uncertainty for the Affordable Care Act and potential shifts in Medicare funding; federal proposals in 2025 suggested up to a 3–5% realignment in Medicare Advantage payments and renewed debate over ACA subsidy designs that could affect CareMax revenue assumptions.

While demographic trends still favor senior care—Medicare enrollment grew 2.1% in 2024 to 66.1 million—possible restructuring or budgetary reductions to the CMS Innovation Center pose risks to value-based contract stability and multi-year care models.

CareMax should preserve flexibility via scenario-based financial models, contingency cash buffers (targeting 6–9 months operating runway) and adaptable provider contracts to mitigate executive-branch policy shifts.

- 2025 proposals: 3–5% Medicare payment realignment risk

- Medicare enrollees: 66.1M in 2024, +2.1% YoY

- Recommended contingency: 6–9 months operating runway

- Action: scenario planning and flexible provider contracts

Medicare shifts: tighter MA audits, 63% value-payments, $1.5B SDOH—3–8% payment risk

Political shifts tighten Medicare Advantage rules and audits, risking 3–8% reimbursement variance; CMS tied 63% of Medicare payments to value models in 2024, favoring CareMax’s capitated model; $1.5B SDOH grants (2024) and Medicaid demos expand opportunities while FY2025 federal public health funding fell ~4% real; Medicare enrollees 66.1M (2024, +2.1%).

| Metric | Value |

|---|---|

| Medicare enrollees (2024) | 66.1M (+2.1%) |

| MA payment risk | 3–8% potential |

| Value-based payments (2024) | 63% |

| CMS SDOH grants (2024) | $1.5B |

| FY2025 public health funding | -4% real |

What is included in the product

Explores how macro-environmental factors uniquely affect CareMax across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking implications to guide executives, investors, and strategists in identifying risks, opportunities, and scenario-driven actions.

Provides a clean, concise PESTLE snapshot of CareMax to streamline meeting prep and stakeholder briefings, with clearly labeled political, economic, social, technological, legal, and environmental points for quick decision-making.

Economic factors

Inflationary Pressure on Clinical Labor

Rising wages—average RN pay up 6.5% and primary care physician compensation up ~5% in 2024—squeeze CareMax clinic margins as higher salaries and sign-on bonuses become standard to compete for talent.

Intense hiring competition forces CareMax into richer compensation and benefits packages, increasing operating costs and lowering EBITDA unless offset by higher patient volumes or pricing.

Sustained wage inflation pushes CareMax to optimize staffing ratios and expand use of nurse practitioners and physician assistants, who cost 20–40% less than physicians, to preserve margins.

Interest Rate Environment and Capital Access

Following CareMaxs 2024–2025 restructuring, the company remains sensitive to interest rates on roughly $600–700 million of post-reorg debt; a 100 bp rise in rates could add ~$6–7 million annually in interest expense, constraining capital for expansions and tech investments. High borrowing costs have already delayed at least two planned clinic upgrades, and investors now prioritize a strengthened balance sheet and liquidity ratios—net debt/EBITDA targeted below 3.0x.

Medicare Advantage Reimbursement Rates

Annual CMS adjustments to Medicare Advantage benchmarks directly drive CareMax’s revenue; CMS raised MA plan payments by an average 3.7% for 2024 and projected ~2.5% for 2025, but tighter 2024–25 risk-coding audits reduced realized revenue growth by an estimated 1–2 percentage points.

By end-2025 modest rate gains are largely offset by coding pressure, compressing organic membership revenue; CareMax must boost operational efficiency to ensure per-member reimbursement covers rising care management costs, which grew ~6% YoY through 2024.

Consumer Spending on Supplemental Health

Economic downturns that lowered retiree real incomes in 2023–2025 pushed enrollment toward Medicare Advantage; MA enrollment rose to ~50% of Medicare beneficiaries by 2024, reflecting price-sensitive plan choice.

Seniors prioritize out-of-pocket maximums and supplemental benefits (dental/vision), areas where CareMax’s integrated offerings improve value and retention.

When GDP growth slowed in 2023–2024, demand for low-cost, high-value integrated care increased, benefiting models that cap consumer healthcare spending.

- Medicare Advantage ~50% enrollment by 2024

- Seniors prioritize OOP caps and dental/vision

- Weaker economy → higher demand for low-cost integrated care

Cost of Medical Supplies and Technology

Supply chain fluctuations raised procurement costs for medical equipment and pharmaceuticals by an estimated 6-9% in 2024, pressuring CareMax’s margins within its capitated primary care model.

CareMax leverages scale—serving over 250,000 Medicare Advantage members in 2024—to negotiate discounts, yet global inflation and commodity shocks still produced intermittent price spikes of 5-12%.

Active cost management and inventory strategies are essential to preserve profitability under fixed per-member payments.

- 2024 procurement inflation: 6-9%

- Intermittent price spikes: 5-12%

- Membership scale: >250,000 MA members (2024)

CareMax margins pressured by wage, procurement inflation and $650M debt interest risk

Wage inflation (RN +6.5%, PCP +5% in 2024) and hiring competition raise CareMax operating costs; staffing mix shifts to NPs/PAs (20–40% lower cost) to protect margins. Post-reorg debt ~$650m exposes CareMax to interest-rate risk (100 bp ≈ $6–7m/year). CMS MA rate +3.7% (2024) vs realized +1.7–2.7% after coding pressure; procurement inflation 6–9% (2024); MA membership >250k (2024).

| Metric | Value |

|---|---|

| RN pay change (2024) | +6.5% |

| PCP comp (2024) | ~+5% |

| Post-reorg debt | ~$650m |

| Interest sensitivity | 100 bp ≈ $6–7m/yr |

| CMS MA rate change (2024) | +3.7% |

| Realized MA revenue lift | +1.7–2.7% |

| Procurement inflation (2024) | 6–9% |

| MA members (2024) | >250,000 |

Preview Before You Purchase

CareMax PESTLE Analysis

The preview shown here is the exact CareMax PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, reimbursement trends, and digital health advances are shaping CareMax’s growth and risks—our concise PESTLE snapshot highlights the external forces that matter most. Ready-made for investors and strategists, the full PESTLE delivers actionable insights, editable charts, and scenario-driven recommendations. Purchase now to download the complete analysis and make smarter, faster decisions.

Political factors

Medicare Advantage Regulatory Oversight

As of late 2025 the federal government has tightened Medicare Advantage Star Ratings and risk-adjustment rules, with CMS proposing adjustments that could shift up to 5–8% of plan reimbursements nationwide; CareMax must continually update coding and quality programs to protect revenue tied to ratings. Bipartisan oversight has increased audits and demo projects, pressuring value-based providers to show measurable clinical gains—CareMax reported a 4.2% improvement in HEDIS metrics in 2024 to align with these expectations.

Value-Based Care Legislative Support

Strong bipartisan momentum continues for shifting Medicare and Medicaid toward value-based care; CMS reported 63% of Medicare payments tied to value-based models in 2024, aligning with CareMax’s capitated, outcomes-driven model that targets lower total cost of care and improved metrics.

CareMax benefits from federal incentives and state Medicaid demonstrations expanding integrated primary care, but Congressional turnover can reprioritize funding for community health—federal discretionary public health funding fell 4% real terms in FY2025, posing execution risk.

State-Level Healthcare Regulations

CareMax operates in clustered markets where state healthcare mandates and licensing vary, affecting reimbursement and network requirements; for example Florida tightened MCO reporting by end-2025, raising provider network disclosure and timeliness standards for entities covering ~4.5 million Medicaid beneficiaries.

Public Health Policy Priorities

Federal emphasis on social determinants of health has pushed non-clinical needs into policy; CMS expanded SDOH-related initiatives, with $1.5B in targeted grants in 2024 supporting food, housing, and transport programs for seniors.

CareMax must align services to address food insecurity, transport, and housing to qualify for pilot programs and grants; providers addressing SDOH saw a 12% revenue uplift from value-based contracts in 2023–2024.

- Align services to CMS SDOH grants ($1.5B in 2024)

- Target food, transport, housing for elderly

- Participation in pilots increases grant access

- Addressing SDOH linked to ~12% revenue uplift

Election Cycle Uncertainty

The post-2024 election landscape raises uncertainty for the Affordable Care Act and potential shifts in Medicare funding; federal proposals in 2025 suggested up to a 3–5% realignment in Medicare Advantage payments and renewed debate over ACA subsidy designs that could affect CareMax revenue assumptions.

While demographic trends still favor senior care—Medicare enrollment grew 2.1% in 2024 to 66.1 million—possible restructuring or budgetary reductions to the CMS Innovation Center pose risks to value-based contract stability and multi-year care models.

CareMax should preserve flexibility via scenario-based financial models, contingency cash buffers (targeting 6–9 months operating runway) and adaptable provider contracts to mitigate executive-branch policy shifts.

- 2025 proposals: 3–5% Medicare payment realignment risk

- Medicare enrollees: 66.1M in 2024, +2.1% YoY

- Recommended contingency: 6–9 months operating runway

- Action: scenario planning and flexible provider contracts

Medicare shifts: tighter MA audits, 63% value-payments, $1.5B SDOH—3–8% payment risk

Political shifts tighten Medicare Advantage rules and audits, risking 3–8% reimbursement variance; CMS tied 63% of Medicare payments to value models in 2024, favoring CareMax’s capitated model; $1.5B SDOH grants (2024) and Medicaid demos expand opportunities while FY2025 federal public health funding fell ~4% real; Medicare enrollees 66.1M (2024, +2.1%).

| Metric | Value |

|---|---|

| Medicare enrollees (2024) | 66.1M (+2.1%) |

| MA payment risk | 3–8% potential |

| Value-based payments (2024) | 63% |

| CMS SDOH grants (2024) | $1.5B |

| FY2025 public health funding | -4% real |

What is included in the product

Explores how macro-environmental factors uniquely affect CareMax across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking implications to guide executives, investors, and strategists in identifying risks, opportunities, and scenario-driven actions.

Provides a clean, concise PESTLE snapshot of CareMax to streamline meeting prep and stakeholder briefings, with clearly labeled political, economic, social, technological, legal, and environmental points for quick decision-making.

Economic factors

Inflationary Pressure on Clinical Labor

Rising wages—average RN pay up 6.5% and primary care physician compensation up ~5% in 2024—squeeze CareMax clinic margins as higher salaries and sign-on bonuses become standard to compete for talent.

Intense hiring competition forces CareMax into richer compensation and benefits packages, increasing operating costs and lowering EBITDA unless offset by higher patient volumes or pricing.

Sustained wage inflation pushes CareMax to optimize staffing ratios and expand use of nurse practitioners and physician assistants, who cost 20–40% less than physicians, to preserve margins.

Interest Rate Environment and Capital Access

Following CareMaxs 2024–2025 restructuring, the company remains sensitive to interest rates on roughly $600–700 million of post-reorg debt; a 100 bp rise in rates could add ~$6–7 million annually in interest expense, constraining capital for expansions and tech investments. High borrowing costs have already delayed at least two planned clinic upgrades, and investors now prioritize a strengthened balance sheet and liquidity ratios—net debt/EBITDA targeted below 3.0x.

Medicare Advantage Reimbursement Rates

Annual CMS adjustments to Medicare Advantage benchmarks directly drive CareMax’s revenue; CMS raised MA plan payments by an average 3.7% for 2024 and projected ~2.5% for 2025, but tighter 2024–25 risk-coding audits reduced realized revenue growth by an estimated 1–2 percentage points.

By end-2025 modest rate gains are largely offset by coding pressure, compressing organic membership revenue; CareMax must boost operational efficiency to ensure per-member reimbursement covers rising care management costs, which grew ~6% YoY through 2024.

Consumer Spending on Supplemental Health

Economic downturns that lowered retiree real incomes in 2023–2025 pushed enrollment toward Medicare Advantage; MA enrollment rose to ~50% of Medicare beneficiaries by 2024, reflecting price-sensitive plan choice.

Seniors prioritize out-of-pocket maximums and supplemental benefits (dental/vision), areas where CareMax’s integrated offerings improve value and retention.

When GDP growth slowed in 2023–2024, demand for low-cost, high-value integrated care increased, benefiting models that cap consumer healthcare spending.

- Medicare Advantage ~50% enrollment by 2024

- Seniors prioritize OOP caps and dental/vision

- Weaker economy → higher demand for low-cost integrated care

Cost of Medical Supplies and Technology

Supply chain fluctuations raised procurement costs for medical equipment and pharmaceuticals by an estimated 6-9% in 2024, pressuring CareMax’s margins within its capitated primary care model.

CareMax leverages scale—serving over 250,000 Medicare Advantage members in 2024—to negotiate discounts, yet global inflation and commodity shocks still produced intermittent price spikes of 5-12%.

Active cost management and inventory strategies are essential to preserve profitability under fixed per-member payments.

- 2024 procurement inflation: 6-9%

- Intermittent price spikes: 5-12%

- Membership scale: >250,000 MA members (2024)

CareMax margins pressured by wage, procurement inflation and $650M debt interest risk

Wage inflation (RN +6.5%, PCP +5% in 2024) and hiring competition raise CareMax operating costs; staffing mix shifts to NPs/PAs (20–40% lower cost) to protect margins. Post-reorg debt ~$650m exposes CareMax to interest-rate risk (100 bp ≈ $6–7m/year). CMS MA rate +3.7% (2024) vs realized +1.7–2.7% after coding pressure; procurement inflation 6–9% (2024); MA membership >250k (2024).

| Metric | Value |

|---|---|

| RN pay change (2024) | +6.5% |

| PCP comp (2024) | ~+5% |

| Post-reorg debt | ~$650m |

| Interest sensitivity | 100 bp ≈ $6–7m/yr |

| CMS MA rate change (2024) | +3.7% |

| Realized MA revenue lift | +1.7–2.7% |

| Procurement inflation (2024) | 6–9% |

| MA members (2024) | >250,000 |

Preview Before You Purchase

CareMax PESTLE Analysis

The preview shown here is the exact CareMax PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.