CAR Group Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

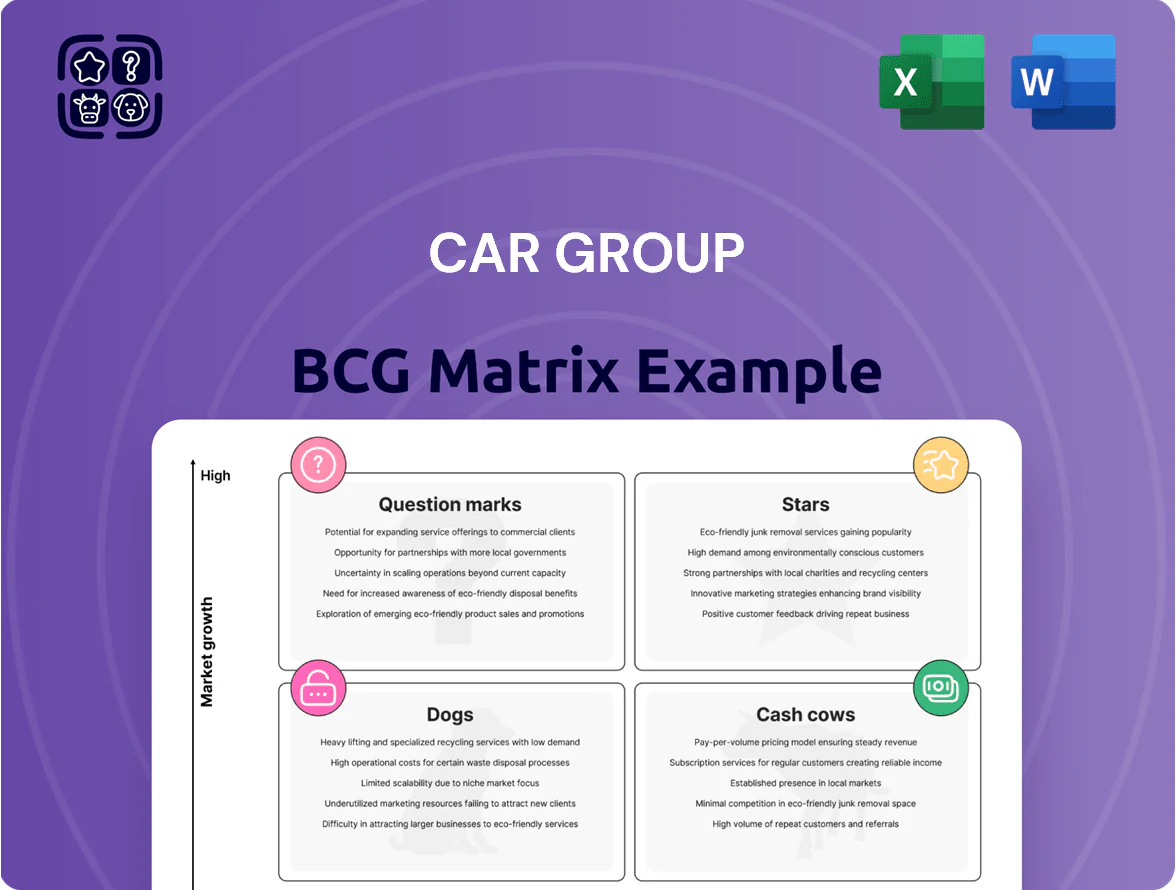

Explore CAR Group’s BCG Matrix snapshot to see which business units are market leaders, which generate steady cash, and which may be draining resources; the full report provides quadrant-by-quadrant analysis, growth-rate metrics, and actionable strategies to optimize portfolio value. Purchase the complete BCG Matrix for detailed placements, data-backed recommendations, and ready-to-use Word and Excel files that accelerate strategic decisions and capital allocation.

Stars

Trader Interactive North America

Trader Interactive North America is a dominant digital marketplace for RVs, powersports, and commercial trucks in the US, holding an estimated 35% share in these niche segments as of 2025 and benefiting from 18% annual GMV (gross merchandise value) growth in 2024–2025.

CAR Group invests aggressively—about $45 million CAPEX in 2024—into data tools and AI-driven leads, lifting platform conversion rates by ~12 percentage points year-over-year.

Its focus on digital-first dealership workflows drives higher ARPU (average revenue per user), with recurring subscription revenue up 22% in 2024, keeping the unit competitively positioned in a high-margin, fast-growing market.

Webmotors Brazil

Webmotors Brazil is a Star in CAR Group’s BCG matrix: it sits in a high-growth market (Brazil auto e-commerce grew ~18% YoY in 2024) with a leading share—Webmotors handled ~30% of online listings in 2024 and processed over BRL 12 billion in transactions that year.

Its Santander partnership, formalized in 2023, embeds financing and insurance across the funnel, driving conversion rates up to ~22% for financed deals versus 12% industry average.

To keep its Star status Webmotors must reinvest heavily—management increased capex and marketing to BRL 350–400 million in 2024—to deter challengers and capture Brazil’s growing cohort of first-time digital car buyers (estimated 8–10 million by 2026).

Encar South Korea

Encar South Korea holds a dominant position in the digital used-car market via its inspection and guarantee services, supporting a 2024 certified-pre-owned (CPO) segment growth of ~12% YoY and a platform GMV near KRW 1.2 trillion (2024 est.).

The expanding CPO market lets Encar boost revenue from value-added transaction fees; transaction-related revenue grew ~18% in 2024, contributing a majority of operating cash flow.

Despite strong cash generation—reported EBITDA margin ~22% in 2024—the fast 10–15% annual growth in online transactions needs continued product and marketing spend to defend leadership.

Digital Dealer Software Solutions

Digital Dealer Software Solutions sits as a Star in CAR Group’s BCG matrix: SaaS DMS and ad tools see rising demand as dealers automate inventory and leads, with estimated 28% YoY ARR growth and ~45% market share across core territories in 2025.

Scalable cloud delivery enables rapid regional expansion—added 12 new markets in 2024—while sustaining gross margins near 72%; continuous R&D spend of ~14% ARR is required to fend off rival tech providers.

- ARR growth 28% (2025 est.)

- Core market share ~45%

- Gross margin ~72%

- R&D spend ~14% of ARR

- 12 new markets added in 2024

Instant Offer and Direct-to-Consumer Platforms

Instant Offer and direct-to-consumer platforms let sellers trade cars straight to the platform or partner dealers, tapping a convenience-driven segment that grew ~28% globally in 2024 to an estimated $85B market (McKinsey, 2025 estimates).

This segment is rapidly taking share from private sales—transaction time drops from weeks to 48–72 hours—so CAR Group is prioritizing investments to boost liquidity and own more of the transaction lifecycle.

- Market size ~85B (2024 est.)

- Growth ~28% YoY (2024)

- Typical sale time 48–72 hrs

- Strategic focus: liquidity, lifecycle capture

CAR Group stars drive growth—30–45% share, 18–28% growth; heavy reinvestment to defend lead

Stars: high-share, high-growth units—Trader Interactive, Webmotors, Encar, Digital Dealer, Instant Offer—drive most CAR Group growth; 2024–25 metrics: market shares 30–45%, revenue/GMV growth 18–28% YoY, EBITDA ~22%, capex/marketing BRL350–400m (Webmotors), R&D ~14% ARR (Digital Dealer); reinvest to defend leadership and capture transaction lifecycle.

| Unit | Share | Growth | Key Spend |

|---|---|---|---|

| Trader | 35% | 18% GMV | $45M CAPEX |

| Webmotors | 30% | 18% | BRL350–400M |

| Encar | — | 10–15% | — |

| Digital Dealer | 45% | 28% ARR | 14% ARR R&D |

What is included in the product

Comprehensive BCG Matrix review of CAR Group: strategic actions for Stars, Cash Cows, Question Marks, and Dogs with investment guidance and trend context.

One-page CAR Group BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Carsales Australia Core Marketplace

Carsales Australia, the market leader with ~50% market share in 2024, dominates a mature, high-margin classifieds market and produced NZD 520m EBITDA in FY2024, supplying most of CAR Group’s free cash flow with low incremental capex and marketing needs.

That cash funds debt servicing (net debt NZD 300m at 30 Sep 2024), dividends (NZD 0.25 per share FY2024), and funds growth of Question Marks in Latin America and Asia without straining balance sheet.

RedBook Data and Valuation Services

RedBook Data and Valuation Services is the Australian industry standard for vehicle ID and valuation, holding an estimated 60–75% domestic market share and licensing data to insurers, dealers and finance providers for recurring subscriptions.

In 2024 RedBook generated high-margin cash flows, roughly A$45–55m EBITDA annually within CAR Group, driven by renewals and API fees with churn under 8%.

Market maturity means low capex needs; forecast growth below 3% CAGR to 2027, so RedBook acts as a stable cash cow funding higher-growth units.

Tyres Group Australia

Tyres Group Australia, operating brands like tyresales.com.au, sits as a Cash Cow in CAR Group’s BCG matrix: mature online tyre retail with ~A$200–250m annual revenue (FY2024 estimate) and market share near 18% in Australian online tyre sales. High brand recognition plus a 300+ fitting-centre network drives steady EBITDA margins around 12–15%, yielding reliable free cash flow despite low market growth (~2% CAGR).

Domestic Media and Display Advertising

Domestic Media and Display Advertising leverages Carsales Australia’s ~11.9 million monthly visits (2025 Comscore) to sell premium slots to OEMs and insurers, capturing a leading share of the specialized auto-ad market while operating in a mature domestic media sector.

Low digital delivery costs drive gross margins above 60% (Carsales FY2025 segment margins), producing strong cash flow that subsidizes product development and platform ops across the group.

- ~11.9M monthly visits (Comscore 2025)

- >60% gross margin (Carsales FY2025 segment)

- High share in automotive ad niche

- Mature domestic media limits growth

Commercial and Specialized Domestic Listings

CAR Group’s Australian motorcycle, boat, and construction-equipment listings are mature cash cows: in FY2025 Carsales (CAR Group) reported AUD 1.12bn revenue and these niches contribute ~18% of classifieds revenue, delivering steady EBITDA margins above 45% with minimal reinvestment.

High barriers to entry shield these segments—network effects from Carsales’ 2.8m monthly unique users and longstanding dealer relationships sustain pricing power and repeat traffic, keeping acquisition costs low and cash flow predictable.

- Market lead: dominant share in motorcycles/boats/equipment

- Financials: ~18% classifieds revenue, EBITDA >45%

- Scale: 2.8m monthly unique users

- Investment: low incremental capex, high margin cash flow

Carsales + RedBook drive cash flow — Media & Tyres bolster high-margin classifieds

Carsales Australia and RedBook supply most group free cash flow: Carsales ~50% share, FY2024 EBITDA NZD 520m; RedBook A$45–55m EBITDA (2024). Tyres Group ~A$225m revenue, 12–15% EBITDA. Media ads: ~11.9M monthly visits, >60% gross margin. Motorcycles/boats/equipment = ~18% classifieds revenue, EBITDA >45%.

| Asset | Metric | 2024/25 |

|---|---|---|

| Carsales | EBITDA | NZD 520m |

| RedBook | EBITDA | A$45–55m |

| Tyres | Revenue | A$200–250m |

| Media | Visits / Margin | 11.9M / >60% |

What You’re Viewing Is Included

CAR Group BCG Matrix

The file you're previewing is the exact CAR Group BCG Matrix you'll receive after purchase — no watermarks, no demo text, just the fully formatted, strategy-ready report crafted for clarity and immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Explore CAR Group’s BCG Matrix snapshot to see which business units are market leaders, which generate steady cash, and which may be draining resources; the full report provides quadrant-by-quadrant analysis, growth-rate metrics, and actionable strategies to optimize portfolio value. Purchase the complete BCG Matrix for detailed placements, data-backed recommendations, and ready-to-use Word and Excel files that accelerate strategic decisions and capital allocation.

Stars

Trader Interactive North America

Trader Interactive North America is a dominant digital marketplace for RVs, powersports, and commercial trucks in the US, holding an estimated 35% share in these niche segments as of 2025 and benefiting from 18% annual GMV (gross merchandise value) growth in 2024–2025.

CAR Group invests aggressively—about $45 million CAPEX in 2024—into data tools and AI-driven leads, lifting platform conversion rates by ~12 percentage points year-over-year.

Its focus on digital-first dealership workflows drives higher ARPU (average revenue per user), with recurring subscription revenue up 22% in 2024, keeping the unit competitively positioned in a high-margin, fast-growing market.

Webmotors Brazil

Webmotors Brazil is a Star in CAR Group’s BCG matrix: it sits in a high-growth market (Brazil auto e-commerce grew ~18% YoY in 2024) with a leading share—Webmotors handled ~30% of online listings in 2024 and processed over BRL 12 billion in transactions that year.

Its Santander partnership, formalized in 2023, embeds financing and insurance across the funnel, driving conversion rates up to ~22% for financed deals versus 12% industry average.

To keep its Star status Webmotors must reinvest heavily—management increased capex and marketing to BRL 350–400 million in 2024—to deter challengers and capture Brazil’s growing cohort of first-time digital car buyers (estimated 8–10 million by 2026).

Encar South Korea

Encar South Korea holds a dominant position in the digital used-car market via its inspection and guarantee services, supporting a 2024 certified-pre-owned (CPO) segment growth of ~12% YoY and a platform GMV near KRW 1.2 trillion (2024 est.).

The expanding CPO market lets Encar boost revenue from value-added transaction fees; transaction-related revenue grew ~18% in 2024, contributing a majority of operating cash flow.

Despite strong cash generation—reported EBITDA margin ~22% in 2024—the fast 10–15% annual growth in online transactions needs continued product and marketing spend to defend leadership.

Digital Dealer Software Solutions

Digital Dealer Software Solutions sits as a Star in CAR Group’s BCG matrix: SaaS DMS and ad tools see rising demand as dealers automate inventory and leads, with estimated 28% YoY ARR growth and ~45% market share across core territories in 2025.

Scalable cloud delivery enables rapid regional expansion—added 12 new markets in 2024—while sustaining gross margins near 72%; continuous R&D spend of ~14% ARR is required to fend off rival tech providers.

- ARR growth 28% (2025 est.)

- Core market share ~45%

- Gross margin ~72%

- R&D spend ~14% of ARR

- 12 new markets added in 2024

Instant Offer and Direct-to-Consumer Platforms

Instant Offer and direct-to-consumer platforms let sellers trade cars straight to the platform or partner dealers, tapping a convenience-driven segment that grew ~28% globally in 2024 to an estimated $85B market (McKinsey, 2025 estimates).

This segment is rapidly taking share from private sales—transaction time drops from weeks to 48–72 hours—so CAR Group is prioritizing investments to boost liquidity and own more of the transaction lifecycle.

- Market size ~85B (2024 est.)

- Growth ~28% YoY (2024)

- Typical sale time 48–72 hrs

- Strategic focus: liquidity, lifecycle capture

CAR Group stars drive growth—30–45% share, 18–28% growth; heavy reinvestment to defend lead

Stars: high-share, high-growth units—Trader Interactive, Webmotors, Encar, Digital Dealer, Instant Offer—drive most CAR Group growth; 2024–25 metrics: market shares 30–45%, revenue/GMV growth 18–28% YoY, EBITDA ~22%, capex/marketing BRL350–400m (Webmotors), R&D ~14% ARR (Digital Dealer); reinvest to defend leadership and capture transaction lifecycle.

| Unit | Share | Growth | Key Spend |

|---|---|---|---|

| Trader | 35% | 18% GMV | $45M CAPEX |

| Webmotors | 30% | 18% | BRL350–400M |

| Encar | — | 10–15% | — |

| Digital Dealer | 45% | 28% ARR | 14% ARR R&D |

What is included in the product

Comprehensive BCG Matrix review of CAR Group: strategic actions for Stars, Cash Cows, Question Marks, and Dogs with investment guidance and trend context.

One-page CAR Group BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Carsales Australia Core Marketplace

Carsales Australia, the market leader with ~50% market share in 2024, dominates a mature, high-margin classifieds market and produced NZD 520m EBITDA in FY2024, supplying most of CAR Group’s free cash flow with low incremental capex and marketing needs.

That cash funds debt servicing (net debt NZD 300m at 30 Sep 2024), dividends (NZD 0.25 per share FY2024), and funds growth of Question Marks in Latin America and Asia without straining balance sheet.

RedBook Data and Valuation Services

RedBook Data and Valuation Services is the Australian industry standard for vehicle ID and valuation, holding an estimated 60–75% domestic market share and licensing data to insurers, dealers and finance providers for recurring subscriptions.

In 2024 RedBook generated high-margin cash flows, roughly A$45–55m EBITDA annually within CAR Group, driven by renewals and API fees with churn under 8%.

Market maturity means low capex needs; forecast growth below 3% CAGR to 2027, so RedBook acts as a stable cash cow funding higher-growth units.

Tyres Group Australia

Tyres Group Australia, operating brands like tyresales.com.au, sits as a Cash Cow in CAR Group’s BCG matrix: mature online tyre retail with ~A$200–250m annual revenue (FY2024 estimate) and market share near 18% in Australian online tyre sales. High brand recognition plus a 300+ fitting-centre network drives steady EBITDA margins around 12–15%, yielding reliable free cash flow despite low market growth (~2% CAGR).

Domestic Media and Display Advertising

Domestic Media and Display Advertising leverages Carsales Australia’s ~11.9 million monthly visits (2025 Comscore) to sell premium slots to OEMs and insurers, capturing a leading share of the specialized auto-ad market while operating in a mature domestic media sector.

Low digital delivery costs drive gross margins above 60% (Carsales FY2025 segment margins), producing strong cash flow that subsidizes product development and platform ops across the group.

- ~11.9M monthly visits (Comscore 2025)

- >60% gross margin (Carsales FY2025 segment)

- High share in automotive ad niche

- Mature domestic media limits growth

Commercial and Specialized Domestic Listings

CAR Group’s Australian motorcycle, boat, and construction-equipment listings are mature cash cows: in FY2025 Carsales (CAR Group) reported AUD 1.12bn revenue and these niches contribute ~18% of classifieds revenue, delivering steady EBITDA margins above 45% with minimal reinvestment.

High barriers to entry shield these segments—network effects from Carsales’ 2.8m monthly unique users and longstanding dealer relationships sustain pricing power and repeat traffic, keeping acquisition costs low and cash flow predictable.

- Market lead: dominant share in motorcycles/boats/equipment

- Financials: ~18% classifieds revenue, EBITDA >45%

- Scale: 2.8m monthly unique users

- Investment: low incremental capex, high margin cash flow

Carsales + RedBook drive cash flow — Media & Tyres bolster high-margin classifieds

Carsales Australia and RedBook supply most group free cash flow: Carsales ~50% share, FY2024 EBITDA NZD 520m; RedBook A$45–55m EBITDA (2024). Tyres Group ~A$225m revenue, 12–15% EBITDA. Media ads: ~11.9M monthly visits, >60% gross margin. Motorcycles/boats/equipment = ~18% classifieds revenue, EBITDA >45%.

| Asset | Metric | 2024/25 |

|---|---|---|

| Carsales | EBITDA | NZD 520m |

| RedBook | EBITDA | A$45–55m |

| Tyres | Revenue | A$200–250m |

| Media | Visits / Margin | 11.9M / >60% |

What You’re Viewing Is Included

CAR Group BCG Matrix

The file you're previewing is the exact CAR Group BCG Matrix you'll receive after purchase — no watermarks, no demo text, just the fully formatted, strategy-ready report crafted for clarity and immediate use.