Carrefour Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

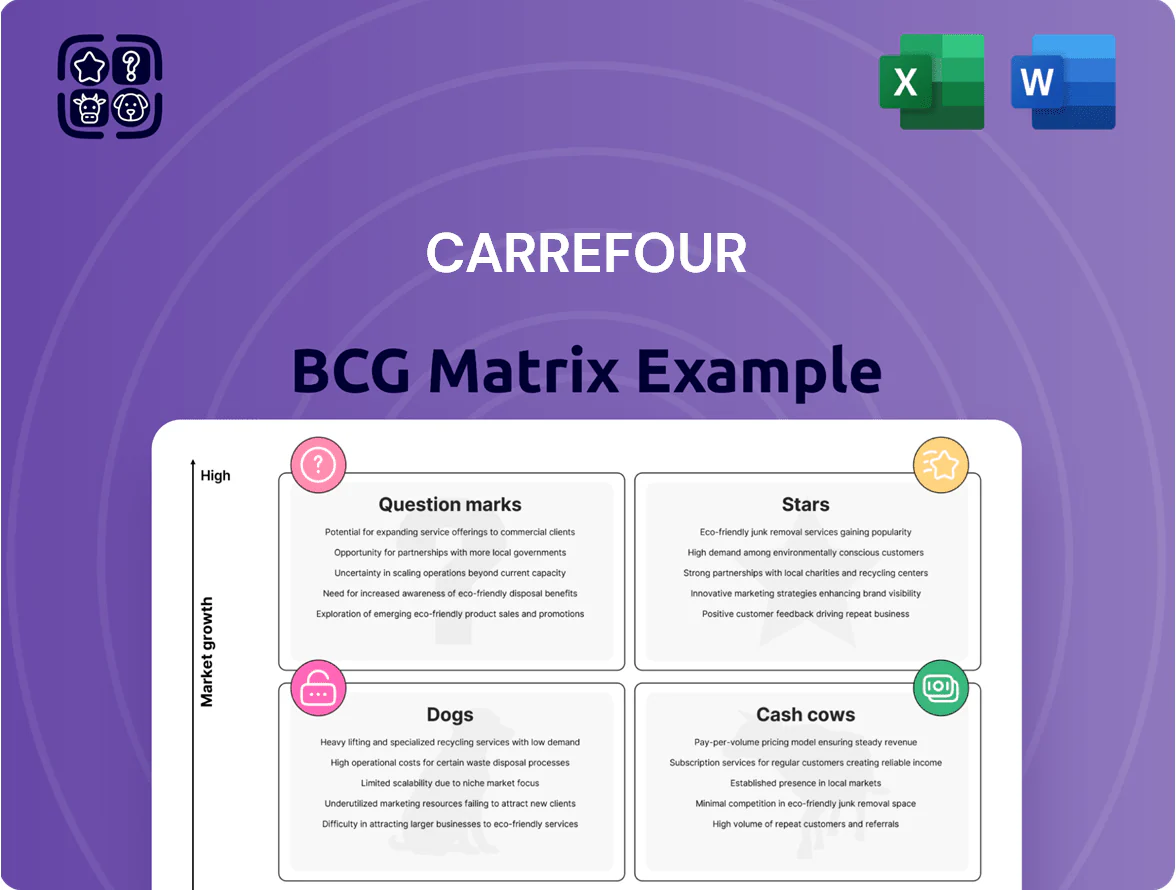

Carrefour’s BCG Matrix snapshot reveals a mix of stable Cash Cows in mature grocery segments, high-potential Stars tied to e‑commerce and fresh‑food innovations, and a few Question Marks in emerging non‑food categories that need investment decisions; a small set of Dogs highlights where divestment could free up capital. This concise view points to strategic priorities—optimizing store productivity, scaling omnichannel strengths, and reallocating resources from underperforming lines. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

E-commerce and Digital Retail

By end-2025 Carrefour's e-commerce and digital retail are market leaders in online grocery, with group online sales rising to about €12.4bn (≈16% of total sales) after high double-digit annual growth driven by omnichannel fulfillment and Carrefour Links data platform.

Heavy capital spending—≈€1.1bn in 2024–2025 on tech and logistics—keeps margins compressed but is essential to capture hybrid shopping; online GMV and click-and-collect volumes grew >40% year-on-year.

Carrefour Brazil Operations

Carrefour Brazil is a Star: post-2023 Grupo BIG integration and Atacadão expansion, Brazil drove group growth—Q4 2024 sales ~€13.5bn (approx R$74bn), with market share ~22% in grocery retail and wholesale combined.

High middle-class growth and value-focused demand keep like-for-like sales up low double digits in 2024, but ongoing capex (~€400–500m annually in 2024–25) is needed to counter local rivals and >5% inflation.

Private Label - Carrefour Sensation and Bio

Carrefour’s Private Label - Carrefour Sensation and Bio are Stars: own-brand sales rose 18% year-on-year in 2025, now forming ~22% of basket value versus 16% for national brands, driven by consumers trading down yet seeking quality.

Carrefour invested €240m in 2024–25 for product R&D and sustainable packaging; Sensation and Bio SKUs grew at 25% CAGR, boosting margins by ~130 bps and strengthening long-term loyalty.

Retail Media Services

Carrefour Links is a high-growth, high-margin retail media player using first-party data; in 2024 Carrefour reported Links ad revenues of about €350m, up ~45% year-on-year, capturing a top-3 share of European retail media spend.

The unit needs continued tech investment—estimated €50–70m capex through 2026—but could scale to €1bn+ EBITDA run-rate if brand budgets shift to point-of-sale digital channels.

- €350m 2024 ad revenue, +45% YoY

- Top-3 European retail media share

- €50–70m tech capex through 2026

- Potential >€1bn EBITDA at scale

Convenience Store Expansion

Carrefour City and Express are Stars: urban proximity formats showing double-digit growth, with city-store sales up ~12% in 2024 and market share gains in Paris, Madrid, and Milan—now ~18% of Carrefour’s European store sales mix.

Carrefour committed ~€600m in 2024–25 to acquire premium urban sites and invest in small-format supply chains, cutting last-mile costs ~8% and boosting same-store daily transactions.

- Sales growth ~12% (2024)

- ~18% share of Carrefour European store sales

- €600m capital allocation (2024–25)

- Last-mile cost reduction ~8%

Carrefour's growth engines—Online €12.4bn, Brazil €13.5bn, Links €350m, Private Label

Stars: Carrefour’s online, Brazil, Private Label, Links, and City formats drive high growth and require heavy capex; online sales ≈€12.4bn (16% of group) in 2025, Brazil sales ≈€13.5bn (22% market share), Links €350m ad rev (+45% YoY), Private Label 22% basket, City formats 18% of store sales.

| Unit | 2024–25 | Key metric |

|---|---|---|

| Online | €12.4bn | 16% group sales |

| Brazil | €13.5bn | ~22% market share |

| Links | €350m | +45% YoY |

| Private Label | 22% basket | +18% YoY |

| City | 18% mix | +12% sales growth |

What is included in the product

Comprehensive BCG Matrix of Carrefour: identifies Stars, Cash Cows, Question Marks, and Dogs with strategic actions, risks, and investment priorities.

One-page Carrefour BCG Matrix placing each business unit in a quadrant for clear strategic prioritization

Cash Cows

French Hypermarkets

The French hypermarket chain remains Carrefour’s cash cow: in 2024 France sales were €22.4bn (about 38% of group sales) in a low-growth market (~1% annual retail growth), producing steady operating cash flow that funded 2024‑25 digital and emerging‑market investments of ~€900m.

Atacadão Cash and Carry

Atacadão Cash and Carry, Carrefour’s high-share Brazilian wholesale chain recently trialed in Europe, delivers strong cash returns: 2024 EBITDA margin ~7.5% on R$48.2bn net sales in Brazil, driven by low overhead and high volume in a mature wholesale segment.

Its steady free cash flow funded Carrefour’s 2024 net interest payments and helped sustain a 2024 dividend payout of €0.60 per share, easing corporate leverage (net debt/EBITDA ~2.1x at year-end 2024).

Financial Services and Carrefour Banque

Carrefour Banque’s consumer credit and insurance sit in a mature French market, serving ~5.2 million clients in 2024 and generating ~€420m EBITDA, showing stable demand and high retention via loyalty ties.

Deep loyalty-program integration drives recurring fee and interest income—~€1.1bn in interest/fees in 2024—requiring little capex, so cash funds growth units.

Spanish Market Operations

Spain is a mature, low-growth market where Carrefour ranks second with ~21% grocery market share (2024 Kantar) and strong brand equity; revenues there contributed about €6.4bn in 2024, making it a reliable cash cow for the group.

Modest sector growth (~1–2% annual same-store sales, 2023–24) lets Carrefour prioritize cost cuts, margin improvement, and free cash flow extraction rather than expansion.

These steady Spanish assets generated stable EBITDA margins near 6–7% in 2024, buffering Carrefour against volatility in higher-growth emerging markets.

- ~21% market share (Kantar 2024)

- €6.4bn revenue contribution (2024)

- 1–2% annual SSS growth (2023–24)

- EBITDA margin ~6–7% (2024)

Logistics and Supply Chain Infrastructure

Carrefour’s Europe-wide network of ~255 distribution centers and 18 automated warehouses (2025) is the backbone of operational efficiency, cutting logistics cost per unit and enabling same-day replenishment across 30+ countries.

Having reached scale, these assets need mainly maintenance capex (≈€350–450m annual) while delivering a 10–15% cost advantage vs regional rivals and supporting high-volume turnover that sustains group gross margin.

- ~255 DCs, 18 automated warehouses (2025)

- Maintenance capex ≈€350–450m/year

- 10–15% logistics cost advantage

- Supports high-volume turnover and stable gross margin

Carrefour’s 2024 cash cows fund €0.60 DPS, €900m growth while net debt ~2.1x

France, Spain, Atacadão, Carrefour Banque and European logistics are Carrefour cash cows in 2024–25, generating stable FCF, covering net interest and a €0.60 DPS while funding €900m digital/emerging investments; key 2024 metrics: France sales €22.4bn, Spain €6.4bn (21% share), Atacadão R$48.2bn (EBITDA margin ~7.5%), Banque EBITDA ~€420m, net debt/EBITDA ~2.1x.

| Asset | 2024 |

|---|---|

| France sales | €22.4bn |

| Spain sales | €6.4bn |

| Atacadão | R$48.2bn, EBITDA ~7.5% |

| Banque EBITDA | €420m |

| Net debt/EBITDA | ~2.1x |

Delivered as Shown

Carrefour BCG Matrix

The file you're previewing on this page is the final Carrefour BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, market-informed strategic report ready for presentation and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Carrefour’s BCG Matrix snapshot reveals a mix of stable Cash Cows in mature grocery segments, high-potential Stars tied to e‑commerce and fresh‑food innovations, and a few Question Marks in emerging non‑food categories that need investment decisions; a small set of Dogs highlights where divestment could free up capital. This concise view points to strategic priorities—optimizing store productivity, scaling omnichannel strengths, and reallocating resources from underperforming lines. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

E-commerce and Digital Retail

By end-2025 Carrefour's e-commerce and digital retail are market leaders in online grocery, with group online sales rising to about €12.4bn (≈16% of total sales) after high double-digit annual growth driven by omnichannel fulfillment and Carrefour Links data platform.

Heavy capital spending—≈€1.1bn in 2024–2025 on tech and logistics—keeps margins compressed but is essential to capture hybrid shopping; online GMV and click-and-collect volumes grew >40% year-on-year.

Carrefour Brazil Operations

Carrefour Brazil is a Star: post-2023 Grupo BIG integration and Atacadão expansion, Brazil drove group growth—Q4 2024 sales ~€13.5bn (approx R$74bn), with market share ~22% in grocery retail and wholesale combined.

High middle-class growth and value-focused demand keep like-for-like sales up low double digits in 2024, but ongoing capex (~€400–500m annually in 2024–25) is needed to counter local rivals and >5% inflation.

Private Label - Carrefour Sensation and Bio

Carrefour’s Private Label - Carrefour Sensation and Bio are Stars: own-brand sales rose 18% year-on-year in 2025, now forming ~22% of basket value versus 16% for national brands, driven by consumers trading down yet seeking quality.

Carrefour invested €240m in 2024–25 for product R&D and sustainable packaging; Sensation and Bio SKUs grew at 25% CAGR, boosting margins by ~130 bps and strengthening long-term loyalty.

Retail Media Services

Carrefour Links is a high-growth, high-margin retail media player using first-party data; in 2024 Carrefour reported Links ad revenues of about €350m, up ~45% year-on-year, capturing a top-3 share of European retail media spend.

The unit needs continued tech investment—estimated €50–70m capex through 2026—but could scale to €1bn+ EBITDA run-rate if brand budgets shift to point-of-sale digital channels.

- €350m 2024 ad revenue, +45% YoY

- Top-3 European retail media share

- €50–70m tech capex through 2026

- Potential >€1bn EBITDA at scale

Convenience Store Expansion

Carrefour City and Express are Stars: urban proximity formats showing double-digit growth, with city-store sales up ~12% in 2024 and market share gains in Paris, Madrid, and Milan—now ~18% of Carrefour’s European store sales mix.

Carrefour committed ~€600m in 2024–25 to acquire premium urban sites and invest in small-format supply chains, cutting last-mile costs ~8% and boosting same-store daily transactions.

- Sales growth ~12% (2024)

- ~18% share of Carrefour European store sales

- €600m capital allocation (2024–25)

- Last-mile cost reduction ~8%

Carrefour's growth engines—Online €12.4bn, Brazil €13.5bn, Links €350m, Private Label

Stars: Carrefour’s online, Brazil, Private Label, Links, and City formats drive high growth and require heavy capex; online sales ≈€12.4bn (16% of group) in 2025, Brazil sales ≈€13.5bn (22% market share), Links €350m ad rev (+45% YoY), Private Label 22% basket, City formats 18% of store sales.

| Unit | 2024–25 | Key metric |

|---|---|---|

| Online | €12.4bn | 16% group sales |

| Brazil | €13.5bn | ~22% market share |

| Links | €350m | +45% YoY |

| Private Label | 22% basket | +18% YoY |

| City | 18% mix | +12% sales growth |

What is included in the product

Comprehensive BCG Matrix of Carrefour: identifies Stars, Cash Cows, Question Marks, and Dogs with strategic actions, risks, and investment priorities.

One-page Carrefour BCG Matrix placing each business unit in a quadrant for clear strategic prioritization

Cash Cows

French Hypermarkets

The French hypermarket chain remains Carrefour’s cash cow: in 2024 France sales were €22.4bn (about 38% of group sales) in a low-growth market (~1% annual retail growth), producing steady operating cash flow that funded 2024‑25 digital and emerging‑market investments of ~€900m.

Atacadão Cash and Carry

Atacadão Cash and Carry, Carrefour’s high-share Brazilian wholesale chain recently trialed in Europe, delivers strong cash returns: 2024 EBITDA margin ~7.5% on R$48.2bn net sales in Brazil, driven by low overhead and high volume in a mature wholesale segment.

Its steady free cash flow funded Carrefour’s 2024 net interest payments and helped sustain a 2024 dividend payout of €0.60 per share, easing corporate leverage (net debt/EBITDA ~2.1x at year-end 2024).

Financial Services and Carrefour Banque

Carrefour Banque’s consumer credit and insurance sit in a mature French market, serving ~5.2 million clients in 2024 and generating ~€420m EBITDA, showing stable demand and high retention via loyalty ties.

Deep loyalty-program integration drives recurring fee and interest income—~€1.1bn in interest/fees in 2024—requiring little capex, so cash funds growth units.

Spanish Market Operations

Spain is a mature, low-growth market where Carrefour ranks second with ~21% grocery market share (2024 Kantar) and strong brand equity; revenues there contributed about €6.4bn in 2024, making it a reliable cash cow for the group.

Modest sector growth (~1–2% annual same-store sales, 2023–24) lets Carrefour prioritize cost cuts, margin improvement, and free cash flow extraction rather than expansion.

These steady Spanish assets generated stable EBITDA margins near 6–7% in 2024, buffering Carrefour against volatility in higher-growth emerging markets.

- ~21% market share (Kantar 2024)

- €6.4bn revenue contribution (2024)

- 1–2% annual SSS growth (2023–24)

- EBITDA margin ~6–7% (2024)

Logistics and Supply Chain Infrastructure

Carrefour’s Europe-wide network of ~255 distribution centers and 18 automated warehouses (2025) is the backbone of operational efficiency, cutting logistics cost per unit and enabling same-day replenishment across 30+ countries.

Having reached scale, these assets need mainly maintenance capex (≈€350–450m annual) while delivering a 10–15% cost advantage vs regional rivals and supporting high-volume turnover that sustains group gross margin.

- ~255 DCs, 18 automated warehouses (2025)

- Maintenance capex ≈€350–450m/year

- 10–15% logistics cost advantage

- Supports high-volume turnover and stable gross margin

Carrefour’s 2024 cash cows fund €0.60 DPS, €900m growth while net debt ~2.1x

France, Spain, Atacadão, Carrefour Banque and European logistics are Carrefour cash cows in 2024–25, generating stable FCF, covering net interest and a €0.60 DPS while funding €900m digital/emerging investments; key 2024 metrics: France sales €22.4bn, Spain €6.4bn (21% share), Atacadão R$48.2bn (EBITDA margin ~7.5%), Banque EBITDA ~€420m, net debt/EBITDA ~2.1x.

| Asset | 2024 |

|---|---|

| France sales | €22.4bn |

| Spain sales | €6.4bn |

| Atacadão | R$48.2bn, EBITDA ~7.5% |

| Banque EBITDA | €420m |

| Net debt/EBITDA | ~2.1x |

Delivered as Shown

Carrefour BCG Matrix

The file you're previewing on this page is the final Carrefour BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, market-informed strategic report ready for presentation and decision-making.