Carriage Services Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

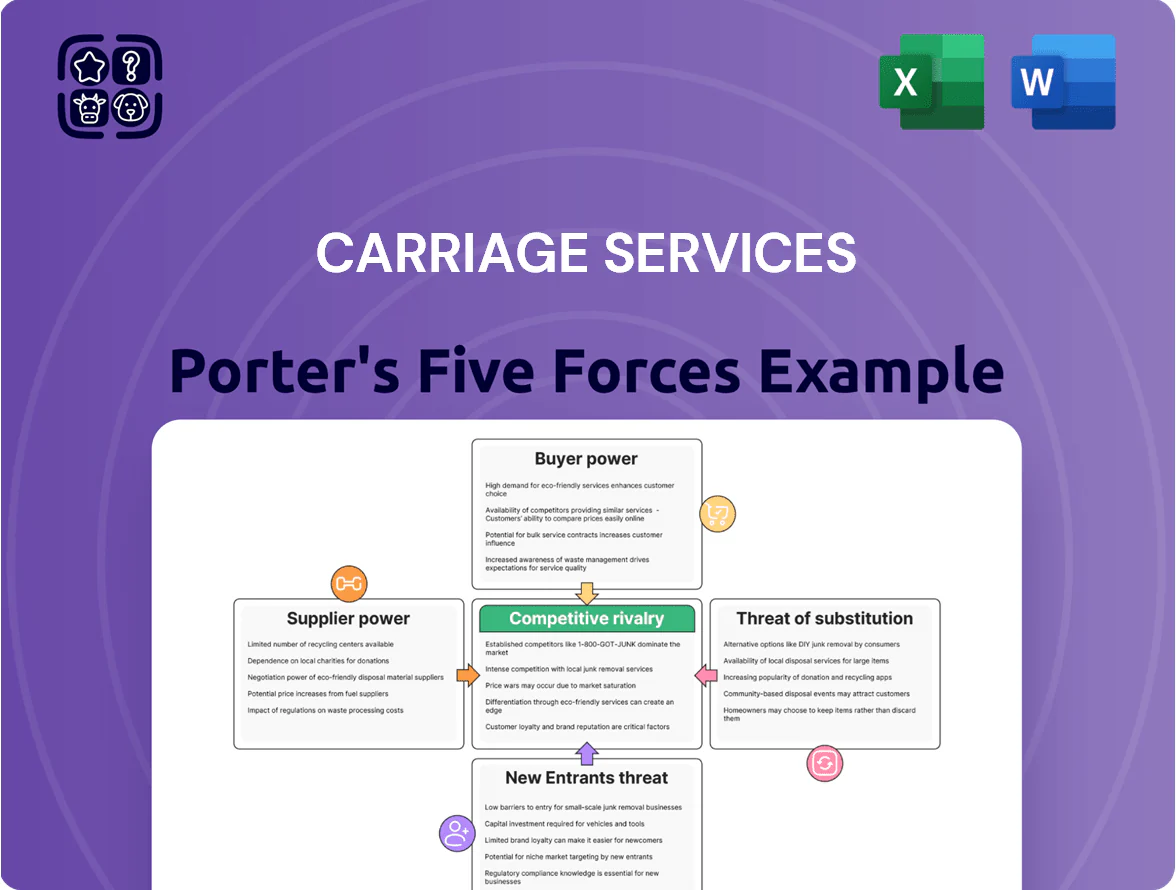

Carriage Services faces moderate buyer power and regional competition, with margin pressure from pricing sensitivity and rising regulatory costs—yet its strong local brands and acquisition-driven growth offer defensive advantages.

Suppliers Bargaining Power

Concentration of Casket and Memorialization Vendors

The casket and burial vault market is highly concentrated: three manufacturers (including Matthews International and Aurora Casket) held roughly 70% of US casket shipments in 2024, giving suppliers strong pricing power and squeezing margins for Carriage Services (NYSE: CSV) unless it secures long‑term contracts or scale discounts; with only a few national high‑volume suppliers able to meet demand, Carriage faces limited ability to push wholesale prices down without risking product quality or service consistency.

Shortage of Licensed Funeral Professionals

The labor supply for licensed funeral directors and embalmers tightened through 2025, raising their bargaining power as the average practitioner age hit about 55 and graduation rates fell ~18% since 2015 (National Funeral Directors Association, 2024).

Carriage Services (NYSE: CSV) must boost wages and benefits; payroll rose 6.2% YoY in 2024, and further increases would compress 2025 operating margins if staffing costs outpace revenue.

Scarcity of Zoned Cemetery Land

Suppliers of undeveloped land suitable for cemetery use hold substantial power because strict local zoning and environmental rules limit available parcels; in 2024 over 60% of U.S. municipalities reported zoning restrictions affecting cemetery expansions, raising bar to entry. Acquiring new land is more costly—median per-acre prices in key urban markets rose 18% from 2020–2024—making growth expensive for Carriage Services. Scarcity forces the company to pay premiums or squeeze more revenue from existing 200+ properties by enhancing plot yield and services.

Fluctuating Energy and Fuel Costs

- Natural gas volatility: +40% (2022–23)

- Cremation mix ~55% of services (2024)

- Fuel exposure: funeral fleet diesel costs rose ~15% in 2022

- Pass-through limited; shocks hit short-term EBITDA

Increasing Reliance on Specialized Technology Vendors

As funeral services digitize, Carriage Services increasingly depends on niche vendors for funeral management systems and digital memorialization; in 2025 Carriage reported 18% of revenue linked to digital services supporting operations and marketing.

These vendors wield moderate bargaining power because switching costs are high: data migration, API rework, and staff retraining can cost 0.5–1.5% of annual revenue for a mid-sized operator.

The shift to virtual arrangements—video services and online memorial platforms—made tech partnerships essential for competitive differentiation by 2026, raising vendor importance for customer experience and compliance.

- 2025: 18% revenue tied to digital services

- Switch cost est. 0.5–1.5% annual revenue

- Vendors = moderate power due to integration/training

Concentrated casket supply, aging labor, zoning crunch and cremation cost risk

Suppliers exert meaningful power: three casket makers held ~70% of US shipments in 2024, labor pool age ~55 with graduation rates down ~18% since 2015, payroll +6.2% YoY in 2024, cemetery land constrained in 60%+ municipalities, and cremation energy exposure (~55% mix) amplifies input-cost risk.

| Metric | Value |

|---|---|

| Casket concentration (2024) | ~70% |

| Funeral labor avg age | ~55 |

| Graduation decline since 2015 | ~18% |

| Payroll change (2024) | +6.2% YoY |

| Cemetery zoning constraints (2024) | >60% municipalities |

| Cremation mix (2024) | ~55% |

What is included in the product

Examines competitive rivalry, supplier and buyer power, threat of substitutes and new entrants specifically for Carriage Services, highlighting key pressures on pricing, margins, and growth prospects within the funeral services industry.

Concise Porter's Five Forces assessment for Carriage Services—ideal for quick boardroom decisions and easy insertion into pitch decks.

Customers Bargaining Power

Enhanced Price Transparency and Regulatory Oversight

Updated federal and state rules now force clearer online price disclosures for funeral services, letting families compare costs—median U.S. funeral spending was $7,848 in 2023, so price visibility matters.

This reduces info asymmetry that favored providers; a 2024 survey found 58% of consumers shop multiple funeral homes before purchase.

For Carriage Services (2024 revenue $914M), this means buyers are more informed, increasing negotiation and competitive-quote pressure.

Widespread Adoption of Lower Cost Cremation

The US cremation rate rose to 60.6% in 2022 and is projected near 66% by 2025, boosting buyer leverage as cremation undercuts traditional burial costs by thousands of dollars; Carriage Services faces pricing pressure as families choose lower-cost providers.

Wider price tiers force Carriage to offer varied, cheaper packages while preserving margins; in 2024 Carriage’s average revenue per contract was about $3,400, so the firm must grow add-on memorialization services to sustain that figure.

Growth of the Pre-need Market

Customers in the pre-need market can shop and lock prices, increasing price sensitivity; industry data shows U.S. pre-need sales grew about 4% in 2024 to roughly $4.8 billion, so buyers push aggressively for long-term value. This bargaining power forces Carriage Services to offer competitive pricing and bundled options, lowering margins at sale. Effective management of pre-need funds—Carriage reported $240.6 million in trust assets at year-end 2024—is vital to keep future obligations profitable and limit cash-flow strain.

Availability of Online Information and Reviews

Digital platforms and social media let customers vet funeral homes fast; 89% of consumers read local business reviews online and 72% trust reviews as much as personal recommendations (BrightLocal 2024), so Carriage Services faces amplified reputational risk.

A single negative review can reach thousands locally via Facebook and Google Maps, cutting referral leads and hurting revenue per arrangement—median 2023 revenue per funeral home ~ $1.1M—so Brand equity is fragile.

Carriage Services must double down on high-touch, personalized care and prompt online response to reviews; firms that reply to 85%+ reviews see 5–10% higher new-customer conversion within 12 months.

- 89% read local reviews (BrightLocal 2024)

- 72% trust online reviews like personal recs

- Neg reviews can cut referrals and revenue

- Replying to 85%+ reviews lifts conversions 5–10%

Rationalization of Post-Pandemic Funeral Spending

Post-pandemic economic stress and changing deathcare norms pushed 27% of U.S. families toward simpler services by 2024, reducing demand for high-margin add-ons like premium caskets and luxury florals and compressing average revenue per arrangement.

Carriage Services must prove premium value—e.g., justify 10–20% price premiums—via bundled services, digital memorials, and transparent pricing to retain upsell conversion rates that fell an estimated 5–8% post-2020.

- 27% of families chose simplified services (2024)

- Premium add-on uptake down ~5–8% since 2020

- Premium pricing opportunity ~10–20% if value shown

Carriage Services pivots to cheaper bundles and add‑ons as consumers shop and cremation rises

Customers have rising price power: transparent pricing (median funeral $7,848 in 2023), higher cremation (60.6% in 2022, ~66% by 2025) and 58% comparison shopping (2024) push Carriage Services (2024 revenue $914M) to offer cheaper bundles and grow add-ons to protect avg revenue/contract ~$3,400 while managing $240.6M pre-need trusts.

| Metric | Value |

|---|---|

| 2024 Revenue | $914M |

| Avg rev/contract | $3,400 |

| Cremation rate (2022/2025) | 60.6% / ~66% |

| Pre-need trust assets (2024) | $240.6M |

| Consumers shopping | 58% (2024) |

Preview Before You Purchase

Carriage Services Porter's Five Forces Analysis

This preview shows the exact Carriage Services Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders; it is the fully formatted, professionally written document ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Carriage Services faces moderate buyer power and regional competition, with margin pressure from pricing sensitivity and rising regulatory costs—yet its strong local brands and acquisition-driven growth offer defensive advantages.

Suppliers Bargaining Power

Concentration of Casket and Memorialization Vendors

The casket and burial vault market is highly concentrated: three manufacturers (including Matthews International and Aurora Casket) held roughly 70% of US casket shipments in 2024, giving suppliers strong pricing power and squeezing margins for Carriage Services (NYSE: CSV) unless it secures long‑term contracts or scale discounts; with only a few national high‑volume suppliers able to meet demand, Carriage faces limited ability to push wholesale prices down without risking product quality or service consistency.

Shortage of Licensed Funeral Professionals

The labor supply for licensed funeral directors and embalmers tightened through 2025, raising their bargaining power as the average practitioner age hit about 55 and graduation rates fell ~18% since 2015 (National Funeral Directors Association, 2024).

Carriage Services (NYSE: CSV) must boost wages and benefits; payroll rose 6.2% YoY in 2024, and further increases would compress 2025 operating margins if staffing costs outpace revenue.

Scarcity of Zoned Cemetery Land

Suppliers of undeveloped land suitable for cemetery use hold substantial power because strict local zoning and environmental rules limit available parcels; in 2024 over 60% of U.S. municipalities reported zoning restrictions affecting cemetery expansions, raising bar to entry. Acquiring new land is more costly—median per-acre prices in key urban markets rose 18% from 2020–2024—making growth expensive for Carriage Services. Scarcity forces the company to pay premiums or squeeze more revenue from existing 200+ properties by enhancing plot yield and services.

Fluctuating Energy and Fuel Costs

- Natural gas volatility: +40% (2022–23)

- Cremation mix ~55% of services (2024)

- Fuel exposure: funeral fleet diesel costs rose ~15% in 2022

- Pass-through limited; shocks hit short-term EBITDA

Increasing Reliance on Specialized Technology Vendors

As funeral services digitize, Carriage Services increasingly depends on niche vendors for funeral management systems and digital memorialization; in 2025 Carriage reported 18% of revenue linked to digital services supporting operations and marketing.

These vendors wield moderate bargaining power because switching costs are high: data migration, API rework, and staff retraining can cost 0.5–1.5% of annual revenue for a mid-sized operator.

The shift to virtual arrangements—video services and online memorial platforms—made tech partnerships essential for competitive differentiation by 2026, raising vendor importance for customer experience and compliance.

- 2025: 18% revenue tied to digital services

- Switch cost est. 0.5–1.5% annual revenue

- Vendors = moderate power due to integration/training

Concentrated casket supply, aging labor, zoning crunch and cremation cost risk

Suppliers exert meaningful power: three casket makers held ~70% of US shipments in 2024, labor pool age ~55 with graduation rates down ~18% since 2015, payroll +6.2% YoY in 2024, cemetery land constrained in 60%+ municipalities, and cremation energy exposure (~55% mix) amplifies input-cost risk.

| Metric | Value |

|---|---|

| Casket concentration (2024) | ~70% |

| Funeral labor avg age | ~55 |

| Graduation decline since 2015 | ~18% |

| Payroll change (2024) | +6.2% YoY |

| Cemetery zoning constraints (2024) | >60% municipalities |

| Cremation mix (2024) | ~55% |

What is included in the product

Examines competitive rivalry, supplier and buyer power, threat of substitutes and new entrants specifically for Carriage Services, highlighting key pressures on pricing, margins, and growth prospects within the funeral services industry.

Concise Porter's Five Forces assessment for Carriage Services—ideal for quick boardroom decisions and easy insertion into pitch decks.

Customers Bargaining Power

Enhanced Price Transparency and Regulatory Oversight

Updated federal and state rules now force clearer online price disclosures for funeral services, letting families compare costs—median U.S. funeral spending was $7,848 in 2023, so price visibility matters.

This reduces info asymmetry that favored providers; a 2024 survey found 58% of consumers shop multiple funeral homes before purchase.

For Carriage Services (2024 revenue $914M), this means buyers are more informed, increasing negotiation and competitive-quote pressure.

Widespread Adoption of Lower Cost Cremation

The US cremation rate rose to 60.6% in 2022 and is projected near 66% by 2025, boosting buyer leverage as cremation undercuts traditional burial costs by thousands of dollars; Carriage Services faces pricing pressure as families choose lower-cost providers.

Wider price tiers force Carriage to offer varied, cheaper packages while preserving margins; in 2024 Carriage’s average revenue per contract was about $3,400, so the firm must grow add-on memorialization services to sustain that figure.

Growth of the Pre-need Market

Customers in the pre-need market can shop and lock prices, increasing price sensitivity; industry data shows U.S. pre-need sales grew about 4% in 2024 to roughly $4.8 billion, so buyers push aggressively for long-term value. This bargaining power forces Carriage Services to offer competitive pricing and bundled options, lowering margins at sale. Effective management of pre-need funds—Carriage reported $240.6 million in trust assets at year-end 2024—is vital to keep future obligations profitable and limit cash-flow strain.

Availability of Online Information and Reviews

Digital platforms and social media let customers vet funeral homes fast; 89% of consumers read local business reviews online and 72% trust reviews as much as personal recommendations (BrightLocal 2024), so Carriage Services faces amplified reputational risk.

A single negative review can reach thousands locally via Facebook and Google Maps, cutting referral leads and hurting revenue per arrangement—median 2023 revenue per funeral home ~ $1.1M—so Brand equity is fragile.

Carriage Services must double down on high-touch, personalized care and prompt online response to reviews; firms that reply to 85%+ reviews see 5–10% higher new-customer conversion within 12 months.

- 89% read local reviews (BrightLocal 2024)

- 72% trust online reviews like personal recs

- Neg reviews can cut referrals and revenue

- Replying to 85%+ reviews lifts conversions 5–10%

Rationalization of Post-Pandemic Funeral Spending

Post-pandemic economic stress and changing deathcare norms pushed 27% of U.S. families toward simpler services by 2024, reducing demand for high-margin add-ons like premium caskets and luxury florals and compressing average revenue per arrangement.

Carriage Services must prove premium value—e.g., justify 10–20% price premiums—via bundled services, digital memorials, and transparent pricing to retain upsell conversion rates that fell an estimated 5–8% post-2020.

- 27% of families chose simplified services (2024)

- Premium add-on uptake down ~5–8% since 2020

- Premium pricing opportunity ~10–20% if value shown

Carriage Services pivots to cheaper bundles and add‑ons as consumers shop and cremation rises

Customers have rising price power: transparent pricing (median funeral $7,848 in 2023), higher cremation (60.6% in 2022, ~66% by 2025) and 58% comparison shopping (2024) push Carriage Services (2024 revenue $914M) to offer cheaper bundles and grow add-ons to protect avg revenue/contract ~$3,400 while managing $240.6M pre-need trusts.

| Metric | Value |

|---|---|

| 2024 Revenue | $914M |

| Avg rev/contract | $3,400 |

| Cremation rate (2022/2025) | 60.6% / ~66% |

| Pre-need trust assets (2024) | $240.6M |

| Consumers shopping | 58% (2024) |

Preview Before You Purchase

Carriage Services Porter's Five Forces Analysis

This preview shows the exact Carriage Services Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders; it is the fully formatted, professionally written document ready for download and use the moment you buy.