Carvana Boston Consulting Group Matrix

See the Bigger Picture

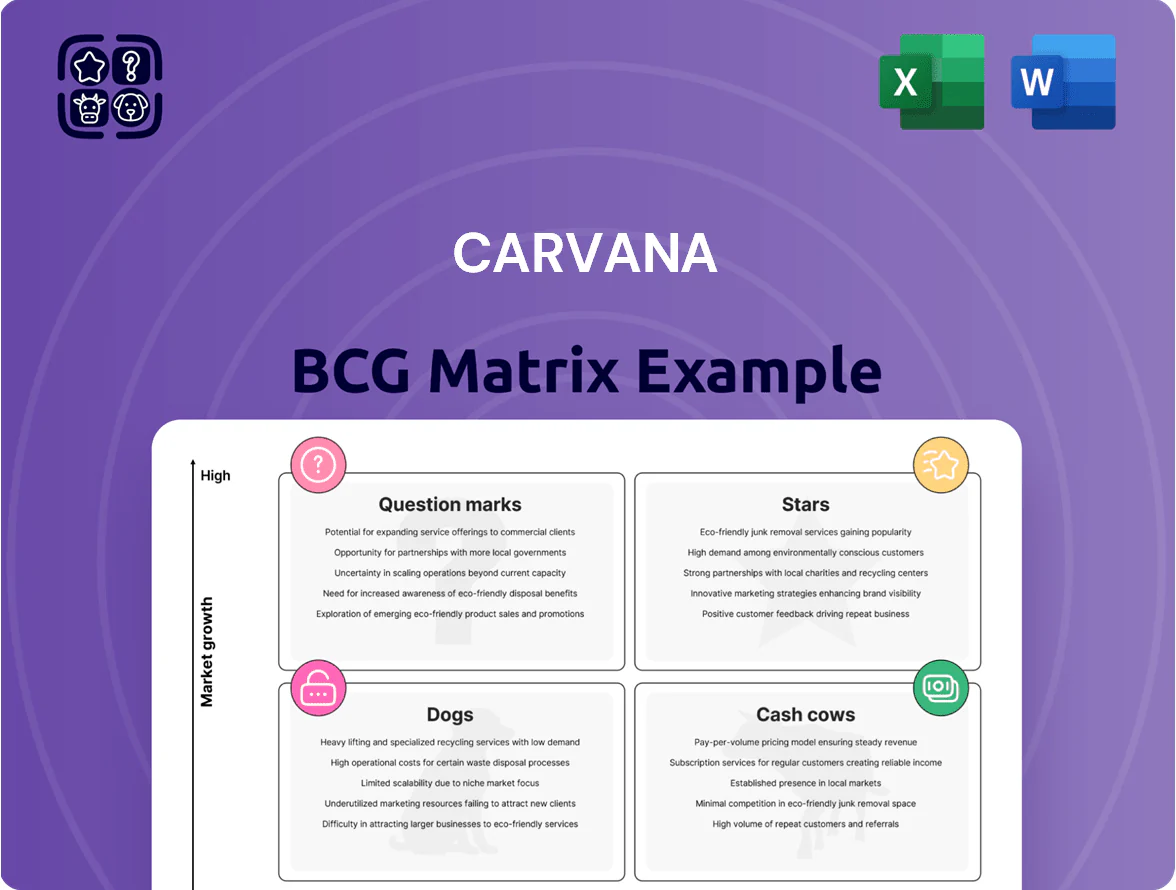

Carvana’s BCG Matrix preview highlights where its core offerings sit amid shifting used-vehicle demand and capital intensity—showing early signs of Question Marks in new markets and Cash Cow potential in mature metro segments. This snapshot teases strategic moves like pruning low-return channels and doubling down on high-share, high-growth corridors. Dive deeper into the full BCG Matrix to get quadrant-level data, actionable recommendations, and ready-to-use Word and Excel deliverables for confident investment and portfolio decisions—purchase now for instant access.

Stars

Digital Retail Platform Growth

Carvana leads the online-only used-vehicle market with an estimated 30–35% share of pure-play digital retail as of 2025, outpacing rivals like Vroom and CarGurus in transaction volume.

Permanent consumer shifts to e-commerce for high-ticket items drive ~20–25% CAGR in digital car sales through 2024–25, demanding continued capex in UX and backend systems.

Platform scalability supports high volume—Carvana sold ~300k units in 2024—but maintaining tech edge burns cash: negative free cash flow of about $1.2B in FY2024.

GPU and Unit Profitability Expansion

Carvana raised Gross Profit per Unit to a record $3,350 in FY2024, driven by vertical integration and faster reconditioning—this GPU spike is a key reason investors treat GPU expansion as a Star in the BCG matrix.

The metric still grows as Carvana expands into new markets, so GPU remains a high-share, high-growth asset rather than a Cash Cow.

Sustaining $3k+ GPU needs ongoing reinvestment: Carvana increased tech and logistics capex to $710M in 2024 to scale proprietary software and fulfillment networks.

In-House Automotive Financing

Carvana’s in-house financing captures a large slice of subprime/near-prime lending tied to its inventory, financing roughly 40% of retail units in 2024 and boosting unit economics per sale.

The unit grows with vehicle sales and in 2024 generated ~$1.2 billion revenue from loan interest and fees plus securitization gains, per company filings.

It’s a star: highly profitable via interest margins and ABS (asset‑backed security) proceeds, yet needs continuous capital—Carvana issued ~$3.5 billion of ABS in 2024 to fund originations and manage credit risk.

Vehicle Reconditioning Centers (IRCs)

Carvana’s Inspection and Reconditioning Centers (IRCs) are a high-market-share infrastructure asset that enables rapid inventory turnover, processing ~10–20 vehicles per technician per day and cutting time-to-sale to under 7 days in 2024.

As Carvana expanded to 300+ markets by end-2025, IRC capacity must scale with fleet growth; adding a single automated IRC costs $30–60M and raises fixed capex materially.

IRCs underpin market leadership via consistent quality control and 95%+ post-sale inspection pass rates, but require ongoing heavy capex and automation spend to sustain margins.

- High share asset: speeds turnover, <7-day sell cycle

- Scale need: 300+ markets (2025)

- Capex: $30–60M per automated IRC

- Quality: ~95% inspection pass rate

Direct-to-Consumer Wholesale Sourcing

The Sell to Carvana engine grew to ~18% of Carvana’s 2024 vehicle sourcing, delivering ~15–20 percentage points higher gross margin vs auction buys and helping reduce days-to-sale to 12 days in 2024; it's a Star because rapid volume growth demands heavy marketing spend to keep brand recall among sellers.

- Grew to ~18% of sourcing in 2024

- ~15–20 pp higher gross margin vs auctions

- Reduced days-to-sale to 12 days (2024)

- Requires aggressive marketing to sustain growth

Carvana’s high-margin growth engines fuel scale—GPU, financing, IRCs, Sell-to-Carvana

Stars: Carvana’s high-share, high-growth assets—GPU ($3,350/unit FY2024), in-house financing (40% of retail, ~$1.2B revenue FY2024), IRCs (300+ markets by 2025; $30–60M per automated IRC), and Sell-to-Carvana (18% sourcing, +15–20pp gross margin)—drive growth but require heavy capex and ABS issuance (~$3.5B 2024).

| Metric | 2024–25 |

|---|---|

| GPU | $3,350/unit |

| Units sold | ~300k (2024) |

| Financing | 40% of retail; $1.2B rev |

| ABS issued | $3.5B (2024) |

| IRCs | 300+ markets; $30–60M each |

| Sell-to-Carvana | 18% sourcing; +15–20pp margin |

What is included in the product

BCG Matrix for Carvana: maps units into Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page Carvana BCG Matrix placing segments in quadrants for quick strategic decisions and investor decks.

Cash Cows

Ancillary Product Sales

Sales of extended warranties, GAP insurance, and protection plans generate high-margin, high-share revenue within Carvana’s customer base—ancillary attach rates exceeded 35% in 2024, contributing roughly $250–300 million in operating cash flow that year.

These products see low product-development growth but near-zero incremental cost, yielding gross margins often above 60%, and they fund riskier segments like inventory financing and marketing.

Established Logistics Network

The mature hubs in Carvana’s proprietary logistics now run at high efficiency, with incremental delivery costs down about 25% versus 2019 levels and last-mile cost per vehicle near $120 in 2024, enabling low-growth, high-margin cash generation.

In established regions where infrastructure is fully built out, Carvana can effectively milk last-mile efficiencies—vehicle throughput per hub rose ~18% YoY in 2024—reducing incremental capex and lifting adjusted EBITDA margins.

The network cuts reliance on third-party carriers; outsourced shipping fell to roughly 12% of deliveries in 2024, lowering variable costs and supporting steady free cash flow in core markets.

Car Vending Machines in Mature Markets

In early-entry cities, Carvana’s iconic car vending machines act as low-cost marketing and automated pickup points, driving local brand recognition—Carvana reported 2024 vending-related visits averaging 12,000 per site annually in top metros, lifting same-store delivery throughput by ~18% versus non-vending locations.

Securitization Gain-on-Sale

The bundling and sale of Carvana’s auto loans into securitizations has become a standardized, high-volume cash cow, delivering steady gain-on-sale revenue; in 2025 Carvana reported roughly $1.2 billion of loan sales and related gains year-to-date, supporting operations.

While loans sit in the financing star, securitization execution is mature and predictable, generating consistent liquidity that helps cover interest on Carvana’s corporate debt and fund vehicle acquisition and tech investments.

- 2025 YTD loan sales ~ $1.2B

- Provides recurring gain-on-sale cash

- Funds debt service and growth spend

Brand Equity and Organic Traffic

Carvana’s mature brand drives high organic search and referrals—US organic visits averaged ~12 million/month in 2024—cutting customer acquisition cost in legacy markets and letting Carvana sustain market share with lower ad spend (marketing expense fell to 5.1% of revenue in FY2024 vs 7.4% in FY2022).

The strong brand underpins launches into riskier ventures (used subscription pilots, wholesale tech) by providing steady unit economics and referral funnels that reduce early-stage marketing burn.

- ~12M organic visits/month (2024)

- Marketing spend 5.1% of revenue FY2024

- Lower CAC in legacy markets (company reports)

- Brand supports new pilots with referral flow

Carvana’s cash engines: high-margin ancillaries, cheap logistics, $1.2B loan sales

Carvana’s cash cows: high-margin ancillaries (35% attach, $250–300M OCF 2024), mature logistics (last-mile ~$120/vehicle, 25% lower incremental delivery costs vs 2019), repeatable loan securitizations ($1.2B YTD loan sales 2025), and strong organic demand (~12M visits/month 2024) that cut marketing to 5.1% of revenue FY2024.

| Metric | 2024/2025 |

|---|---|

| Ancillary OCF | $250–300M (2024) |

| Attach rate | 35% (2024) |

| Last-mile cost | $120/vehicle (2024) |

| Loan sales | $1.2B YTD (2025) |

| Organic visits | ~12M/mo (2024) |

| Marketing spend | 5.1% rev (FY2024) |

Preview = Final Product

Carvana BCG Matrix

The file you're previewing is the exact Carvana BCG Matrix report you’ll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use. This preview mirrors the final downloadable file, built from market-backed insights and ready for editing, printing, or presentation. Purchase grants immediate access to the same polished report delivered to your inbox—no surprises, no revisions required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Carvana’s BCG Matrix preview highlights where its core offerings sit amid shifting used-vehicle demand and capital intensity—showing early signs of Question Marks in new markets and Cash Cow potential in mature metro segments. This snapshot teases strategic moves like pruning low-return channels and doubling down on high-share, high-growth corridors. Dive deeper into the full BCG Matrix to get quadrant-level data, actionable recommendations, and ready-to-use Word and Excel deliverables for confident investment and portfolio decisions—purchase now for instant access.

Stars

Digital Retail Platform Growth

Carvana leads the online-only used-vehicle market with an estimated 30–35% share of pure-play digital retail as of 2025, outpacing rivals like Vroom and CarGurus in transaction volume.

Permanent consumer shifts to e-commerce for high-ticket items drive ~20–25% CAGR in digital car sales through 2024–25, demanding continued capex in UX and backend systems.

Platform scalability supports high volume—Carvana sold ~300k units in 2024—but maintaining tech edge burns cash: negative free cash flow of about $1.2B in FY2024.

GPU and Unit Profitability Expansion

Carvana raised Gross Profit per Unit to a record $3,350 in FY2024, driven by vertical integration and faster reconditioning—this GPU spike is a key reason investors treat GPU expansion as a Star in the BCG matrix.

The metric still grows as Carvana expands into new markets, so GPU remains a high-share, high-growth asset rather than a Cash Cow.

Sustaining $3k+ GPU needs ongoing reinvestment: Carvana increased tech and logistics capex to $710M in 2024 to scale proprietary software and fulfillment networks.

In-House Automotive Financing

Carvana’s in-house financing captures a large slice of subprime/near-prime lending tied to its inventory, financing roughly 40% of retail units in 2024 and boosting unit economics per sale.

The unit grows with vehicle sales and in 2024 generated ~$1.2 billion revenue from loan interest and fees plus securitization gains, per company filings.

It’s a star: highly profitable via interest margins and ABS (asset‑backed security) proceeds, yet needs continuous capital—Carvana issued ~$3.5 billion of ABS in 2024 to fund originations and manage credit risk.

Vehicle Reconditioning Centers (IRCs)

Carvana’s Inspection and Reconditioning Centers (IRCs) are a high-market-share infrastructure asset that enables rapid inventory turnover, processing ~10–20 vehicles per technician per day and cutting time-to-sale to under 7 days in 2024.

As Carvana expanded to 300+ markets by end-2025, IRC capacity must scale with fleet growth; adding a single automated IRC costs $30–60M and raises fixed capex materially.

IRCs underpin market leadership via consistent quality control and 95%+ post-sale inspection pass rates, but require ongoing heavy capex and automation spend to sustain margins.

- High share asset: speeds turnover, <7-day sell cycle

- Scale need: 300+ markets (2025)

- Capex: $30–60M per automated IRC

- Quality: ~95% inspection pass rate

Direct-to-Consumer Wholesale Sourcing

The Sell to Carvana engine grew to ~18% of Carvana’s 2024 vehicle sourcing, delivering ~15–20 percentage points higher gross margin vs auction buys and helping reduce days-to-sale to 12 days in 2024; it's a Star because rapid volume growth demands heavy marketing spend to keep brand recall among sellers.

- Grew to ~18% of sourcing in 2024

- ~15–20 pp higher gross margin vs auctions

- Reduced days-to-sale to 12 days (2024)

- Requires aggressive marketing to sustain growth

Carvana’s high-margin growth engines fuel scale—GPU, financing, IRCs, Sell-to-Carvana

Stars: Carvana’s high-share, high-growth assets—GPU ($3,350/unit FY2024), in-house financing (40% of retail, ~$1.2B revenue FY2024), IRCs (300+ markets by 2025; $30–60M per automated IRC), and Sell-to-Carvana (18% sourcing, +15–20pp gross margin)—drive growth but require heavy capex and ABS issuance (~$3.5B 2024).

| Metric | 2024–25 |

|---|---|

| GPU | $3,350/unit |

| Units sold | ~300k (2024) |

| Financing | 40% of retail; $1.2B rev |

| ABS issued | $3.5B (2024) |

| IRCs | 300+ markets; $30–60M each |

| Sell-to-Carvana | 18% sourcing; +15–20pp margin |

What is included in the product

BCG Matrix for Carvana: maps units into Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page Carvana BCG Matrix placing segments in quadrants for quick strategic decisions and investor decks.

Cash Cows

Ancillary Product Sales

Sales of extended warranties, GAP insurance, and protection plans generate high-margin, high-share revenue within Carvana’s customer base—ancillary attach rates exceeded 35% in 2024, contributing roughly $250–300 million in operating cash flow that year.

These products see low product-development growth but near-zero incremental cost, yielding gross margins often above 60%, and they fund riskier segments like inventory financing and marketing.

Established Logistics Network

The mature hubs in Carvana’s proprietary logistics now run at high efficiency, with incremental delivery costs down about 25% versus 2019 levels and last-mile cost per vehicle near $120 in 2024, enabling low-growth, high-margin cash generation.

In established regions where infrastructure is fully built out, Carvana can effectively milk last-mile efficiencies—vehicle throughput per hub rose ~18% YoY in 2024—reducing incremental capex and lifting adjusted EBITDA margins.

The network cuts reliance on third-party carriers; outsourced shipping fell to roughly 12% of deliveries in 2024, lowering variable costs and supporting steady free cash flow in core markets.

Car Vending Machines in Mature Markets

In early-entry cities, Carvana’s iconic car vending machines act as low-cost marketing and automated pickup points, driving local brand recognition—Carvana reported 2024 vending-related visits averaging 12,000 per site annually in top metros, lifting same-store delivery throughput by ~18% versus non-vending locations.

Securitization Gain-on-Sale

The bundling and sale of Carvana’s auto loans into securitizations has become a standardized, high-volume cash cow, delivering steady gain-on-sale revenue; in 2025 Carvana reported roughly $1.2 billion of loan sales and related gains year-to-date, supporting operations.

While loans sit in the financing star, securitization execution is mature and predictable, generating consistent liquidity that helps cover interest on Carvana’s corporate debt and fund vehicle acquisition and tech investments.

- 2025 YTD loan sales ~ $1.2B

- Provides recurring gain-on-sale cash

- Funds debt service and growth spend

Brand Equity and Organic Traffic

Carvana’s mature brand drives high organic search and referrals—US organic visits averaged ~12 million/month in 2024—cutting customer acquisition cost in legacy markets and letting Carvana sustain market share with lower ad spend (marketing expense fell to 5.1% of revenue in FY2024 vs 7.4% in FY2022).

The strong brand underpins launches into riskier ventures (used subscription pilots, wholesale tech) by providing steady unit economics and referral funnels that reduce early-stage marketing burn.

- ~12M organic visits/month (2024)

- Marketing spend 5.1% of revenue FY2024

- Lower CAC in legacy markets (company reports)

- Brand supports new pilots with referral flow

Carvana’s cash engines: high-margin ancillaries, cheap logistics, $1.2B loan sales

Carvana’s cash cows: high-margin ancillaries (35% attach, $250–300M OCF 2024), mature logistics (last-mile ~$120/vehicle, 25% lower incremental delivery costs vs 2019), repeatable loan securitizations ($1.2B YTD loan sales 2025), and strong organic demand (~12M visits/month 2024) that cut marketing to 5.1% of revenue FY2024.

| Metric | 2024/2025 |

|---|---|

| Ancillary OCF | $250–300M (2024) |

| Attach rate | 35% (2024) |

| Last-mile cost | $120/vehicle (2024) |

| Loan sales | $1.2B YTD (2025) |

| Organic visits | ~12M/mo (2024) |

| Marketing spend | 5.1% rev (FY2024) |

Preview = Final Product

Carvana BCG Matrix

The file you're previewing is the exact Carvana BCG Matrix report you’ll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use. This preview mirrors the final downloadable file, built from market-backed insights and ready for editing, printing, or presentation. Purchase grants immediate access to the same polished report delivered to your inbox—no surprises, no revisions required.