Casa Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Casa faces moderate supplier leverage and rising buyer sophistication, while new entrants are tempered by scale and brand requirements; substitutes and competitive rivalry create pockets of pressure that demand strategic differentiation and cost discipline. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Casa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Subcontractor Market

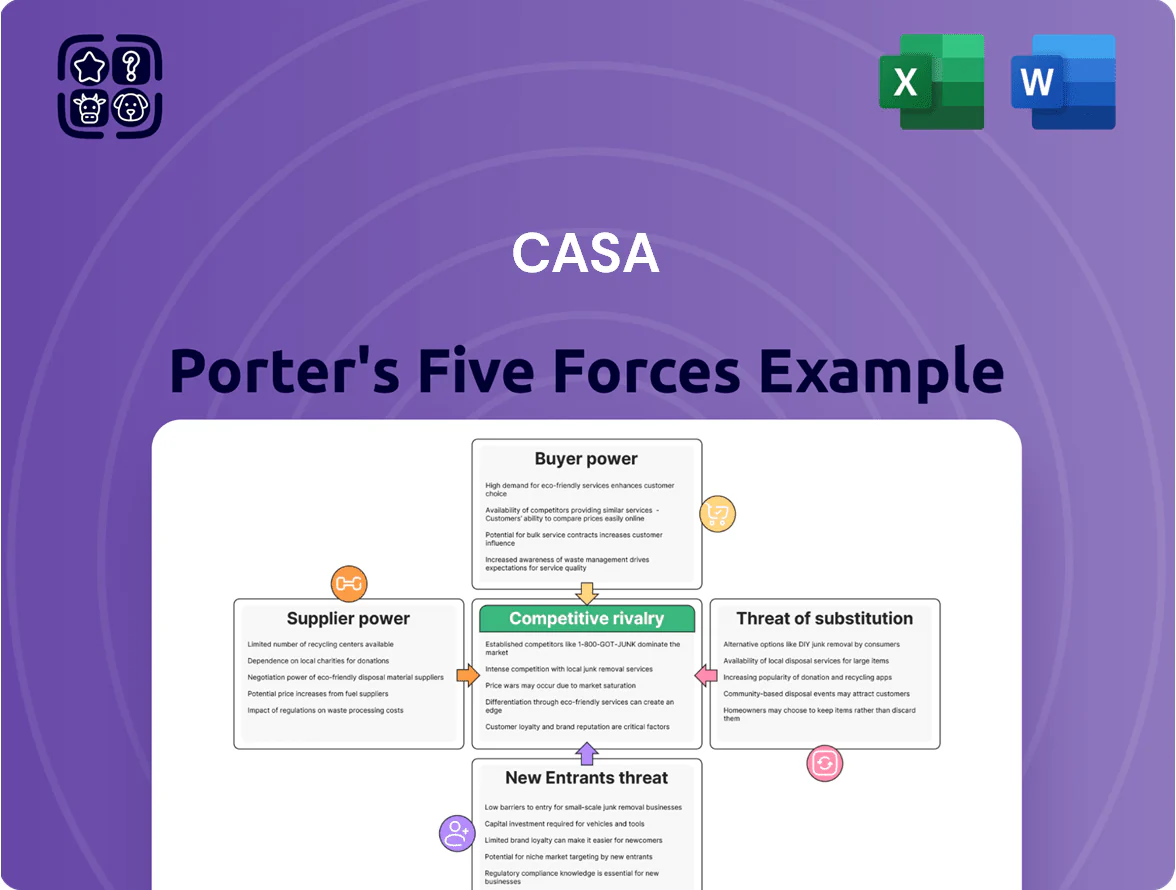

The Danish construction sector has about 28,000 subcontracting firms as of 2024, mostly small-to-medium specialists, so individual supplier bargaining power vs Casa Porter is generally low.

Market fragmentation means Casa can switch vendors, press for standard terms, and consolidate volumes to get discounts—average subcontractor revenue is under DKK 10m, limiting their clout.

Still, for high-end architectural work—complex façades or bespoke MEP systems—niche specialists hold leverage; 14% of projects in 2024 required such expertise, raising supplier pricing and schedule risk.

Volatility in Raw Material Pricing

Global supply-chain shocks through 2025 pushed steel, timber and concrete prices up 18–27% year-over-year; Casa Porter uses scale to cut unit costs by ~6% versus SMEs but still faces dependency on major producers for 65% of inputs.

Specialized Green Material Scarcity

Skilled Labor Shortages

Technological Integration Costs

Suppliers of BIM and construction-management platforms hold moderate bargaining power for Casa because high switching costs create technical lock-in; industry surveys show 62% of firms report migration costs over $250,000 and 6–12 months of downtime (McKinsey, 2024).

This lock-in lets vendors keep steady subscription pricing—median annual SaaS contract renewals rose 8% in 2024—while Casa faces trade-offs between flexibility and operational disruption.

- 62% report migration >$250k

- 6–12 months typical downtime

- 2024 SaaS renewals +8%

Supply squeeze: niche suppliers, wage hikes & costly BIM migrations drive Casa costs up

Suppliers have mixed power: fragmented subcontractor market (28,000 firms; avg revenue

| Metric | 2024–25 |

|---|---|

| Subcontractors | 28,000 |

| Niche projects | 14% |

| Low‑carbon suppliers | 12 major |

| Labor wage rise | 6–8% |

| Casa labour cost | +3–5% |

| BIM migration | 62% >$250k |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitution risks, and entry barriers specific to Casa, highlighting disruptive threats and strategic levers to protect market share and profitability in an editable format for investor or internal use.

Casa Porter's Five Forces one-sheet quickly highlights competitive pressures and relief strategies—ideal for rapid boardroom decisions.

Customers Bargaining Power

Institutional Investor Influence

Low Switching Costs in Tendering

In general contracting, customers face low switching costs and routinely choose between Casa Porter's bids and rivals like NCC or Per Aarsleff; in 2024 Norwegian tender win rates showed top three firms competing for ~62% of large projects, raising buyer leverage.

Because most contracts use competitive bidding, buyers compare price, timeline, and risk transfer, so Casa must cut bid margins—average sector EBITDA fell to 5.8% in 2023—while preserving quality to win repeat work.

This tender-driven market forces continuous innovation and cost optimization: Casa’s procurement efficiencies and modular designs reduced bid costs by ~9% in 2024, or it risks losing volume to lower-priced competitors.

High Demand for Sustainable Housing

End-users in 2025 prioritize energy-efficient, socially responsible homes—64% of global buyers say sustainability influences purchase decisions (2024 Edelman Trust Barometer); this raises buyer leverage as developers must meet ESG standards to sell.

Buyers’ demand forces higher upfront costs: green construction adds 3–8% to CAPEX but supports 5–10% price premiums in markets like Madrid and Lisbon (2023–25 transaction data). Casa must embed net-zero targets and social amenities to retain demand and margins.

Transparency and Information Access

Digital tools give buyers real-time access to comps and contractor ratings; 72% of US homebuyers used online pricing tools in 2024, so clients can benchmark Casa Porter against market medians precisely.

That transparency shifts leverage: customers negotiate on price, timelines, and warranties using live market indices and Casa’s past-project metrics (on-time rate, cost variance), reducing Casa’s markup power.

- 72% of buyers used online pricing tools (2024)

- Benchmarking enables precise price and timeline demands

- Historical on-time rate and cost variance drive tougher negotiations

Economic Sensitivity and Interest Rates

- Rates ~5.5% Q4 2025

- Decision cycles lengthen 20% (industry data)

- 35% buyers cite affordability

- Offer longer terms, lower deposits, value-engineering

Casa must offer flexible financing, value‑engineering & stronger ESG to protect margins

| Metric | Value |

|---|---|

| Institutional revenue | 45% (2024) |

| ESG tenders | 70% (2024) |

| Sector EBITDA | 5.8% (2023) |

| Bid-cost reduction | 9% (2024) |

| Rates | 5.5% Q4 2025 |

Preview Before You Purchase

Casa Porter's Five Forces Analysis

This preview shows the exact Casa Porter Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. You're looking at the actual, fully formatted document ready for download and use the moment you buy. The file includes the complete competitive assessment, supplier and buyer power evaluation, threat of entrants and substitutes, and rivalry analysis. Once purchased, you’ll get instant access to this same professional report.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Casa faces moderate supplier leverage and rising buyer sophistication, while new entrants are tempered by scale and brand requirements; substitutes and competitive rivalry create pockets of pressure that demand strategic differentiation and cost discipline. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Casa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Subcontractor Market

The Danish construction sector has about 28,000 subcontracting firms as of 2024, mostly small-to-medium specialists, so individual supplier bargaining power vs Casa Porter is generally low.

Market fragmentation means Casa can switch vendors, press for standard terms, and consolidate volumes to get discounts—average subcontractor revenue is under DKK 10m, limiting their clout.

Still, for high-end architectural work—complex façades or bespoke MEP systems—niche specialists hold leverage; 14% of projects in 2024 required such expertise, raising supplier pricing and schedule risk.

Volatility in Raw Material Pricing

Global supply-chain shocks through 2025 pushed steel, timber and concrete prices up 18–27% year-over-year; Casa Porter uses scale to cut unit costs by ~6% versus SMEs but still faces dependency on major producers for 65% of inputs.

Specialized Green Material Scarcity

Skilled Labor Shortages

Technological Integration Costs

Suppliers of BIM and construction-management platforms hold moderate bargaining power for Casa because high switching costs create technical lock-in; industry surveys show 62% of firms report migration costs over $250,000 and 6–12 months of downtime (McKinsey, 2024).

This lock-in lets vendors keep steady subscription pricing—median annual SaaS contract renewals rose 8% in 2024—while Casa faces trade-offs between flexibility and operational disruption.

- 62% report migration >$250k

- 6–12 months typical downtime

- 2024 SaaS renewals +8%

Supply squeeze: niche suppliers, wage hikes & costly BIM migrations drive Casa costs up

Suppliers have mixed power: fragmented subcontractor market (28,000 firms; avg revenue

| Metric | 2024–25 |

|---|---|

| Subcontractors | 28,000 |

| Niche projects | 14% |

| Low‑carbon suppliers | 12 major |

| Labor wage rise | 6–8% |

| Casa labour cost | +3–5% |

| BIM migration | 62% >$250k |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitution risks, and entry barriers specific to Casa, highlighting disruptive threats and strategic levers to protect market share and profitability in an editable format for investor or internal use.

Casa Porter's Five Forces one-sheet quickly highlights competitive pressures and relief strategies—ideal for rapid boardroom decisions.

Customers Bargaining Power

Institutional Investor Influence

Low Switching Costs in Tendering

In general contracting, customers face low switching costs and routinely choose between Casa Porter's bids and rivals like NCC or Per Aarsleff; in 2024 Norwegian tender win rates showed top three firms competing for ~62% of large projects, raising buyer leverage.

Because most contracts use competitive bidding, buyers compare price, timeline, and risk transfer, so Casa must cut bid margins—average sector EBITDA fell to 5.8% in 2023—while preserving quality to win repeat work.

This tender-driven market forces continuous innovation and cost optimization: Casa’s procurement efficiencies and modular designs reduced bid costs by ~9% in 2024, or it risks losing volume to lower-priced competitors.

High Demand for Sustainable Housing

End-users in 2025 prioritize energy-efficient, socially responsible homes—64% of global buyers say sustainability influences purchase decisions (2024 Edelman Trust Barometer); this raises buyer leverage as developers must meet ESG standards to sell.

Buyers’ demand forces higher upfront costs: green construction adds 3–8% to CAPEX but supports 5–10% price premiums in markets like Madrid and Lisbon (2023–25 transaction data). Casa must embed net-zero targets and social amenities to retain demand and margins.

Transparency and Information Access

Digital tools give buyers real-time access to comps and contractor ratings; 72% of US homebuyers used online pricing tools in 2024, so clients can benchmark Casa Porter against market medians precisely.

That transparency shifts leverage: customers negotiate on price, timelines, and warranties using live market indices and Casa’s past-project metrics (on-time rate, cost variance), reducing Casa’s markup power.

- 72% of buyers used online pricing tools (2024)

- Benchmarking enables precise price and timeline demands

- Historical on-time rate and cost variance drive tougher negotiations

Economic Sensitivity and Interest Rates

- Rates ~5.5% Q4 2025

- Decision cycles lengthen 20% (industry data)

- 35% buyers cite affordability

- Offer longer terms, lower deposits, value-engineering

Casa must offer flexible financing, value‑engineering & stronger ESG to protect margins

| Metric | Value |

|---|---|

| Institutional revenue | 45% (2024) |

| ESG tenders | 70% (2024) |

| Sector EBITDA | 5.8% (2023) |

| Bid-cost reduction | 9% (2024) |

| Rates | 5.5% Q4 2025 |

Preview Before You Purchase

Casa Porter's Five Forces Analysis

This preview shows the exact Casa Porter Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. You're looking at the actual, fully formatted document ready for download and use the moment you buy. The file includes the complete competitive assessment, supplier and buyer power evaluation, threat of entrants and substitutes, and rivalry analysis. Once purchased, you’ll get instant access to this same professional report.