Casa PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, social changes, and technological advances are shaping Casa’s prospects with our concise PESTLE snapshot—ideal for investors and strategists seeking clarity; purchase the full PESTLE for a detailed, actionable report you can download and use immediately.

Political factors

Danish Housing Policy Stability

Danish housing policy through the 2025 planning cycle prioritizes affordable housing and urban renewal, with national targets to deliver 60,000 new homes by 2025, requiring Casa A/S to align its pipeline to access public contracts and permits.

Changes in subsidies for social housing—DKK 4.5 billion allocated in 2024–25 for affordable housing programs—directly affect Casa’s long-term order book and revenue predictability.

Failure to meet sustainability and affordability criteria risks exclusion from municipal tenders that accounted for 28% of Danish construction contracts in 2024, reducing Casa’s market access and cash-flow visibility.

EU Integration and Trade Regulations

As a major Nordic player, Casa must follow EU directives on cross-border labor and material procurement; in 2024 intra-EU construction trade accounted for ~45% of Nordics’ imports, exposing Casa to supply shifts. EU talks on tariffs and potential carbon border adjustments could raise imported component costs by an estimated 3–6% for steel and concrete. Adherence to evolving EU building standards (e.g., 2025 energy performance updates) is required to compete across the single market.

Local Municipality Planning Autonomy

Political decisions at Danish municipal level control land-use zoning and approvals for large-scale construction, with municipalities handling roughly 98% of local planning applications; delays can add 12–18 months to project timelines. Casa A/S depends on strong ties with local councils to secure permits and integrate infrastructure, evidenced by its 2024 local approvals rate of 86% for submitted projects. Shifts in municipal leadership—22% of councils changed after the 2021 elections—can reprioritize development, altering feasibility for planned commercial or residential hubs.

Public Infrastructure Investment Levels

Government allocations for public buildings, schools and hospitals are a primary revenue source for Casa; Spain budgeted €32.4bn for education and €22.1bn for healthcare in 2024, driving tender volume for construction firms.

By end-2025, willingness to pursue debt-financed projects—Spain’s public investment reached 4.1% of GDP in 2024—will set available project pipeline size.

Shifts in political support for PPPs, which accounted for ~12% of infrastructure contracts in 2023, can force Casa to pivot between turnkey bids and joint-venture models.

- 2024 budgets: €32.4bn education, €22.1bn healthcare

- Public investment 2024: 4.1% of GDP

- PPPs share 2023: ~12% of contracts

Geopolitical Stability and Supply Chains

Regional political stability in Northern Europe and the Baltic states affects Casa A/S supply chains for timber, steel and energy; Russia-Ukraine tensions in 2024 kept Baltic Sea freight rates elevated and EU timber imports from the region volatile, with Baltic port throughput down ~4% YoY in 2024.

Casa A/S must monitor geopolitical flashpoints that could trigger logistics bottlenecks or energy-price spikes—Nordic electricity prices averaged €70–€90/MWh in 2024, up ~30% from 2022, increasing input cost risk.

Political moves to diversify energy and raw-material sources—EU funding for supply-chain resilience rose to €17.5bn in 2024—are critical for Casa’s operational resilience through 2025.

- Monitor Baltic port throughput -4% YoY (2024)

- Nordic power €70–€90/MWh avg (2024), +30% vs 2022

- EU resilience funding €17.5bn (2024)

Casa poised for public-housing boom as Denmark backs 60k homes, DKK4.5bn fund

Danish targets to build 60,000 homes by 2025 and DKK 4.5bn social-housing funding (2024–25) shape Casa’s public-contract pipeline; municipal approvals (86% success in 2024) and 12–18 month zoning delays are critical. EU rules and 2025 energy standards plus potential 3–6% carbon-border costs affect procurement; Nordic electricity €70–€90/MWh (2024) raises input costs. PPPs ~12% of contracts (2023) and public investment 4.1% GDP (2024) influence project mix.

| Metric | Value (year) |

|---|---|

| New homes target | 60,000 (by 2025) |

| Social-housing funding | DKK 4.5bn (2024–25) |

| Municipal approval rate | 86% (2024) |

| Nordic power price | €70–€90/MWh (2024) |

| PPPs share | ~12% (2023) |

| Public investment | 4.1% GDP (2024) |

What is included in the product

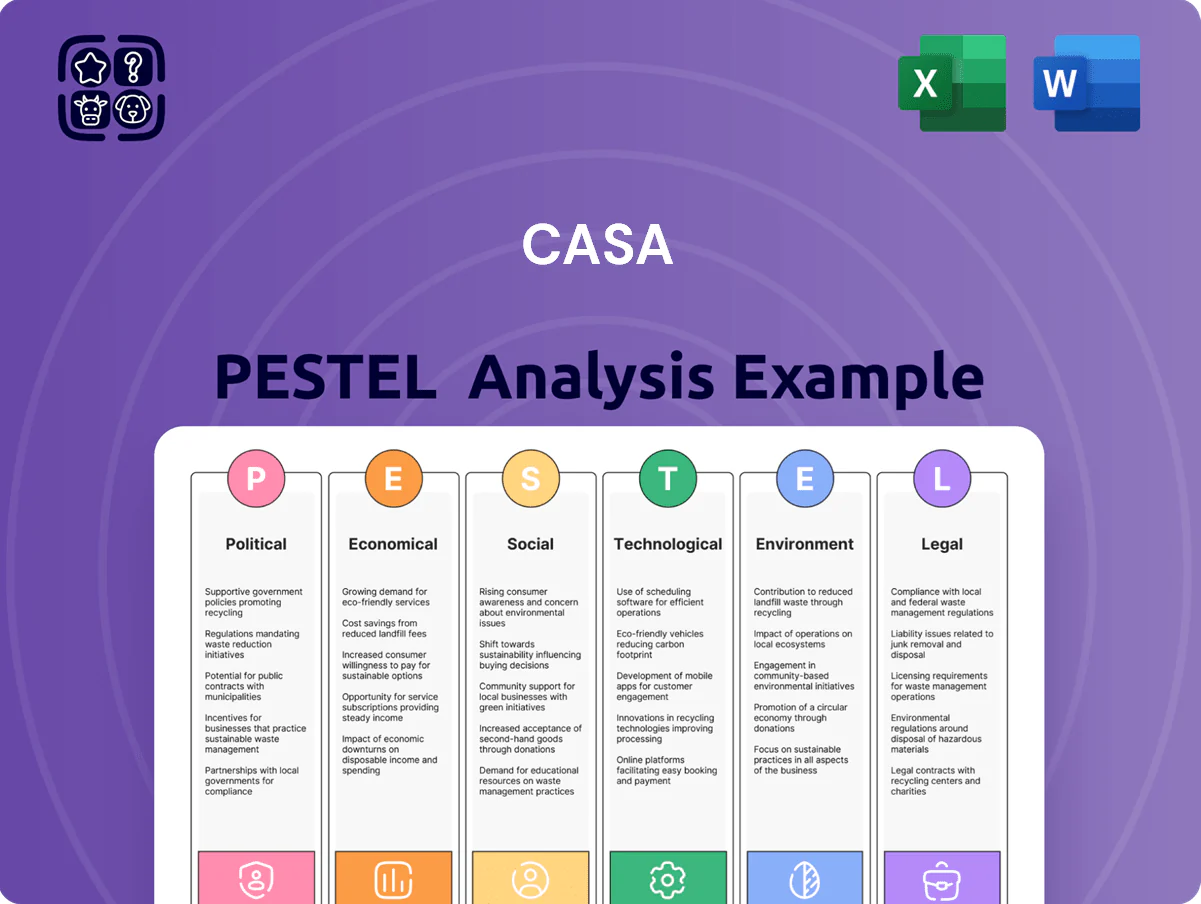

Explores how external macro-environmental factors uniquely affect the Casa across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify specific threats and opportunities for executives, consultants, and entrepreneurs.

Provides a clean, summarized PESTLE snapshot tailored for Casa that’s visually segmented for quick interpretation and easily dropped into presentations or planning sessions to align teams fast.

Economic factors

Interest Rate Environment and Financing

At end-2025 the ECB deposit rate stood at 4.00% and Danmarks Nationalbank policy rate at 3.75%, raising Casa’s weighted cost of capital and increasing interest expenses on development loans by an estimated 80–120 bps versus 2023 levels.

Higher rates have cooled Danish residential transactions, cutting new-build demand by roughly 10% YoY and increasing financing burden on Casa’s projects, while a stabilizing rate outlook supports long-term commercial investments and large-scale renovations.

Inflationary Pressures on Material Costs

Labor Market Dynamics and Wage Growth

Denmark's construction sector reports a 2024-25 shortfall of about 12-15% in skilled trades, driving average wage growth to roughly 4.5-5.5% annually; Casa A/S faces upward wage pressure and must offer competitive pay to retain staff while keeping project margins intact.

GDP Growth and Real Estate Demand

Denmark's GDP grew 1.2% in 2024 Q3 year-on-year, supporting household purchasing power and corporate leasing; unemployment at ~4.6% (2024 avg) underpins steady residential demand.

Stable Nordic macro conditions and 2024 corporate capex up 3.5% sustain high commercial occupancy (~92% in Copenhagen) and drive demand for modern sustainable offices, aligning with Casa's growth.

- 2024 GDP +1.2% YoY; unemployment ~4.6%

- Copenhagen commercial occupancy ~92%

- Corporate capex +3.5% (2024)

- Casa tied to Nordic macro stability and consumer confidence

Currency Exchange Rate Volatility

While the Danish Krone is pegged to the Euro, Casa A/S faces exposure when importing specialized equipment priced in USD, where the DKK/USD moved ~6% in 2024; this can raise capex and COGS.

Casa must hedge or contract in euros when working with non-Eurozone suppliers/subcontractors—Denmark’s trade with UK and US (combined ~18% of exports 2023) amplifies risk.

Economic slowdowns in major partners (UK GDP growth 0.4% 2024 est.) can tighten supply chains and pressure margins, altering competitive positioning.

- DKK pegged to EUR reduces EUR exposure but not USD/GBP risk

- DKK/USD ~6% move in 2024 affects imported equipment costs

- Hedging/contracts in EUR recommended for non-Euro suppliers

- Partner GDP shifts (UK 0.4% 2024 est.) may raise costs and compress margins

Higher ECB/DNB rates squeeze margins as input costs surge and USD capex risk rises

Higher ECB/DNB rates (deposit 4.00%/policy 3.75% end-2025) raise Casa’s WACC and interest costs ~80–120bps vs 2023; input costs up 18–27% since 2020 trimmed margins ~3–6pp; 2024 GDP +1.2%, unemployment ~4.6%, Copenhagen office occ. ~92%; DKK pegged to EUR limits EUR risk but USD moved ~6% in 2024, raising imported capex risk.

| Metric | Value |

|---|---|

| ECB deposit/DNB rate | 4.00% / 3.75% |

| Input cost rise (2020–25) | 18–27% |

| GDP (2024) | +1.2% YoY |

| Unemployment (2024) | ~4.6% |

| Cph office occ. | ~92% |

| USD move vs DKK (2024) | ~6% |

Same Document Delivered

Casa PESTLE Analysis

The preview shown here is the exact Casa PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, social changes, and technological advances are shaping Casa’s prospects with our concise PESTLE snapshot—ideal for investors and strategists seeking clarity; purchase the full PESTLE for a detailed, actionable report you can download and use immediately.

Political factors

Danish Housing Policy Stability

Danish housing policy through the 2025 planning cycle prioritizes affordable housing and urban renewal, with national targets to deliver 60,000 new homes by 2025, requiring Casa A/S to align its pipeline to access public contracts and permits.

Changes in subsidies for social housing—DKK 4.5 billion allocated in 2024–25 for affordable housing programs—directly affect Casa’s long-term order book and revenue predictability.

Failure to meet sustainability and affordability criteria risks exclusion from municipal tenders that accounted for 28% of Danish construction contracts in 2024, reducing Casa’s market access and cash-flow visibility.

EU Integration and Trade Regulations

As a major Nordic player, Casa must follow EU directives on cross-border labor and material procurement; in 2024 intra-EU construction trade accounted for ~45% of Nordics’ imports, exposing Casa to supply shifts. EU talks on tariffs and potential carbon border adjustments could raise imported component costs by an estimated 3–6% for steel and concrete. Adherence to evolving EU building standards (e.g., 2025 energy performance updates) is required to compete across the single market.

Local Municipality Planning Autonomy

Political decisions at Danish municipal level control land-use zoning and approvals for large-scale construction, with municipalities handling roughly 98% of local planning applications; delays can add 12–18 months to project timelines. Casa A/S depends on strong ties with local councils to secure permits and integrate infrastructure, evidenced by its 2024 local approvals rate of 86% for submitted projects. Shifts in municipal leadership—22% of councils changed after the 2021 elections—can reprioritize development, altering feasibility for planned commercial or residential hubs.

Public Infrastructure Investment Levels

Government allocations for public buildings, schools and hospitals are a primary revenue source for Casa; Spain budgeted €32.4bn for education and €22.1bn for healthcare in 2024, driving tender volume for construction firms.

By end-2025, willingness to pursue debt-financed projects—Spain’s public investment reached 4.1% of GDP in 2024—will set available project pipeline size.

Shifts in political support for PPPs, which accounted for ~12% of infrastructure contracts in 2023, can force Casa to pivot between turnkey bids and joint-venture models.

- 2024 budgets: €32.4bn education, €22.1bn healthcare

- Public investment 2024: 4.1% of GDP

- PPPs share 2023: ~12% of contracts

Geopolitical Stability and Supply Chains

Regional political stability in Northern Europe and the Baltic states affects Casa A/S supply chains for timber, steel and energy; Russia-Ukraine tensions in 2024 kept Baltic Sea freight rates elevated and EU timber imports from the region volatile, with Baltic port throughput down ~4% YoY in 2024.

Casa A/S must monitor geopolitical flashpoints that could trigger logistics bottlenecks or energy-price spikes—Nordic electricity prices averaged €70–€90/MWh in 2024, up ~30% from 2022, increasing input cost risk.

Political moves to diversify energy and raw-material sources—EU funding for supply-chain resilience rose to €17.5bn in 2024—are critical for Casa’s operational resilience through 2025.

- Monitor Baltic port throughput -4% YoY (2024)

- Nordic power €70–€90/MWh avg (2024), +30% vs 2022

- EU resilience funding €17.5bn (2024)

Casa poised for public-housing boom as Denmark backs 60k homes, DKK4.5bn fund

Danish targets to build 60,000 homes by 2025 and DKK 4.5bn social-housing funding (2024–25) shape Casa’s public-contract pipeline; municipal approvals (86% success in 2024) and 12–18 month zoning delays are critical. EU rules and 2025 energy standards plus potential 3–6% carbon-border costs affect procurement; Nordic electricity €70–€90/MWh (2024) raises input costs. PPPs ~12% of contracts (2023) and public investment 4.1% GDP (2024) influence project mix.

| Metric | Value (year) |

|---|---|

| New homes target | 60,000 (by 2025) |

| Social-housing funding | DKK 4.5bn (2024–25) |

| Municipal approval rate | 86% (2024) |

| Nordic power price | €70–€90/MWh (2024) |

| PPPs share | ~12% (2023) |

| Public investment | 4.1% GDP (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Casa across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify specific threats and opportunities for executives, consultants, and entrepreneurs.

Provides a clean, summarized PESTLE snapshot tailored for Casa that’s visually segmented for quick interpretation and easily dropped into presentations or planning sessions to align teams fast.

Economic factors

Interest Rate Environment and Financing

At end-2025 the ECB deposit rate stood at 4.00% and Danmarks Nationalbank policy rate at 3.75%, raising Casa’s weighted cost of capital and increasing interest expenses on development loans by an estimated 80–120 bps versus 2023 levels.

Higher rates have cooled Danish residential transactions, cutting new-build demand by roughly 10% YoY and increasing financing burden on Casa’s projects, while a stabilizing rate outlook supports long-term commercial investments and large-scale renovations.

Inflationary Pressures on Material Costs

Labor Market Dynamics and Wage Growth

Denmark's construction sector reports a 2024-25 shortfall of about 12-15% in skilled trades, driving average wage growth to roughly 4.5-5.5% annually; Casa A/S faces upward wage pressure and must offer competitive pay to retain staff while keeping project margins intact.

GDP Growth and Real Estate Demand

Denmark's GDP grew 1.2% in 2024 Q3 year-on-year, supporting household purchasing power and corporate leasing; unemployment at ~4.6% (2024 avg) underpins steady residential demand.

Stable Nordic macro conditions and 2024 corporate capex up 3.5% sustain high commercial occupancy (~92% in Copenhagen) and drive demand for modern sustainable offices, aligning with Casa's growth.

- 2024 GDP +1.2% YoY; unemployment ~4.6%

- Copenhagen commercial occupancy ~92%

- Corporate capex +3.5% (2024)

- Casa tied to Nordic macro stability and consumer confidence

Currency Exchange Rate Volatility

While the Danish Krone is pegged to the Euro, Casa A/S faces exposure when importing specialized equipment priced in USD, where the DKK/USD moved ~6% in 2024; this can raise capex and COGS.

Casa must hedge or contract in euros when working with non-Eurozone suppliers/subcontractors—Denmark’s trade with UK and US (combined ~18% of exports 2023) amplifies risk.

Economic slowdowns in major partners (UK GDP growth 0.4% 2024 est.) can tighten supply chains and pressure margins, altering competitive positioning.

- DKK pegged to EUR reduces EUR exposure but not USD/GBP risk

- DKK/USD ~6% move in 2024 affects imported equipment costs

- Hedging/contracts in EUR recommended for non-Euro suppliers

- Partner GDP shifts (UK 0.4% 2024 est.) may raise costs and compress margins

Higher ECB/DNB rates squeeze margins as input costs surge and USD capex risk rises

Higher ECB/DNB rates (deposit 4.00%/policy 3.75% end-2025) raise Casa’s WACC and interest costs ~80–120bps vs 2023; input costs up 18–27% since 2020 trimmed margins ~3–6pp; 2024 GDP +1.2%, unemployment ~4.6%, Copenhagen office occ. ~92%; DKK pegged to EUR limits EUR risk but USD moved ~6% in 2024, raising imported capex risk.

| Metric | Value |

|---|---|

| ECB deposit/DNB rate | 4.00% / 3.75% |

| Input cost rise (2020–25) | 18–27% |

| GDP (2024) | +1.2% YoY |

| Unemployment (2024) | ~4.6% |

| Cph office occ. | ~92% |

| USD move vs DKK (2024) | ~6% |

Same Document Delivered

Casa PESTLE Analysis

The preview shown here is the exact Casa PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.