Casio Computer Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Casio faces moderate rivalry from established electronics firms, strong buyer sensitivity for price and features, supplier stability for key components, low threat from niche entrants, and rising substitute risks from smart devices impacting watches and calculators.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Casio Computer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on specialized semiconductor manufacturers

Casio depends on high-performance chips for calculators, watches, and musical instruments; by Q4 2025, 70% of advanced microcontrollers were produced by three foundries (TSMC, Samsung, GlobalFoundries), giving suppliers pricing and delivery leverage.

Sourcing of proprietary durable materials

G-Shock production needs specialized resins, carbon fibers, and high-grade metals tied to patents held by a small set of chemical and materials firms; in 2024, 60–70% of advanced polymer supply for wearable tech came from the top five suppliers, amplifying supplier concentration risk. Switching to new providers raises technical requalification costs and testing timelines that can exceed $5–10 million and 6–12 months per material line. As a result, Casio faces high switching costs and limited bargaining power, pressuring margins if suppliers raise prices or cut capacity. This dependence also creates strategic lock-in that competitors could exploit.

Geographic concentration of component vendors

Impact of energy costs on raw material pricing

Energy makes up roughly 10–15% of electronics and plastics input costs, so spikes in natural gas and electricity lift suppliers’ breakevens and they pass increases to Casio to protect margins.

By end-2025, 40%+ of long-term component contracts saw energy-linked clauses, giving suppliers stronger leverage to demand price adjustments amid volatile LNG and power markets.

- Energy = ~10–15% of input cost

- 40%+ contracts energy-linked by 2025

- Suppliers passed through price rises to protect margins

Integration of smart technology components

As Casio adds Bluetooth and sensors to classic watches, it grows dependent on tech suppliers who serve fast-growing markets; global MEMS sensor revenue reached $16.4B in 2024, concentrating R&D at large smartphone-focused vendors.

Those suppliers favor big clients, squeezing lead-time and pricing for smaller buyers; Casio’s bargaining power weakens when sourcing cutting-edge modules and 5–15% premium parts.

- Higher supplier leverage: MEMS market $16.4B (2024)

- Priority to large OEMs: smartphone firms capture ~60% sensor volume

- Price/lead-time pressure: 5–15% premium for small buyers

Supplier dominance squeezes Casio: foundry, polymers, energy & MEMS concentration

Suppliers hold strong leverage over Casio due to concentrated foundry (70% by three firms in 2025) and polymer suppliers (60–70% top five in 2024), high switching costs ($5–10M, 6–12 months), regional sourcing concentration (65–75% East Asia), energy exposure (10–15% input; 40%+ contracts energy-linked by 2025), and sensor/MEMS supplier favoritism (MEMS $16.4B 2024; smartphone OEMs ~60% volume).

| Metric | Value |

|---|---|

| Foundry concentration (2025) | 70% (TSMC, Samsung, GF) |

| Polymer suppliers (2024) | 60–70% top 5 |

| East Asia sourcing (2025) | 65–75% |

| Energy share | 10–15% |

| Energy-linked contracts (2025) | 40%+ |

| MEMS market (2024) | $16.4B; smartphone OEMs ~60% |

What is included in the product

Provides a concise Porter's Five Forces overview for Casio Computer, highlighting competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with strategic implications for profitability and market positioning.

A concise Porter's Five Forces snapshot for Casio—highlighting supplier, buyer, rivalry, substitute, and entrant pressures to speed strategic decisions and pitch-ready slides.

Customers Bargaining Power

Low switching costs for consumer electronics

Individual buyers face low switching costs for digital watches and keyboards, so Casio risks churn if rivals offer better features or prices; global smartwatch shipments fell 1% to 163 million in 2024, increasing mid-range competition.

The crowded mid-range market (estimated $45B global wearables in 2024) forces Casio to update models and software frequently to keep users.

If perceived value shifts, customers can leave Casio with minimal friction—retention hinges on continuous value improvements.

High price sensitivity in the educational sector

Students and schools drive ~70–80% of global scientific and graphing calculator demand, making price sensitivity high; a 2023 U.S. College Board survey found 62% of schools cite cost as the top purchase factor, constraining Casio’s pricing power.

Parents and districts routinely compare Casio prices with Texas Instruments and low-cost substitutes; in 2024 TI held ~55% U.S. classroom share vs Casio ~30%, so price hikes risk share loss.

Influence of massive retail and e-commerce platforms

Brand loyalty and the G-Shock community

Casio benefits from intense brand loyalty among G-Shock and Pro Trek collectors; in 2024 G-Shock limited editions sold at 10–30% premiums and secondary-market prices rose 18% YoY, showing low price sensitivity.

This devoted segment values heritage and exclusives, reducing overall customer bargaining power and stabilizing margins—G-Shock accounted for ~22% of Casio’s 2024 watch revenue.

- Collectors pay 10–30% premium

- Secondary prices +18% YoY (2024)

- G-Shock ≈22% of watch revenue (2024)

Information transparency and online reviews

Modern consumers use instant price comparisons and reviews—68% consult online reviews before buying electronics (2024 Edelman Trust Barometer data), boosting buyer leverage over features and price.

This transparency forces Casio to sustain product reliability and service; a 1-star shift on major review sites can cut sales by ~5–9% within months, raising churn risk.

Maintain quality and fast support to prevent negative sentiment that quickly shifts power to buyers.

- 68% consult reviews

- 1-star drop → ~5–9% sales hit

- Focus: reliability + support

Wearables face churn and margin pressure—G-Shock loyalty provides pricing buffer

Customers have mixed leverage: low switching costs in wearables and calculators raise churn risk (smartwatch shipments 163M in 2024; wearables market ~$45B), big retailers/marketplaces squeeze margins (top-5 US retailers ≈60% of electronics sales, 2025), but G-Shock loyalty cushions pricing (G-Shock ≈22% of watch revenue, 2024).

| Metric | Value |

|---|---|

| Smartwatch shipments (2024) | 163M |

| Wearables market (2024) | $45B |

| Top-5 US retailers share (2025) | ≈60% |

| G-Shock share of watch revenue (2024) | ≈22% |

Same Document Delivered

Casio Computer Porter's Five Forces Analysis

This preview shows the exact Casio Computer Porter's Five Forces analysis you'll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.

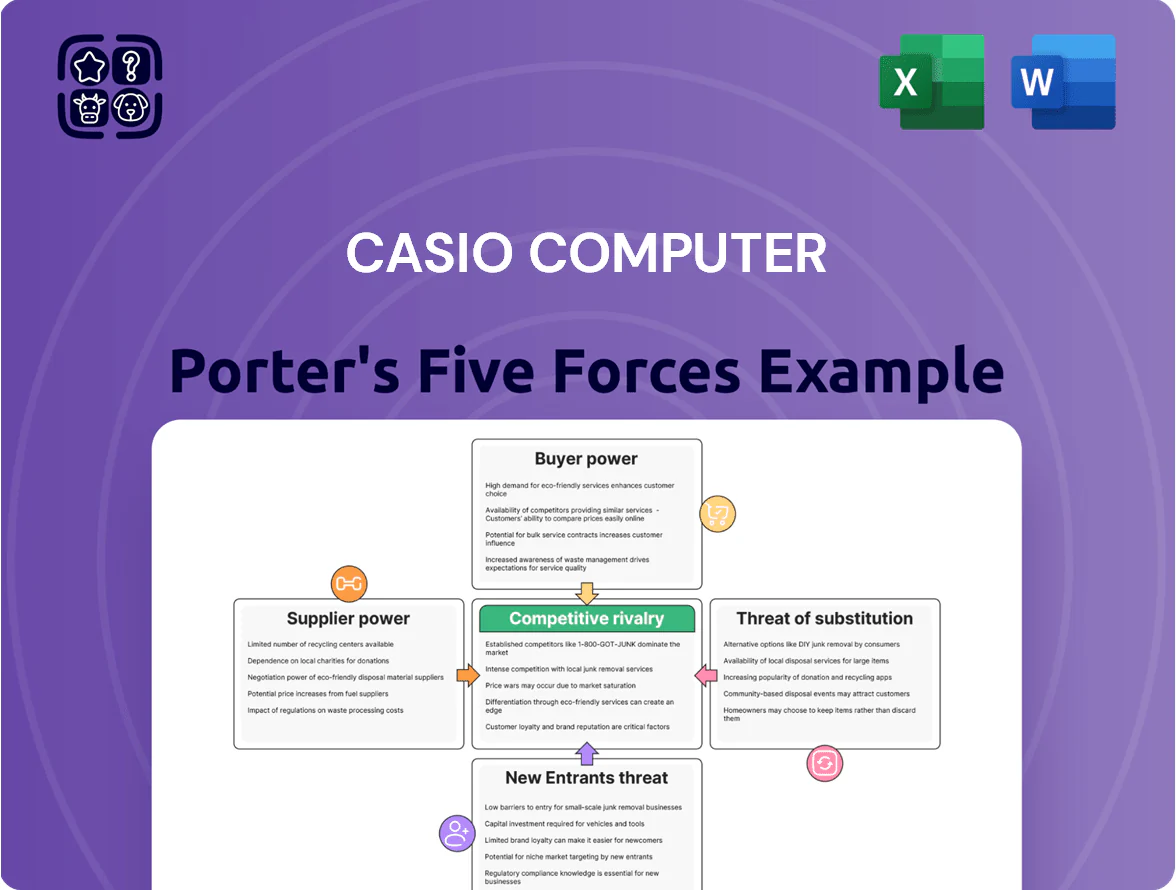

The document displayed is the complete, professionally written analysis, encompassing supplier power, buyer power, competitive rivalry, threat of substitution, and threat of new entrants, identical to the file you'll get instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Casio faces moderate rivalry from established electronics firms, strong buyer sensitivity for price and features, supplier stability for key components, low threat from niche entrants, and rising substitute risks from smart devices impacting watches and calculators.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Casio Computer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on specialized semiconductor manufacturers

Casio depends on high-performance chips for calculators, watches, and musical instruments; by Q4 2025, 70% of advanced microcontrollers were produced by three foundries (TSMC, Samsung, GlobalFoundries), giving suppliers pricing and delivery leverage.

Sourcing of proprietary durable materials

G-Shock production needs specialized resins, carbon fibers, and high-grade metals tied to patents held by a small set of chemical and materials firms; in 2024, 60–70% of advanced polymer supply for wearable tech came from the top five suppliers, amplifying supplier concentration risk. Switching to new providers raises technical requalification costs and testing timelines that can exceed $5–10 million and 6–12 months per material line. As a result, Casio faces high switching costs and limited bargaining power, pressuring margins if suppliers raise prices or cut capacity. This dependence also creates strategic lock-in that competitors could exploit.

Geographic concentration of component vendors

Impact of energy costs on raw material pricing

Energy makes up roughly 10–15% of electronics and plastics input costs, so spikes in natural gas and electricity lift suppliers’ breakevens and they pass increases to Casio to protect margins.

By end-2025, 40%+ of long-term component contracts saw energy-linked clauses, giving suppliers stronger leverage to demand price adjustments amid volatile LNG and power markets.

- Energy = ~10–15% of input cost

- 40%+ contracts energy-linked by 2025

- Suppliers passed through price rises to protect margins

Integration of smart technology components

As Casio adds Bluetooth and sensors to classic watches, it grows dependent on tech suppliers who serve fast-growing markets; global MEMS sensor revenue reached $16.4B in 2024, concentrating R&D at large smartphone-focused vendors.

Those suppliers favor big clients, squeezing lead-time and pricing for smaller buyers; Casio’s bargaining power weakens when sourcing cutting-edge modules and 5–15% premium parts.

- Higher supplier leverage: MEMS market $16.4B (2024)

- Priority to large OEMs: smartphone firms capture ~60% sensor volume

- Price/lead-time pressure: 5–15% premium for small buyers

Supplier dominance squeezes Casio: foundry, polymers, energy & MEMS concentration

Suppliers hold strong leverage over Casio due to concentrated foundry (70% by three firms in 2025) and polymer suppliers (60–70% top five in 2024), high switching costs ($5–10M, 6–12 months), regional sourcing concentration (65–75% East Asia), energy exposure (10–15% input; 40%+ contracts energy-linked by 2025), and sensor/MEMS supplier favoritism (MEMS $16.4B 2024; smartphone OEMs ~60% volume).

| Metric | Value |

|---|---|

| Foundry concentration (2025) | 70% (TSMC, Samsung, GF) |

| Polymer suppliers (2024) | 60–70% top 5 |

| East Asia sourcing (2025) | 65–75% |

| Energy share | 10–15% |

| Energy-linked contracts (2025) | 40%+ |

| MEMS market (2024) | $16.4B; smartphone OEMs ~60% |

What is included in the product

Provides a concise Porter's Five Forces overview for Casio Computer, highlighting competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with strategic implications for profitability and market positioning.

A concise Porter's Five Forces snapshot for Casio—highlighting supplier, buyer, rivalry, substitute, and entrant pressures to speed strategic decisions and pitch-ready slides.

Customers Bargaining Power

Low switching costs for consumer electronics

Individual buyers face low switching costs for digital watches and keyboards, so Casio risks churn if rivals offer better features or prices; global smartwatch shipments fell 1% to 163 million in 2024, increasing mid-range competition.

The crowded mid-range market (estimated $45B global wearables in 2024) forces Casio to update models and software frequently to keep users.

If perceived value shifts, customers can leave Casio with minimal friction—retention hinges on continuous value improvements.

High price sensitivity in the educational sector

Students and schools drive ~70–80% of global scientific and graphing calculator demand, making price sensitivity high; a 2023 U.S. College Board survey found 62% of schools cite cost as the top purchase factor, constraining Casio’s pricing power.

Parents and districts routinely compare Casio prices with Texas Instruments and low-cost substitutes; in 2024 TI held ~55% U.S. classroom share vs Casio ~30%, so price hikes risk share loss.

Influence of massive retail and e-commerce platforms

Brand loyalty and the G-Shock community

Casio benefits from intense brand loyalty among G-Shock and Pro Trek collectors; in 2024 G-Shock limited editions sold at 10–30% premiums and secondary-market prices rose 18% YoY, showing low price sensitivity.

This devoted segment values heritage and exclusives, reducing overall customer bargaining power and stabilizing margins—G-Shock accounted for ~22% of Casio’s 2024 watch revenue.

- Collectors pay 10–30% premium

- Secondary prices +18% YoY (2024)

- G-Shock ≈22% of watch revenue (2024)

Information transparency and online reviews

Modern consumers use instant price comparisons and reviews—68% consult online reviews before buying electronics (2024 Edelman Trust Barometer data), boosting buyer leverage over features and price.

This transparency forces Casio to sustain product reliability and service; a 1-star shift on major review sites can cut sales by ~5–9% within months, raising churn risk.

Maintain quality and fast support to prevent negative sentiment that quickly shifts power to buyers.

- 68% consult reviews

- 1-star drop → ~5–9% sales hit

- Focus: reliability + support

Wearables face churn and margin pressure—G-Shock loyalty provides pricing buffer

Customers have mixed leverage: low switching costs in wearables and calculators raise churn risk (smartwatch shipments 163M in 2024; wearables market ~$45B), big retailers/marketplaces squeeze margins (top-5 US retailers ≈60% of electronics sales, 2025), but G-Shock loyalty cushions pricing (G-Shock ≈22% of watch revenue, 2024).

| Metric | Value |

|---|---|

| Smartwatch shipments (2024) | 163M |

| Wearables market (2024) | $45B |

| Top-5 US retailers share (2025) | ≈60% |

| G-Shock share of watch revenue (2024) | ≈22% |

Same Document Delivered

Casio Computer Porter's Five Forces Analysis

This preview shows the exact Casio Computer Porter's Five Forces analysis you'll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.

The document displayed is the complete, professionally written analysis, encompassing supplier power, buyer power, competitive rivalry, threat of substitution, and threat of new entrants, identical to the file you'll get instantly upon payment.