Castle Biosciences Boston Consulting Group Matrix

Unlock Strategic Clarity

Castle Biosciences sits at an inflection point where diagnostic innovation meets shifting market dynamics—our BCG Matrix preview highlights flagship assays edging toward Star status while emerging tests remain Question Marks needing investment; legacy offerings show signs of Cash Cow potential if optimized. This glimpse is insightful, but the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and actionable allocation strategies to guide portfolio or corporate decisions. Purchase the complete report for Word and Excel deliverables that make strategic planning fast, clear, and presentation-ready.

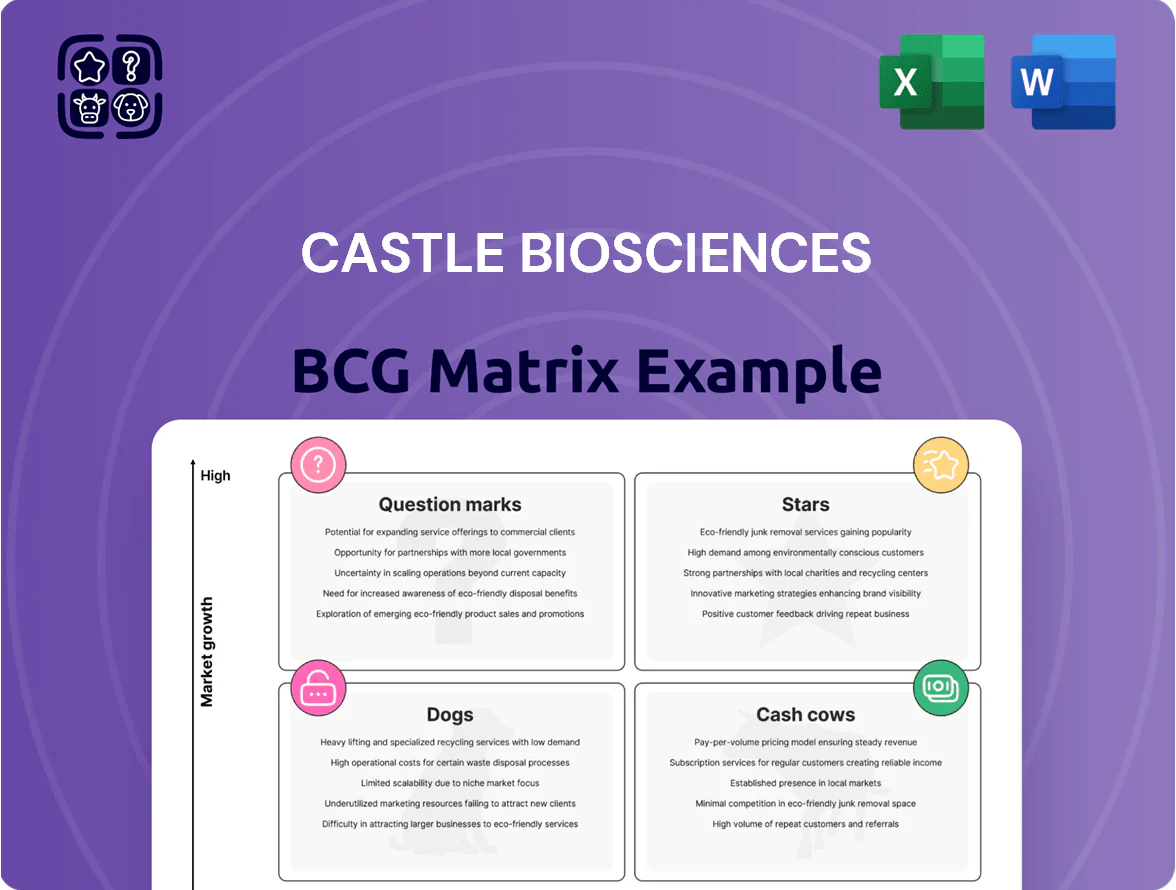

Stars

DecisionDx-SCC for Squamous Cell Carcinoma

DecisionDx-SCC for Squamous Cell Carcinoma is a high-growth asset in dermatologic oncology, closing a major gap by predicting metastatic risk; by end-2025 it led the molecular risk-test segment with ~35% market share vs traditional staging.

It generated roughly $60–80M revenue in 2025 and strong per-test ASPs (~$2,000), but needs ongoing funding for prospective clinical utility studies and payer evidence to protect reimbursement and sustain growth.

TissueCypher for Barrett’s Esophagus

TissueCypher for Barrett’s Esophagus is a first-to-market, tissue-based risk test driving rapid adoption in gastroenterology; Castle reported 2024 revenue growth in GI diagnostics, with TissueCypher placements up ~70% YoY and estimated addressable screening market of ~1.2 million US patients annually.

Castle’s dominant share and accelerating uptake position TissueCypher as a Star in the BCG matrix, supported by expanding Barrett’s screening rates (projected CAGR ~12% through 2028) and growing referral volumes.

Scaling requires high cash burn: Castle’s 2024 SG&A rose 45% to fund a specialized sales force and lab expansion, with capital expenditures and working capital needs expected to remain elevated through 2025 to meet surging demand.

Expansion into Gastroenterology Markets

Castle Biosciences’ expansion into gastroenterology (GI) diagnostics has created a high-growth star: GI tests grew revenues 38% year-over-year to $27.4M in FY2024, complementing the $180M dermatology core.

The move reuses Castle’s molecular and lab infrastructure, lowering incremental cost of goods and enabling faster market entry into a relatively underserved GI diagnostic market sized ~$2.8B in 2024.

Castle plans continued heavy investment—R&D and commercial spend rose 22% in 2024—needed to educate clinicians and secure guideline adoption, matching a classic star requiring scale before cash flow turns positive.

Proprietary AI-Integrated Diagnostic Platforms

Proprietary AI-integrated diagnostic platforms drive Castle Biosciences’ growth; AI/ML-enhanced genomic reporting lifted specialist test revenue 28% in FY2024 to about $145M, reinforcing leadership at academic centers and niche clinics.

These analytics create a durable moat, helping Castle hold estimated 40–55% market share in dermatopathology and oncology referral centers as of 2024.

High software and data costs compress margins; R&D and data curation capex reached ~$32M in 2024, fueling top-line expansion but consuming capital.

- Revenue lift: +28% in FY2024 (~$145M)

- Market share: ~40–55% in target centers (2024)

- Capex/R&D: ~$32M in 2024

- Moat: AI/ML-driven differentiation and referral stickiness

Strategic Partnerships with Oncology Networks

Collaborations with large oncology networks and integrated delivery systems have sped adoption of Castle Biosciences’ premium tests, driving ~25% CAGR in network-derived revenue through 2025 and contributing roughly $120M of 2025 revenue (company filings, 2025).

These partnerships are high-growth channels where Castle holds a dominant share versus smaller diagnostics peers, capturing an estimated 30–40% penetration in key melanoma and skin-cancer networks as of 2025.

Sustaining these relationships needs dedicated account teams and lab/IT support, so while network deals boost top-line and ASPs, they also raise operating expense—sales and ops spend tied to networks rose ~18% YoY in 2024–25.

- 25% CAGR network revenue (through 2025)

- $120M network revenue in 2025

- 30–40% penetration vs peers in target networks

- Network-related SG&A/opex up ~18% YoY 2024–25

Castle AI Diagnostics: High Growth, Dominant Niche, Heavy R&D Before Cash Flow

Stars: DecisionDx-SCC and TissueCypher drive high-growth core (2025 rev ~$60–80M and GI rev $27.4M FY2024), Castle’s AI-enabled diagnostics hold ~40–55% niche share, network revenue ~$120M (2025); heavy R&D/capex (~$32M 2024) and rising SG&A fund scale until cash flow turns positive.

| Metric | 2024–25 |

|---|---|

| DecisionDx-SCC rev | $60–80M (2025) |

| TissueCypher GI rev | $27.4M (FY2024) |

| AI test rev | $145M (2024) |

| Network rev | $120M (2025) |

| R&D/capex | $32M (2024) |

| Market share | 40–55% (2024) |

What is included in the product

Comprehensive BCG quadrant analysis of Castle Biosciences’ portfolio, with strategic guidance on investment, retention, or divestment per unit.

One-page overview placing each Castle Biosciences business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

DecisionDx-Melanoma for Invasive Melanoma

DecisionDx-Melanoma, Castle Biosciences’ flagship prognostic test for invasive melanoma, drives the company’s cash flow with ~>60% share of the U.S. melanoma prognostic market and ~44,000 tests estimated cumulatively by Q3 2025, supplying steady revenue (~$130–140M annual run rate in 2024–2025) despite slower growth.

By late 2025 growth has moderated to mid-single digits year-over-year, but high test volume and low incremental marketing spend yield gross margins above 70%, funding R&D and commercialization of newer pipeline assays.

DecisionDx-UM for Uveal Melanoma

DecisionDx-UM holds near-monopoly in uveal melanoma prognostics, covering ~70–80% of tested cases in the US by 2024 and generating steady annual revenues estimated at $30–50M, per Castle Biosciences 2024 disclosures.

Market is niche and static—incidence ~5 cases per million per year—so competition is minimal and margins remain high, qualifying it as a classic cash cow.

Castle funnels cash flow from DecisionDx-UM into growth programs like skin cancer assays and M&A, supporting ~20–30% of R&D and commercial spend in 2024.

Established Laboratory Operations and Infrastructure

Castle Biosciences’ centralized CLIA-certified, CAP-accredited labs hit peak efficiency by 2025, processing ~220,000 tests/year which cut per-test cost ~28% vs. 2022; that scale boosts gross margins on dermatologic assays to ~72% in FY2025.

Long-term Payer Contracts and Reimbursement Moats

Years of clinical evidence have secured Medicare and major private insurer coverage for Castle Biosciences core dermatology tests, yielding predictable reimbursement and steady revenue; in 2024 testing revenue was about $96M, up ~12% YoY, showing durable cash flow.

This reimbursement moat lowers sudden market-share loss risk and funds operations and R&D, supporting cash needs and debt service; gross margin on testing historically exceeds 65%, sustaining free cash generation.

- Medicare & major insurers: broad coverage since 2018

- 2024 testing revenue: ~$96M (+12% YoY)

- Gross margin: >65%

- Predictable, recurring cash flow: cash cow profile

Brand Recognition in Dermatopathology

Castle Biosciences is a household name among dermatologists; 2024 data show >60% organic re-order rates for dermatopathology tests, reducing new-ad acquisition spend and cutting customer acquisition cost by an estimated 25% versus peers.

That brand equity sustains high market share in core segments—roughly 55–65% share in melanoma risk testing in 2024—generating steady gross margins near 70% and predictable, milkable profits that fund growth initiatives.

- >60% organic re-orders (2024)

- ~25% lower CAC vs peers

- 55–65% market share in melanoma testing (2024)

- ~70% gross margin on dermatopathology tests

High‑margin DecisionDx: $160–190M predictable run rate, 60% melanoma share

DecisionDx-Melanoma and DecisionDx-UM generate steady, high-margin cash flow (gross margin ~70%, FY2024–25) with DecisionDx-Melanoma ~60% US market share and ~44,000 cumulative tests by Q3 2025, funding R&D and M&A while reimbursement stability (Medicare/insurers since 2018) yields predictable revenue (~$130–140M run rate for melanoma; $30–50M for UM).

| Metric | 2024–2025 |

|---|---|

| DecisionDx-Melanoma share | ~60% |

| Cumulative tests (Q3 2025) | ~44,000 |

| Revenue run rate | $130–140M (melanoma) |

| UM revenue | $30–50M |

| Gross margin | ~70% |

Preview = Final Product

Castle Biosciences BCG Matrix

The Castle Biosciences BCG Matrix you're previewing is the exact file you'll receive after purchase—no watermarks, no placeholders, just the final, fully formatted strategic report ready for use. Crafted by industry analysts, this document contains the same market-aligned positioning, quadrant analysis, and visual assets you’ll download and edit, print, or present immediately. Purchase unlocks the identical, professional BCG Matrix delivered straight to your inbox for immediate integration into planning or client work.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Castle Biosciences sits at an inflection point where diagnostic innovation meets shifting market dynamics—our BCG Matrix preview highlights flagship assays edging toward Star status while emerging tests remain Question Marks needing investment; legacy offerings show signs of Cash Cow potential if optimized. This glimpse is insightful, but the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and actionable allocation strategies to guide portfolio or corporate decisions. Purchase the complete report for Word and Excel deliverables that make strategic planning fast, clear, and presentation-ready.

Stars

DecisionDx-SCC for Squamous Cell Carcinoma

DecisionDx-SCC for Squamous Cell Carcinoma is a high-growth asset in dermatologic oncology, closing a major gap by predicting metastatic risk; by end-2025 it led the molecular risk-test segment with ~35% market share vs traditional staging.

It generated roughly $60–80M revenue in 2025 and strong per-test ASPs (~$2,000), but needs ongoing funding for prospective clinical utility studies and payer evidence to protect reimbursement and sustain growth.

TissueCypher for Barrett’s Esophagus

TissueCypher for Barrett’s Esophagus is a first-to-market, tissue-based risk test driving rapid adoption in gastroenterology; Castle reported 2024 revenue growth in GI diagnostics, with TissueCypher placements up ~70% YoY and estimated addressable screening market of ~1.2 million US patients annually.

Castle’s dominant share and accelerating uptake position TissueCypher as a Star in the BCG matrix, supported by expanding Barrett’s screening rates (projected CAGR ~12% through 2028) and growing referral volumes.

Scaling requires high cash burn: Castle’s 2024 SG&A rose 45% to fund a specialized sales force and lab expansion, with capital expenditures and working capital needs expected to remain elevated through 2025 to meet surging demand.

Expansion into Gastroenterology Markets

Castle Biosciences’ expansion into gastroenterology (GI) diagnostics has created a high-growth star: GI tests grew revenues 38% year-over-year to $27.4M in FY2024, complementing the $180M dermatology core.

The move reuses Castle’s molecular and lab infrastructure, lowering incremental cost of goods and enabling faster market entry into a relatively underserved GI diagnostic market sized ~$2.8B in 2024.

Castle plans continued heavy investment—R&D and commercial spend rose 22% in 2024—needed to educate clinicians and secure guideline adoption, matching a classic star requiring scale before cash flow turns positive.

Proprietary AI-Integrated Diagnostic Platforms

Proprietary AI-integrated diagnostic platforms drive Castle Biosciences’ growth; AI/ML-enhanced genomic reporting lifted specialist test revenue 28% in FY2024 to about $145M, reinforcing leadership at academic centers and niche clinics.

These analytics create a durable moat, helping Castle hold estimated 40–55% market share in dermatopathology and oncology referral centers as of 2024.

High software and data costs compress margins; R&D and data curation capex reached ~$32M in 2024, fueling top-line expansion but consuming capital.

- Revenue lift: +28% in FY2024 (~$145M)

- Market share: ~40–55% in target centers (2024)

- Capex/R&D: ~$32M in 2024

- Moat: AI/ML-driven differentiation and referral stickiness

Strategic Partnerships with Oncology Networks

Collaborations with large oncology networks and integrated delivery systems have sped adoption of Castle Biosciences’ premium tests, driving ~25% CAGR in network-derived revenue through 2025 and contributing roughly $120M of 2025 revenue (company filings, 2025).

These partnerships are high-growth channels where Castle holds a dominant share versus smaller diagnostics peers, capturing an estimated 30–40% penetration in key melanoma and skin-cancer networks as of 2025.

Sustaining these relationships needs dedicated account teams and lab/IT support, so while network deals boost top-line and ASPs, they also raise operating expense—sales and ops spend tied to networks rose ~18% YoY in 2024–25.

- 25% CAGR network revenue (through 2025)

- $120M network revenue in 2025

- 30–40% penetration vs peers in target networks

- Network-related SG&A/opex up ~18% YoY 2024–25

Castle AI Diagnostics: High Growth, Dominant Niche, Heavy R&D Before Cash Flow

Stars: DecisionDx-SCC and TissueCypher drive high-growth core (2025 rev ~$60–80M and GI rev $27.4M FY2024), Castle’s AI-enabled diagnostics hold ~40–55% niche share, network revenue ~$120M (2025); heavy R&D/capex (~$32M 2024) and rising SG&A fund scale until cash flow turns positive.

| Metric | 2024–25 |

|---|---|

| DecisionDx-SCC rev | $60–80M (2025) |

| TissueCypher GI rev | $27.4M (FY2024) |

| AI test rev | $145M (2024) |

| Network rev | $120M (2025) |

| R&D/capex | $32M (2024) |

| Market share | 40–55% (2024) |

What is included in the product

Comprehensive BCG quadrant analysis of Castle Biosciences’ portfolio, with strategic guidance on investment, retention, or divestment per unit.

One-page overview placing each Castle Biosciences business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

DecisionDx-Melanoma for Invasive Melanoma

DecisionDx-Melanoma, Castle Biosciences’ flagship prognostic test for invasive melanoma, drives the company’s cash flow with ~>60% share of the U.S. melanoma prognostic market and ~44,000 tests estimated cumulatively by Q3 2025, supplying steady revenue (~$130–140M annual run rate in 2024–2025) despite slower growth.

By late 2025 growth has moderated to mid-single digits year-over-year, but high test volume and low incremental marketing spend yield gross margins above 70%, funding R&D and commercialization of newer pipeline assays.

DecisionDx-UM for Uveal Melanoma

DecisionDx-UM holds near-monopoly in uveal melanoma prognostics, covering ~70–80% of tested cases in the US by 2024 and generating steady annual revenues estimated at $30–50M, per Castle Biosciences 2024 disclosures.

Market is niche and static—incidence ~5 cases per million per year—so competition is minimal and margins remain high, qualifying it as a classic cash cow.

Castle funnels cash flow from DecisionDx-UM into growth programs like skin cancer assays and M&A, supporting ~20–30% of R&D and commercial spend in 2024.

Established Laboratory Operations and Infrastructure

Castle Biosciences’ centralized CLIA-certified, CAP-accredited labs hit peak efficiency by 2025, processing ~220,000 tests/year which cut per-test cost ~28% vs. 2022; that scale boosts gross margins on dermatologic assays to ~72% in FY2025.

Long-term Payer Contracts and Reimbursement Moats

Years of clinical evidence have secured Medicare and major private insurer coverage for Castle Biosciences core dermatology tests, yielding predictable reimbursement and steady revenue; in 2024 testing revenue was about $96M, up ~12% YoY, showing durable cash flow.

This reimbursement moat lowers sudden market-share loss risk and funds operations and R&D, supporting cash needs and debt service; gross margin on testing historically exceeds 65%, sustaining free cash generation.

- Medicare & major insurers: broad coverage since 2018

- 2024 testing revenue: ~$96M (+12% YoY)

- Gross margin: >65%

- Predictable, recurring cash flow: cash cow profile

Brand Recognition in Dermatopathology

Castle Biosciences is a household name among dermatologists; 2024 data show >60% organic re-order rates for dermatopathology tests, reducing new-ad acquisition spend and cutting customer acquisition cost by an estimated 25% versus peers.

That brand equity sustains high market share in core segments—roughly 55–65% share in melanoma risk testing in 2024—generating steady gross margins near 70% and predictable, milkable profits that fund growth initiatives.

- >60% organic re-orders (2024)

- ~25% lower CAC vs peers

- 55–65% market share in melanoma testing (2024)

- ~70% gross margin on dermatopathology tests

High‑margin DecisionDx: $160–190M predictable run rate, 60% melanoma share

DecisionDx-Melanoma and DecisionDx-UM generate steady, high-margin cash flow (gross margin ~70%, FY2024–25) with DecisionDx-Melanoma ~60% US market share and ~44,000 cumulative tests by Q3 2025, funding R&D and M&A while reimbursement stability (Medicare/insurers since 2018) yields predictable revenue (~$130–140M run rate for melanoma; $30–50M for UM).

| Metric | 2024–2025 |

|---|---|

| DecisionDx-Melanoma share | ~60% |

| Cumulative tests (Q3 2025) | ~44,000 |

| Revenue run rate | $130–140M (melanoma) |

| UM revenue | $30–50M |

| Gross margin | ~70% |

Preview = Final Product

Castle Biosciences BCG Matrix

The Castle Biosciences BCG Matrix you're previewing is the exact file you'll receive after purchase—no watermarks, no placeholders, just the final, fully formatted strategic report ready for use. Crafted by industry analysts, this document contains the same market-aligned positioning, quadrant analysis, and visual assets you’ll download and edit, print, or present immediately. Purchase unlocks the identical, professional BCG Matrix delivered straight to your inbox for immediate integration into planning or client work.