Castle Biosciences PESTLE Analysis

Skip the Research. Get the Strategy.

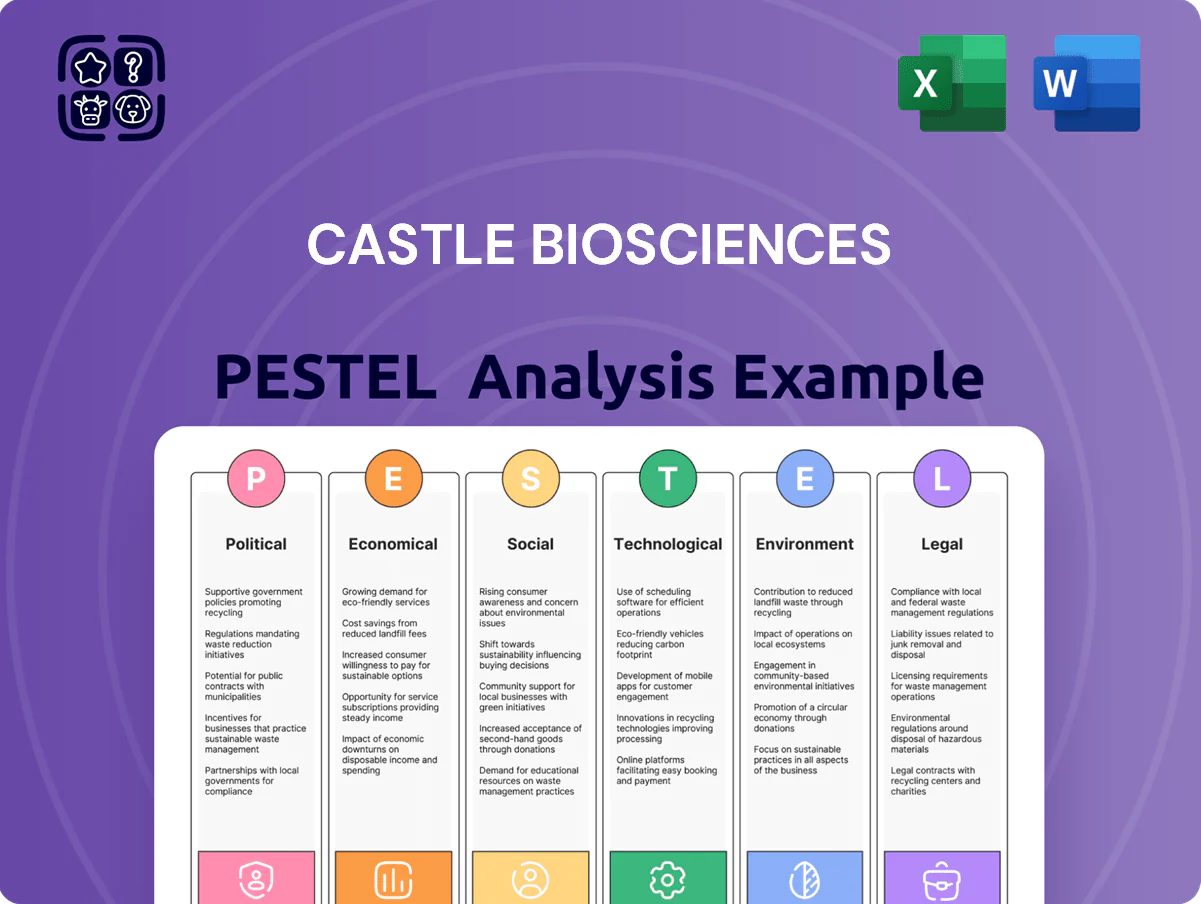

Discover how political, economic, social, technological, legal, and environmental forces are shaping Castle Biosciences’ trajectory—our concise PESTLE snapshot highlights key risks and opportunities to inform your strategy. Buy the full analysis for a detailed, actionable report with editable charts and scenario-ready insights tailored for investors, advisors, and executives.

Political factors

Medicare Reimbursement Policy

Medicare reimbursement policies heavily affect Castle Biosciences, given ~61% of melanoma and skin cancer diagnoses occur in patients 65+; Medicare covers a substantial share of DecisionDx-SCC billing, so CMS and MAC Local Coverage Determinations can materially sway revenue stability for FY2024–2025. In 2024 Castle reported 2023 revenue of $161.6M with Medicare exposure risk concentrated in older cohorts, making evidence-based advocacy and political engagement essential to preserve federal coverage for genomic tests.

FDA Regulatory Oversight of LDTs

The political push for FDA oversight of LDTs has produced draft and final guidance through 2024–2025, requiring Castle Biosciences to align certain tests with medical device classifications and premarket pathways, increasing compliance costs estimated industry-wide at 10–15% of revenue for affected firms.

Government Healthcare Spending Levels

Federal budget allocations for cancer research—notably the NIH cancer portfolio which received about $8.5 billion in FY2024—directly affect Castle Biosciences by shaping grant availability and translational research funding.

Shifts in political priorities for national healthcare spending influence clinical adoption rates for high-end diagnostics; increased emphasis on personalized medicine (CMS coverage expansions in 2023–24) benefits genomic testing providers.

Reduced government spending or reallocations could tighten reimbursement pathways and slow market growth, while continued federal support for precision oncology offers a clear tailwind for Castle’s products.

State-Level Healthcare Mandates

State-level mandates shape access to Castle Biosciences genomic tests: 20 states had specific cancer screening or genetic testing directives by 2024, affecting reimbursement and utilization.

Medicaid expansion status (39 states + DC expanded by 2024) creates a patchwork of coverage, requiring tailored market access strategies across jurisdictions.

Active state advocacy is critical to secure inclusion of genomic assays in standard care and insurer formularies; legislative wins correlate with faster adoption and higher reimbursement rates.

- 20 states with screening/genetic directives (2024)

- 39 states + DC Medicaid expansion (2024)

- State advocacy boosts coverage and reimbursement

International Trade and Expansion Policies

As Castle Biosciences pursues international expansion, US trade relations and agreements matter—US goods exports faced 2.4% growth in 2024, but tariffs on lab equipment (up to 10–25% in some markets) and export controls on genomic technologies can raise COGS and delay market entry.

Cross-border genomic data transfer faces tightening rules (EU GDPR fines up to 4% of global turnover); political instability in target markets increases IP risk and can affect projected revenue streams.

- Tariff exposure: 10–25% on lab equipment in select markets

- Regulatory risk: GDPR fines up to 4% of global turnover

- Trade growth context: US exports +2.4% in 2024

- Strategic need: assess political stability and IP enforcement before entry

Medicare, FDA LDT costs, and NIH funding to steer Castle's 2024–25 outlook

Medicare reimbursement risk is material—~61% of melanoma cases are 65+ and Castle reported $161.6M revenue (2023), making CMS/LCDs pivotal for FY2024–25; FDA LDT oversight raised compliance costs ~10–15% industry-wide; NIH cancer funding ~$8.5B (FY2024) supports translational pipelines; 39 states+DC expanded Medicaid (2024) and 20 states had genetic directives, affecting access.

| Metric | Value (2023/2024) |

|---|---|

| Castle Revenue | $161.6M (2023) |

| Medicare exposure | ~61% melanoma in 65+ |

| NIH cancer funding | $8.5B (FY2024) |

| Medicaid expansion | 39 states + DC (2024) |

What is included in the product

Explores how macro-environmental forces uniquely impact Castle Biosciences across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current industry data and trends.

A concise Castle Biosciences PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Healthcare Cost Containment Pressures

Broad efforts to cut US healthcare spending—which reached about 19.7% of GDP ($5.1 trillion) in 2023—pressure pricing for Castle Biosciences’ premium diagnostics, as payers push back on higher per-test costs. Insurers increasingly demand clinical utility data; Medicare/Medicaid coverage decisions hinge on demonstrated downstream savings from avoided surgeries or treatments. Castle must show tests like DecisionDx-UM and DecisionDx-Melanoma produce net system savings—e.g., reduced unnecessary procedures or follow-up costs—to secure reimbursement and sustain revenue growth.

Inflationary Impact on Laboratory Supplies

Persistent inflation through 2025 raised costs for chemical reagents, consumables and equipment maintenance by an estimated 8–12% year-over-year, increasing Castle Biosciences' per-test input costs and pressuring gross margins reported at ~60% in 2024.

If Castle cannot pass these higher costs to payers or improve throughput, operating margins (around 18% in 2024) may compress further; achieving 3–5% efficiency gains could offset a large portion of the impact.

Active supply-chain management—long-term vendor contracts, bulk purchasing and dual-sourcing—has material value: industry data show multi-year contracts can lock prices and reduce input volatility by roughly 30–40% versus spot buys.

Capital Market Access and Interest Rates

As of late 2025, the US federal funds rate at about 5.25–5.50% raises Castle Biosciences' cost of capital, making debt-funded R&D and acquisitions more expensive; higher borrowing costs can extend payback periods for long clinical trials. Elevated rates compress biotech valuations—Q4 2025 median EV/Revenue for small-cap biotech hovered near 6x—reducing investor appetite and tightening Castle's liquidity and secondary financing options.

Consumer Disposable Income Trends

Economic weakness reduces discretionary healthcare spending; U.S. consumer disposable personal income fell 1.3% QoQ in Q4 2023 annualized, and higher deductibles (median individual deductible ~$1,500 in 2024) can push patients to defer non-urgent dermatologic tests like Castle Biosciences’ diagnostics.

During downturns dermatology visit volumes drop—Medicare Advantage data showed ~5–8% fewer outpatient dermatology visits in 2023 vs 2022—lowering diagnostic orders tied to non-emergency skin conditions.

Reduced visit volume and higher out-of-pocket exposure can compress Castle’s addressable test uptake and revenue sensitivity to macroeconomic cycles.

- Disposable income dip (Q4 2023 −1.3% QoQ) pressures out-of-pocket capacity

- Median deductible ~$1,500 (2024) increases patient cost-share

- Dermatology visits down ~5–8% in 2023 → fewer diagnostic orders

- Revenue and test volume sensitive to consumer economic health

Insurance Payer Mix Volatility

The balance between commercial insurance, Medicare, and self-pay creates revenue variability for Castle Biosciences; in 2024 roughly 45% of US adults had employer coverage while Medicare covered about 17% of the population, affecting reimbursement mixes for genomic tests.

Rising unemployment in 2023–2024 shifted some patients from private to public coverage, where Medicare reimbursement rates for molecular diagnostics are often lower, pressuring margins.

Castle must adapt billing, prior authorization, and collections; in 2024 the company reported payer-denied rates around industry averages near 10–15%, underscoring the need for dynamic revenue cycle management.

- Mix volatility: commercial ~45%, Medicare ~17% (2024)

- Unemployment-driven shifts altered payer mix 2023–2024

- Medicare reimbursement typically lower than commercial for genomic tests

- Payer-denial rates ~10–15% (industry 2024)

Castle faces margin squeeze: inflation, reimbursement and tighter biotech financing

Healthcare spending ~19.7% GDP ($5.1T, 2023) pressures pricing; Castle needs clinical utility to secure reimbursement. Inflation raised per-test inputs ~8–12% through 2025, squeezing gross margin ~60% (2024) and operating margin ~18% (2024). Fed funds ~5.25–5.50% (late 2025) raises cost of capital; Q4 2025 median small-cap biotech EV/Rev ~6x, tightening financing.

| Metric | Value |

|---|---|

| US healthcare %GDP (2023) | 19.7% ($5.1T) |

| Castle gross margin (2024) | ~60% |

| Operating margin (2024) | ~18% |

| Input cost inflation | 8–12% YoY |

| Fed funds (late 2025) | 5.25–5.50% |

| Small-cap biotech EV/Rev (Q4 2025) | ~6x |

What You See Is What You Get

Castle Biosciences PESTLE Analysis

The preview shown here is the exact Castle Biosciences PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Castle Biosciences’ trajectory—our concise PESTLE snapshot highlights key risks and opportunities to inform your strategy. Buy the full analysis for a detailed, actionable report with editable charts and scenario-ready insights tailored for investors, advisors, and executives.

Political factors

Medicare Reimbursement Policy

Medicare reimbursement policies heavily affect Castle Biosciences, given ~61% of melanoma and skin cancer diagnoses occur in patients 65+; Medicare covers a substantial share of DecisionDx-SCC billing, so CMS and MAC Local Coverage Determinations can materially sway revenue stability for FY2024–2025. In 2024 Castle reported 2023 revenue of $161.6M with Medicare exposure risk concentrated in older cohorts, making evidence-based advocacy and political engagement essential to preserve federal coverage for genomic tests.

FDA Regulatory Oversight of LDTs

The political push for FDA oversight of LDTs has produced draft and final guidance through 2024–2025, requiring Castle Biosciences to align certain tests with medical device classifications and premarket pathways, increasing compliance costs estimated industry-wide at 10–15% of revenue for affected firms.

Government Healthcare Spending Levels

Federal budget allocations for cancer research—notably the NIH cancer portfolio which received about $8.5 billion in FY2024—directly affect Castle Biosciences by shaping grant availability and translational research funding.

Shifts in political priorities for national healthcare spending influence clinical adoption rates for high-end diagnostics; increased emphasis on personalized medicine (CMS coverage expansions in 2023–24) benefits genomic testing providers.

Reduced government spending or reallocations could tighten reimbursement pathways and slow market growth, while continued federal support for precision oncology offers a clear tailwind for Castle’s products.

State-Level Healthcare Mandates

State-level mandates shape access to Castle Biosciences genomic tests: 20 states had specific cancer screening or genetic testing directives by 2024, affecting reimbursement and utilization.

Medicaid expansion status (39 states + DC expanded by 2024) creates a patchwork of coverage, requiring tailored market access strategies across jurisdictions.

Active state advocacy is critical to secure inclusion of genomic assays in standard care and insurer formularies; legislative wins correlate with faster adoption and higher reimbursement rates.

- 20 states with screening/genetic directives (2024)

- 39 states + DC Medicaid expansion (2024)

- State advocacy boosts coverage and reimbursement

International Trade and Expansion Policies

As Castle Biosciences pursues international expansion, US trade relations and agreements matter—US goods exports faced 2.4% growth in 2024, but tariffs on lab equipment (up to 10–25% in some markets) and export controls on genomic technologies can raise COGS and delay market entry.

Cross-border genomic data transfer faces tightening rules (EU GDPR fines up to 4% of global turnover); political instability in target markets increases IP risk and can affect projected revenue streams.

- Tariff exposure: 10–25% on lab equipment in select markets

- Regulatory risk: GDPR fines up to 4% of global turnover

- Trade growth context: US exports +2.4% in 2024

- Strategic need: assess political stability and IP enforcement before entry

Medicare, FDA LDT costs, and NIH funding to steer Castle's 2024–25 outlook

Medicare reimbursement risk is material—~61% of melanoma cases are 65+ and Castle reported $161.6M revenue (2023), making CMS/LCDs pivotal for FY2024–25; FDA LDT oversight raised compliance costs ~10–15% industry-wide; NIH cancer funding ~$8.5B (FY2024) supports translational pipelines; 39 states+DC expanded Medicaid (2024) and 20 states had genetic directives, affecting access.

| Metric | Value (2023/2024) |

|---|---|

| Castle Revenue | $161.6M (2023) |

| Medicare exposure | ~61% melanoma in 65+ |

| NIH cancer funding | $8.5B (FY2024) |

| Medicaid expansion | 39 states + DC (2024) |

What is included in the product

Explores how macro-environmental forces uniquely impact Castle Biosciences across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current industry data and trends.

A concise Castle Biosciences PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Healthcare Cost Containment Pressures

Broad efforts to cut US healthcare spending—which reached about 19.7% of GDP ($5.1 trillion) in 2023—pressure pricing for Castle Biosciences’ premium diagnostics, as payers push back on higher per-test costs. Insurers increasingly demand clinical utility data; Medicare/Medicaid coverage decisions hinge on demonstrated downstream savings from avoided surgeries or treatments. Castle must show tests like DecisionDx-UM and DecisionDx-Melanoma produce net system savings—e.g., reduced unnecessary procedures or follow-up costs—to secure reimbursement and sustain revenue growth.

Inflationary Impact on Laboratory Supplies

Persistent inflation through 2025 raised costs for chemical reagents, consumables and equipment maintenance by an estimated 8–12% year-over-year, increasing Castle Biosciences' per-test input costs and pressuring gross margins reported at ~60% in 2024.

If Castle cannot pass these higher costs to payers or improve throughput, operating margins (around 18% in 2024) may compress further; achieving 3–5% efficiency gains could offset a large portion of the impact.

Active supply-chain management—long-term vendor contracts, bulk purchasing and dual-sourcing—has material value: industry data show multi-year contracts can lock prices and reduce input volatility by roughly 30–40% versus spot buys.

Capital Market Access and Interest Rates

As of late 2025, the US federal funds rate at about 5.25–5.50% raises Castle Biosciences' cost of capital, making debt-funded R&D and acquisitions more expensive; higher borrowing costs can extend payback periods for long clinical trials. Elevated rates compress biotech valuations—Q4 2025 median EV/Revenue for small-cap biotech hovered near 6x—reducing investor appetite and tightening Castle's liquidity and secondary financing options.

Consumer Disposable Income Trends

Economic weakness reduces discretionary healthcare spending; U.S. consumer disposable personal income fell 1.3% QoQ in Q4 2023 annualized, and higher deductibles (median individual deductible ~$1,500 in 2024) can push patients to defer non-urgent dermatologic tests like Castle Biosciences’ diagnostics.

During downturns dermatology visit volumes drop—Medicare Advantage data showed ~5–8% fewer outpatient dermatology visits in 2023 vs 2022—lowering diagnostic orders tied to non-emergency skin conditions.

Reduced visit volume and higher out-of-pocket exposure can compress Castle’s addressable test uptake and revenue sensitivity to macroeconomic cycles.

- Disposable income dip (Q4 2023 −1.3% QoQ) pressures out-of-pocket capacity

- Median deductible ~$1,500 (2024) increases patient cost-share

- Dermatology visits down ~5–8% in 2023 → fewer diagnostic orders

- Revenue and test volume sensitive to consumer economic health

Insurance Payer Mix Volatility

The balance between commercial insurance, Medicare, and self-pay creates revenue variability for Castle Biosciences; in 2024 roughly 45% of US adults had employer coverage while Medicare covered about 17% of the population, affecting reimbursement mixes for genomic tests.

Rising unemployment in 2023–2024 shifted some patients from private to public coverage, where Medicare reimbursement rates for molecular diagnostics are often lower, pressuring margins.

Castle must adapt billing, prior authorization, and collections; in 2024 the company reported payer-denied rates around industry averages near 10–15%, underscoring the need for dynamic revenue cycle management.

- Mix volatility: commercial ~45%, Medicare ~17% (2024)

- Unemployment-driven shifts altered payer mix 2023–2024

- Medicare reimbursement typically lower than commercial for genomic tests

- Payer-denial rates ~10–15% (industry 2024)

Castle faces margin squeeze: inflation, reimbursement and tighter biotech financing

Healthcare spending ~19.7% GDP ($5.1T, 2023) pressures pricing; Castle needs clinical utility to secure reimbursement. Inflation raised per-test inputs ~8–12% through 2025, squeezing gross margin ~60% (2024) and operating margin ~18% (2024). Fed funds ~5.25–5.50% (late 2025) raises cost of capital; Q4 2025 median small-cap biotech EV/Rev ~6x, tightening financing.

| Metric | Value |

|---|---|

| US healthcare %GDP (2023) | 19.7% ($5.1T) |

| Castle gross margin (2024) | ~60% |

| Operating margin (2024) | ~18% |

| Input cost inflation | 8–12% YoY |

| Fed funds (late 2025) | 5.25–5.50% |

| Small-cap biotech EV/Rev (Q4 2025) | ~6x |

What You See Is What You Get

Castle Biosciences PESTLE Analysis

The preview shown here is the exact Castle Biosciences PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.