Contemporary Amperex Technology Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

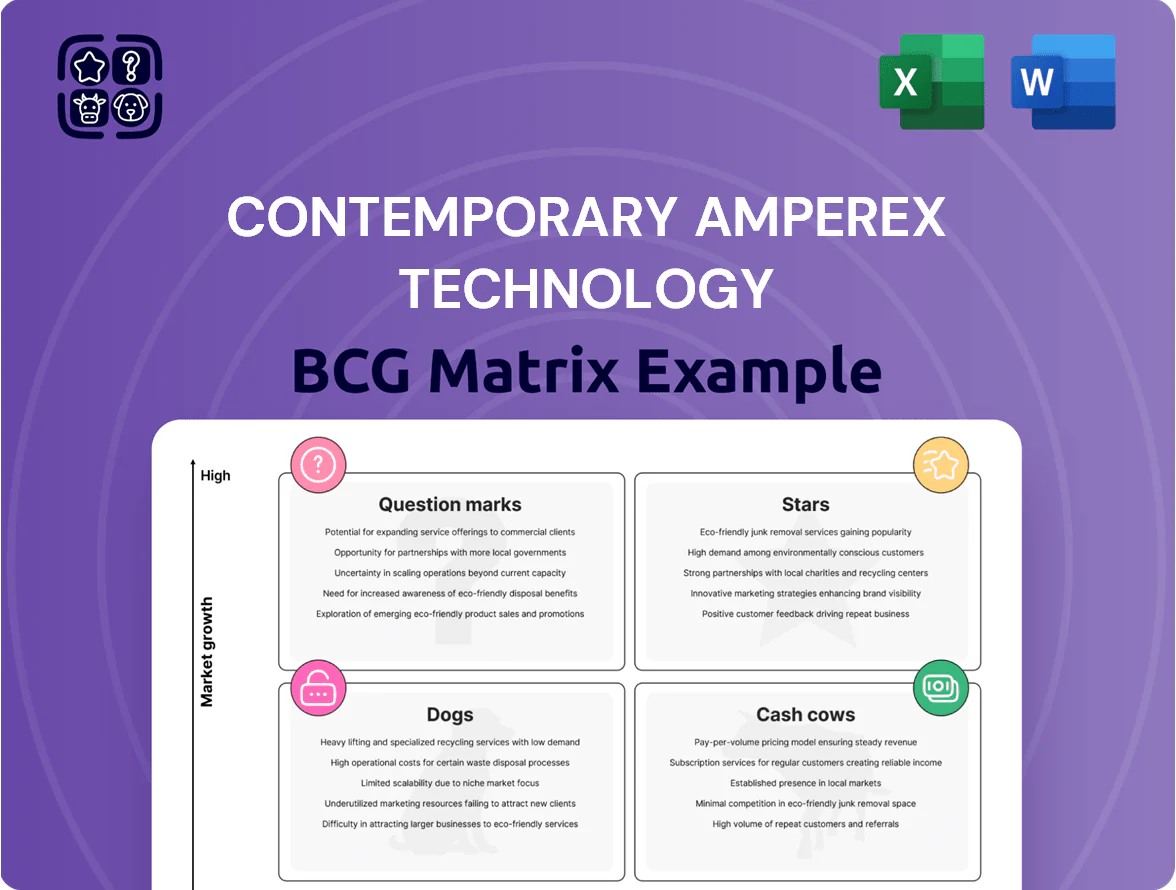

Contemporary Amperex Technology's brief BCG Matrix preview shows a company balancing high-growth battery segments that could be Stars with mature, high-share lines acting as Cash Cows, while emerging tech areas remain Question Marks needing capital allocation; a few low-performing units risk becoming Dogs without strategic shifts. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

LFP Battery Systems for Global Mass Markets

CATL (Contemporary Amperex Technology Co., Ltd.) leads global LFP (lithium iron phosphate) batteries with ~40%+ market share in LFP cells by capacity in 2025, keeping LFP the low-cost choice for mass-market EVs.

Through late 2025 LFP demand rose ~18% YoY in Europe/North America as affordable EVs expanded; scaling LFP needs heavy CAPEX—CATL reported RMB 120–150 billion planned 2024–26 capex for cell expansion.

High-volume supply contracts drive revenue: CATL’s 2025 battery sales reached RMB 230 billion, with LFP a core contributor, making this segment a principal growth engine toward full electrification.

Energy Storage Systems Industrial Division

The utility-scale energy storage segment is a high-growth leader as grids shift to renewables; global installed battery storage capacity grew 85% in 2024 to about 32 GW/176 GWh, and CATL (Contemporary Amperex Technology Co., Ltd.) captured roughly 30–35% of utility-scale orders with liquid-cooling systems that boost safety and cycle life.

Heavy R&D and capex are required—CATL’s 2024 R&D spend was RMB 35.8 billion (about US$5.2 billion)—but rapid market expansion (BloombergNEF forecasts 2030 cumulative deployments >400 GW/2,500 GWh) makes this division a cornerstone of CATL’s valuation.

Synergy between cell manufacturing and grid management lets CATL offer integrated solutions and service contracts, improving gross margins; utility-storage contributed an estimated mid-teens percentage of CATL’s 2024 revenue, positioning the unit as a BCG Matrix star.

Shenxing Superfast Charging Batteries

Shenxing Superfast Charging Batteries, CATL’s fast-charging LFP line, cuts charge to 80% in ~10–15 minutes and adds ~200 km in 10 minutes, addressing EV range anxiety and driving rapid adoption by premium and mid-range OEMs; shipments rose ~220% YoY to ~3 GWh in 2024.

CATL spent ~RMB 4.2bn on marketing and placement in 2024 to secure design wins, keeping its first-to-market edge and pushing Shenxing toward scale economics.

Market forecasts from SNE Research estimate Shenxing could reach ~25–30 GWh annual demand by 2027, shifting the line from growth to major cash generator as fast-charge LFP becomes standard.

European Manufacturing Hubs

CATL’s European manufacturing hubs in Hungary and Germany are a high-growth Stars move, targeting >€20bn EU battery demand projected by 2030 and enabling direct supply to VW, BMW, and Stellantis while avoiding tariffs and cutting logistics by ~20%.

These plants tie up substantial capex—€2–4bn per gigafactory and >€500m annual opex early—but are vital to secure >30% market share outside China and preserve CATL’s global leadership.

- Targets EU demand >€20bn by 2030

- Capex ≈€2–4bn per gigafactory

- Logistics cuts ~20%

- Goal: >30% non-China market share

Qilin Battery Technology

Qilin Battery Technology, CATL’s flagship high-end ternary cell, delivers record volume energy density (~300 Wh/L in 2025 tests) and superior cooling, aimed at luxury EVs where performance beats cost.

It holds ≈40% share of the premium EV battery segment in 2024 and saw unit sales growth ~28% YoY as luxury brands shift to dedicated EV platforms.

High R and D spend (~¥6.5B in 2024) is offset by premium pricing and strategic brand value, supporting margin resilience.

- ~300 Wh/L volume energy density (2025)

- ~40% premium-segment share (2024)

- 28% unit growth YoY (2024→2025)

- ¥6.5B R and D spend (2024)

CATL’s growth surge: LFP, Shenxing, Qilin push 2025 sales to RMB230bn

CATL’s Stars—LFP cells, utility storage, Shenxing fast-charge, Qilin premium—drive high growth and share: 2025 LFP ≈40% global capacity; 2025 sales RMB230bn; 2024 R&D RMB35.8bn; Shenxing 2024 shipments ~3GWh (↑220%); utility storage share 30–35%; Qilin ~40% premium share.

| Unit | Key 2024–25 |

|---|---|

| LFP share | ~40% |

| Sales | RMB230bn (2025) |

| R&D | RMB35.8bn (2024) |

| Shenxing | ~3GWh (2024) |

What is included in the product

Comprehensive BCG Matrix for Contemporary Amperex: quadrant-by-quadrant insights, investment recommendations, and trend-driven risks/opportunities.

One-page BCG Matrix placing CATL's business units in quadrants for quick strategic clarity and decision-making.

Cash Cows

Domestic Chinese Passenger EV Market

The domestic Chinese passenger EV battery market is mature and CATL (Contemporary Amperex Technology Co., Limited) holds ~55–60% market share in 2025, giving it a commanding, stable lead.

Annual segment growth slowed to ~8–12% in 2024–25 from 30%+ in early 2020s, letting CATL cut unit costs (cell-level costs down ~12% YoY) and boost gross margins.

This cash-generating core funded R&D and overseas deals—CATL reported RMB 98.6 billion cash and equivalents at end-2024—supporting next-gen battery and international expansion.

Standard NCM Battery Cell Production

Nickel Cobalt Manganese (NCM) cell tech is mature with global NCM battery shipments ~120 GWh in 2024, and CATL supplied roughly 20–25% of that to long-range EV makers, backing steady demand.

Development costs are largely recouped, enabling gross margins ~20–28% on standard NCM cells in 2024, so minimal new marketing spend is needed.

CATL milks this cash cow by delivering reliable, high-quality NCM cells to long-term partners, generating predictable operating cash flow that funded ~CNY 15–20 billion of R&D and investments into Question Marks in 2024.

Supply Chain and Mineral Resource Investments

CATL’s strategic stakes in lithium, cobalt, and nickel mines give it vertical integration that cut raw-material costs; by 2024 CATL sourced ~28% of battery-grade lithium internally, lowering COGS and supporting gross margins near 25% in 2024.

Battery Management Systems Software

CATL’s proprietary Battery Management Systems (BMS) software is a high-margin, low-capex cash cow, adding roughly 8–12% margin uplift per pack and contributing an estimated RMB 10–15 billion in operating cash flow in 2024 tied to global battery sales.

As a mature product with negligible incremental cost, BMS is embedded across ~95% of CATL’s packs, securing steady revenue and reinforcing pricing power and market share through software-driven differentiation.

- High margin: +8–12% per pack

- 2024 cash flow: RMB 10–15 billion (est.)

- Integration: ~95% of CATL packs

- Low incremental cost, low capex

Global After-sales and Maintenance Services

As CATL-powered vehicles age globally, certified maintenance, diagnostics, and spare parts form a stable service market—estimated at $3.2 billion in 2025 after 18% CAGR since 2020—and this unit holds a dominant share of the installed base, driving predictable demand.

The service network needs low growth investment, yields high-margin recurring revenue (roughly 12–15% EBIT contribution in 2024), and boosts brand loyalty, acting as a cash cow that stabilizes CATL’s cash flow.

- Market size ~$3.2B (2025)

- 18% CAGR since 2020

- EBIT contribution ~12–15% (2024)

- Low capex, recurring revenue

CATL cash cows: NCM + BMS fuel dominant China EV margins and strong cash flow

CATL’s domestic NCM cells and embedded BMS are cash cows: ~55–60% China EV battery share (2025), NCM shipments ~120 GWh (2024) with CATL ~20–25%, gross margins ~20–28% on NCM, BMS adds +8–12% margin and ~RMB10–15bn cash flow (2024), service market ~$3.2bn (2025) with ~12–15% EBIT (2024).

| Metric | Value |

|---|---|

| China share (2025) | 55–60% |

| NCM global (2024) | ~120 GWh |

| BMS cash (2024) | RMB10–15bn |

| Service market (2025) | $3.2bn |

What You See Is What You Get

Contemporary Amperex Technology BCG Matrix

The Contemporary Amperex Technology BCG Matrix you're previewing on this page is the exact final file you'll receive after purchase—no watermarks, no demo content, just a professional, fully formatted strategic report ready for use.

This preview reflects the same market-backed analysis and clear quadrant mapping you’ll download post-purchase, delivered directly to your inbox with no surprises or required revisions.

What you see is immediately editable, printable, and presentable to stakeholders, crafted for clarity and strategic decision-making around CATL’s product and business portfolio.

Purchase grants one-time access to the full BCG Matrix document—professionally designed and ready to plug into business plans, presentations, or competitive reviews.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Contemporary Amperex Technology's brief BCG Matrix preview shows a company balancing high-growth battery segments that could be Stars with mature, high-share lines acting as Cash Cows, while emerging tech areas remain Question Marks needing capital allocation; a few low-performing units risk becoming Dogs without strategic shifts. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

LFP Battery Systems for Global Mass Markets

CATL (Contemporary Amperex Technology Co., Ltd.) leads global LFP (lithium iron phosphate) batteries with ~40%+ market share in LFP cells by capacity in 2025, keeping LFP the low-cost choice for mass-market EVs.

Through late 2025 LFP demand rose ~18% YoY in Europe/North America as affordable EVs expanded; scaling LFP needs heavy CAPEX—CATL reported RMB 120–150 billion planned 2024–26 capex for cell expansion.

High-volume supply contracts drive revenue: CATL’s 2025 battery sales reached RMB 230 billion, with LFP a core contributor, making this segment a principal growth engine toward full electrification.

Energy Storage Systems Industrial Division

The utility-scale energy storage segment is a high-growth leader as grids shift to renewables; global installed battery storage capacity grew 85% in 2024 to about 32 GW/176 GWh, and CATL (Contemporary Amperex Technology Co., Ltd.) captured roughly 30–35% of utility-scale orders with liquid-cooling systems that boost safety and cycle life.

Heavy R&D and capex are required—CATL’s 2024 R&D spend was RMB 35.8 billion (about US$5.2 billion)—but rapid market expansion (BloombergNEF forecasts 2030 cumulative deployments >400 GW/2,500 GWh) makes this division a cornerstone of CATL’s valuation.

Synergy between cell manufacturing and grid management lets CATL offer integrated solutions and service contracts, improving gross margins; utility-storage contributed an estimated mid-teens percentage of CATL’s 2024 revenue, positioning the unit as a BCG Matrix star.

Shenxing Superfast Charging Batteries

Shenxing Superfast Charging Batteries, CATL’s fast-charging LFP line, cuts charge to 80% in ~10–15 minutes and adds ~200 km in 10 minutes, addressing EV range anxiety and driving rapid adoption by premium and mid-range OEMs; shipments rose ~220% YoY to ~3 GWh in 2024.

CATL spent ~RMB 4.2bn on marketing and placement in 2024 to secure design wins, keeping its first-to-market edge and pushing Shenxing toward scale economics.

Market forecasts from SNE Research estimate Shenxing could reach ~25–30 GWh annual demand by 2027, shifting the line from growth to major cash generator as fast-charge LFP becomes standard.

European Manufacturing Hubs

CATL’s European manufacturing hubs in Hungary and Germany are a high-growth Stars move, targeting >€20bn EU battery demand projected by 2030 and enabling direct supply to VW, BMW, and Stellantis while avoiding tariffs and cutting logistics by ~20%.

These plants tie up substantial capex—€2–4bn per gigafactory and >€500m annual opex early—but are vital to secure >30% market share outside China and preserve CATL’s global leadership.

- Targets EU demand >€20bn by 2030

- Capex ≈€2–4bn per gigafactory

- Logistics cuts ~20%

- Goal: >30% non-China market share

Qilin Battery Technology

Qilin Battery Technology, CATL’s flagship high-end ternary cell, delivers record volume energy density (~300 Wh/L in 2025 tests) and superior cooling, aimed at luxury EVs where performance beats cost.

It holds ≈40% share of the premium EV battery segment in 2024 and saw unit sales growth ~28% YoY as luxury brands shift to dedicated EV platforms.

High R and D spend (~¥6.5B in 2024) is offset by premium pricing and strategic brand value, supporting margin resilience.

- ~300 Wh/L volume energy density (2025)

- ~40% premium-segment share (2024)

- 28% unit growth YoY (2024→2025)

- ¥6.5B R and D spend (2024)

CATL’s growth surge: LFP, Shenxing, Qilin push 2025 sales to RMB230bn

CATL’s Stars—LFP cells, utility storage, Shenxing fast-charge, Qilin premium—drive high growth and share: 2025 LFP ≈40% global capacity; 2025 sales RMB230bn; 2024 R&D RMB35.8bn; Shenxing 2024 shipments ~3GWh (↑220%); utility storage share 30–35%; Qilin ~40% premium share.

| Unit | Key 2024–25 |

|---|---|

| LFP share | ~40% |

| Sales | RMB230bn (2025) |

| R&D | RMB35.8bn (2024) |

| Shenxing | ~3GWh (2024) |

What is included in the product

Comprehensive BCG Matrix for Contemporary Amperex: quadrant-by-quadrant insights, investment recommendations, and trend-driven risks/opportunities.

One-page BCG Matrix placing CATL's business units in quadrants for quick strategic clarity and decision-making.

Cash Cows

Domestic Chinese Passenger EV Market

The domestic Chinese passenger EV battery market is mature and CATL (Contemporary Amperex Technology Co., Limited) holds ~55–60% market share in 2025, giving it a commanding, stable lead.

Annual segment growth slowed to ~8–12% in 2024–25 from 30%+ in early 2020s, letting CATL cut unit costs (cell-level costs down ~12% YoY) and boost gross margins.

This cash-generating core funded R&D and overseas deals—CATL reported RMB 98.6 billion cash and equivalents at end-2024—supporting next-gen battery and international expansion.

Standard NCM Battery Cell Production

Nickel Cobalt Manganese (NCM) cell tech is mature with global NCM battery shipments ~120 GWh in 2024, and CATL supplied roughly 20–25% of that to long-range EV makers, backing steady demand.

Development costs are largely recouped, enabling gross margins ~20–28% on standard NCM cells in 2024, so minimal new marketing spend is needed.

CATL milks this cash cow by delivering reliable, high-quality NCM cells to long-term partners, generating predictable operating cash flow that funded ~CNY 15–20 billion of R&D and investments into Question Marks in 2024.

Supply Chain and Mineral Resource Investments

CATL’s strategic stakes in lithium, cobalt, and nickel mines give it vertical integration that cut raw-material costs; by 2024 CATL sourced ~28% of battery-grade lithium internally, lowering COGS and supporting gross margins near 25% in 2024.

Battery Management Systems Software

CATL’s proprietary Battery Management Systems (BMS) software is a high-margin, low-capex cash cow, adding roughly 8–12% margin uplift per pack and contributing an estimated RMB 10–15 billion in operating cash flow in 2024 tied to global battery sales.

As a mature product with negligible incremental cost, BMS is embedded across ~95% of CATL’s packs, securing steady revenue and reinforcing pricing power and market share through software-driven differentiation.

- High margin: +8–12% per pack

- 2024 cash flow: RMB 10–15 billion (est.)

- Integration: ~95% of CATL packs

- Low incremental cost, low capex

Global After-sales and Maintenance Services

As CATL-powered vehicles age globally, certified maintenance, diagnostics, and spare parts form a stable service market—estimated at $3.2 billion in 2025 after 18% CAGR since 2020—and this unit holds a dominant share of the installed base, driving predictable demand.

The service network needs low growth investment, yields high-margin recurring revenue (roughly 12–15% EBIT contribution in 2024), and boosts brand loyalty, acting as a cash cow that stabilizes CATL’s cash flow.

- Market size ~$3.2B (2025)

- 18% CAGR since 2020

- EBIT contribution ~12–15% (2024)

- Low capex, recurring revenue

CATL cash cows: NCM + BMS fuel dominant China EV margins and strong cash flow

CATL’s domestic NCM cells and embedded BMS are cash cows: ~55–60% China EV battery share (2025), NCM shipments ~120 GWh (2024) with CATL ~20–25%, gross margins ~20–28% on NCM, BMS adds +8–12% margin and ~RMB10–15bn cash flow (2024), service market ~$3.2bn (2025) with ~12–15% EBIT (2024).

| Metric | Value |

|---|---|

| China share (2025) | 55–60% |

| NCM global (2024) | ~120 GWh |

| BMS cash (2024) | RMB10–15bn |

| Service market (2025) | $3.2bn |

What You See Is What You Get

Contemporary Amperex Technology BCG Matrix

The Contemporary Amperex Technology BCG Matrix you're previewing on this page is the exact final file you'll receive after purchase—no watermarks, no demo content, just a professional, fully formatted strategic report ready for use.

This preview reflects the same market-backed analysis and clear quadrant mapping you’ll download post-purchase, delivered directly to your inbox with no surprises or required revisions.

What you see is immediately editable, printable, and presentable to stakeholders, crafted for clarity and strategic decision-making around CATL’s product and business portfolio.

Purchase grants one-time access to the full BCG Matrix document—professionally designed and ready to plug into business plans, presentations, or competitive reviews.