Cato Porter's Five Forces Analysis

From Overview to Strategy Blueprint

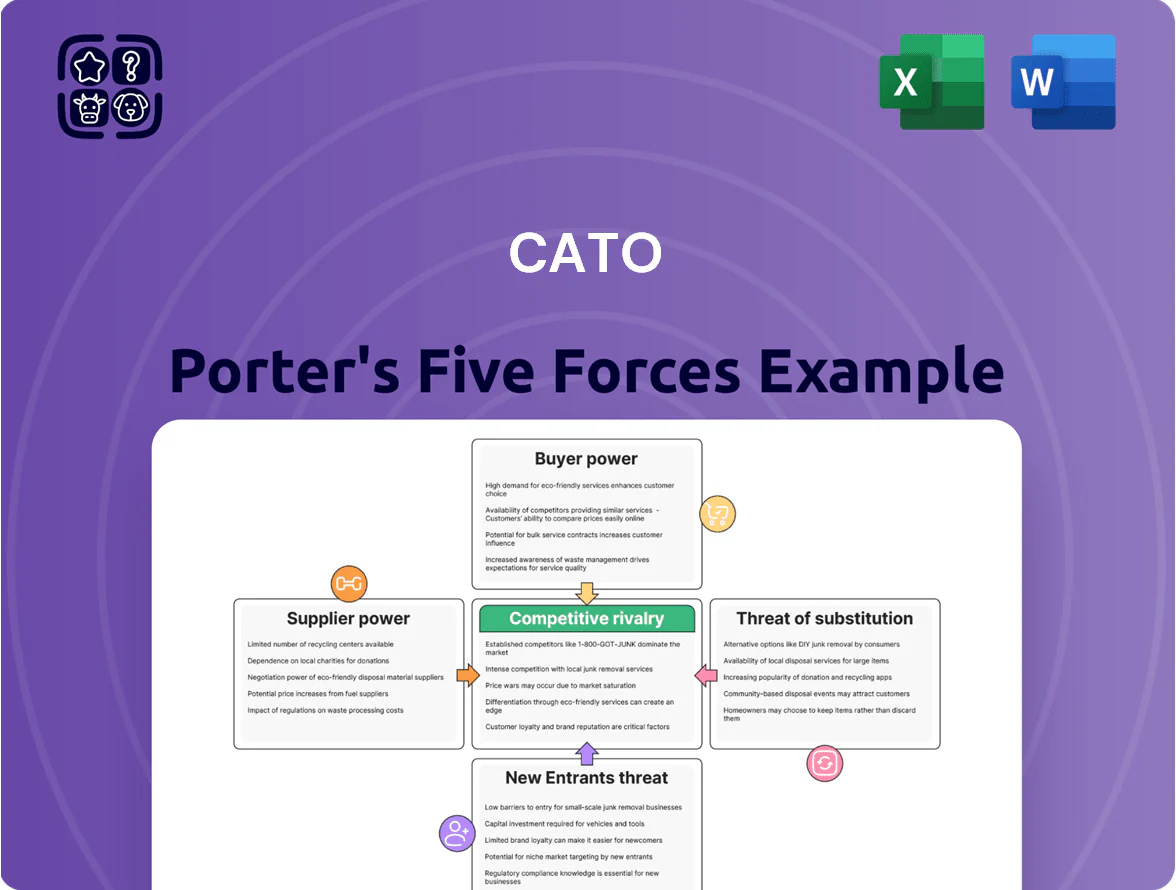

Cato’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry shaping its retail apparel niche; strategic levers and risk points emerge even in this brief view. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Fragmented Global Vendor Base

The apparel supply base is highly fragmented, dominated by thousands of small–mid manufacturers in Asia and Central America; Cato sources from hundreds of vendors, so no single supplier commands pricing power.

This dispersion lets Cato negotiate discounts and agile terms—industry data shows top 10% of vendors account for <20% of volumes—so Cato can reallocate orders quickly if cost or quality slips.

Low Switching Costs for Production

Because Cato offers value-priced fashion using standard materials and mass-production techniques, switching suppliers is low-cost and fast, letting Cato re-source across Asia or the Americas to chase prices; in 2024 apparel import data showed average unit costs varied up to 18% between top suppliers, so flexibility matters. Cato avoids proprietary manufacturing, so no single partner can lock its supply. This lets Cato pursue lowest global production costs to protect its ~20% gross margin target on core lines.

Standardized Raw Material Requirements

Fabrics and components for Cato’s apparel are commoditized in the global textile market, with cotton, polyester and basic trims available from hundreds of suppliers; global cotton production hit ~25.7 million tonnes in 2024, keeping input supply ample. Suppliers hold low bargaining power because Cato can switch among alternative providers—typical supplier concentration ratios are low—so lacking patented or unique materials prevents suppliers from forcing price hikes without losing business.

Potential for Forward Integration

Most garment makers still lack US retail infrastructure, so forward integration risk is low; however, e-commerce growth raised the threat—global marketplace sales grew 18% in 2024, and some large manufacturers now list on Amazon and Shein Marketplace, cutting retailers out.

Direct-to-consumer sales remain limited: only ~6–8% of global apparel manufacturers reported selling consumer-facing in 2024, and opening physical stores is costly, so supplier bargaining power stays modest.

- E-commerce growth +18% (2024)

- 6–8% manufacturers sell DTC (2024)

- Physical retail costs keep barrier high

Impact of Geopolitical and Labor Volatility

Supplier power spikes when strikes, regional instability, or trade-policy shifts hit manufacturing hubs; in 2025 Southeast Asia minimum-wage increases (up to 12% in Vietnam Q1 2025) and a 18% year-over-year average shipping-cost volatility gave suppliers leverage to seek higher unit prices.

Cato should diversify sourcing across at least 3 regions and hold 6–10 weeks of inventory to cut localized supplier bargaining power and contain COGS inflation risks.

- 2025 Vietnam min wage +12%

- Shipping cost volatility +18% YoY

- Target: 3+ sourcing regions

- Hold 6–10 weeks inventory

Keep 3+ sourcing regions and 6–10 weeks inventory as supplier risks rise

Suppliers have low-to-moderate power: fragmented vendor base, commoditized inputs (global cotton ~25.7M t in 2024), and low DTC forward integration (6–8% makers DTC in 2024) let Cato re-source quickly; risk rises with regional wage shocks (Vietnam +12% Q1 2025) and shipping volatility (+18% YoY), so Cato should keep 3+ sourcing regions and 6–10 weeks inventory.

| Metric | Value |

|---|---|

| Global cotton (2024) | 25.7M tonnes |

| DTC manufacturers (2024) | 6–8% |

| Vietnam min wage (Q1 2025) | +12% |

| Shipping cost volatility (YoY 2025) | +18% |

| Recommended sourcing regions | 3+ |

| Target inventory | 6–10 weeks |

What is included in the product

Concise Five Forces analysis tailored to Cato that uncovers competitive dynamics, supplier and buyer power, entry barriers, substitutes, and emerging threats, with strategic commentary and editable Word-ready insights for investor presentations and strategy decks.

A concise Cato Porter Five Forces one-sheet that quantifies competitive pressure, visualizes threats with a radar chart, and lets you swap in fresh data or scenarios—ideal for quick strategic decisions and slide-ready reporting.

Customers Bargaining Power

Minimal Switching Costs for Shoppers

Consumers in retail fashion face near-zero switching costs—no fees, contracts, or loyalty barriers—so 72% of US apparel shoppers said price or style drove store switching in 2024 (National Retail Federation). A Cato customer can easily leave a store and buy from a nearby competitor offering a 10–30% lower price or trendier SKU. This low friction forces Cato to refresh assortments and promotions frequently; otherwise monthly footfall can drop by 5–8% versus peers.

High Price Sensitivity in Value Segment

Cato’s core demographic—value-focused shoppers—shows high price sensitivity: 2024 Nielsen data found 68% of US budget shoppers compared prices online before buying, and BLS inflation at 3.4% in 2024 raised comparison shopping. In this segment small price hikes (even 2–3%) can cut volume sharply; Cato must fine-tune pricing tiers, promotions, and markdown cadence to avoid traffic and basket-size erosion.

Availability of Comprehensive Market Information

Smartphone ubiquity lets shoppers compare prices in real time inside Cato stores; 85% of US adults owned a smartphone in 2023, and 72% of shoppers used phones to compare prices in 2024, shifting leverage to buyers.

Low Brand Loyalty in Fast Fashion

Low brand loyalty in fast fashion means shoppers trade brands for trends; 2025 surveys show 62% of value-fashion buyers prioritize trend fit over brand name, driving transactional buying.

Customers pick immediate availability and price; Cato must spend more on marketing and trend data—fast-fashion peers spend ~4–6% of revenue on trend analytics and agile replenishment.

- 62% prioritize trend fit (2025 survey)

- 4–6% revenue spent on trend/analytics by peers

- High SKU turnover needed to match fleeting demand

Large Volume of Substitute Options

The abundance of substitute shopping venues—off-price chains, fast-fashion, and digital marketplaces—gives consumers strong leverage; US online apparel sales hit 142 billion USD in 2024, widening channels shoppers can switch to.

Oversupply in apparel means customers control discretionary spend, so Cato must compete on convenience, curation, and experience, not just price.

- 2024 US online apparel sales: 142B USD

- Off-price market growth: ~6% CAGR 2021–24

- Competition factors: price, convenience, curation

High buyer leverage squeezes Cato: price gaps, rapid SKU churn, 4–6% trend spend

Buyers hold high leverage: near-zero switching costs, 68–72% price/style comparison rates (2024), and 62% prioritizing trend fit (2025), forcing Cato into 10–30% competitive price gaps, frequent SKU turnover, and 4–6% revenue spend on trend/analytics; US online apparel sales were 142B USD in 2024, widening substitutes and pressuring margins.

| Metric | Value |

|---|---|

| Price/style switch rate | 72% (2024) |

| Compare-before-buy | 68% (2024) |

| Trend over brand | 62% (2025) |

| Online apparel sales | 142B USD (2024) |

| Peer spend on trend analytics | 4–6% revenue |

Full Version Awaits

Cato Porter's Five Forces Analysis

This preview shows the exact Cato Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted, professionally written, and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Cato’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry shaping its retail apparel niche; strategic levers and risk points emerge even in this brief view. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Fragmented Global Vendor Base

The apparel supply base is highly fragmented, dominated by thousands of small–mid manufacturers in Asia and Central America; Cato sources from hundreds of vendors, so no single supplier commands pricing power.

This dispersion lets Cato negotiate discounts and agile terms—industry data shows top 10% of vendors account for <20% of volumes—so Cato can reallocate orders quickly if cost or quality slips.

Low Switching Costs for Production

Because Cato offers value-priced fashion using standard materials and mass-production techniques, switching suppliers is low-cost and fast, letting Cato re-source across Asia or the Americas to chase prices; in 2024 apparel import data showed average unit costs varied up to 18% between top suppliers, so flexibility matters. Cato avoids proprietary manufacturing, so no single partner can lock its supply. This lets Cato pursue lowest global production costs to protect its ~20% gross margin target on core lines.

Standardized Raw Material Requirements

Fabrics and components for Cato’s apparel are commoditized in the global textile market, with cotton, polyester and basic trims available from hundreds of suppliers; global cotton production hit ~25.7 million tonnes in 2024, keeping input supply ample. Suppliers hold low bargaining power because Cato can switch among alternative providers—typical supplier concentration ratios are low—so lacking patented or unique materials prevents suppliers from forcing price hikes without losing business.

Potential for Forward Integration

Most garment makers still lack US retail infrastructure, so forward integration risk is low; however, e-commerce growth raised the threat—global marketplace sales grew 18% in 2024, and some large manufacturers now list on Amazon and Shein Marketplace, cutting retailers out.

Direct-to-consumer sales remain limited: only ~6–8% of global apparel manufacturers reported selling consumer-facing in 2024, and opening physical stores is costly, so supplier bargaining power stays modest.

- E-commerce growth +18% (2024)

- 6–8% manufacturers sell DTC (2024)

- Physical retail costs keep barrier high

Impact of Geopolitical and Labor Volatility

Supplier power spikes when strikes, regional instability, or trade-policy shifts hit manufacturing hubs; in 2025 Southeast Asia minimum-wage increases (up to 12% in Vietnam Q1 2025) and a 18% year-over-year average shipping-cost volatility gave suppliers leverage to seek higher unit prices.

Cato should diversify sourcing across at least 3 regions and hold 6–10 weeks of inventory to cut localized supplier bargaining power and contain COGS inflation risks.

- 2025 Vietnam min wage +12%

- Shipping cost volatility +18% YoY

- Target: 3+ sourcing regions

- Hold 6–10 weeks inventory

Keep 3+ sourcing regions and 6–10 weeks inventory as supplier risks rise

Suppliers have low-to-moderate power: fragmented vendor base, commoditized inputs (global cotton ~25.7M t in 2024), and low DTC forward integration (6–8% makers DTC in 2024) let Cato re-source quickly; risk rises with regional wage shocks (Vietnam +12% Q1 2025) and shipping volatility (+18% YoY), so Cato should keep 3+ sourcing regions and 6–10 weeks inventory.

| Metric | Value |

|---|---|

| Global cotton (2024) | 25.7M tonnes |

| DTC manufacturers (2024) | 6–8% |

| Vietnam min wage (Q1 2025) | +12% |

| Shipping cost volatility (YoY 2025) | +18% |

| Recommended sourcing regions | 3+ |

| Target inventory | 6–10 weeks |

What is included in the product

Concise Five Forces analysis tailored to Cato that uncovers competitive dynamics, supplier and buyer power, entry barriers, substitutes, and emerging threats, with strategic commentary and editable Word-ready insights for investor presentations and strategy decks.

A concise Cato Porter Five Forces one-sheet that quantifies competitive pressure, visualizes threats with a radar chart, and lets you swap in fresh data or scenarios—ideal for quick strategic decisions and slide-ready reporting.

Customers Bargaining Power

Minimal Switching Costs for Shoppers

Consumers in retail fashion face near-zero switching costs—no fees, contracts, or loyalty barriers—so 72% of US apparel shoppers said price or style drove store switching in 2024 (National Retail Federation). A Cato customer can easily leave a store and buy from a nearby competitor offering a 10–30% lower price or trendier SKU. This low friction forces Cato to refresh assortments and promotions frequently; otherwise monthly footfall can drop by 5–8% versus peers.

High Price Sensitivity in Value Segment

Cato’s core demographic—value-focused shoppers—shows high price sensitivity: 2024 Nielsen data found 68% of US budget shoppers compared prices online before buying, and BLS inflation at 3.4% in 2024 raised comparison shopping. In this segment small price hikes (even 2–3%) can cut volume sharply; Cato must fine-tune pricing tiers, promotions, and markdown cadence to avoid traffic and basket-size erosion.

Availability of Comprehensive Market Information

Smartphone ubiquity lets shoppers compare prices in real time inside Cato stores; 85% of US adults owned a smartphone in 2023, and 72% of shoppers used phones to compare prices in 2024, shifting leverage to buyers.

Low Brand Loyalty in Fast Fashion

Low brand loyalty in fast fashion means shoppers trade brands for trends; 2025 surveys show 62% of value-fashion buyers prioritize trend fit over brand name, driving transactional buying.

Customers pick immediate availability and price; Cato must spend more on marketing and trend data—fast-fashion peers spend ~4–6% of revenue on trend analytics and agile replenishment.

- 62% prioritize trend fit (2025 survey)

- 4–6% revenue spent on trend/analytics by peers

- High SKU turnover needed to match fleeting demand

Large Volume of Substitute Options

The abundance of substitute shopping venues—off-price chains, fast-fashion, and digital marketplaces—gives consumers strong leverage; US online apparel sales hit 142 billion USD in 2024, widening channels shoppers can switch to.

Oversupply in apparel means customers control discretionary spend, so Cato must compete on convenience, curation, and experience, not just price.

- 2024 US online apparel sales: 142B USD

- Off-price market growth: ~6% CAGR 2021–24

- Competition factors: price, convenience, curation

High buyer leverage squeezes Cato: price gaps, rapid SKU churn, 4–6% trend spend

Buyers hold high leverage: near-zero switching costs, 68–72% price/style comparison rates (2024), and 62% prioritizing trend fit (2025), forcing Cato into 10–30% competitive price gaps, frequent SKU turnover, and 4–6% revenue spend on trend/analytics; US online apparel sales were 142B USD in 2024, widening substitutes and pressuring margins.

| Metric | Value |

|---|---|

| Price/style switch rate | 72% (2024) |

| Compare-before-buy | 68% (2024) |

| Trend over brand | 62% (2025) |

| Online apparel sales | 142B USD (2024) |

| Peer spend on trend analytics | 4–6% revenue |

Full Version Awaits

Cato Porter's Five Forces Analysis

This preview shows the exact Cato Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted, professionally written, and ready for download and use the moment you buy.