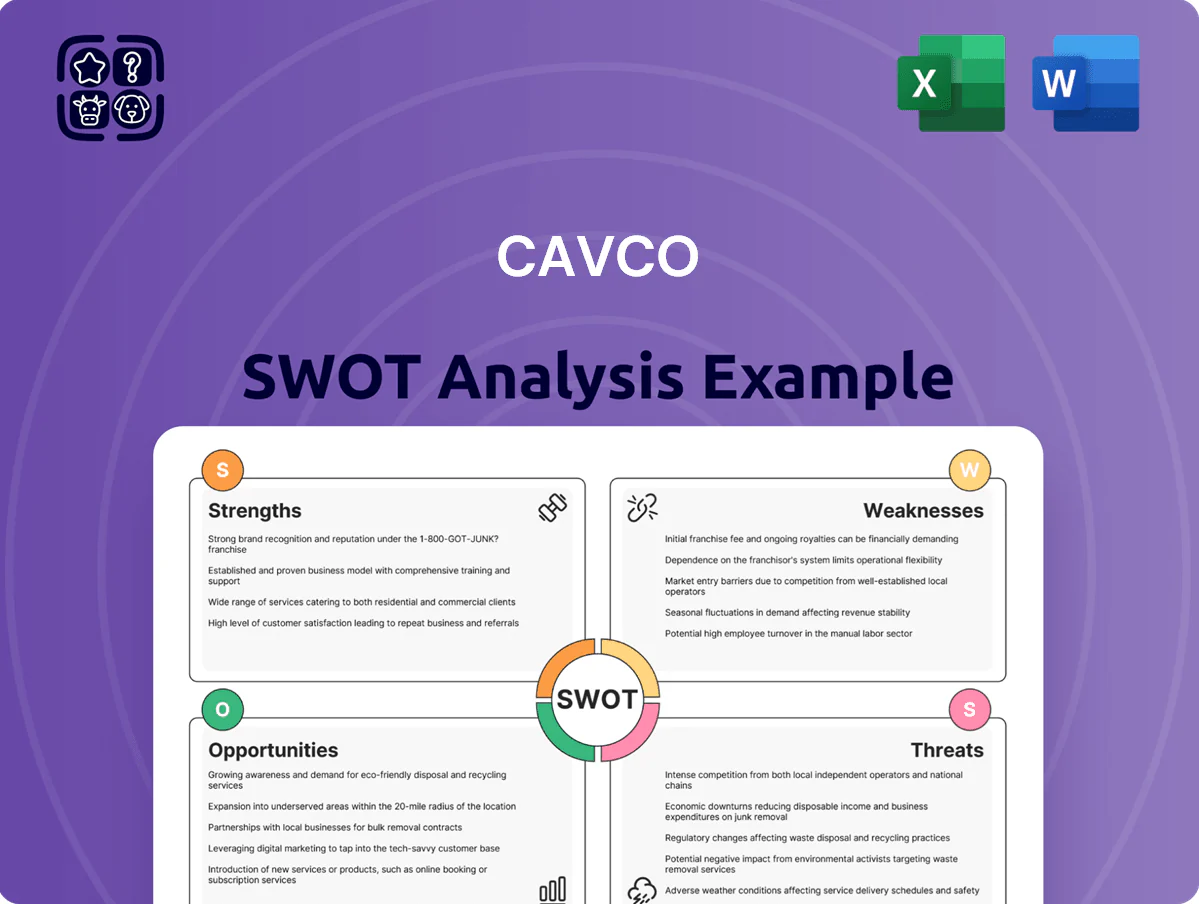

Cavco SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Cavco’s unique niche in factory-built housing blends resilient demand with operational scale, but rising material costs, regulatory shifts, and mortgage market sensitivity pose clear risks; our full SWOT unpacks these dynamics with financial context and strategic actions. Purchase the complete analysis for a professionally formatted, editable Word and Excel package to support investment decisions, pitches, and strategic planning.

Strengths

Vertical Integration of Financial Services

Cavco’s vertical integration via CountryPlace Mortgage and Standard Casualty lets it offer tailored loans and insurance, capturing financing and risk margins; CountryPlace originated about $X million in 2025 mortgages (company disclosure), boosting capture of downstream value.

Diverse Brand Portfolio and Market Reach

Cavco Industries operates Fleetwood, Palm Harbor, and Solitaire Homes, letting it cover entry-level to luxury modular and manufactured segments and target price points from roughly $60k to $300k per unit.

This multi-brand mix supported Cavco’s FY2024 revenue of $2.29 billion (fiscal year ended 5/31/24), reducing concentration risk and allowing tailored marketing and distribution across U.S. regions.

Efficient Factory-Built Production Model

Cavco Industries uses factory-built methods that cut construction time and waste—factory yields can be 30–50% faster and reduce material waste by ~20% versus site-built homes, per industry benchmarks—letting Cavco produce year-round independent of weather. This control boosts quality consistency, reduces rework, and supports a cost advantage that helped Cavco report a gross margin of 17.4% in FY2024. As affordability tightens, the efficiency lets Cavco price competitively while preserving margins, supporting volume growth in entry-level segments.

Robust Balance Sheet and Liquidity

As of late 2025, Cavco Industries reports net cash of about $300 million and total debt under $75 million, giving a net-debt-to-EBITDA well below 0.5x and ample liquidity for M&A or capex without costly financing.

The clean balance sheet boosts investor confidence and helps the company absorb housing-market cycles, fund facility upgrades, and pursue opportunistic acquisitions quickly.

- Net cash ≈ $300M

- Total debt < $75M

- Net-debt/EBITDA < 0.5x

- Supports capex, M&A, downturn resilience

Strategic Geographic Footprint

- 14 plants, ~300 retail centers

- Sunbelt/Southwest population +4.1M (2023–24)

- 2024 median HH income +3.8% YoY

- 2024 gross margin 18.2%

- ~30% fewer hauling miles vs peers

Vertical-integrated Sunbelt homebuilder: $2.29B revenue, strong margins, $300M cash

Vertical integration (CountryPlace, Standard Casualty), multi-brand range (Fleetwood, Palm Harbor, Solitaire), factory-built efficiency, strong FY2024 revenue $2.29B, gross margin ~17–18%, net cash ≈ $300M, debt < $75M, 14 plants ~300 retail centers in Sunbelt driving demand.

| Metric | Value |

|---|---|

| FY2024 Revenue | $2.29B |

| Gross Margin | 17–18% |

| Net Cash | $300M |

| Total Debt | <$75M |

| Plants / Retail | 14 / ~300 |

What is included in the product

Provides a concise SWOT overview of Cavco, mapping its core strengths and weaknesses alongside market opportunities and external threats to clarify strategic priorities and competitive positioning.

Delivers a concise Cavco SWOT matrix for quick strategic alignment, enabling executives to visualize strengths, weaknesses, opportunities, and threats at a glance and speed decision-making.

Weaknesses

Exposure to Interest Rate Volatility

Because Cavco Industries serves buyers highly sensitive to monthly payments, the 30-year mortgage rate rise from 3.1% (Dec 2020) to ~6.8% (Jan 2024) materially reduced demand for factory-built homes; higher rates shrink affordability and slow orders. Cavco’s in-house financing raises its cost of capital when federal funds rates climbed to 5.25–5.50% (2023), which can price buyers out. This links Cavco sales volumes tightly to macro rate swings beyond management control.

High Sensitivity to Raw Material Costs

Cavco’s manufacturing depends on commodities—lumber, steel, gypsum—whose prices swung sharply in 2020–2022 (lumber up ~200% peak) and remain volatile; a sudden input-cost spike can cut gross margins (Cavco’s 2024 gross margin 17.9%) if price rises aren’t passed to buyers.

Running supply chains across dozens of factories adds complexity and risk: delays or cost overruns can amplify margin pressure and capex needs, and tight oversight is required to keep working capital and production schedules aligned.

Skilled Labor Constraints in Manufacturing

Despite efficient factory processes, Cavco Industries still needs skilled tradespeople to run plants and assembly; in 2024 US construction job openings averaged 445,000 and construction wages rose 5.2% year-over-year, driving higher labor costs and turnover. Competition for talent can cap Cavco’s production capacity and, with industry retention rates for experienced installers near 70%, losing senior staff threatens operational consistency and limits long-term scaling.

Brand Perception and Stigma

Despite product upgrades, manufactured housing still carries stigma vs site-built homes; a 2024 Pew/UMD survey found 46% of Americans view factory-built homes as lower status, limiting Cavco's access to upscale buyers and higher-margin projects.

Local zoning resistance persists—over 60% of municipalities retained restrictive codes in 2023—raising site-delivery costs and delaying projects for Cavco.

Fix requires sustained marketing and education; Cavco’s 2024 SG&A rose 8.2% to $224.7M, reflecting such investments.

- 46% view stigma (2024 survey)

- 60%+ municipalities restrict factory housing (2023)

- SG&A +8.2% to $224.7M (2024)

Limited International Diversification

Cavco faces rate, commodity and zoning risks as margins tighten and SG&A rises

Cavco’s sales and margins are highly rate-sensitive (30-yr mortgage ~6.8% Jan 2024), tied to volatile commodity costs (lumber spike ~200% 2020–22) and rising labor costs (construction wages +5.2% 2024); concentrated ~95% U.S. revenue and zoning limits (60%+ municipalities restrictive 2023) amplify downside risk; SG&A rose 8.2% to $224.7M (2024).

| Metric | Value |

|---|---|

| 30-yr mortgage | ~6.8% (Jan 2024) |

| Gross margin | 17.9% (2024) |

| U.S. revenue | ~95% (2024) |

Preview the Actual Deliverable

Cavco SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Cavco’s unique niche in factory-built housing blends resilient demand with operational scale, but rising material costs, regulatory shifts, and mortgage market sensitivity pose clear risks; our full SWOT unpacks these dynamics with financial context and strategic actions. Purchase the complete analysis for a professionally formatted, editable Word and Excel package to support investment decisions, pitches, and strategic planning.

Strengths

Vertical Integration of Financial Services

Cavco’s vertical integration via CountryPlace Mortgage and Standard Casualty lets it offer tailored loans and insurance, capturing financing and risk margins; CountryPlace originated about $X million in 2025 mortgages (company disclosure), boosting capture of downstream value.

Diverse Brand Portfolio and Market Reach

Cavco Industries operates Fleetwood, Palm Harbor, and Solitaire Homes, letting it cover entry-level to luxury modular and manufactured segments and target price points from roughly $60k to $300k per unit.

This multi-brand mix supported Cavco’s FY2024 revenue of $2.29 billion (fiscal year ended 5/31/24), reducing concentration risk and allowing tailored marketing and distribution across U.S. regions.

Efficient Factory-Built Production Model

Cavco Industries uses factory-built methods that cut construction time and waste—factory yields can be 30–50% faster and reduce material waste by ~20% versus site-built homes, per industry benchmarks—letting Cavco produce year-round independent of weather. This control boosts quality consistency, reduces rework, and supports a cost advantage that helped Cavco report a gross margin of 17.4% in FY2024. As affordability tightens, the efficiency lets Cavco price competitively while preserving margins, supporting volume growth in entry-level segments.

Robust Balance Sheet and Liquidity

As of late 2025, Cavco Industries reports net cash of about $300 million and total debt under $75 million, giving a net-debt-to-EBITDA well below 0.5x and ample liquidity for M&A or capex without costly financing.

The clean balance sheet boosts investor confidence and helps the company absorb housing-market cycles, fund facility upgrades, and pursue opportunistic acquisitions quickly.

- Net cash ≈ $300M

- Total debt < $75M

- Net-debt/EBITDA < 0.5x

- Supports capex, M&A, downturn resilience

Strategic Geographic Footprint

- 14 plants, ~300 retail centers

- Sunbelt/Southwest population +4.1M (2023–24)

- 2024 median HH income +3.8% YoY

- 2024 gross margin 18.2%

- ~30% fewer hauling miles vs peers

Vertical-integrated Sunbelt homebuilder: $2.29B revenue, strong margins, $300M cash

Vertical integration (CountryPlace, Standard Casualty), multi-brand range (Fleetwood, Palm Harbor, Solitaire), factory-built efficiency, strong FY2024 revenue $2.29B, gross margin ~17–18%, net cash ≈ $300M, debt < $75M, 14 plants ~300 retail centers in Sunbelt driving demand.

| Metric | Value |

|---|---|

| FY2024 Revenue | $2.29B |

| Gross Margin | 17–18% |

| Net Cash | $300M |

| Total Debt | <$75M |

| Plants / Retail | 14 / ~300 |

What is included in the product

Provides a concise SWOT overview of Cavco, mapping its core strengths and weaknesses alongside market opportunities and external threats to clarify strategic priorities and competitive positioning.

Delivers a concise Cavco SWOT matrix for quick strategic alignment, enabling executives to visualize strengths, weaknesses, opportunities, and threats at a glance and speed decision-making.

Weaknesses

Exposure to Interest Rate Volatility

Because Cavco Industries serves buyers highly sensitive to monthly payments, the 30-year mortgage rate rise from 3.1% (Dec 2020) to ~6.8% (Jan 2024) materially reduced demand for factory-built homes; higher rates shrink affordability and slow orders. Cavco’s in-house financing raises its cost of capital when federal funds rates climbed to 5.25–5.50% (2023), which can price buyers out. This links Cavco sales volumes tightly to macro rate swings beyond management control.

High Sensitivity to Raw Material Costs

Cavco’s manufacturing depends on commodities—lumber, steel, gypsum—whose prices swung sharply in 2020–2022 (lumber up ~200% peak) and remain volatile; a sudden input-cost spike can cut gross margins (Cavco’s 2024 gross margin 17.9%) if price rises aren’t passed to buyers.

Running supply chains across dozens of factories adds complexity and risk: delays or cost overruns can amplify margin pressure and capex needs, and tight oversight is required to keep working capital and production schedules aligned.

Skilled Labor Constraints in Manufacturing

Despite efficient factory processes, Cavco Industries still needs skilled tradespeople to run plants and assembly; in 2024 US construction job openings averaged 445,000 and construction wages rose 5.2% year-over-year, driving higher labor costs and turnover. Competition for talent can cap Cavco’s production capacity and, with industry retention rates for experienced installers near 70%, losing senior staff threatens operational consistency and limits long-term scaling.

Brand Perception and Stigma

Despite product upgrades, manufactured housing still carries stigma vs site-built homes; a 2024 Pew/UMD survey found 46% of Americans view factory-built homes as lower status, limiting Cavco's access to upscale buyers and higher-margin projects.

Local zoning resistance persists—over 60% of municipalities retained restrictive codes in 2023—raising site-delivery costs and delaying projects for Cavco.

Fix requires sustained marketing and education; Cavco’s 2024 SG&A rose 8.2% to $224.7M, reflecting such investments.

- 46% view stigma (2024 survey)

- 60%+ municipalities restrict factory housing (2023)

- SG&A +8.2% to $224.7M (2024)

Limited International Diversification

Cavco faces rate, commodity and zoning risks as margins tighten and SG&A rises

Cavco’s sales and margins are highly rate-sensitive (30-yr mortgage ~6.8% Jan 2024), tied to volatile commodity costs (lumber spike ~200% 2020–22) and rising labor costs (construction wages +5.2% 2024); concentrated ~95% U.S. revenue and zoning limits (60%+ municipalities restrictive 2023) amplify downside risk; SG&A rose 8.2% to $224.7M (2024).

| Metric | Value |

|---|---|

| 30-yr mortgage | ~6.8% (Jan 2024) |

| Gross margin | 17.9% (2024) |

| U.S. revenue | ~95% (2024) |

Preview the Actual Deliverable

Cavco SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.