CBAK Energy PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, market dynamics, and technological advances are shaping CBAK Energy’s trajectory—our concise PESTLE snapshot highlights risk and opportunity for investors and strategists; purchase the full analysis to access the complete, actionable intelligence you need to inform decisions and build a competitive advantage.

Political factors

Geopolitical Trade Relations

Ongoing US-China trade tensions affect CBAK Energy's NASDAQ status and access to US capital, with US tariffs on Chinese EV/battery imports rising risk; US imposed 7.5–25% tariffs on some Chinese goods in 2023 and considered tech export controls in 2024. Potential tariffs or export restrictions on lithium-ion components and battery machinery could raise input costs by an estimated 5–12% and disrupt 2024–25 supply chains. CBAK must manage compliance costs and potential delisting risks while aligning Chinese manufacturing with international trade rules through 2025.

Government Subsidies and Incentives

The Chinese government continues to back NEVs with subsidies and quotas; in 2024 subsidies and tax incentives helped sustain ~25% YoY EV sales growth, indirectly benefiting battery makers like CBAK by tying support to energy density and local production targets that shape R&D and capacity decisions.

Energy Security Policies

Global energy independence drives Europe and North America to localize battery supply chains, with the EU’s 2023 Critical Raw Materials Act targeting 80% domestic sourcing by 2030, creating market access barriers for Chinese-based CBAK while opening localized JV opportunities; political clean-energy mandates (IEA projects 4,500 TWh of battery storage demand by 2040) support long-term demand for CBAK’s residential and industrial storage solutions despite export constraints.

Local Government Support in China

CBAK Energy depends on municipal support in Dalian and Nanjing for land use, tax incentives and infrastructure, which enabled its latest 2024 cell production expansion funded partly by a reported RMB 200–300 million in local low-interest loans.

These partnerships accelerate factory build-out and capex deployment but expose CBAK to shifts in local leadership or policy: a change in priorities could slow permitting and reduce access to preferential financing, affecting planned capacity scaling.

- 2024 local low-interest loans ~RMB 200–300M

- Key sites: Dalian, Nanjing — primary for manufacturing expansion

- Risks: leadership changes, reprioritized regional economic plans

International Regulatory Alignment

As CBAK expands in light EVs and ESS, it must navigate varied battery-safety and data-security regimes across EU, US, China and ASEAN; EU battery regulation updates (Recast expected 2024–25) raise compliance costs—industry estimates show 5–8% higher OPEX for certified supply chains.

Political scrutiny on raw-material provenance (EU Critical Raw Materials Act, US CHIPS/IRA sourcing clauses) imposes stricter reporting—traceability rules push suppliers to disclose cobalt/nickel origins; 2024 audits show 30% more documentation requests for battery makers.

To manage political risk CBAK should diversify clients by region, strengthen board-level transparency and publish enhanced ESG and supply-chain due-diligence; firms with clear governance report 12–18% lower risk-premium in funding markets.

- Comply with evolving EU/US battery/data rules—expect 5–8% OPEX rise

- Prepare for increased raw-material provenance reporting—~30% more audits in 2024

- Diversify client geography and boost governance to lower political risk premium by ~12–18%

Trade frictions, subsidies and rules reshape EV supply chains—costs up, demand and funding rise

US-China trade tensions and potential tariffs/export controls (7.5–25% tariffs in 2023; tech controls considered 2024) threaten NASDAQ access and could raise input costs 5–12%; Chinese NEV subsidies sustained ~25% YoY EV growth in 2024 aiding battery demand; EU/US localization rules (EU CRM Act, IRA) increase compliance OPEX ~5–8% and audits ~30%; local loans ~RMB 200–300M supported 2024 expansion.

| Factor | 2023–24 Data | Impact |

|---|---|---|

| US tariffs/controls | 7.5–25% (2023); controls considered (2024) | Input cost +5–12% |

| China NEV support | ~25% YoY EV sales growth (2024) | Higher battery demand |

| Compliance/OPEX | EU/US rules → +5–8% OPEX | Margin pressure |

| Local financing | Loans ~RMB 200–300M (2024) | Enabled capex |

What is included in the product

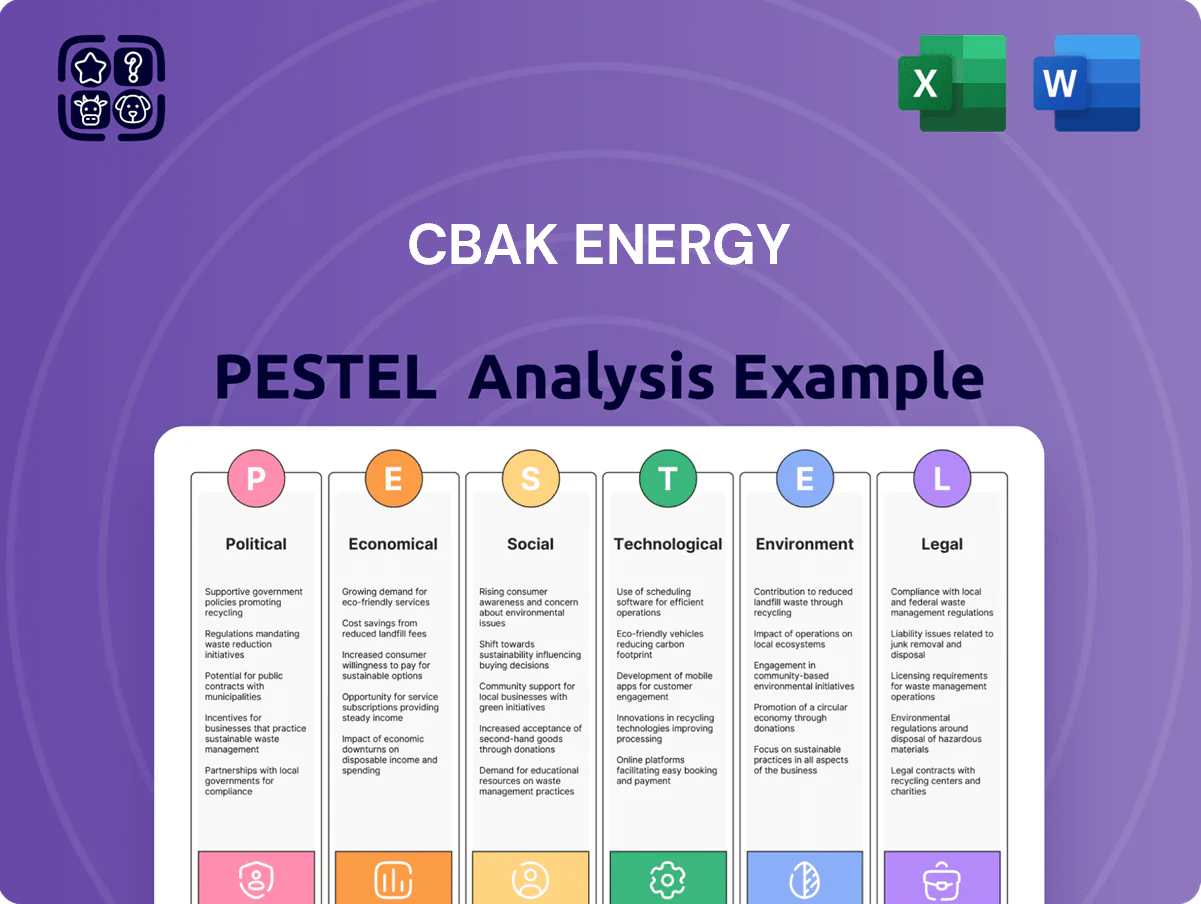

Explores how macro-environmental factors uniquely affect CBAK Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to its battery manufacturing and energy storage markets.

Provides a clean, visually segmented PESTLE summary of CBAK Energy for quick reference in meetings or presentations, easily editable with notes to reflect regional or business-line specifics.

Economic factors

Raw Material Price Volatility

Raw material price volatility—particularly lithium, nickel, and cobalt—directly drives CBAK Energy’s COGS and margins; lithium averaged about $15,000/tonne in 2024 after a mid-2020s correction while nickel and cobalt traded near $22,000/tonne and $30,000/tonne respectively in 2025, exposing margin risk.

Price spikes from supply-demand imbalances can compress margins if CBAK cannot pass costs to customers, as seen in 2021–2022 episodes where spot surges exceeded 40% year-over-year.

Securing long-term offtake or investing upstream is crucial: companies locking multiyear contracts in 2023–2025 reported 5–12% operating margin stability versus peers relying on spot purchases.

Global Inflation and Interest Rates

Persistent global inflation—core CPI running near 3.5–4.5% in 2024–2025 in many markets—raises CBAK’s labor, logistics and factory input costs, squeezing margins on cathode and battery cells.

Higher policy rates (global average short-term rates rose to ~3.5% by end-2025) increases borrowing costs for CBAK’s capex and for consumers financing EVs, potentially slowing demand.

Against this backdrop, disciplined capital allocation and debt management are required to preserve liquidity and support measured expansion.

Growth of the Energy Storage Market

The global energy storage market grew to about 33 GWh of battery deployments in 2024, and BloombergNEF projects cumulative battery storage capacity to exceed 450 GWh by 2030, creating a strong economic tailwind for CBAK Energy as it pivots from EV cells; utility-scale and grid-tied projects—backed by $200+ billion renewable investments in 2024—demand large-format batteries and typically yield multi-year, stable contracts versus volatile consumer or light EV segments.

Currency Exchange Rate Fluctuations

CBAK reports in USD but generates most revenue/costs in RMB, exposing it to USD/RMB volatility; a 2023–2025 swing of roughly 6.7% (CNY weakening from ~6.3 to ~6.72 per USD in 2023–2024) can materially change reported revenue and net assets on NASDAQ filings.

US Fed rate decisions and PBOC easing in 2024–25 directly affect FX and funding costs, altering valuation multiples and investor sentiment toward CBAK.

- USD reporting vs RMB operations creates translation risk

- ~6–7% USD/RMB moves in 2023–24 illustrate magnitude

- Fed and PBOC policy shifts drive FX, funding, and valuation impacts

Consumer Purchasing Power

The demand for light electric vehicles and passenger EVs in China and Southeast Asia is tied to disposable income; China’s urban per capita disposable income rose 3.8% in 2024 while Southeast Asia real GDP averaged ~4.5% in 2024, but rising unemployment or slower growth could delay purchases and hit CBAK’s order book.

Monitoring GDP growth and consumer confidence—China’s 2024 GDP growth 5.2% and ASEAN consumer confidence indices down ~4–6% in late 2024—helps forecast production and inventory needs to avoid excess stock or missed deliveries.

- China urban disposable income +3.8% (2024)

- China GDP growth 5.2% (2024)

- ASEAN real GDP ~4.5% (2024)

- Consumer confidence down ~4–6% in late 2024

Commodity shocks, rising costs and FX risk cloud battery storage upside

Key economic risks: raw-material price swings (Li ~$15,000/t 2024; Ni ~$22,000/t, Co ~$30,000/t 2025) press margins; global core CPI ~3.5–4.5% (2024–25) and avg short rates ~3.5% (end-2025) raise input and funding costs; USD/RMB ~6.3→6.72 (2023–24) creates translation risk; battery storage demand ~33 GWh (2024) supports long-term contracts.

| Metric | Value |

|---|---|

| Li price (2024) | $15,000/t |

| Ni/Co (2025) | $22k / $30k/t |

| Core CPI (2024–25) | 3.5–4.5% |

| USD/RMB swing (2023–24) | ~6.3→6.72 |

| Storage deployments (2024) | 33 GWh |

What You See Is What You Get

CBAK Energy PESTLE Analysis

The preview shown here is the exact CBAK Energy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, market dynamics, and technological advances are shaping CBAK Energy’s trajectory—our concise PESTLE snapshot highlights risk and opportunity for investors and strategists; purchase the full analysis to access the complete, actionable intelligence you need to inform decisions and build a competitive advantage.

Political factors

Geopolitical Trade Relations

Ongoing US-China trade tensions affect CBAK Energy's NASDAQ status and access to US capital, with US tariffs on Chinese EV/battery imports rising risk; US imposed 7.5–25% tariffs on some Chinese goods in 2023 and considered tech export controls in 2024. Potential tariffs or export restrictions on lithium-ion components and battery machinery could raise input costs by an estimated 5–12% and disrupt 2024–25 supply chains. CBAK must manage compliance costs and potential delisting risks while aligning Chinese manufacturing with international trade rules through 2025.

Government Subsidies and Incentives

The Chinese government continues to back NEVs with subsidies and quotas; in 2024 subsidies and tax incentives helped sustain ~25% YoY EV sales growth, indirectly benefiting battery makers like CBAK by tying support to energy density and local production targets that shape R&D and capacity decisions.

Energy Security Policies

Global energy independence drives Europe and North America to localize battery supply chains, with the EU’s 2023 Critical Raw Materials Act targeting 80% domestic sourcing by 2030, creating market access barriers for Chinese-based CBAK while opening localized JV opportunities; political clean-energy mandates (IEA projects 4,500 TWh of battery storage demand by 2040) support long-term demand for CBAK’s residential and industrial storage solutions despite export constraints.

Local Government Support in China

CBAK Energy depends on municipal support in Dalian and Nanjing for land use, tax incentives and infrastructure, which enabled its latest 2024 cell production expansion funded partly by a reported RMB 200–300 million in local low-interest loans.

These partnerships accelerate factory build-out and capex deployment but expose CBAK to shifts in local leadership or policy: a change in priorities could slow permitting and reduce access to preferential financing, affecting planned capacity scaling.

- 2024 local low-interest loans ~RMB 200–300M

- Key sites: Dalian, Nanjing — primary for manufacturing expansion

- Risks: leadership changes, reprioritized regional economic plans

International Regulatory Alignment

As CBAK expands in light EVs and ESS, it must navigate varied battery-safety and data-security regimes across EU, US, China and ASEAN; EU battery regulation updates (Recast expected 2024–25) raise compliance costs—industry estimates show 5–8% higher OPEX for certified supply chains.

Political scrutiny on raw-material provenance (EU Critical Raw Materials Act, US CHIPS/IRA sourcing clauses) imposes stricter reporting—traceability rules push suppliers to disclose cobalt/nickel origins; 2024 audits show 30% more documentation requests for battery makers.

To manage political risk CBAK should diversify clients by region, strengthen board-level transparency and publish enhanced ESG and supply-chain due-diligence; firms with clear governance report 12–18% lower risk-premium in funding markets.

- Comply with evolving EU/US battery/data rules—expect 5–8% OPEX rise

- Prepare for increased raw-material provenance reporting—~30% more audits in 2024

- Diversify client geography and boost governance to lower political risk premium by ~12–18%

Trade frictions, subsidies and rules reshape EV supply chains—costs up, demand and funding rise

US-China trade tensions and potential tariffs/export controls (7.5–25% tariffs in 2023; tech controls considered 2024) threaten NASDAQ access and could raise input costs 5–12%; Chinese NEV subsidies sustained ~25% YoY EV growth in 2024 aiding battery demand; EU/US localization rules (EU CRM Act, IRA) increase compliance OPEX ~5–8% and audits ~30%; local loans ~RMB 200–300M supported 2024 expansion.

| Factor | 2023–24 Data | Impact |

|---|---|---|

| US tariffs/controls | 7.5–25% (2023); controls considered (2024) | Input cost +5–12% |

| China NEV support | ~25% YoY EV sales growth (2024) | Higher battery demand |

| Compliance/OPEX | EU/US rules → +5–8% OPEX | Margin pressure |

| Local financing | Loans ~RMB 200–300M (2024) | Enabled capex |

What is included in the product

Explores how macro-environmental factors uniquely affect CBAK Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to its battery manufacturing and energy storage markets.

Provides a clean, visually segmented PESTLE summary of CBAK Energy for quick reference in meetings or presentations, easily editable with notes to reflect regional or business-line specifics.

Economic factors

Raw Material Price Volatility

Raw material price volatility—particularly lithium, nickel, and cobalt—directly drives CBAK Energy’s COGS and margins; lithium averaged about $15,000/tonne in 2024 after a mid-2020s correction while nickel and cobalt traded near $22,000/tonne and $30,000/tonne respectively in 2025, exposing margin risk.

Price spikes from supply-demand imbalances can compress margins if CBAK cannot pass costs to customers, as seen in 2021–2022 episodes where spot surges exceeded 40% year-over-year.

Securing long-term offtake or investing upstream is crucial: companies locking multiyear contracts in 2023–2025 reported 5–12% operating margin stability versus peers relying on spot purchases.

Global Inflation and Interest Rates

Persistent global inflation—core CPI running near 3.5–4.5% in 2024–2025 in many markets—raises CBAK’s labor, logistics and factory input costs, squeezing margins on cathode and battery cells.

Higher policy rates (global average short-term rates rose to ~3.5% by end-2025) increases borrowing costs for CBAK’s capex and for consumers financing EVs, potentially slowing demand.

Against this backdrop, disciplined capital allocation and debt management are required to preserve liquidity and support measured expansion.

Growth of the Energy Storage Market

The global energy storage market grew to about 33 GWh of battery deployments in 2024, and BloombergNEF projects cumulative battery storage capacity to exceed 450 GWh by 2030, creating a strong economic tailwind for CBAK Energy as it pivots from EV cells; utility-scale and grid-tied projects—backed by $200+ billion renewable investments in 2024—demand large-format batteries and typically yield multi-year, stable contracts versus volatile consumer or light EV segments.

Currency Exchange Rate Fluctuations

CBAK reports in USD but generates most revenue/costs in RMB, exposing it to USD/RMB volatility; a 2023–2025 swing of roughly 6.7% (CNY weakening from ~6.3 to ~6.72 per USD in 2023–2024) can materially change reported revenue and net assets on NASDAQ filings.

US Fed rate decisions and PBOC easing in 2024–25 directly affect FX and funding costs, altering valuation multiples and investor sentiment toward CBAK.

- USD reporting vs RMB operations creates translation risk

- ~6–7% USD/RMB moves in 2023–24 illustrate magnitude

- Fed and PBOC policy shifts drive FX, funding, and valuation impacts

Consumer Purchasing Power

The demand for light electric vehicles and passenger EVs in China and Southeast Asia is tied to disposable income; China’s urban per capita disposable income rose 3.8% in 2024 while Southeast Asia real GDP averaged ~4.5% in 2024, but rising unemployment or slower growth could delay purchases and hit CBAK’s order book.

Monitoring GDP growth and consumer confidence—China’s 2024 GDP growth 5.2% and ASEAN consumer confidence indices down ~4–6% in late 2024—helps forecast production and inventory needs to avoid excess stock or missed deliveries.

- China urban disposable income +3.8% (2024)

- China GDP growth 5.2% (2024)

- ASEAN real GDP ~4.5% (2024)

- Consumer confidence down ~4–6% in late 2024

Commodity shocks, rising costs and FX risk cloud battery storage upside

Key economic risks: raw-material price swings (Li ~$15,000/t 2024; Ni ~$22,000/t, Co ~$30,000/t 2025) press margins; global core CPI ~3.5–4.5% (2024–25) and avg short rates ~3.5% (end-2025) raise input and funding costs; USD/RMB ~6.3→6.72 (2023–24) creates translation risk; battery storage demand ~33 GWh (2024) supports long-term contracts.

| Metric | Value |

|---|---|

| Li price (2024) | $15,000/t |

| Ni/Co (2025) | $22k / $30k/t |

| Core CPI (2024–25) | 3.5–4.5% |

| USD/RMB swing (2023–24) | ~6.3→6.72 |

| Storage deployments (2024) | 33 GWh |

What You See Is What You Get

CBAK Energy PESTLE Analysis

The preview shown here is the exact CBAK Energy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.