China Bohai Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Assess how regulatory shifts, economic cycles, and rapid fintech adoption are reshaping China Bohai Bank’s strategic outlook—our concise PESTLE snapshot highlights key external risks and opportunities you need to know. Purchase the full PESTLE analysis to access detailed, actionable intelligence and downloadable charts that power investment decisions and strategic plans.

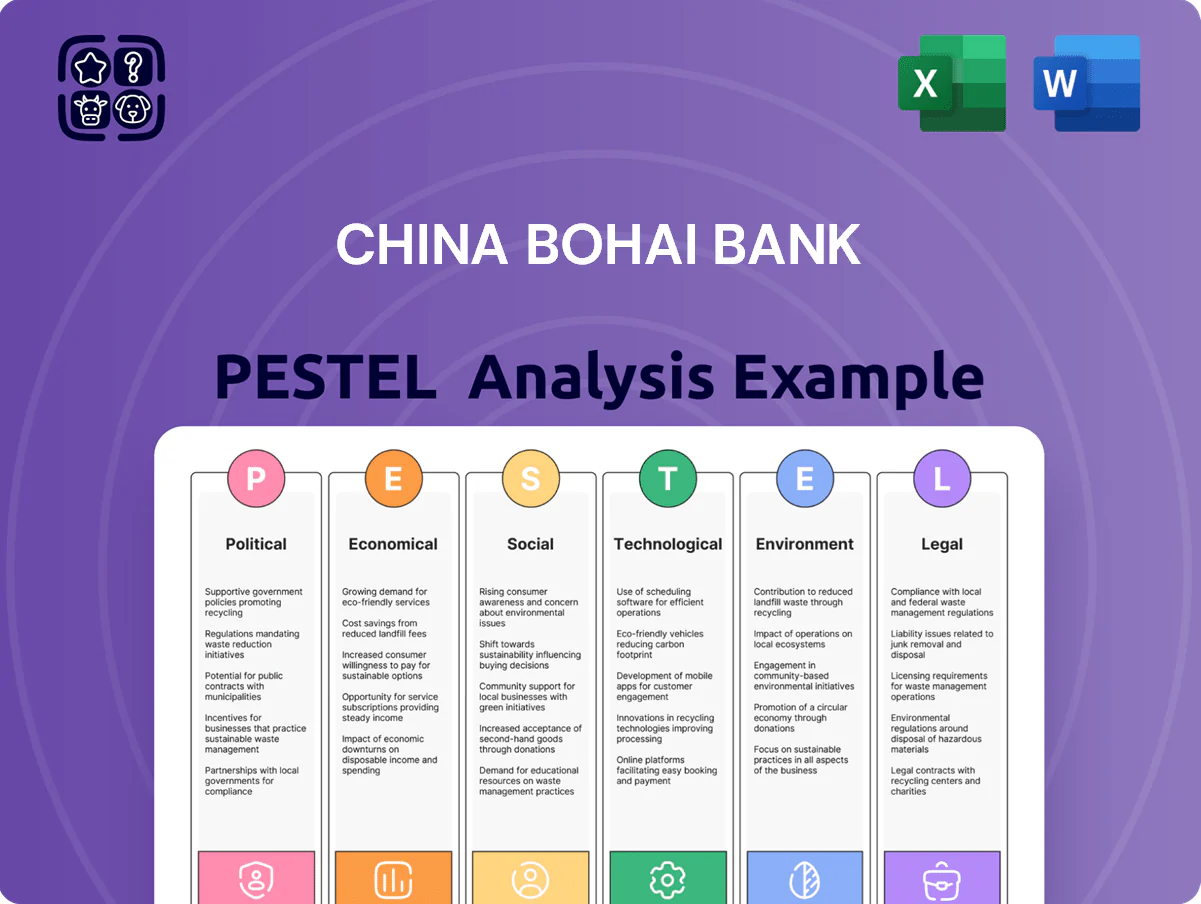

Political factors

Alignment with national strategic objectives

China Bohai Bank must align lending and investment with the 14th and 15th Five-Year Plans and Central Financial Work Conference directives, prioritizing high-tech manufacturing, strategic emerging industries and the digital economy; in 2024 China targeted 20% annual growth in strategic emerging sector output, guiding banks to increase sector exposure.

Local government influence and regional development

As a national joint-stock bank headquartered in Tianjin, Bohai Bank leverages strong ties with municipal governments, driving financing for Beijing‑Tianjin‑Hebei integration projects where it arranged an estimated CNY 120–150bn in regional infrastructure and industrial loans by end‑2024.

This political proximity grants preferential access to large-scale projects but concentrates exposure to local government financing vehicles (LGFVs), which comprised roughly 18% of the bank’s corporate loan book in 2024.

Municipal policy shifts—such as tighter LGFV deleveraging or land‑sale revenue fluctuations—can quickly affect asset quality and regional growth prospects, requiring active risk limits and close coordination with regulators.

Geopolitical tensions and cross-border operations

Ongoing geopolitical friction between China and Western economies has reduced correspondent banking links and raised compliance costs for Bohai Bank, which handled CNY 120bn in cross-border settlements in 2024; trade finance volumes grew 6% y/y but face sanction-related counterparty risks. Sanctions regimes and shifting trade alliances force investment in compliance—global AML/KYC spend rose ~15% industry-wide—affecting FX liquidity management and USD/CNH corridors. Supporting RMB internationalization and Belt and Road lending (China’s outbound loans to BRI partners ≈ $60bn in 2024) requires balancing commercial goals with national economic-security screening. Overseas expansion and partner selection are now vetted for geopolitical risk, constraining M&A and correspondent-network growth.

Common Prosperity and social equity mandates

The political push for Common Prosperity forces Bohai Bank to scale inclusive finance and rural revitalization, aligning with Beijing targets to cut SME financing costs by ~15% and boost rural lending—which grew 12% y/y in 2024—into its portfolio.

Mandates require improved access for underserved households and microenterprises, shifting priorities from pure profit to social outcomes; missed social-performance metrics risk regulatory penalties and reputational harm in China’s domestic market.

- Increase rural lending (2024: +12% y/y)

- Reduce SME financing costs (~15% target)

- Prioritize underserved access and microloans

- Regulatory/reputation risk if targets unmet

Party leadership and corporate governance

Strengthened Communist Party leadership in China’s financial sector ensures Bohai Bank’s corporate governance is aligned with state priorities; since 2018 Party committees have formal roles in governance across state-backed banks, reducing incidence of major regulatory breaches (nonperforming loans in provincial banks averaged 1.8% in 2024 vs 3.2% in 2016).

Centralized oversight aims to curb irregularities and hold management accountable to national interests; Party influence affects executive appointments and strategic plans, with board-level Party secretaries present in over 90% of joint-stock banks by 2024.

Investors must factor the dual-track governance—company boards plus Party committees—into assessments of Bohai Bank’s operational independence and risk management, as this structure can both mitigate systemic risk and constrain commercial agility.

- Party committees integrated into board processes; >90% presence (2024)

- Provincial bank NPLs fell to 1.8% (2024) from 3.2% (2016)

- Executive appointments influenced by Party oversight

- Dual-track governance impacts perceived operational independence

Bohai Bank tilts to high‑tech regional lending; LGFV concentration and compliance costs rise

Political alignment with Five‑Year Plans directs Bohai Bank toward high‑tech and regional integration lending; strategic sector output growth target ~20% (2024) guides portfolio tilt. Strong municipal ties enabled CNY 120–150bn regional loans (2024) but LGFVs made up ~18% of corporate book, raising concentration risk. Geopolitical tensions raised compliance costs (~+15% industry AML spend) and pressured FX corridors; Party committees (>90% banks) shape governance and executive appointments.

| Metric | 2024 |

|---|---|

| Strategic sector growth target | ~20% |

| Regional/infra loans arranged | CNY 120–150bn |

| LGFV share of corporate book | ~18% |

| Cross‑border settlements | CNY 120bn |

| Industry AML/KYC spend change | +15% |

| Party committee presence in joint‑stock banks | >90% |

What is included in the product

Explores how macro-environmental factors specifically impact China Bohai Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks, opportunities, and strategic actions.

A concise PESTLE snapshot of China Bohai Bank, segmented for quick risk assessment and strategic planning, enabling teams to drop key political, economic, social, technological, legal, and environmental points directly into presentations or meeting briefs.

Economic factors

Macroeconomic transition and GDP growth dynamics

China's shift from double-digit growth to targeted high-quality development has seen GDP growth moderate to about 5.2% in 2024 and IMF projecting ~4.8% for 2025, reducing traditional loan demand, notably in real estate where outstanding property sector loans fell 3.5% YoY in 2024.

For Bohai Bank this implies reallocating credit toward high-end services and green tech—sectors that attracted 18% of new corporate loans in 2024—requiring balance-sheet repricing to preserve NIMs.

Global volatility—2024 global trade growth near 2% and tighter US rates—heightens credit and market risk, so Bohai Bank must strengthen asset-liability management, stress testing, and liquidity buffers to sustain earnings.

Interest rate environment and margin compression

Persistent cuts in the Loan Prime Rate—LPR fell to 3.45% (1Y) by end-2025 from 3.65% in 2023—plus intense competition for deposits compressed joint-stock banks’ NIMs; Bohai Bank’s NIM narrowed to about 1.35% in 2024, down ~25 bps year-on-year.

With the PBOC keeping policy accommodative to support consumption and growth, Bohai must protect profitability amid narrowing spreads by optimizing liability mix and boosting low-cost deposits.

Management is targeting higher CASA and retail deposit growth and expanding fee-income: non-interest income rose to ~28% of operating income in 2024 as wealth management and fee-based services scale up.

Real estate sector restructuring and asset quality

The ongoing correction in China’s property market remains a primary economic concern for Bohai Bank, with sector-related loans comprising about 18% of its corporate loan book and contributing to a rise in non-performing loans to 2.9% in 2024 H2. Bohai has significant exposure to developers and suppliers and has joined state-led support programs, backing restructuring for projects totaling roughly CNY 45–60 billion. Stabilization of prices and successful debt restructurings are critical to restoring capital ratios and profitability. Continued pressure necessitates rigorous stress testing and higher provisioning—management increased loan loss reserves by 22% year-on-year into 2024.

Consumption recovery and retail banking potential

Economic stimulus measures—including 2024 targeted consumption coupons and a 2023–24 VAT/fee relief—support higher retail lending demand, offering Bohai Bank growth in personal loans and credit cards as household consumption recovered 5.2% YoY in 2024.

Rising middle-class incomes and urbanization drove retail financial asset growth; Chinese household financial assets reached CNY 291 trillion in 2024, increasing demand for customized wealth management products that Bohai Bank is targeting via digital retail transformation.

Bohai Bank’s investment in branch modernization and fintech partnerships aims to capture higher-margin consumer finance, but sensitivity to job market volatility—urban surveyed unemployment ~5.2% in 2024—could slow uptake and temper credit risk appetite.

- Stimulus + consumption recovery: 5.2% YoY (2024)

- Household financial assets: CNY 291 trillion (2024)

- Urban surveyed unemployment: ~5.2% (2024)

- Focus: loans, credit cards, wealth products via retail digitalization

Inflationary trends and monetary policy shifts

Fluctuations in domestic CPI—3.0% in 2024—alongside divergent global central bank tightening affect Bohai Bank's liquidity management and mark-to-market on bond portfolios.

PBoC's targeted tools, notably MLF operations totaling CNY 1.8 trillion in 2024, directly influence the bank's short-term funding costs and interbank liquidity.

Bohai Bank must keep treasury agile to manage yield-curve shifts and RMB moves (USD/CNY ~7.20 in early 2025) while macro-prudential rules adjust capital adequacy and leverage through the cycle.

- 2024 CPI 3.0%; MLF CNY 1.8T; USD/CNY ~7.20 (early 2025)

Bohai outlook: slowing growth, NIM squeeze, property risks — retail assets and fees shine

Bohai faces slower GDP (~5.2% 2024; IMF ~4.8% 2025), NIM pressure (1.35% 2024), 18% property exposure, NPLs 2.9% H2 2024, CASA/fee income rising (non-interest 28% 2024); PBoC tools (MLF CNY1.8T) and CPI 3.0% affect liquidity and bond MTM; retail opportunity: household assets CNY291T, consumption +5.2% 2024.

| Metric | Value |

|---|---|

| GDP growth 2024 | 5.2% |

| IMF 2025 | ~4.8% |

| NIM (2024) | 1.35% |

| Property exposure | 18% |

| NPLs H2 2024 | 2.9% |

| Household assets 2024 | CNY 291T |

| Consumption 2024 | +5.2% |

| MLF 2024 | CNY 1.8T |

Preview Before You Purchase

China Bohai Bank PESTLE Analysis

The preview shown here is the exact China Bohai Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Assess how regulatory shifts, economic cycles, and rapid fintech adoption are reshaping China Bohai Bank’s strategic outlook—our concise PESTLE snapshot highlights key external risks and opportunities you need to know. Purchase the full PESTLE analysis to access detailed, actionable intelligence and downloadable charts that power investment decisions and strategic plans.

Political factors

Alignment with national strategic objectives

China Bohai Bank must align lending and investment with the 14th and 15th Five-Year Plans and Central Financial Work Conference directives, prioritizing high-tech manufacturing, strategic emerging industries and the digital economy; in 2024 China targeted 20% annual growth in strategic emerging sector output, guiding banks to increase sector exposure.

Local government influence and regional development

As a national joint-stock bank headquartered in Tianjin, Bohai Bank leverages strong ties with municipal governments, driving financing for Beijing‑Tianjin‑Hebei integration projects where it arranged an estimated CNY 120–150bn in regional infrastructure and industrial loans by end‑2024.

This political proximity grants preferential access to large-scale projects but concentrates exposure to local government financing vehicles (LGFVs), which comprised roughly 18% of the bank’s corporate loan book in 2024.

Municipal policy shifts—such as tighter LGFV deleveraging or land‑sale revenue fluctuations—can quickly affect asset quality and regional growth prospects, requiring active risk limits and close coordination with regulators.

Geopolitical tensions and cross-border operations

Ongoing geopolitical friction between China and Western economies has reduced correspondent banking links and raised compliance costs for Bohai Bank, which handled CNY 120bn in cross-border settlements in 2024; trade finance volumes grew 6% y/y but face sanction-related counterparty risks. Sanctions regimes and shifting trade alliances force investment in compliance—global AML/KYC spend rose ~15% industry-wide—affecting FX liquidity management and USD/CNH corridors. Supporting RMB internationalization and Belt and Road lending (China’s outbound loans to BRI partners ≈ $60bn in 2024) requires balancing commercial goals with national economic-security screening. Overseas expansion and partner selection are now vetted for geopolitical risk, constraining M&A and correspondent-network growth.

Common Prosperity and social equity mandates

The political push for Common Prosperity forces Bohai Bank to scale inclusive finance and rural revitalization, aligning with Beijing targets to cut SME financing costs by ~15% and boost rural lending—which grew 12% y/y in 2024—into its portfolio.

Mandates require improved access for underserved households and microenterprises, shifting priorities from pure profit to social outcomes; missed social-performance metrics risk regulatory penalties and reputational harm in China’s domestic market.

- Increase rural lending (2024: +12% y/y)

- Reduce SME financing costs (~15% target)

- Prioritize underserved access and microloans

- Regulatory/reputation risk if targets unmet

Party leadership and corporate governance

Strengthened Communist Party leadership in China’s financial sector ensures Bohai Bank’s corporate governance is aligned with state priorities; since 2018 Party committees have formal roles in governance across state-backed banks, reducing incidence of major regulatory breaches (nonperforming loans in provincial banks averaged 1.8% in 2024 vs 3.2% in 2016).

Centralized oversight aims to curb irregularities and hold management accountable to national interests; Party influence affects executive appointments and strategic plans, with board-level Party secretaries present in over 90% of joint-stock banks by 2024.

Investors must factor the dual-track governance—company boards plus Party committees—into assessments of Bohai Bank’s operational independence and risk management, as this structure can both mitigate systemic risk and constrain commercial agility.

- Party committees integrated into board processes; >90% presence (2024)

- Provincial bank NPLs fell to 1.8% (2024) from 3.2% (2016)

- Executive appointments influenced by Party oversight

- Dual-track governance impacts perceived operational independence

Bohai Bank tilts to high‑tech regional lending; LGFV concentration and compliance costs rise

Political alignment with Five‑Year Plans directs Bohai Bank toward high‑tech and regional integration lending; strategic sector output growth target ~20% (2024) guides portfolio tilt. Strong municipal ties enabled CNY 120–150bn regional loans (2024) but LGFVs made up ~18% of corporate book, raising concentration risk. Geopolitical tensions raised compliance costs (~+15% industry AML spend) and pressured FX corridors; Party committees (>90% banks) shape governance and executive appointments.

| Metric | 2024 |

|---|---|

| Strategic sector growth target | ~20% |

| Regional/infra loans arranged | CNY 120–150bn |

| LGFV share of corporate book | ~18% |

| Cross‑border settlements | CNY 120bn |

| Industry AML/KYC spend change | +15% |

| Party committee presence in joint‑stock banks | >90% |

What is included in the product

Explores how macro-environmental factors specifically impact China Bohai Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks, opportunities, and strategic actions.

A concise PESTLE snapshot of China Bohai Bank, segmented for quick risk assessment and strategic planning, enabling teams to drop key political, economic, social, technological, legal, and environmental points directly into presentations or meeting briefs.

Economic factors

Macroeconomic transition and GDP growth dynamics

China's shift from double-digit growth to targeted high-quality development has seen GDP growth moderate to about 5.2% in 2024 and IMF projecting ~4.8% for 2025, reducing traditional loan demand, notably in real estate where outstanding property sector loans fell 3.5% YoY in 2024.

For Bohai Bank this implies reallocating credit toward high-end services and green tech—sectors that attracted 18% of new corporate loans in 2024—requiring balance-sheet repricing to preserve NIMs.

Global volatility—2024 global trade growth near 2% and tighter US rates—heightens credit and market risk, so Bohai Bank must strengthen asset-liability management, stress testing, and liquidity buffers to sustain earnings.

Interest rate environment and margin compression

Persistent cuts in the Loan Prime Rate—LPR fell to 3.45% (1Y) by end-2025 from 3.65% in 2023—plus intense competition for deposits compressed joint-stock banks’ NIMs; Bohai Bank’s NIM narrowed to about 1.35% in 2024, down ~25 bps year-on-year.

With the PBOC keeping policy accommodative to support consumption and growth, Bohai must protect profitability amid narrowing spreads by optimizing liability mix and boosting low-cost deposits.

Management is targeting higher CASA and retail deposit growth and expanding fee-income: non-interest income rose to ~28% of operating income in 2024 as wealth management and fee-based services scale up.

Real estate sector restructuring and asset quality

The ongoing correction in China’s property market remains a primary economic concern for Bohai Bank, with sector-related loans comprising about 18% of its corporate loan book and contributing to a rise in non-performing loans to 2.9% in 2024 H2. Bohai has significant exposure to developers and suppliers and has joined state-led support programs, backing restructuring for projects totaling roughly CNY 45–60 billion. Stabilization of prices and successful debt restructurings are critical to restoring capital ratios and profitability. Continued pressure necessitates rigorous stress testing and higher provisioning—management increased loan loss reserves by 22% year-on-year into 2024.

Consumption recovery and retail banking potential

Economic stimulus measures—including 2024 targeted consumption coupons and a 2023–24 VAT/fee relief—support higher retail lending demand, offering Bohai Bank growth in personal loans and credit cards as household consumption recovered 5.2% YoY in 2024.

Rising middle-class incomes and urbanization drove retail financial asset growth; Chinese household financial assets reached CNY 291 trillion in 2024, increasing demand for customized wealth management products that Bohai Bank is targeting via digital retail transformation.

Bohai Bank’s investment in branch modernization and fintech partnerships aims to capture higher-margin consumer finance, but sensitivity to job market volatility—urban surveyed unemployment ~5.2% in 2024—could slow uptake and temper credit risk appetite.

- Stimulus + consumption recovery: 5.2% YoY (2024)

- Household financial assets: CNY 291 trillion (2024)

- Urban surveyed unemployment: ~5.2% (2024)

- Focus: loans, credit cards, wealth products via retail digitalization

Inflationary trends and monetary policy shifts

Fluctuations in domestic CPI—3.0% in 2024—alongside divergent global central bank tightening affect Bohai Bank's liquidity management and mark-to-market on bond portfolios.

PBoC's targeted tools, notably MLF operations totaling CNY 1.8 trillion in 2024, directly influence the bank's short-term funding costs and interbank liquidity.

Bohai Bank must keep treasury agile to manage yield-curve shifts and RMB moves (USD/CNY ~7.20 in early 2025) while macro-prudential rules adjust capital adequacy and leverage through the cycle.

- 2024 CPI 3.0%; MLF CNY 1.8T; USD/CNY ~7.20 (early 2025)

Bohai outlook: slowing growth, NIM squeeze, property risks — retail assets and fees shine

Bohai faces slower GDP (~5.2% 2024; IMF ~4.8% 2025), NIM pressure (1.35% 2024), 18% property exposure, NPLs 2.9% H2 2024, CASA/fee income rising (non-interest 28% 2024); PBoC tools (MLF CNY1.8T) and CPI 3.0% affect liquidity and bond MTM; retail opportunity: household assets CNY291T, consumption +5.2% 2024.

| Metric | Value |

|---|---|

| GDP growth 2024 | 5.2% |

| IMF 2025 | ~4.8% |

| NIM (2024) | 1.35% |

| Property exposure | 18% |

| NPLs H2 2024 | 2.9% |

| Household assets 2024 | CNY 291T |

| Consumption 2024 | +5.2% |

| MLF 2024 | CNY 1.8T |

Preview Before You Purchase

China Bohai Bank PESTLE Analysis

The preview shown here is the exact China Bohai Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.