China Communications Construction Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

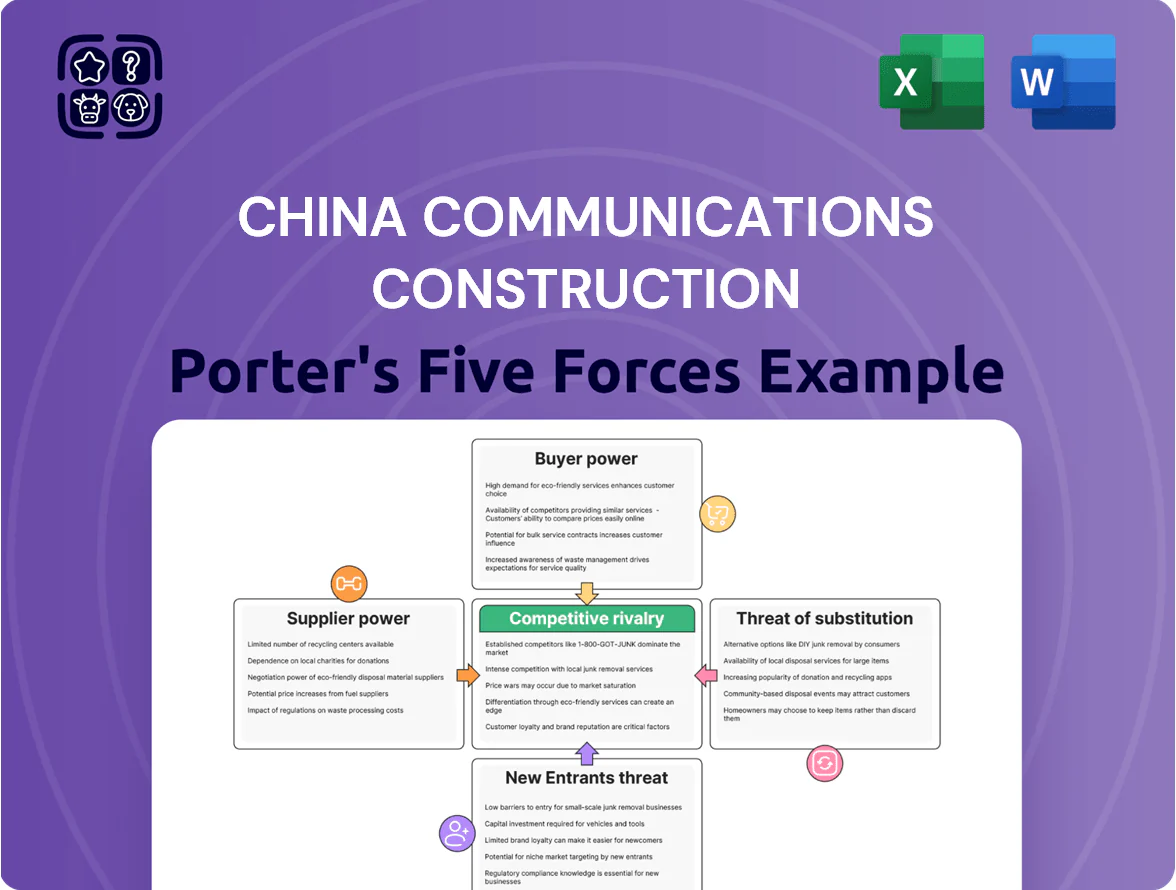

China Communications Construction (CCCC) operates in a capital-intensive, government-linked sector where supplier bargaining is moderate, buyer power varies by contract size, and barriers to entry are high—yet geopolitical risk and project-level competition raise rivalry and substitute risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CCCC’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

The cost of steel, cement and asphalt remains a key driver for China Communications Construction (CCCC); steel accounted for roughly 18% of construction input costs in 2024 and global steel prices swung ±22% year-to-year, raising exposure. By end-2025 supply-chain realignments and tighter emissions rules in China pushed cement and bitumen prices up ~12–15%, increasing volatility. CCCC uses long-term purchase contracts covering ~60% of volumes, but large projects mean a 3–5% supplier price rise can trim margins materially.

Dependence on Specialized Technology

For high-end projects like deep-water ports and advanced rail systems, CCCC depends on specialized components and high-tech machinery, giving suppliers of proprietary tunnel boring machines and advanced dredging sensors strong leverage due to few alternatives.

Major suppliers — e.g., TBM makers in Germany and dredging sensor firms in the Netherlands — control pricing and lead times, impacting project margins; in 2024 CCCC reported 7.8% higher procurement costs for imported equipment year-on-year.

That creates reliance on a small group of global tech providers, but CCCC is internalizing capabilities: its manufacturing divisions increased in-house production of key components by 18% in 2024, reducing supplier share in capex spend.

Labor Market Dynamics

The pool of skilled engineers and specialized construction workers has tightened, with China’s working-age population (15–59) falling 2.6% from 2015–2024 and median construction wages up about 45% in real terms by 2025, boosting supplier (labor) leverage for China Communications Construction on bids.

Energy and Fuel Requirements

Heavy dredging and construction make China Communications Construction Company (CCCC) highly exposed to energy price swings; marine diesel and bunker fuel accounted for an estimated 12–18% of operating costs on major projects in 2024, so state-owned and global fuel suppliers hold strong leverage.

The shift to low-carbon construction raised dependence on renewable tech and low-emission fuels—renewable fuel and electrification suppliers gained bargaining power as China tightened construction carbon rules aiming net-zero by 2060 and sector targets for carbon-neutral processes by mid-2020s.

Suppliers’ power grows as regulation, limited green-fuel supply, and higher capital costs for retrofit drive CCCC to accept premium pricing; green fuel premiums reached 15–30% over conventional bunker prices in 2024 on some routes.

- Energy = 12–18% project costs (2024 est.)

- Green fuel premium 15–30% (2024)

- Regulatory push for carbon-neutral processes by mid-2020s

State-Directed Sourcing Strategies

As a state-owned enterprise, China Communications Construction Company (CCCC) sources heavily from Chinese SOEs, creating a supplier relationship driven by national policy and coordination.

That yields stable supply: CCCC reported 78% of major material contracts with domestic SOEs in 2024, but it limits switching to lower-cost foreign suppliers when domestic prices rose 9% YoY in 2023.

The central government actively coordinates these ties to keep the port and infrastructure supply chain resilient against sanctions or trade shocks.

- 78% major contracts with domestic SOEs (2024)

- Domestic material prices +9% YoY (2023)

- State coordination reduces supply disruption risk

- Limited flexibility to pursue cheaper international inputs

Suppliers wield moderate–high power as steel, energy costs and green premiums squeeze margins

Suppliers hold moderate-to-high power: key inputs (steel ~18% of costs, energy 12–18% in 2024) and proprietary machinery give vendors leverage; 60% long-term contracts and 78% domestic SOE procurement (2024) temper but do not eliminate price risk—import equipment costs rose 7.8% in 2024 and green-fuel premiums hit 15–30%.

| Metric | 2024/25 |

|---|---|

| Steel share | ~18% |

| Energy share | 12–18% |

| Long-term contracts | ~60% |

| Domestic SOE sourcing | 78% |

| Imported equip. cost rise | +7.8% YoY |

| Green fuel premium | 15–30% |

What is included in the product

Tailored Porter's Five Forces overview for China Communications Construction that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive risks and protective market dynamics shaping pricing and profitability.

A concise Porter's Five Forces one-sheet for China Communications Construction—quickly spot supplier, buyer, and competitor pressures to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Public Sector Concentration

The vast majority of China Communications Construction Company (CCCC) projects—over 70% of contract value in 2024—are commissioned by national governments or state-backed agencies, giving buyers strong leverage over pricing and risk allocation. These clients set timelines, technical specs, and payment milestones, squeezing contractors’ negotiation space and margins; CCCC’s gross margin fell to 8.9% in FY2024. By 2025, consolidation of provincial procurement offices reduced vendor diversity by ~20%, further tilting power to buyers.

Belt and Road Initiative Geopolitics

International clients in Belt and Road Initiative (BRI) projects wield strong leverage, using diplomatic ties to reshape outcomes; for example, Pakistan and Malaysia secured loan term relaxations on over $30bn of CCCC-led projects by 2023.

These governments regularly demand concessional financing and local hiring quotas—often 15–30% local labor—raising CCCC’s costs and lowering margins.

CCCC must align project economics with Chinese state diplomacy, increasing buyer power and pushing win-rate sensitivity; delays or renegotiations occurred on ~22% of BRI contracts in 2022.

Rigorous Competitive Bidding

Rigorous, transparent bidding for ports and infrastructure lets customers compare multiple offers and push prices down; global tenders saw average bid spreads of 6–12% in 2024 for Chinese-led port projects. Even at CCCC (China Communications Construction Company Ltd., 2024 revenue RMB 346.6 billion), it must outbid global giants by offering leaner designs or lower unit costs. That power forces customers to demand higher quality and tighter delivery terms, squeezing contractors’ profit margins.

Financing and Credit Terms

Customers often demand that China Communications Construction (CCCC) provide or arrange project financing, letting buyers pick contractors with stronger financial flexibility; in 2024 CCCC reported RMB 400+ billion in contract assets, a proxy for financed work.

With global policy rates near 4–5% in 2024–25, access to low-cost capital is a key buyer criterion, raising switching power toward contractors who can offer cheaper financing.

Sovereign buyers, especially in BRI markets, shift financing risk onto contractors via PPPs and mobilisation guarantees, increasing CCCC’s contingent liabilities and credit exposure.

- CCCC contract assets ~RMB 400bn (2024)

- Global policy rates ~4–5% (2024–25)

- PPPs raise contractor contingent liabilities

Strict Performance and Safety Standards

Global buyers now demand strict ESG compliance, pushing China Communications Construction Company (CCCC) to meet standards like Equator Principles and ISO 45001; missing specs risks fines or exclusion—CCCClost a 2023 port tender in Africa after failing local environmental terms (estimated $120m project) and faces rising prequalification ESG thresholds of 30–40% across EU tenders as of 2025.

Customers now dictate execution details beyond engineering—supply-chain traceability, carbon caps, and worker safety clauses—shifting bargaining power toward buyers and increasing CCCC's compliance costs and bid risk.

- 30–40%: ESG weight in EU tender scoring (2025)

- $120m: reported lost 2023 port tender tied to environmental noncompliance

- Standards: Equator Principles, ISO 45001 commonly required

State buyers squeeze CCCC: low margins, vendor cuts, $30bn+ concessions, rising ESG costs

Buyers (mainly sovereigns/state agencies) hold strong leverage over CCCC—>70% govt work in 2024, forcing tighter specs, concessional finance, and lower margins (gross margin 8.9% FY2024); procurement consolidation cut vendor diversity ~20% by 2025. BRI clients extract loan/term concessions (>$30bn by 2023) and ESG prequalifications (30–40% EU tender weight 2025), raising compliance costs and contingent liabilities.

| Metric | Value |

|---|---|

| Govt/state share | >70% (2024) |

| Gross margin | 8.9% (FY2024) |

| Vendor diversity drop | ~20% (2025) |

| BRI loan concessions | >$30bn (by 2023) |

| ESG tender weight | 30–40% (EU, 2025) |

Full Version Awaits

China Communications Construction Porter's Five Forces Analysis

This preview shows the exact China Communications Construction Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, complete, and ready for use with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

China Communications Construction (CCCC) operates in a capital-intensive, government-linked sector where supplier bargaining is moderate, buyer power varies by contract size, and barriers to entry are high—yet geopolitical risk and project-level competition raise rivalry and substitute risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CCCC’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

The cost of steel, cement and asphalt remains a key driver for China Communications Construction (CCCC); steel accounted for roughly 18% of construction input costs in 2024 and global steel prices swung ±22% year-to-year, raising exposure. By end-2025 supply-chain realignments and tighter emissions rules in China pushed cement and bitumen prices up ~12–15%, increasing volatility. CCCC uses long-term purchase contracts covering ~60% of volumes, but large projects mean a 3–5% supplier price rise can trim margins materially.

Dependence on Specialized Technology

For high-end projects like deep-water ports and advanced rail systems, CCCC depends on specialized components and high-tech machinery, giving suppliers of proprietary tunnel boring machines and advanced dredging sensors strong leverage due to few alternatives.

Major suppliers — e.g., TBM makers in Germany and dredging sensor firms in the Netherlands — control pricing and lead times, impacting project margins; in 2024 CCCC reported 7.8% higher procurement costs for imported equipment year-on-year.

That creates reliance on a small group of global tech providers, but CCCC is internalizing capabilities: its manufacturing divisions increased in-house production of key components by 18% in 2024, reducing supplier share in capex spend.

Labor Market Dynamics

The pool of skilled engineers and specialized construction workers has tightened, with China’s working-age population (15–59) falling 2.6% from 2015–2024 and median construction wages up about 45% in real terms by 2025, boosting supplier (labor) leverage for China Communications Construction on bids.

Energy and Fuel Requirements

Heavy dredging and construction make China Communications Construction Company (CCCC) highly exposed to energy price swings; marine diesel and bunker fuel accounted for an estimated 12–18% of operating costs on major projects in 2024, so state-owned and global fuel suppliers hold strong leverage.

The shift to low-carbon construction raised dependence on renewable tech and low-emission fuels—renewable fuel and electrification suppliers gained bargaining power as China tightened construction carbon rules aiming net-zero by 2060 and sector targets for carbon-neutral processes by mid-2020s.

Suppliers’ power grows as regulation, limited green-fuel supply, and higher capital costs for retrofit drive CCCC to accept premium pricing; green fuel premiums reached 15–30% over conventional bunker prices in 2024 on some routes.

- Energy = 12–18% project costs (2024 est.)

- Green fuel premium 15–30% (2024)

- Regulatory push for carbon-neutral processes by mid-2020s

State-Directed Sourcing Strategies

As a state-owned enterprise, China Communications Construction Company (CCCC) sources heavily from Chinese SOEs, creating a supplier relationship driven by national policy and coordination.

That yields stable supply: CCCC reported 78% of major material contracts with domestic SOEs in 2024, but it limits switching to lower-cost foreign suppliers when domestic prices rose 9% YoY in 2023.

The central government actively coordinates these ties to keep the port and infrastructure supply chain resilient against sanctions or trade shocks.

- 78% major contracts with domestic SOEs (2024)

- Domestic material prices +9% YoY (2023)

- State coordination reduces supply disruption risk

- Limited flexibility to pursue cheaper international inputs

Suppliers wield moderate–high power as steel, energy costs and green premiums squeeze margins

Suppliers hold moderate-to-high power: key inputs (steel ~18% of costs, energy 12–18% in 2024) and proprietary machinery give vendors leverage; 60% long-term contracts and 78% domestic SOE procurement (2024) temper but do not eliminate price risk—import equipment costs rose 7.8% in 2024 and green-fuel premiums hit 15–30%.

| Metric | 2024/25 |

|---|---|

| Steel share | ~18% |

| Energy share | 12–18% |

| Long-term contracts | ~60% |

| Domestic SOE sourcing | 78% |

| Imported equip. cost rise | +7.8% YoY |

| Green fuel premium | 15–30% |

What is included in the product

Tailored Porter's Five Forces overview for China Communications Construction that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive risks and protective market dynamics shaping pricing and profitability.

A concise Porter's Five Forces one-sheet for China Communications Construction—quickly spot supplier, buyer, and competitor pressures to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Public Sector Concentration

The vast majority of China Communications Construction Company (CCCC) projects—over 70% of contract value in 2024—are commissioned by national governments or state-backed agencies, giving buyers strong leverage over pricing and risk allocation. These clients set timelines, technical specs, and payment milestones, squeezing contractors’ negotiation space and margins; CCCC’s gross margin fell to 8.9% in FY2024. By 2025, consolidation of provincial procurement offices reduced vendor diversity by ~20%, further tilting power to buyers.

Belt and Road Initiative Geopolitics

International clients in Belt and Road Initiative (BRI) projects wield strong leverage, using diplomatic ties to reshape outcomes; for example, Pakistan and Malaysia secured loan term relaxations on over $30bn of CCCC-led projects by 2023.

These governments regularly demand concessional financing and local hiring quotas—often 15–30% local labor—raising CCCC’s costs and lowering margins.

CCCC must align project economics with Chinese state diplomacy, increasing buyer power and pushing win-rate sensitivity; delays or renegotiations occurred on ~22% of BRI contracts in 2022.

Rigorous Competitive Bidding

Rigorous, transparent bidding for ports and infrastructure lets customers compare multiple offers and push prices down; global tenders saw average bid spreads of 6–12% in 2024 for Chinese-led port projects. Even at CCCC (China Communications Construction Company Ltd., 2024 revenue RMB 346.6 billion), it must outbid global giants by offering leaner designs or lower unit costs. That power forces customers to demand higher quality and tighter delivery terms, squeezing contractors’ profit margins.

Financing and Credit Terms

Customers often demand that China Communications Construction (CCCC) provide or arrange project financing, letting buyers pick contractors with stronger financial flexibility; in 2024 CCCC reported RMB 400+ billion in contract assets, a proxy for financed work.

With global policy rates near 4–5% in 2024–25, access to low-cost capital is a key buyer criterion, raising switching power toward contractors who can offer cheaper financing.

Sovereign buyers, especially in BRI markets, shift financing risk onto contractors via PPPs and mobilisation guarantees, increasing CCCC’s contingent liabilities and credit exposure.

- CCCC contract assets ~RMB 400bn (2024)

- Global policy rates ~4–5% (2024–25)

- PPPs raise contractor contingent liabilities

Strict Performance and Safety Standards

Global buyers now demand strict ESG compliance, pushing China Communications Construction Company (CCCC) to meet standards like Equator Principles and ISO 45001; missing specs risks fines or exclusion—CCCClost a 2023 port tender in Africa after failing local environmental terms (estimated $120m project) and faces rising prequalification ESG thresholds of 30–40% across EU tenders as of 2025.

Customers now dictate execution details beyond engineering—supply-chain traceability, carbon caps, and worker safety clauses—shifting bargaining power toward buyers and increasing CCCC's compliance costs and bid risk.

- 30–40%: ESG weight in EU tender scoring (2025)

- $120m: reported lost 2023 port tender tied to environmental noncompliance

- Standards: Equator Principles, ISO 45001 commonly required

State buyers squeeze CCCC: low margins, vendor cuts, $30bn+ concessions, rising ESG costs

Buyers (mainly sovereigns/state agencies) hold strong leverage over CCCC—>70% govt work in 2024, forcing tighter specs, concessional finance, and lower margins (gross margin 8.9% FY2024); procurement consolidation cut vendor diversity ~20% by 2025. BRI clients extract loan/term concessions (>$30bn by 2023) and ESG prequalifications (30–40% EU tender weight 2025), raising compliance costs and contingent liabilities.

| Metric | Value |

|---|---|

| Govt/state share | >70% (2024) |

| Gross margin | 8.9% (FY2024) |

| Vendor diversity drop | ~20% (2025) |

| BRI loan concessions | >$30bn (by 2023) |

| ESG tender weight | 30–40% (EU, 2025) |

Full Version Awaits

China Communications Construction Porter's Five Forces Analysis

This preview shows the exact China Communications Construction Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, complete, and ready for use with no placeholders or samples.