China Eastern Airlines Porter's Five Forces Analysis

Don't Miss the Bigger Picture

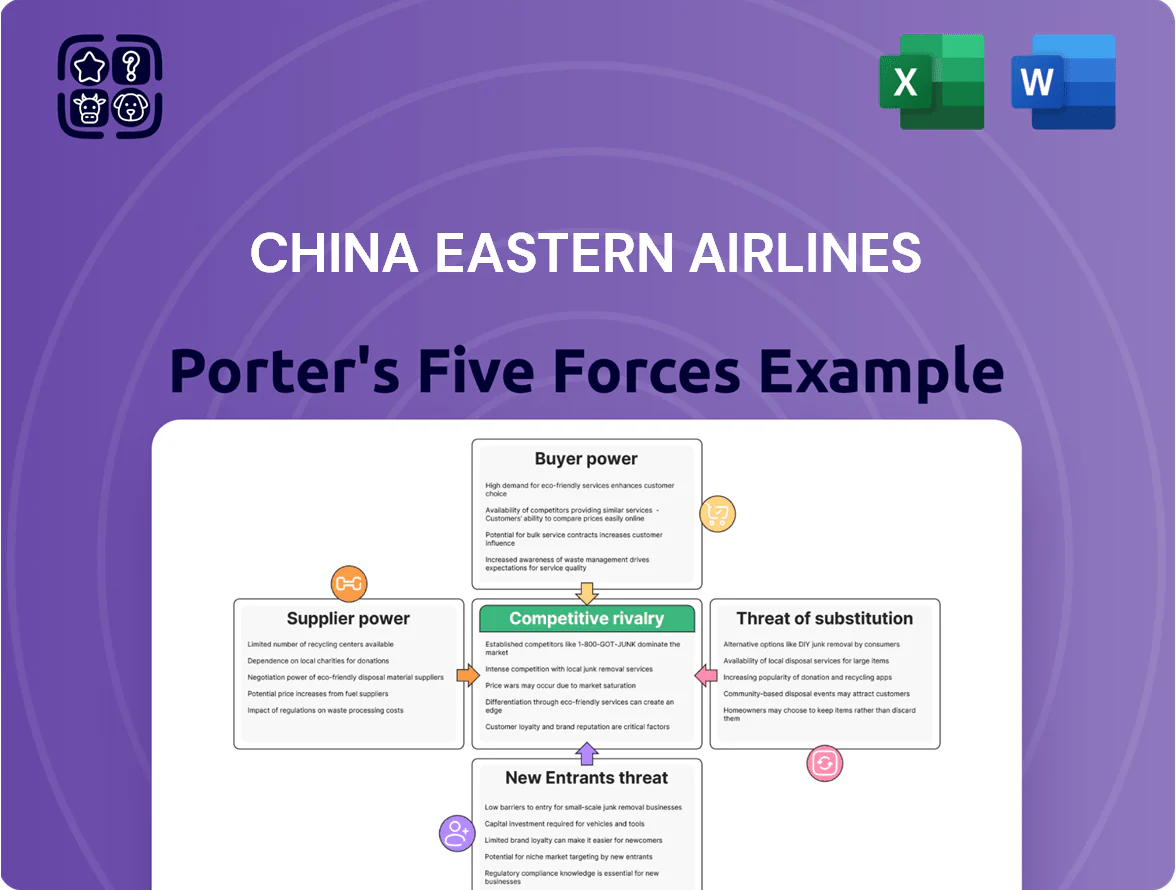

China Eastern Airlines operates in a capital-intensive, state-influenced market with moderate buyer power, concentrated supplier leverage (aircraft and fuel), significant rivalry among domestic and regional carriers, low threat of substitutes for long-haul travel but moderate for short-haul, and regulatory barriers that raise entry costs and shape competition.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Eastern Airlines’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Aircraft Manufacturers

The commercial-aircraft market is effectively a Boeing-Airbus duopoly, though COMAC’s C919 has given China Eastern a domestic option; by end-2025 China Eastern operated about 25 C919s alongside 400+ total aircraft.

For long-haul wide-bodies the airline still depends on Boeing 787s and Airbus A330/A350s, so a few suppliers hold strong bargaining power over price, delivery slots, and maintenance contracts, squeezing margins and flexibility.

Volatility of Jet Fuel Supply

Jet fuel accounts for about 23% of China Eastern Airlines’ operating costs in 2024, and prices track Brent crude, so global oil swings and geopolitics drive cost spikes beyond the airline’s control.

State-owned refiners in China give supply stability, but domestic prices still follow international benchmarks and OPEC moves, keeping suppliers’ leverage high.

China Eastern hedges fuel (reported $1.1bn notional hedges in 2024) to cushion shocks, but ultimate pricing power stays with energy producers and market regulators.

Control of Airport Slots and Infrastructure

Access to take-off and landing slots at Shanghai Pudong and Hongqiao is controlled by government-affiliated airport authorities, giving suppliers direct control over China Eastern’s route capacity and scheduling.

These authorities dictate timing and frequency; with Shanghai airports handling ~140 million combined passengers in 2023, limited peak-hour slots sharply affect yield and fleet utilization.

Because slots are finite and highly regulated, China Eastern (market cap ~CN¥120bn in 2025) must sustain strong ties and slot exchanges to protect revenue and network position.

Dependence on Specialized Engine Manufacturers

China Eastern relies on a handful of engine makers—General Electric, Rolls-Royce, and Pratt & Whitney—for engines and technical support, a supply base concentrated among top OEMs.

Engines need specialized MRO (maintenance, repair, overhaul) tied to long-term, often exclusive contracts; global OEMs captured about 70% of commercial engine aftermarket revenue in 2024, raising supplier leverage.

This technical lock-in raises switching costs and gives suppliers strong bargaining power over lifecycle costs, spares pricing, and turnaround times—impacting fleet economics and CAPEX planning.

- Dependence: few OEMs (GE, RR, P&W)

- MRO concentration: OEMs ~70% aftermarket share (2024)

- High switching costs: exclusive long-term contracts

- Outcome: elevated supplier bargaining on lifecycle costs

Scarcity of Certified Pilots and Technical Staff

Demand for licensed pilots and certified aviation engineers in China rose with passenger traffic recovering to 82% of 2019 levels by 2024, keeping skill supply tight and pushing avg. pilot pay up ~12% year-on-year through 2024.

China Eastern competes with Air China and international carriers for a limited talent pool, raising labor costs and maintenance outsourcing; in 2024 crew costs made up about 18% of operating expenses.

This scarcity gives pilot unions and specialized technicians leverage to negotiate higher wages, better rosters, and richer benefits, increasing fixed labor commitments and unit cost pressure.

- Pilot pay +12% YoY (2024)

- Crew costs ~18% of opex (2024)

- Passenger traffic 82% of 2019 (2024)

High supplier power, fuel & staffing squeeze airlines—OEMs dominate aftermarket

Supplier power is high: airframe OEMs Boeing/Airbus duopoly (COMAC niche) and engine OEMs GE/RR/P&W dominate pricing, delivery and MRO—OEMs held ~70% of engine aftermarket revenue in 2024.

Fuel suppliers and geopolitics drive cost volatility—jet fuel ≈23% of opex in 2024; China Eastern had $1.1bn fuel hedges that year.

Airport slot control in Shanghai (≈140m pax 2023) and tight pilot/engineer supply (pilot pay +12% YoY 2024; crew ≈18% opex) add leverage.

| Metric | 2024/2025 |

|---|---|

| Jet fuel share of opex | 23% |

| Fuel hedges (notional) | $1.1bn |

| Engine aftermarket share (OEMs) | ~70% |

| Pilot pay change | +12% YoY |

| Crew costs of opex | ~18% |

| Shanghai airports pax (2023) | ~140m |

What is included in the product

Tailored Porter’s Five Forces for China Eastern Airlines: assesses competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and regulatory restraints—highlighting key drivers of profitability, emerging low-cost and international rivals, supplier concentration, and barriers that protect incumbents.

A concise Porter's Five Forces snapshot for China Eastern Airlines—instantly highlights competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes to guide strategic moves.

Customers Bargaining Power

High Price Sensitivity of Leisure Travelers

Low Switching Costs for Passengers

For most domestic and short-haul international routes, passengers face minimal switching costs, so they can pick competitors based on price or schedule; China Eastern lost market share to low-cost rivals in 2024, with China’s LCC capacity up ~9% year-over-year. Frequent flyer program Eastern Miles raises retention but rarely offsets a fare gap of 10–20% or a better timing; surveys show <30% of Chinese leisure flyers cite loyalty as primary choice. This ease of switching forces China Eastern to keep fares competitive and service quality high to protect yield and load factors.

Influence of Online Travel Agencies

Platforms such as Trip.com Group and Meituan control over 40% of online ticket distribution in China (2024), giving them leverage via search rankings, promo bundles, and integrated hotel/transport packages that steer customer choice.

China Eastern must negotiate commission rates often ranging 8–15% and data-sharing terms, which raises distribution costs and limits direct customer capture.

This shifts bargaining power toward digital distributors, constraining China Eastern’s pricing flexibility and loyalty-program effectiveness.

Volume Leverage of Corporate Clients

Large corporations and government bodies that buy tickets in bulk can demand deep corporate fares and flexible terms; in 2024 China Eastern reported corporate and cargo together made up roughly 28% of passenger revenue, so these clients directly affect premium-cabin yields.

During contract renewals institutional buyers wield leverage because they supply steady, high-yield seats; losing one large account can cut premium revenue noticeably in peak routes.

China Eastern must deliver tailored service, dedicated sales teams, and incentives—such as dynamic rebates or route guarantees—to keep accounts in a crowded domestic and international market.

- Corporate share ≈28% of passenger revenue (2024)

- High-volume clients influence premium-cabin yields

- Tailored services + rebates reduce churn risk

Impact of Social Media and Public Perception

In China’s connected market, Weibo and WeChat feedback can swing China Eastern Airlines’ reputation and bookings within 24–72 hours; a 2019 study showed 60% of Chinese travelers change carriers after negative social posts.

A single viral safety or service incident can cut short-term load factors by 5–12% and force fare discounts to restore trust, hitting revenue per ASK (RASK) immediately.

The real-time feedback loop raises customer power, holding the airline accountable for punctuality, cleanliness, staff conduct, and crisis communication.

- 60% of travelers switch after negative posts

- Reputation hits can drop load factor 5–12%

- Brands must manage 24–72 hour viral cycles

- Immediate fare cuts lower RASK until trust returns

High customer leverage: leisure-driven volumes, heavy online bookings, reputation risk hits

| Metric | 2024 |

|---|---|

| Leisure share | 58% |

| Load factor | ~79% |

| LCC capacity change | +9% YoY |

| Online distribution | >40% |

| Commissions | 8–15% |

| Corporate rev | ~28% |

| Reputation hit | LF −5–12% |

Preview the Actual Deliverable

China Eastern Airlines Porter's Five Forces Analysis

This preview shows the exact China Eastern Airlines Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use; the document covers bargaining power of suppliers and buyers, threat of new entrants and substitutes, and competitive rivalry with concise strategic implications.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

China Eastern Airlines operates in a capital-intensive, state-influenced market with moderate buyer power, concentrated supplier leverage (aircraft and fuel), significant rivalry among domestic and regional carriers, low threat of substitutes for long-haul travel but moderate for short-haul, and regulatory barriers that raise entry costs and shape competition.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Eastern Airlines’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Aircraft Manufacturers

The commercial-aircraft market is effectively a Boeing-Airbus duopoly, though COMAC’s C919 has given China Eastern a domestic option; by end-2025 China Eastern operated about 25 C919s alongside 400+ total aircraft.

For long-haul wide-bodies the airline still depends on Boeing 787s and Airbus A330/A350s, so a few suppliers hold strong bargaining power over price, delivery slots, and maintenance contracts, squeezing margins and flexibility.

Volatility of Jet Fuel Supply

Jet fuel accounts for about 23% of China Eastern Airlines’ operating costs in 2024, and prices track Brent crude, so global oil swings and geopolitics drive cost spikes beyond the airline’s control.

State-owned refiners in China give supply stability, but domestic prices still follow international benchmarks and OPEC moves, keeping suppliers’ leverage high.

China Eastern hedges fuel (reported $1.1bn notional hedges in 2024) to cushion shocks, but ultimate pricing power stays with energy producers and market regulators.

Control of Airport Slots and Infrastructure

Access to take-off and landing slots at Shanghai Pudong and Hongqiao is controlled by government-affiliated airport authorities, giving suppliers direct control over China Eastern’s route capacity and scheduling.

These authorities dictate timing and frequency; with Shanghai airports handling ~140 million combined passengers in 2023, limited peak-hour slots sharply affect yield and fleet utilization.

Because slots are finite and highly regulated, China Eastern (market cap ~CN¥120bn in 2025) must sustain strong ties and slot exchanges to protect revenue and network position.

Dependence on Specialized Engine Manufacturers

China Eastern relies on a handful of engine makers—General Electric, Rolls-Royce, and Pratt & Whitney—for engines and technical support, a supply base concentrated among top OEMs.

Engines need specialized MRO (maintenance, repair, overhaul) tied to long-term, often exclusive contracts; global OEMs captured about 70% of commercial engine aftermarket revenue in 2024, raising supplier leverage.

This technical lock-in raises switching costs and gives suppliers strong bargaining power over lifecycle costs, spares pricing, and turnaround times—impacting fleet economics and CAPEX planning.

- Dependence: few OEMs (GE, RR, P&W)

- MRO concentration: OEMs ~70% aftermarket share (2024)

- High switching costs: exclusive long-term contracts

- Outcome: elevated supplier bargaining on lifecycle costs

Scarcity of Certified Pilots and Technical Staff

Demand for licensed pilots and certified aviation engineers in China rose with passenger traffic recovering to 82% of 2019 levels by 2024, keeping skill supply tight and pushing avg. pilot pay up ~12% year-on-year through 2024.

China Eastern competes with Air China and international carriers for a limited talent pool, raising labor costs and maintenance outsourcing; in 2024 crew costs made up about 18% of operating expenses.

This scarcity gives pilot unions and specialized technicians leverage to negotiate higher wages, better rosters, and richer benefits, increasing fixed labor commitments and unit cost pressure.

- Pilot pay +12% YoY (2024)

- Crew costs ~18% of opex (2024)

- Passenger traffic 82% of 2019 (2024)

High supplier power, fuel & staffing squeeze airlines—OEMs dominate aftermarket

Supplier power is high: airframe OEMs Boeing/Airbus duopoly (COMAC niche) and engine OEMs GE/RR/P&W dominate pricing, delivery and MRO—OEMs held ~70% of engine aftermarket revenue in 2024.

Fuel suppliers and geopolitics drive cost volatility—jet fuel ≈23% of opex in 2024; China Eastern had $1.1bn fuel hedges that year.

Airport slot control in Shanghai (≈140m pax 2023) and tight pilot/engineer supply (pilot pay +12% YoY 2024; crew ≈18% opex) add leverage.

| Metric | 2024/2025 |

|---|---|

| Jet fuel share of opex | 23% |

| Fuel hedges (notional) | $1.1bn |

| Engine aftermarket share (OEMs) | ~70% |

| Pilot pay change | +12% YoY |

| Crew costs of opex | ~18% |

| Shanghai airports pax (2023) | ~140m |

What is included in the product

Tailored Porter’s Five Forces for China Eastern Airlines: assesses competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and regulatory restraints—highlighting key drivers of profitability, emerging low-cost and international rivals, supplier concentration, and barriers that protect incumbents.

A concise Porter's Five Forces snapshot for China Eastern Airlines—instantly highlights competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes to guide strategic moves.

Customers Bargaining Power

High Price Sensitivity of Leisure Travelers

Low Switching Costs for Passengers

For most domestic and short-haul international routes, passengers face minimal switching costs, so they can pick competitors based on price or schedule; China Eastern lost market share to low-cost rivals in 2024, with China’s LCC capacity up ~9% year-over-year. Frequent flyer program Eastern Miles raises retention but rarely offsets a fare gap of 10–20% or a better timing; surveys show <30% of Chinese leisure flyers cite loyalty as primary choice. This ease of switching forces China Eastern to keep fares competitive and service quality high to protect yield and load factors.

Influence of Online Travel Agencies

Platforms such as Trip.com Group and Meituan control over 40% of online ticket distribution in China (2024), giving them leverage via search rankings, promo bundles, and integrated hotel/transport packages that steer customer choice.

China Eastern must negotiate commission rates often ranging 8–15% and data-sharing terms, which raises distribution costs and limits direct customer capture.

This shifts bargaining power toward digital distributors, constraining China Eastern’s pricing flexibility and loyalty-program effectiveness.

Volume Leverage of Corporate Clients

Large corporations and government bodies that buy tickets in bulk can demand deep corporate fares and flexible terms; in 2024 China Eastern reported corporate and cargo together made up roughly 28% of passenger revenue, so these clients directly affect premium-cabin yields.

During contract renewals institutional buyers wield leverage because they supply steady, high-yield seats; losing one large account can cut premium revenue noticeably in peak routes.

China Eastern must deliver tailored service, dedicated sales teams, and incentives—such as dynamic rebates or route guarantees—to keep accounts in a crowded domestic and international market.

- Corporate share ≈28% of passenger revenue (2024)

- High-volume clients influence premium-cabin yields

- Tailored services + rebates reduce churn risk

Impact of Social Media and Public Perception

In China’s connected market, Weibo and WeChat feedback can swing China Eastern Airlines’ reputation and bookings within 24–72 hours; a 2019 study showed 60% of Chinese travelers change carriers after negative social posts.

A single viral safety or service incident can cut short-term load factors by 5–12% and force fare discounts to restore trust, hitting revenue per ASK (RASK) immediately.

The real-time feedback loop raises customer power, holding the airline accountable for punctuality, cleanliness, staff conduct, and crisis communication.

- 60% of travelers switch after negative posts

- Reputation hits can drop load factor 5–12%

- Brands must manage 24–72 hour viral cycles

- Immediate fare cuts lower RASK until trust returns

High customer leverage: leisure-driven volumes, heavy online bookings, reputation risk hits

| Metric | 2024 |

|---|---|

| Leisure share | 58% |

| Load factor | ~79% |

| LCC capacity change | +9% YoY |

| Online distribution | >40% |

| Commissions | 8–15% |

| Corporate rev | ~28% |

| Reputation hit | LF −5–12% |

Preview the Actual Deliverable

China Eastern Airlines Porter's Five Forces Analysis

This preview shows the exact China Eastern Airlines Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use; the document covers bargaining power of suppliers and buyers, threat of new entrants and substitutes, and competitive rivalry with concise strategic implications.