Ceconomy PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and rapid tech adoption are reshaping Ceconomy's prospects in our concise PESTLE snapshot—perfect for investors and strategists seeking immediate clarity. Purchase the full PESTLE analysis to unlock detailed risk assessments, regulatory impacts, and actionable opportunities tailored to Ceconomy. Download now for a ready-to-use, fully editable report that accelerates smarter decisions.

Political factors

European trade policy and internal market stability

Ceconomy’s cross-border operations rely on the EU Single Market; intra-EU trade accounted for roughly 75% of its 2024 supply-chain movements, lowering tariffs and paperwork across 10+ countries where it operates.

Standardized regulations and trade agreements enabled inventory turnover improvements, supporting gross margin recovery to 18.1% in FY 2024.

Any shift toward protectionism or altered intra-EU trade relations by late 2025 could raise logistics costs and lead times, risking inventory write-downs and EBITDA volatility.

Geopolitical tensions affecting supply chain security

Ongoing geopolitical instability in Eastern Europe and trade frictions between Western nations and Asian manufacturing hubs remain critical risks for electronics retailers; by Q4 2025 global semiconductor spot prices rose ~12% YoY, squeezing margins. As of late 2025 these tensions continue to disrupt availability and push lead times for chips and finished goods to averages of 18–22 weeks versus 12–16 in 2023. Ceconomy must diversify suppliers—already expanding sourcing from Turkey and Vietnam—and allocate capital to buffer logistics delays, given that supply-chain disruptions lifted working capital needs by an estimated €180–220m in 2024–25.

National labor and wage regulations in Germany

As a major German employer, Ceconomy faces direct impact from domestic labor policies and the 2024 statutory minimum wage of 12.41 EUR/hr (planned increases to 12.82 EUR/hr in 2025), raising wage bills across its ~43,000 employees. Changes to employer social security contributions and tighter working-hour regulations can increase personnel costs, already ~60% of store operating expenses, squeezing margins. By end-2025, labor reforms force Ceconomy to balance higher compensation with leaner store staffing and automation investments to protect EBITDA, which was 4.1% in FY2023/24.

EU digital sovereignty and platform regulation

The Digital Markets Act, effective since March 2024, forces gatekeepers to open ecosystems, improving market access for Ceconomy against US e-commerce giants; EU rules could raise Ceconomy marketplace revenue share, supporting its 2024 goal to grow online sales beyond the 30% group target.

EU digital sovereignty pushes stricter data residency and vendor scrutiny—impacting Ceconomy’s data handling and contracts with non-EU tech providers after 2024 regulatory updates.

- DMA enforcement from 2024 levels playing field vs gatekeepers

- Ceconomy online sales target >30% (2024 strategic objective)

- Increased data residency and vendor controls affecting non-EU suppliers

Governmental incentives for energy-efficient transitions

Political initiatives reducing household energy use have increased demand for high-efficiency appliances at MediaMarkt and Saturn; EU energy-efficiency standards and national schemes lifted smart appliance sales by ~18% YoY in 2024.

Subsidies and tax breaks for greener upgrades—e.g., Germany’s 2024 appliance subsidy and Italy’s ecobonus—boost Ceconomy’s white goods revenue, supporting a ~3–5% uplift in segment sales in 2024.

By 2025, climate-target pressures solidified these incentives across key EU markets, making them a structural tailwind for Ceconomy’s appliance mix and average selling price growth.

- EU/national incentives increased smart/high-efficiency appliance demand ~18% YoY in 2024

- White goods sales gain ~3–5% revenue uplift in 2024 from subsidies

- Incentives became permanent policy across major EU markets by 2025

Ceconomy faces EU reliance, rising wages and DMA-driven online growth

Political risks for Ceconomy include EU Single Market dependence (≈75% intra‑EU supply flows in 2024), rising labor costs from Germany’s €12.41→€12.82/hr min wage (2024–25) affecting ~43,000 staff, DMA-driven improved marketplace access boosting online sales target >30% (2024), and energy-efficiency subsidies that lifted white‑goods sales ~3–5% in 2024.

| Metric | Value |

|---|---|

| Intra‑EU supply share 2024 | ≈75% |

| Employees | ≈43,000 |

| Min wage 2024→25 | €12.41→€12.82/hr |

| Online sales target | >30% |

| White‑goods uplift 2024 | 3–5% |

What is included in the product

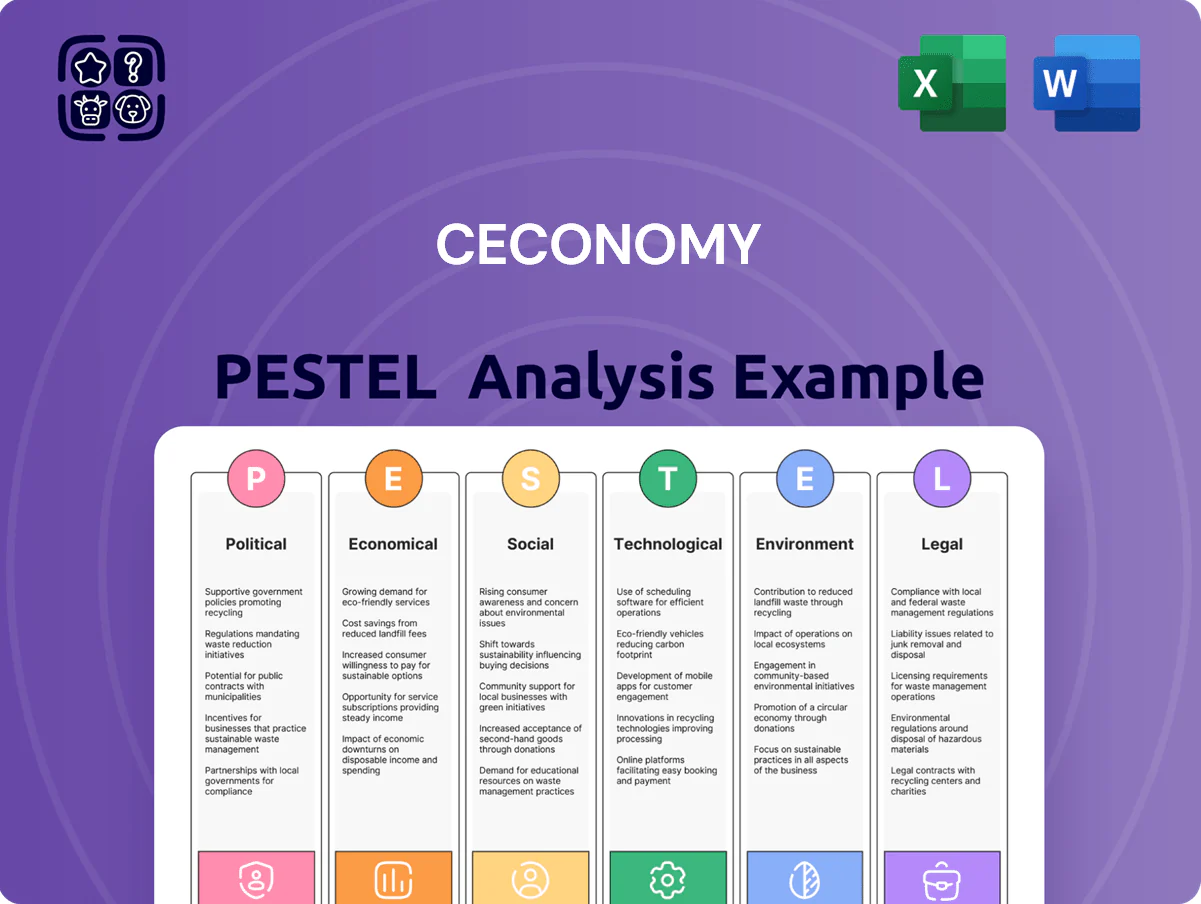

Explores how external macro-environmental factors uniquely affect Ceconomy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

A concise, shareable Ceconomy PESTLE summary that’s visually segmented for quick reference, letting teams drop it into presentations, annotate for local context, and rapidly align on external risks and strategic positioning.

Economic factors

Inflationary pressures and consumer purchasing power

While headline inflation eased to 2.7% by December 2025 from peaks above 8% in 2022–23, cumulative real-income loss left German household real incomes down about 4% versus pre‑pandemic levels, pressuring discretionary spend; high housing and energy costs (energy bills up ~15% YoY in 2024) push consumers to delay premium electronics. Ceconomy counters with value-focused assortments and expanded financing—installment uptake rose ~20% in 2024—to sustain volumes.

Eurozone interest rate environment

The ECB lifted its deposit rate to 4.00% by mid-2024 and signaled a pause through late 2025, raising Ceconomy’s borrowing costs and increasing inventory carry expenses; higher rates also pressured consumer credit, with Euro area household loan rates averaging ~6.2% in 2024. A stabilizing trajectory toward end-2025 supports steadier capex planning and bolsters demand for installment financing, which accounted for ~28% of Ceconomy’s POS financing in 2023.

Rise of the refurbished and second-hand market

Economic constraints and a stronger value focus have driven a 12% global CAGR for refurbished electronics (2020–2025); Ceconomy expanded trade-in programs and launched 'as-new' lines, with refurbished sales contributing an estimated €250m in FY2024, targeting budget-conscious consumers.

This trend pressures new-product margins—used devices often sell 30–50% cheaper—but offers Ceconomy a chance to increase customer lifetime value and loyalty via sustainable, lower-cost offerings and recurring service revenue.

Competition from low-cost international e-commerce platforms

The expansion of Asian direct-to-consumer platforms, which cut prices by up to 20–30% on standardized electronics, intensifies margin pressure on Ceconomy’s consumer electronics lines.

Ceconomy must differentiate via its 1,000+ German stores and service-led Solution business, aiming to offset price gaps with in‑store expertise and installation services.

By end‑2025 the strategy targets integrated omnichannel pricing parity plus local advisory revenue growth to stabilize gross margins.

- Asian D2C price cuts: 20–30%

- Ceconomy retail footprint: 1,000+ stores

- Strategy: combine competitive online pricing with local expert services by 2025

Labor market shortages and rising operational costs

Ceconomy faces rising personnel expenses as Europe’s tight labor market—EU unemployment ~6.2% (2025) but acute shortages in logistics/technical roles—pushes wage costs; FY 2024 personnel expenses rose ~4-6% YoY in retail peers, pressuring margins.

Attracting skilled staff for service hubs while managing store payrolls forces investment in automation and digital self-service; Ceconomy has accelerated self-checkout and remote diagnostics to contain labor-related OPEX and improve throughput.

- EU unemployment ~6.2% (2025) with shortages in logistics/tech

- Retail personnel costs up ~4-6% YoY in 2024 peers

- Increased investment in self-checkout, remote diagnostics, and automation

Ceconomy weathers weak real incomes, rising rates as refurbished sales surge to €250m

Slower real-income recovery (household real incomes ~4% below pre‑pandemic by 2025) and 2.7% inflation in Dec 2025 reduced discretionary spend; ECB rates ~4.00% through 2025 lifted borrowing/inventory costs and pushed household loan rates to ~6.2% in 2024, boosting installment financing (~28% POS). Refurbished CAGR 2020–25 ~12% (refurb sales ~€250m FY2024); Asian D2C price cuts 20–30% pressure margins; Ceconomy leans on 1,000+ stores and service offerings.

| Metric | Value |

|---|---|

| Inflation (Dec 2025) | 2.7% |

| ECB deposit rate (mid‑2024) | 4.00% |

| Household loan rate (2024) | ~6.2% |

| Refurb CAGR (2020–25) | 12% |

| Refurb sales FY2024 | €250m |

| Ceconomy stores | 1,000+ |

Preview the Actual Deliverable

Ceconomy PESTLE Analysis

The preview shown here is the exact Ceconomy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and rapid tech adoption are reshaping Ceconomy's prospects in our concise PESTLE snapshot—perfect for investors and strategists seeking immediate clarity. Purchase the full PESTLE analysis to unlock detailed risk assessments, regulatory impacts, and actionable opportunities tailored to Ceconomy. Download now for a ready-to-use, fully editable report that accelerates smarter decisions.

Political factors

European trade policy and internal market stability

Ceconomy’s cross-border operations rely on the EU Single Market; intra-EU trade accounted for roughly 75% of its 2024 supply-chain movements, lowering tariffs and paperwork across 10+ countries where it operates.

Standardized regulations and trade agreements enabled inventory turnover improvements, supporting gross margin recovery to 18.1% in FY 2024.

Any shift toward protectionism or altered intra-EU trade relations by late 2025 could raise logistics costs and lead times, risking inventory write-downs and EBITDA volatility.

Geopolitical tensions affecting supply chain security

Ongoing geopolitical instability in Eastern Europe and trade frictions between Western nations and Asian manufacturing hubs remain critical risks for electronics retailers; by Q4 2025 global semiconductor spot prices rose ~12% YoY, squeezing margins. As of late 2025 these tensions continue to disrupt availability and push lead times for chips and finished goods to averages of 18–22 weeks versus 12–16 in 2023. Ceconomy must diversify suppliers—already expanding sourcing from Turkey and Vietnam—and allocate capital to buffer logistics delays, given that supply-chain disruptions lifted working capital needs by an estimated €180–220m in 2024–25.

National labor and wage regulations in Germany

As a major German employer, Ceconomy faces direct impact from domestic labor policies and the 2024 statutory minimum wage of 12.41 EUR/hr (planned increases to 12.82 EUR/hr in 2025), raising wage bills across its ~43,000 employees. Changes to employer social security contributions and tighter working-hour regulations can increase personnel costs, already ~60% of store operating expenses, squeezing margins. By end-2025, labor reforms force Ceconomy to balance higher compensation with leaner store staffing and automation investments to protect EBITDA, which was 4.1% in FY2023/24.

EU digital sovereignty and platform regulation

The Digital Markets Act, effective since March 2024, forces gatekeepers to open ecosystems, improving market access for Ceconomy against US e-commerce giants; EU rules could raise Ceconomy marketplace revenue share, supporting its 2024 goal to grow online sales beyond the 30% group target.

EU digital sovereignty pushes stricter data residency and vendor scrutiny—impacting Ceconomy’s data handling and contracts with non-EU tech providers after 2024 regulatory updates.

- DMA enforcement from 2024 levels playing field vs gatekeepers

- Ceconomy online sales target >30% (2024 strategic objective)

- Increased data residency and vendor controls affecting non-EU suppliers

Governmental incentives for energy-efficient transitions

Political initiatives reducing household energy use have increased demand for high-efficiency appliances at MediaMarkt and Saturn; EU energy-efficiency standards and national schemes lifted smart appliance sales by ~18% YoY in 2024.

Subsidies and tax breaks for greener upgrades—e.g., Germany’s 2024 appliance subsidy and Italy’s ecobonus—boost Ceconomy’s white goods revenue, supporting a ~3–5% uplift in segment sales in 2024.

By 2025, climate-target pressures solidified these incentives across key EU markets, making them a structural tailwind for Ceconomy’s appliance mix and average selling price growth.

- EU/national incentives increased smart/high-efficiency appliance demand ~18% YoY in 2024

- White goods sales gain ~3–5% revenue uplift in 2024 from subsidies

- Incentives became permanent policy across major EU markets by 2025

Ceconomy faces EU reliance, rising wages and DMA-driven online growth

Political risks for Ceconomy include EU Single Market dependence (≈75% intra‑EU supply flows in 2024), rising labor costs from Germany’s €12.41→€12.82/hr min wage (2024–25) affecting ~43,000 staff, DMA-driven improved marketplace access boosting online sales target >30% (2024), and energy-efficiency subsidies that lifted white‑goods sales ~3–5% in 2024.

| Metric | Value |

|---|---|

| Intra‑EU supply share 2024 | ≈75% |

| Employees | ≈43,000 |

| Min wage 2024→25 | €12.41→€12.82/hr |

| Online sales target | >30% |

| White‑goods uplift 2024 | 3–5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ceconomy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

A concise, shareable Ceconomy PESTLE summary that’s visually segmented for quick reference, letting teams drop it into presentations, annotate for local context, and rapidly align on external risks and strategic positioning.

Economic factors

Inflationary pressures and consumer purchasing power

While headline inflation eased to 2.7% by December 2025 from peaks above 8% in 2022–23, cumulative real-income loss left German household real incomes down about 4% versus pre‑pandemic levels, pressuring discretionary spend; high housing and energy costs (energy bills up ~15% YoY in 2024) push consumers to delay premium electronics. Ceconomy counters with value-focused assortments and expanded financing—installment uptake rose ~20% in 2024—to sustain volumes.

Eurozone interest rate environment

The ECB lifted its deposit rate to 4.00% by mid-2024 and signaled a pause through late 2025, raising Ceconomy’s borrowing costs and increasing inventory carry expenses; higher rates also pressured consumer credit, with Euro area household loan rates averaging ~6.2% in 2024. A stabilizing trajectory toward end-2025 supports steadier capex planning and bolsters demand for installment financing, which accounted for ~28% of Ceconomy’s POS financing in 2023.

Rise of the refurbished and second-hand market

Economic constraints and a stronger value focus have driven a 12% global CAGR for refurbished electronics (2020–2025); Ceconomy expanded trade-in programs and launched 'as-new' lines, with refurbished sales contributing an estimated €250m in FY2024, targeting budget-conscious consumers.

This trend pressures new-product margins—used devices often sell 30–50% cheaper—but offers Ceconomy a chance to increase customer lifetime value and loyalty via sustainable, lower-cost offerings and recurring service revenue.

Competition from low-cost international e-commerce platforms

The expansion of Asian direct-to-consumer platforms, which cut prices by up to 20–30% on standardized electronics, intensifies margin pressure on Ceconomy’s consumer electronics lines.

Ceconomy must differentiate via its 1,000+ German stores and service-led Solution business, aiming to offset price gaps with in‑store expertise and installation services.

By end‑2025 the strategy targets integrated omnichannel pricing parity plus local advisory revenue growth to stabilize gross margins.

- Asian D2C price cuts: 20–30%

- Ceconomy retail footprint: 1,000+ stores

- Strategy: combine competitive online pricing with local expert services by 2025

Labor market shortages and rising operational costs

Ceconomy faces rising personnel expenses as Europe’s tight labor market—EU unemployment ~6.2% (2025) but acute shortages in logistics/technical roles—pushes wage costs; FY 2024 personnel expenses rose ~4-6% YoY in retail peers, pressuring margins.

Attracting skilled staff for service hubs while managing store payrolls forces investment in automation and digital self-service; Ceconomy has accelerated self-checkout and remote diagnostics to contain labor-related OPEX and improve throughput.

- EU unemployment ~6.2% (2025) with shortages in logistics/tech

- Retail personnel costs up ~4-6% YoY in 2024 peers

- Increased investment in self-checkout, remote diagnostics, and automation

Ceconomy weathers weak real incomes, rising rates as refurbished sales surge to €250m

Slower real-income recovery (household real incomes ~4% below pre‑pandemic by 2025) and 2.7% inflation in Dec 2025 reduced discretionary spend; ECB rates ~4.00% through 2025 lifted borrowing/inventory costs and pushed household loan rates to ~6.2% in 2024, boosting installment financing (~28% POS). Refurbished CAGR 2020–25 ~12% (refurb sales ~€250m FY2024); Asian D2C price cuts 20–30% pressure margins; Ceconomy leans on 1,000+ stores and service offerings.

| Metric | Value |

|---|---|

| Inflation (Dec 2025) | 2.7% |

| ECB deposit rate (mid‑2024) | 4.00% |

| Household loan rate (2024) | ~6.2% |

| Refurb CAGR (2020–25) | 12% |

| Refurb sales FY2024 | €250m |

| Ceconomy stores | 1,000+ |

Preview the Actual Deliverable

Ceconomy PESTLE Analysis

The preview shown here is the exact Ceconomy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.