Ceconomy SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Ceconomy faces a pivotal moment as digital disruption reshapes retail—our concise SWOT highlights strong brand reach and scale but flags margin pressure, supply-chain risks, and intensifying online competition; uncover the strategic moves that can unlock value. Purchase the full SWOT analysis for a professionally formatted Word report and editable Excel model to inform investment, strategic planning, or board-level decisions.

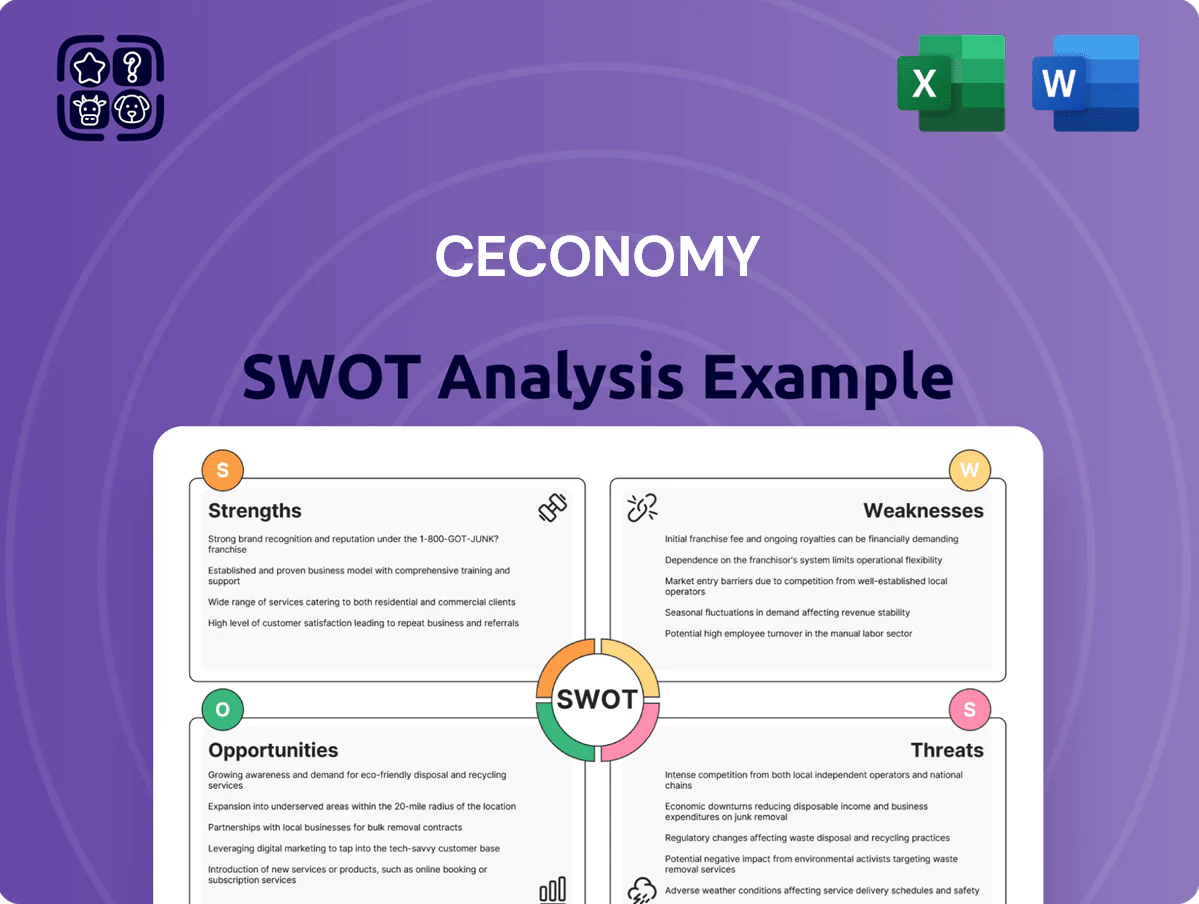

Strengths

Dominant European Market Position

As of late 2025, Ceconomy, via MediaMarkt and Saturn, leads European consumer electronics retail with ~1,000 stores and ~€20.4bn revenue in FY2024/25, giving strong bargaining power with suppliers and access to ~120m loyalty customers across key markets.

Integrated Omnichannel Infrastructure

The integrated omnichannel infrastructure lets Ceconomy blend 800+ MediaMarktSaturn stores with a digital platform, enabling Click and Collect and same-day pickup that lifted Q3 2025 store-attributed sales by 12% year-over-year; this hybrid model reduced online-only churn and delivered 18% faster inventory turnover versus pure-play peers, improving stock days from 42 to 34 and smoothing logistics costs across channels.

Growth in Services and Solutions

Modernized Experience Center Format

- 18% higher basket size at concept stores (2024)

- 12% rise in service revenues (FY2024)

- €1.9bn revenue tied to property-backed locations

Strong Private Label Portfolio

Ceconomy’s expansion of private labels Peaq and Koenic boosted gross margins—private label sales reached ~12% of revenue in 2024, lifting product-margin contribution by ~1.2 percentage points versus 2022; this lets Ceconomy price aggressively for value shoppers while protecting margins.

Owning brands improves control over assortment and supply chains, lowering procurement costs and reducing stockouts; vertical integration supports competitiveness in price-sensitive European markets.

- Private label share ~12% of 2024 revenue

- Margin uplift ≈ +1.2 pp vs 2022

- Lower procurement/unit costs, fewer stockouts

Ceconomy: EU electronics leader—€20.4bn, ~1,000 stores, services €1.24bn, private labels 12%

Ceconomy leads EU electronics retail (~1,000 stores) with €20.4bn revenue (FY2024/25), ~120m loyalty users, 18% higher basket size at concept stores, services revenue €1.24bn (15% sales), private labels 12% of revenue (±1.2pp margin uplift vs 2022), inventory days cut 42→34 and store-driven sales +12% Q3 2025.

| Metric | Value |

|---|---|

| Stores | ~1,000 |

| Revenue FY24/25 | €20.4bn |

| Services rev | €1.24bn |

| Private label | 12% |

What is included in the product

Provides a concise SWOT overview of Ceconomy, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Offers a concise Ceconomy SWOT snapshot for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Slim Operating Profit Margins

Ceconomy’s core retailing of consumer electronics faces fierce price competition and slim operating margins; in FY2024 (ending Sept 30, 2024) group EBIT margin stayed around 1.8%, showing limited buffer vs. cost shocks.

Despite pushing services (like installation, warranties), services still represent under 15% of revenue, so small cost increases or price cuts quickly erode profitability.

High Fixed Costs of Physical Stores

Maintaining Ceconomy’s 1,000+ large-format stores in Europe drives high fixed costs—rent, energy, and staff—contributing to roughly €800–900 million in annual store-related operating expenses (estimated 2024 run rate).

These strategic assets become heavy burdens in low-footfall periods; Ceconomy reported a 6% like-for-like sales drop in FY2023/24 in some markets, tightening margins.

High, rigid costs limit pricing and promo flexibility and raise break-even sales targets, challenging long-term profitability and cash flow resilience.

Geographic Concentration in Germany

Around 62% of Ceconomy’s 2024 revenue came from Germany, so local consumer demand swings hit consolidated sales hard. A 1% drop in German retail spending could shave roughly €60–70m off annual revenue, based on 2024 top-line figures. Recent German regulatory moves on consumer warranties and energy-efficiency rules add compliance costs and margin pressure. International investors face higher volatility due to limited geographic diversification.

Complex Corporate History and Structure

Ceconomy’s past organizational complexity and the 2017 Metro demerger legacy have at times slowed strategic decisions, contributing to slower store conversions and digital rollouts versus peers.

Restructuring since 2021 improved agility, but a remaining traditional hierarchy can still delay product launches in a market where 2024 European online electronics growth hit ~6% YoY.

Further streamlining internal processes is essential to match digital-native competitors that cut time-to-market to months instead of quarters.

- Legacy demerger (2017) left layered governance

- Post-2021 cuts reduced SG&A but reporting lag persists

- 2024 online growth ~6% YoY raises urgency

- Faster processes could shorten launch time from quarters to months

Slower Digital Transformation Pace

Ceconomy’s omnichannel strength masks a slower digital transformation: logistics and data analytics trailed pure-play e-commerce, forcing roughly €1.2bn in tech and supply-chain capex since 2021 that still pressures the balance sheet through end-2025.

Legacy IT modernization remains unfinished, limiting operational efficiency and advanced personalization despite ongoing investments; online revenue growth lagged peers at ~6% CAGR vs ~12% for pure players (2021–24).

- €1.2bn capex since 2021

- Online revenue CAGR ~6% (2021–24)

- Peer CAGR ~12% (2021–24)

- Legacy IT hindering personalization

Ceconomy under pressure: thin EBIT, high store costs, German concentration, lagging online

Ceconomy faces tight EBIT margins (≈1.8% FY2024), high fixed store costs (€800–900m run rate 2024), revenue concentration in Germany (~62% of 2024 sales), slow online CAGR (~6% 2021–24 vs peers ~12%), and unfinished IT capex (€1.2bn since 2021) that strains cash and agility.

| Metric | Value (2024) |

|---|---|

| EBIT margin | ≈1.8% |

| Store costs | €800–900m |

| Germany share | ~62% |

| Online CAGR | ~6% |

| Capex since 2021 | €1.2bn |

Full Version Awaits

Ceconomy SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file, structured and ready to use, with the complete document available immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Ceconomy faces a pivotal moment as digital disruption reshapes retail—our concise SWOT highlights strong brand reach and scale but flags margin pressure, supply-chain risks, and intensifying online competition; uncover the strategic moves that can unlock value. Purchase the full SWOT analysis for a professionally formatted Word report and editable Excel model to inform investment, strategic planning, or board-level decisions.

Strengths

Dominant European Market Position

As of late 2025, Ceconomy, via MediaMarkt and Saturn, leads European consumer electronics retail with ~1,000 stores and ~€20.4bn revenue in FY2024/25, giving strong bargaining power with suppliers and access to ~120m loyalty customers across key markets.

Integrated Omnichannel Infrastructure

The integrated omnichannel infrastructure lets Ceconomy blend 800+ MediaMarktSaturn stores with a digital platform, enabling Click and Collect and same-day pickup that lifted Q3 2025 store-attributed sales by 12% year-over-year; this hybrid model reduced online-only churn and delivered 18% faster inventory turnover versus pure-play peers, improving stock days from 42 to 34 and smoothing logistics costs across channels.

Growth in Services and Solutions

Modernized Experience Center Format

- 18% higher basket size at concept stores (2024)

- 12% rise in service revenues (FY2024)

- €1.9bn revenue tied to property-backed locations

Strong Private Label Portfolio

Ceconomy’s expansion of private labels Peaq and Koenic boosted gross margins—private label sales reached ~12% of revenue in 2024, lifting product-margin contribution by ~1.2 percentage points versus 2022; this lets Ceconomy price aggressively for value shoppers while protecting margins.

Owning brands improves control over assortment and supply chains, lowering procurement costs and reducing stockouts; vertical integration supports competitiveness in price-sensitive European markets.

- Private label share ~12% of 2024 revenue

- Margin uplift ≈ +1.2 pp vs 2022

- Lower procurement/unit costs, fewer stockouts

Ceconomy: EU electronics leader—€20.4bn, ~1,000 stores, services €1.24bn, private labels 12%

Ceconomy leads EU electronics retail (~1,000 stores) with €20.4bn revenue (FY2024/25), ~120m loyalty users, 18% higher basket size at concept stores, services revenue €1.24bn (15% sales), private labels 12% of revenue (±1.2pp margin uplift vs 2022), inventory days cut 42→34 and store-driven sales +12% Q3 2025.

| Metric | Value |

|---|---|

| Stores | ~1,000 |

| Revenue FY24/25 | €20.4bn |

| Services rev | €1.24bn |

| Private label | 12% |

What is included in the product

Provides a concise SWOT overview of Ceconomy, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Offers a concise Ceconomy SWOT snapshot for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Slim Operating Profit Margins

Ceconomy’s core retailing of consumer electronics faces fierce price competition and slim operating margins; in FY2024 (ending Sept 30, 2024) group EBIT margin stayed around 1.8%, showing limited buffer vs. cost shocks.

Despite pushing services (like installation, warranties), services still represent under 15% of revenue, so small cost increases or price cuts quickly erode profitability.

High Fixed Costs of Physical Stores

Maintaining Ceconomy’s 1,000+ large-format stores in Europe drives high fixed costs—rent, energy, and staff—contributing to roughly €800–900 million in annual store-related operating expenses (estimated 2024 run rate).

These strategic assets become heavy burdens in low-footfall periods; Ceconomy reported a 6% like-for-like sales drop in FY2023/24 in some markets, tightening margins.

High, rigid costs limit pricing and promo flexibility and raise break-even sales targets, challenging long-term profitability and cash flow resilience.

Geographic Concentration in Germany

Around 62% of Ceconomy’s 2024 revenue came from Germany, so local consumer demand swings hit consolidated sales hard. A 1% drop in German retail spending could shave roughly €60–70m off annual revenue, based on 2024 top-line figures. Recent German regulatory moves on consumer warranties and energy-efficiency rules add compliance costs and margin pressure. International investors face higher volatility due to limited geographic diversification.

Complex Corporate History and Structure

Ceconomy’s past organizational complexity and the 2017 Metro demerger legacy have at times slowed strategic decisions, contributing to slower store conversions and digital rollouts versus peers.

Restructuring since 2021 improved agility, but a remaining traditional hierarchy can still delay product launches in a market where 2024 European online electronics growth hit ~6% YoY.

Further streamlining internal processes is essential to match digital-native competitors that cut time-to-market to months instead of quarters.

- Legacy demerger (2017) left layered governance

- Post-2021 cuts reduced SG&A but reporting lag persists

- 2024 online growth ~6% YoY raises urgency

- Faster processes could shorten launch time from quarters to months

Slower Digital Transformation Pace

Ceconomy’s omnichannel strength masks a slower digital transformation: logistics and data analytics trailed pure-play e-commerce, forcing roughly €1.2bn in tech and supply-chain capex since 2021 that still pressures the balance sheet through end-2025.

Legacy IT modernization remains unfinished, limiting operational efficiency and advanced personalization despite ongoing investments; online revenue growth lagged peers at ~6% CAGR vs ~12% for pure players (2021–24).

- €1.2bn capex since 2021

- Online revenue CAGR ~6% (2021–24)

- Peer CAGR ~12% (2021–24)

- Legacy IT hindering personalization

Ceconomy under pressure: thin EBIT, high store costs, German concentration, lagging online

Ceconomy faces tight EBIT margins (≈1.8% FY2024), high fixed store costs (€800–900m run rate 2024), revenue concentration in Germany (~62% of 2024 sales), slow online CAGR (~6% 2021–24 vs peers ~12%), and unfinished IT capex (€1.2bn since 2021) that strains cash and agility.

| Metric | Value (2024) |

|---|---|

| EBIT margin | ≈1.8% |

| Store costs | €800–900m |

| Germany share | ~62% |

| Online CAGR | ~6% |

| Capex since 2021 | €1.2bn |

Full Version Awaits

Ceconomy SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file, structured and ready to use, with the complete document available immediately after checkout.