China Energy Engineering Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

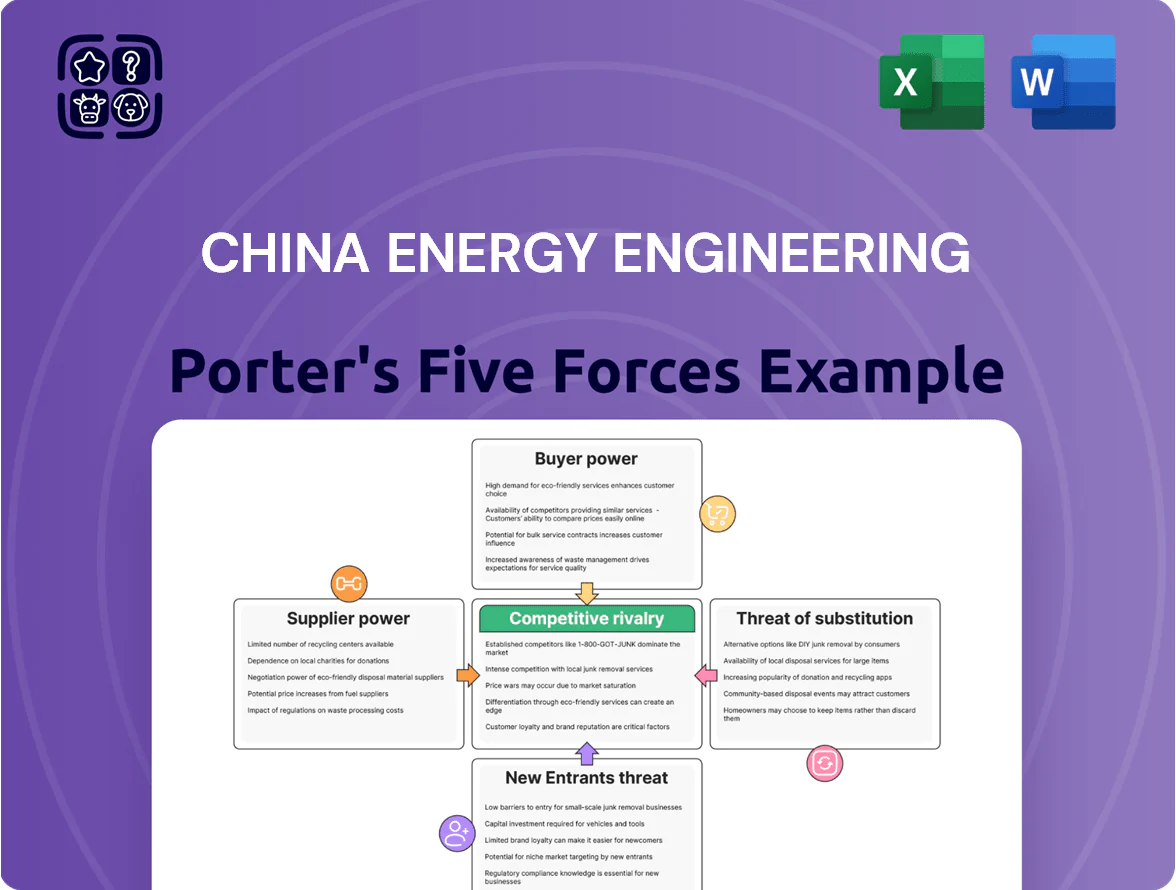

China Energy Engineering faces moderate supplier leverage, high project-based buyer scrutiny, and significant rivalry from state-backed peers, while regulatory shifts and renewable tech convergence heighten both threat of substitutes and entry barriers.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to investment or corporate planning.

Suppliers Bargaining Power

Raw Material Price Volatility

The procurement of steel, copper and cement drives ~18–24% of CEEC project costs; by late 2025 global commodity volatility—steel up 12% YTD, copper 8% YTD, cement regional spikes to 15%—reflects geopolitical tensions and trade shifts. CEEC uses multi-year contracts and 60–70% forward coverage to cut risk, but suppliers retain moderate leverage due to price sensitivity, so advanced hedging (futures, swaps, indexed contracts) is needed to shield margins from sudden inflationary spikes.

Specialized Equipment Dependencies

For advanced power generation and UHV (ultra-high voltage) transmission, CEEC depends on a small set of high-tech suppliers for turbines, power semiconductors and control systems, giving suppliers strong bargaining power; global market share for these vendors is concentrated—top 5 firms hold ~60% of supply for large gas/steam turbines as of 2025.

Digitization by 2026 raised component complexity and lead times—power semiconductor lead times averaged 28–40 weeks in 2025—so CEEC faces higher switching costs and price exposure.

CEEC counters with strategic partnerships, co‑development deals, and stepped-up R&D: internal capital R&D spending rose to ~1.8% of revenue in 2024 to build proprietary turbine controls and semiconductor testing capacity.

Labor Market Constraints

Strategic SOE Procurement Scale

As a massive state-owned enterprise, China Energy Engineering (CEEC) uses procurement scale to push prices down and secure priority supply; CEEC reported RMB 280 billion in 2024 procurement volume, giving it strong counter-leverage vs general suppliers.

Domestic vendors prioritize CEEC for steady orders and state-backed payments, lowering their bargaining power; only niche global suppliers (specialized turbines, HV equipment) retain leverage.

- RMB 280bn 2024 procurement

- Domestic suppliers favor long-term CEEC contracts

- Bargaining capped except for specialized global vendors

Energy Input Costs for Manufacturing

CEEC’s in-house equipment units remain sensitive to industrial electricity and fuel prices; China’s shift to market-based electricity pricing by 2025 has raised cost volatility—wholesale prices varied ±15% year-over-year in 2024–25 for heavy-industry provinces.

Despite CEEC building captive plants, it still pays grid tariffs and carbon costs: national carbon market average EUA price reached ~CNY 70/ton in 2025, adding ~2–4% to manufacturing unit costs.

Suppliers wield moderate–strong leverage as commodity, niche vendors and wages squeeze margins

Suppliers hold moderate-to-strong power: commodity inputs drive 18–24% of costs (steel +12% YTD 2025, copper +8% YTD), niche turbine/semiconductor vendors (top‑5 = ~60% market share) and skilled labor shortages (wage +6.8% y/y 2025) raise leverage; CEEC uses RMB 280bn 2024 procurement scale, 60–70% forward coverage, 1.8% revenue R&D and automation capex to contain supplier pressure.

| Metric | Value |

|---|---|

| Procurement 2024 | RMB 280bn |

| Commodity share of costs | 18–24% |

| Steel/Copper 2025 YTD | +12% / +8% |

| Top‑5 turbine share 2025 | ~60% |

| Forward coverage | 60–70% |

| R&D spend 2024 | ~1.8% revenue |

| Manufacturing wage growth 2025 | +6.8% y/y |

| Power price volatility | ±15% y/y |

| Carbon price 2025 | CNY ~70/ton |

What is included in the product

Tailored exclusively for China Energy Engineering, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise Porter's Five Forces snapshot for China Energy Engineering—quickly highlights supplier, buyer, competitor, entrant, and substitute pressures to simplify strategic choices and boardroom decisions.

Customers Bargaining Power

Concentration of Domestic Utility Buyers

The primary buyers for China Energy Engineering Corporation (CEEC) domestic projects are a few state-owned giants—State Grid and China Southern Power Grid—creating a monopsony-like market where buyers set technical specs and squeeze prices.

By 2026 these grids demand low-carbon tech; State Grid pledged net-zero scope 2 by 2030 and increased green procurement to ~28% of capex in 2025, forcing CEEC to retrofit offerings.

The concentrated client base—two buyers handling ~70% of grid procurement—means CEEC must keep service high and pricing competitive to win repeat contracts.

International Sovereign Client Influence

Shift Toward Green Energy Procurement

By year-end 2025 customer demand shifted decisively to renewables, hydrogen, and storage, giving buyers power to reject fossil-focused services; global green procurement drove CEEC to pivot or risk share loss—renewables made 48% of new project RFPs in China in 2025, per NEA.

Buyers now require construction plus performance guarantees and carbon transparency; 62% of corporate energy buyers demanded lifecycle emissions reporting in 2025, forcing CEEC to offer long-term O&M contracts and guaranteed output metrics.

Competitive Bidding and Price Sensitivity

Open competitive bidding for EPC contracts compresses CEEC’s margins as multi-round tenders push prices down; CEEC’s EBIT margin in 2024 for domestic EPC projects averaged ~4.5%, down from 6.1% in 2019.

Digital procurement platforms by 2025 widened price transparency—one platform showed bid-price spreads tightening by 18% year-on-year—giving buyers more leverage.

CEEC defends margins by selling integrated full-cycle services (design, construction, O&M), claiming lifecycle value that can boost project IRR by 2–4 percentage points versus lowest-bid rivals.

Demand for Integrated Solutions

Modern customers want turnkey deals covering design, financing, construction, and O&M, letting buyers demand integrated risk-sharing from China Energy Engineering Corporation (CEEC).

By end-2025, holistic-package capability is a prerequisite for major tenders; CEEC must offer bundled contracts and keep a strong balance sheet—2024 revenue was RMB 276.4 billion, helping meet bid bonds and financing needs.

Clients shift operational and financial risk onto contractors, so CEEC needs diverse technical teams and project finance capacity to win contracts.

- Turnkey demand raises buyer bargaining power

- 2024 revenue RMB 276.4 billion supports bidding capacity

- Holistic offering required for major tenders by end-2025

- Clients transfer ops/finance risk onto CEEC

CEEC squeezed by concentrated buyers but scale, financing and renewables cushion earnings

Buyers (mainly State Grid and China Southern, ~70% procurement) exert strong bargaining power, forcing price pressure and green-tech specs; CEEC’s domestic EPC EBIT fell to ~4.5% in 2024 from 6.1% in 2019. Overseas sovereign clients also hold leverage, but bundled financing from China Development Bank/Exim (≈30% of 2024–25 overseas contract value) and CEEC’s RMB 276.4bn 2024 revenue mitigate risk.

| Metric | Value |

|---|---|

| Buyer concentration (domestic) | ~70% |

| Domestic EPC EBIT 2024 | ~4.5% |

| Revenue 2024 | RMB 276.4bn |

| Overseas financing share | ~30% |

| Renewables in RFPs 2025 | 48% |

Preview Before You Purchase

China Energy Engineering Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of China Energy Engineering you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted version you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: a ready-to-use, fully written analysis that will be available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

China Energy Engineering faces moderate supplier leverage, high project-based buyer scrutiny, and significant rivalry from state-backed peers, while regulatory shifts and renewable tech convergence heighten both threat of substitutes and entry barriers.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to investment or corporate planning.

Suppliers Bargaining Power

Raw Material Price Volatility

The procurement of steel, copper and cement drives ~18–24% of CEEC project costs; by late 2025 global commodity volatility—steel up 12% YTD, copper 8% YTD, cement regional spikes to 15%—reflects geopolitical tensions and trade shifts. CEEC uses multi-year contracts and 60–70% forward coverage to cut risk, but suppliers retain moderate leverage due to price sensitivity, so advanced hedging (futures, swaps, indexed contracts) is needed to shield margins from sudden inflationary spikes.

Specialized Equipment Dependencies

For advanced power generation and UHV (ultra-high voltage) transmission, CEEC depends on a small set of high-tech suppliers for turbines, power semiconductors and control systems, giving suppliers strong bargaining power; global market share for these vendors is concentrated—top 5 firms hold ~60% of supply for large gas/steam turbines as of 2025.

Digitization by 2026 raised component complexity and lead times—power semiconductor lead times averaged 28–40 weeks in 2025—so CEEC faces higher switching costs and price exposure.

CEEC counters with strategic partnerships, co‑development deals, and stepped-up R&D: internal capital R&D spending rose to ~1.8% of revenue in 2024 to build proprietary turbine controls and semiconductor testing capacity.

Labor Market Constraints

Strategic SOE Procurement Scale

As a massive state-owned enterprise, China Energy Engineering (CEEC) uses procurement scale to push prices down and secure priority supply; CEEC reported RMB 280 billion in 2024 procurement volume, giving it strong counter-leverage vs general suppliers.

Domestic vendors prioritize CEEC for steady orders and state-backed payments, lowering their bargaining power; only niche global suppliers (specialized turbines, HV equipment) retain leverage.

- RMB 280bn 2024 procurement

- Domestic suppliers favor long-term CEEC contracts

- Bargaining capped except for specialized global vendors

Energy Input Costs for Manufacturing

CEEC’s in-house equipment units remain sensitive to industrial electricity and fuel prices; China’s shift to market-based electricity pricing by 2025 has raised cost volatility—wholesale prices varied ±15% year-over-year in 2024–25 for heavy-industry provinces.

Despite CEEC building captive plants, it still pays grid tariffs and carbon costs: national carbon market average EUA price reached ~CNY 70/ton in 2025, adding ~2–4% to manufacturing unit costs.

Suppliers wield moderate–strong leverage as commodity, niche vendors and wages squeeze margins

Suppliers hold moderate-to-strong power: commodity inputs drive 18–24% of costs (steel +12% YTD 2025, copper +8% YTD), niche turbine/semiconductor vendors (top‑5 = ~60% market share) and skilled labor shortages (wage +6.8% y/y 2025) raise leverage; CEEC uses RMB 280bn 2024 procurement scale, 60–70% forward coverage, 1.8% revenue R&D and automation capex to contain supplier pressure.

| Metric | Value |

|---|---|

| Procurement 2024 | RMB 280bn |

| Commodity share of costs | 18–24% |

| Steel/Copper 2025 YTD | +12% / +8% |

| Top‑5 turbine share 2025 | ~60% |

| Forward coverage | 60–70% |

| R&D spend 2024 | ~1.8% revenue |

| Manufacturing wage growth 2025 | +6.8% y/y |

| Power price volatility | ±15% y/y |

| Carbon price 2025 | CNY ~70/ton |

What is included in the product

Tailored exclusively for China Energy Engineering, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise Porter's Five Forces snapshot for China Energy Engineering—quickly highlights supplier, buyer, competitor, entrant, and substitute pressures to simplify strategic choices and boardroom decisions.

Customers Bargaining Power

Concentration of Domestic Utility Buyers

The primary buyers for China Energy Engineering Corporation (CEEC) domestic projects are a few state-owned giants—State Grid and China Southern Power Grid—creating a monopsony-like market where buyers set technical specs and squeeze prices.

By 2026 these grids demand low-carbon tech; State Grid pledged net-zero scope 2 by 2030 and increased green procurement to ~28% of capex in 2025, forcing CEEC to retrofit offerings.

The concentrated client base—two buyers handling ~70% of grid procurement—means CEEC must keep service high and pricing competitive to win repeat contracts.

International Sovereign Client Influence

Shift Toward Green Energy Procurement

By year-end 2025 customer demand shifted decisively to renewables, hydrogen, and storage, giving buyers power to reject fossil-focused services; global green procurement drove CEEC to pivot or risk share loss—renewables made 48% of new project RFPs in China in 2025, per NEA.

Buyers now require construction plus performance guarantees and carbon transparency; 62% of corporate energy buyers demanded lifecycle emissions reporting in 2025, forcing CEEC to offer long-term O&M contracts and guaranteed output metrics.

Competitive Bidding and Price Sensitivity

Open competitive bidding for EPC contracts compresses CEEC’s margins as multi-round tenders push prices down; CEEC’s EBIT margin in 2024 for domestic EPC projects averaged ~4.5%, down from 6.1% in 2019.

Digital procurement platforms by 2025 widened price transparency—one platform showed bid-price spreads tightening by 18% year-on-year—giving buyers more leverage.

CEEC defends margins by selling integrated full-cycle services (design, construction, O&M), claiming lifecycle value that can boost project IRR by 2–4 percentage points versus lowest-bid rivals.

Demand for Integrated Solutions

Modern customers want turnkey deals covering design, financing, construction, and O&M, letting buyers demand integrated risk-sharing from China Energy Engineering Corporation (CEEC).

By end-2025, holistic-package capability is a prerequisite for major tenders; CEEC must offer bundled contracts and keep a strong balance sheet—2024 revenue was RMB 276.4 billion, helping meet bid bonds and financing needs.

Clients shift operational and financial risk onto contractors, so CEEC needs diverse technical teams and project finance capacity to win contracts.

- Turnkey demand raises buyer bargaining power

- 2024 revenue RMB 276.4 billion supports bidding capacity

- Holistic offering required for major tenders by end-2025

- Clients transfer ops/finance risk onto CEEC

CEEC squeezed by concentrated buyers but scale, financing and renewables cushion earnings

Buyers (mainly State Grid and China Southern, ~70% procurement) exert strong bargaining power, forcing price pressure and green-tech specs; CEEC’s domestic EPC EBIT fell to ~4.5% in 2024 from 6.1% in 2019. Overseas sovereign clients also hold leverage, but bundled financing from China Development Bank/Exim (≈30% of 2024–25 overseas contract value) and CEEC’s RMB 276.4bn 2024 revenue mitigate risk.

| Metric | Value |

|---|---|

| Buyer concentration (domestic) | ~70% |

| Domestic EPC EBIT 2024 | ~4.5% |

| Revenue 2024 | RMB 276.4bn |

| Overseas financing share | ~30% |

| Renewables in RFPs 2025 | 48% |

Preview Before You Purchase

China Energy Engineering Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of China Energy Engineering you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted version you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: a ready-to-use, fully written analysis that will be available to you instantly after payment.