Cegedim Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Cegedim operates in a moderately concentrated healthcare IT market where bargaining power of buyers and regulatory pressures shape pricing and innovation, while established rivals and specialized suppliers limit margin expansion.

Threats from digital entrants and substitutes are rising, but Cegedim’s niche solutions, client relationships, and data assets provide defensible advantages—though execution and M&A strategy will determine long-term positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cegedim’s competitive dynamics, market pressures, and strategic advantages in detail.

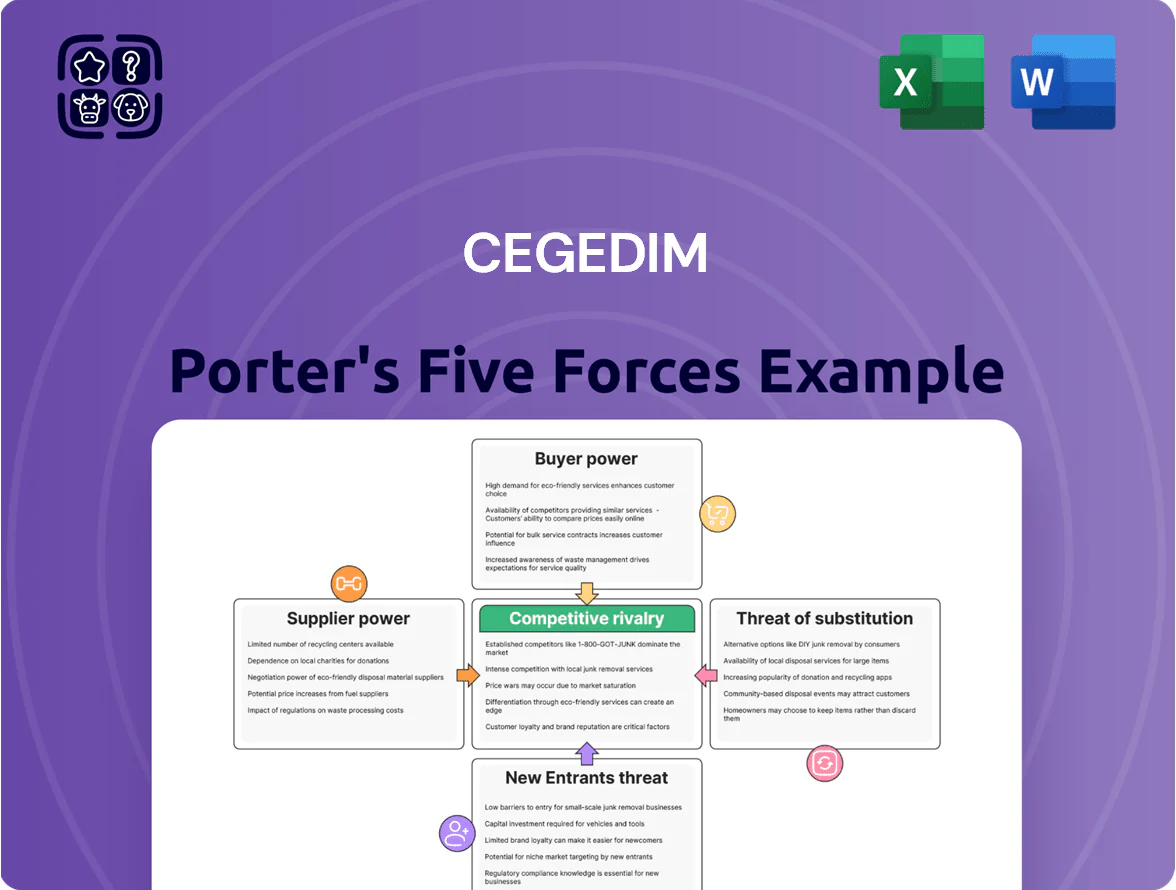

Suppliers Bargaining Power

Dependence on Cloud Infrastructure Providers

Scarcity of Specialized IT Talent

The market for healthcare-compliance and AI software developers and data scientists remained tight at end-2025, with global demand outstripping supply and median US salaries hitting roughly $180k–$220k for senior specialists per Glassdoor/LinkedIn aggregates.

These niche professionals act as vital human-capital suppliers, negotiating remote work and equity, raising Cegedim’s labor costs and bargaining power versus vendors and rivals.

Cegedim must invest in retention—estimated at 15%+ of payroll for top talent—to stop core IP migrating to Big Tech, digital-health startups, or consulting firms.

Data Acquisition and Licensing Costs

To deliver high-quality analytics and CRM services, Cegedim often licenses specialized medical datasets or integrates with third-party healthcare databases, giving these data providers notable bargaining power because Cegedim’s insights rely on that raw accuracy and depth.

Data providers' leverage rises as unique clinical, claims, and real-world evidence (RWE) sources are scarce; industry reports show commercial healthcare data licensing can cost $50k–$500k+ annually per dataset in 2024–2025 for enterprise use.

Stricter privacy rules—GDPR updates in EU and HIPAA enforcement in the US—raise compliance costs, so Cegedim faces higher acquisition and anonymization fees, increasing supplier power and squeezing margins.

Hardware and Cybersecurity Vendors

Suppliers of high-end encryption software and secure server hardware hold strong bargaining power because Cegedim depends on specialized hardware for its pharmacy and practice management systems and advanced cybersecurity to protect PHI; global healthcare cybersecurity spending reached about $34.5B in 2024, keeping premium vendors scarce and costly.

Because a breach would be catastrophic for Cegedim’s reputation and regulatory fines (HIPAA/EU GDPR), the company has limited flexibility to switch to lower-quality or unproven vendors, raising switching costs and vendor leverage.

- Healthcare cybersecurity market: $34.5B (2024)

- High switching costs due to compliance and integration

- Premium vendors command price and service terms

- Reputational/fine risk increases supplier leverage

Regulatory and Compliance Consultants

Cegedim depends on specialized regulatory and compliance consultants due to evolving healthcare laws like GDPR and country-level medical data rules; in 2024 GDPR fines totaled €2.4 billion EU-wide, underscoring high stakes. These consultants shape Cegedim’s operating framework, reducing legal risk and enabling continued market access across ~80 countries where Cegedim reports activity. Their bargaining power rises from technical expertise and scarcity of trusted firms with healthcare and cross-border data skills.

- 2024 EU GDPR fines €2.4bn

- Cegedim active in ~80 countries

- Specialist firms limited, increasing supplier leverage

Supplier squeeze: cloud, AI talent, data and compliance driving margin pressure

Cegedim faces high supplier power from concentrated cloud vendors (AWS/Azure/GCP ~65–70% IaaS/PaaS 2025), scarce AI/data talent (senior pay $180k–$220k), pricey healthcare datasets ($50k–$500k+/yr), and cybersecurity vendors (market $34.5B 2024), plus compliance consultants amid €2.4bn GDPR fines (2024), all raising costs, switching barriers, and margin pressure.

| Supplier | Key stat |

|---|---|

| Cloud | 65–70% market share (top3, 2025) |

| Talent | $180k–$220k senior pay (2025) |

| Data | $50k–$500k+/dataset/yr (2024–25) |

| Cybersec | $34.5B market (2024) |

| Compliance | €2.4bn GDPR fines (2024) |

What is included in the product

Tailored exclusively for Cegedim, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A one-sheet Porter's Five Forces summary for Cegedim—instantly highlights competitive pressures and relief levers for strategic decisions.

Customers Bargaining Power

Consolidation of Pharmaceutical Giants

By 2025 pharma M&A cut the client base: top 10 global drugmakers now account for roughly 45% of industry R&D spend, concentrating demand for Cegedim’s CRM and data services in far fewer, larger buyers.

These giants wield strong bargaining power, routinely extracting double-digit volume discounts or demanding bespoke features; 2024 vendor surveys show 60% of large pharmas secured customized SaaS terms.

Losing one top-tier client can shave >5–10% off Cegedim’s ARR given its customer revenue concentration, raising churn and margin risk.

High Switching Costs for Medical Practices

For individual doctors and pharmacies, bargaining power is low because migrating patient records is costly and complex; industry estimates show EMR migrations cost €5,000–€20,000 per practice and risk 6–12% workflow downtime. Once Cegedim’s tools are embedded in daily workflows, providers face structural dependence and technical lock-in. That lock-in supports Cegedim keeping stable pricing and multi-year contracts despite a fragmented customer base; typical contract lengths exceed 3 years.

Demand for Integrated Health Analytics

By late 2025, 78% of pharma buyers surveyed want integrated, AI-driven insights linking CRM with real-world evidence (RWE), eroding tolerance for standalone data and raising customer bargaining power.

This forces Cegedim to accelerate product upgrades; failure risks churn—clients demand performance-based pricing when ROI under 12 months isn’t met, with enterprise deals now tying 15–30% of fees to outcomes.

Public Health Sector Procurement Policies

Transparent, competitive bidding and strict cost-efficiency rules empower buyers to push down margins during negotiations; public contracts in EU healthcare procurements saw average price discounts of 12–18% in 2023.

Influence of Insurance and Payor Groups

Health insurers and payors, controlling ~60–70% of EU healthcare spending in 2024, push for direct access to analytics and often set interoperability and data standards Cegedim must meet to remain in-network.

Their move to in-house analytics and preferred-platform mandates constrains Cegedim’s roadmap, forcing custom integrations and delaying feature releases, and can pressure pricing and margins.

Concentrated buyers squeeze margins: top-10 pharma, procurement & payors force discounts

Buyers are concentrated: top 10 pharma now drive ~45% of R&D spend, giving large drugmakers strong leverage to extract discounts and bespoke terms; losing one top client can cut Cegedim ARR by 5–10%. Public tenders (≈38% revenue, 2024) and EU procurements pushed prices down 12–18% in 2023, while payors (~60–70% of EU spend) demand interoperability (≈65% required FHIR, 2024), raising customization costs and outcome‑linked fees (15–30%).

| Metric | Value (year) |

|---|---|

| Top-10 pharma R&D share | ≈45% (2025) |

| Revenue from public buyers | ≈38% (2024) |

| EU public procurement discounts | 12–18% (2023) |

| Payor share of EU spend | 60–70% (2024) |

| Payors requiring FHIR | ≈65% (2024) |

| Outcome-linked fees in deals | 15–30% (2025) |

Same Document Delivered

Cegedim Porter's Five Forces Analysis

This preview shows the exact Cegedim Porter's Five Forces analysis you'll receive after purchase—no samples or placeholders, fully formatted and ready to use. It provides the complete competitive assessment, including bargaining power, supplier dynamics, threat vectors, and industry rivalry, and will be available for instant download once you buy. Use it immediately for decision-making or reporting without further setup.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Cegedim operates in a moderately concentrated healthcare IT market where bargaining power of buyers and regulatory pressures shape pricing and innovation, while established rivals and specialized suppliers limit margin expansion.

Threats from digital entrants and substitutes are rising, but Cegedim’s niche solutions, client relationships, and data assets provide defensible advantages—though execution and M&A strategy will determine long-term positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cegedim’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Cloud Infrastructure Providers

Scarcity of Specialized IT Talent

The market for healthcare-compliance and AI software developers and data scientists remained tight at end-2025, with global demand outstripping supply and median US salaries hitting roughly $180k–$220k for senior specialists per Glassdoor/LinkedIn aggregates.

These niche professionals act as vital human-capital suppliers, negotiating remote work and equity, raising Cegedim’s labor costs and bargaining power versus vendors and rivals.

Cegedim must invest in retention—estimated at 15%+ of payroll for top talent—to stop core IP migrating to Big Tech, digital-health startups, or consulting firms.

Data Acquisition and Licensing Costs

To deliver high-quality analytics and CRM services, Cegedim often licenses specialized medical datasets or integrates with third-party healthcare databases, giving these data providers notable bargaining power because Cegedim’s insights rely on that raw accuracy and depth.

Data providers' leverage rises as unique clinical, claims, and real-world evidence (RWE) sources are scarce; industry reports show commercial healthcare data licensing can cost $50k–$500k+ annually per dataset in 2024–2025 for enterprise use.

Stricter privacy rules—GDPR updates in EU and HIPAA enforcement in the US—raise compliance costs, so Cegedim faces higher acquisition and anonymization fees, increasing supplier power and squeezing margins.

Hardware and Cybersecurity Vendors

Suppliers of high-end encryption software and secure server hardware hold strong bargaining power because Cegedim depends on specialized hardware for its pharmacy and practice management systems and advanced cybersecurity to protect PHI; global healthcare cybersecurity spending reached about $34.5B in 2024, keeping premium vendors scarce and costly.

Because a breach would be catastrophic for Cegedim’s reputation and regulatory fines (HIPAA/EU GDPR), the company has limited flexibility to switch to lower-quality or unproven vendors, raising switching costs and vendor leverage.

- Healthcare cybersecurity market: $34.5B (2024)

- High switching costs due to compliance and integration

- Premium vendors command price and service terms

- Reputational/fine risk increases supplier leverage

Regulatory and Compliance Consultants

Cegedim depends on specialized regulatory and compliance consultants due to evolving healthcare laws like GDPR and country-level medical data rules; in 2024 GDPR fines totaled €2.4 billion EU-wide, underscoring high stakes. These consultants shape Cegedim’s operating framework, reducing legal risk and enabling continued market access across ~80 countries where Cegedim reports activity. Their bargaining power rises from technical expertise and scarcity of trusted firms with healthcare and cross-border data skills.

- 2024 EU GDPR fines €2.4bn

- Cegedim active in ~80 countries

- Specialist firms limited, increasing supplier leverage

Supplier squeeze: cloud, AI talent, data and compliance driving margin pressure

Cegedim faces high supplier power from concentrated cloud vendors (AWS/Azure/GCP ~65–70% IaaS/PaaS 2025), scarce AI/data talent (senior pay $180k–$220k), pricey healthcare datasets ($50k–$500k+/yr), and cybersecurity vendors (market $34.5B 2024), plus compliance consultants amid €2.4bn GDPR fines (2024), all raising costs, switching barriers, and margin pressure.

| Supplier | Key stat |

|---|---|

| Cloud | 65–70% market share (top3, 2025) |

| Talent | $180k–$220k senior pay (2025) |

| Data | $50k–$500k+/dataset/yr (2024–25) |

| Cybersec | $34.5B market (2024) |

| Compliance | €2.4bn GDPR fines (2024) |

What is included in the product

Tailored exclusively for Cegedim, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A one-sheet Porter's Five Forces summary for Cegedim—instantly highlights competitive pressures and relief levers for strategic decisions.

Customers Bargaining Power

Consolidation of Pharmaceutical Giants

By 2025 pharma M&A cut the client base: top 10 global drugmakers now account for roughly 45% of industry R&D spend, concentrating demand for Cegedim’s CRM and data services in far fewer, larger buyers.

These giants wield strong bargaining power, routinely extracting double-digit volume discounts or demanding bespoke features; 2024 vendor surveys show 60% of large pharmas secured customized SaaS terms.

Losing one top-tier client can shave >5–10% off Cegedim’s ARR given its customer revenue concentration, raising churn and margin risk.

High Switching Costs for Medical Practices

For individual doctors and pharmacies, bargaining power is low because migrating patient records is costly and complex; industry estimates show EMR migrations cost €5,000–€20,000 per practice and risk 6–12% workflow downtime. Once Cegedim’s tools are embedded in daily workflows, providers face structural dependence and technical lock-in. That lock-in supports Cegedim keeping stable pricing and multi-year contracts despite a fragmented customer base; typical contract lengths exceed 3 years.

Demand for Integrated Health Analytics

By late 2025, 78% of pharma buyers surveyed want integrated, AI-driven insights linking CRM with real-world evidence (RWE), eroding tolerance for standalone data and raising customer bargaining power.

This forces Cegedim to accelerate product upgrades; failure risks churn—clients demand performance-based pricing when ROI under 12 months isn’t met, with enterprise deals now tying 15–30% of fees to outcomes.

Public Health Sector Procurement Policies

Transparent, competitive bidding and strict cost-efficiency rules empower buyers to push down margins during negotiations; public contracts in EU healthcare procurements saw average price discounts of 12–18% in 2023.

Influence of Insurance and Payor Groups

Health insurers and payors, controlling ~60–70% of EU healthcare spending in 2024, push for direct access to analytics and often set interoperability and data standards Cegedim must meet to remain in-network.

Their move to in-house analytics and preferred-platform mandates constrains Cegedim’s roadmap, forcing custom integrations and delaying feature releases, and can pressure pricing and margins.

Concentrated buyers squeeze margins: top-10 pharma, procurement & payors force discounts

Buyers are concentrated: top 10 pharma now drive ~45% of R&D spend, giving large drugmakers strong leverage to extract discounts and bespoke terms; losing one top client can cut Cegedim ARR by 5–10%. Public tenders (≈38% revenue, 2024) and EU procurements pushed prices down 12–18% in 2023, while payors (~60–70% of EU spend) demand interoperability (≈65% required FHIR, 2024), raising customization costs and outcome‑linked fees (15–30%).

| Metric | Value (year) |

|---|---|

| Top-10 pharma R&D share | ≈45% (2025) |

| Revenue from public buyers | ≈38% (2024) |

| EU public procurement discounts | 12–18% (2023) |

| Payor share of EU spend | 60–70% (2024) |

| Payors requiring FHIR | ≈65% (2024) |

| Outcome-linked fees in deals | 15–30% (2025) |

Same Document Delivered

Cegedim Porter's Five Forces Analysis

This preview shows the exact Cegedim Porter's Five Forces analysis you'll receive after purchase—no samples or placeholders, fully formatted and ready to use. It provides the complete competitive assessment, including bargaining power, supplier dynamics, threat vectors, and industry rivalry, and will be available for instant download once you buy. Use it immediately for decision-making or reporting without further setup.