Cellcom Israel Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

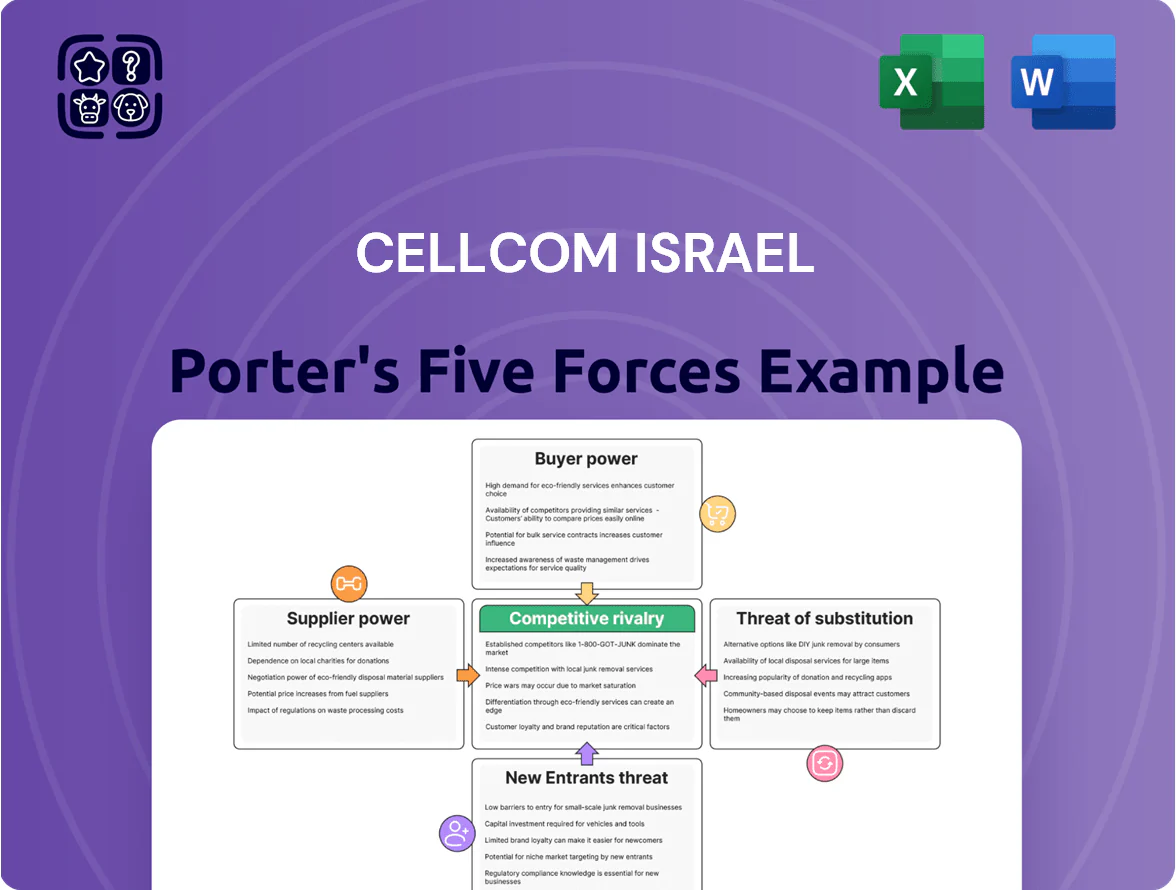

Cellcom Israel faces intense competitive rivalry, high buyer expectations, and technological disruption that compress margins and accelerate churn; supplier power and regulatory oversight further shape strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cellcom Israel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Infrastructure and Equipment Vendors

Cellcom depends on a small group of international vendors—Ericsson and Nokia—for core 5G radios and fiber-optic gear, giving suppliers strong leverage; global 5G RAN market share for these vendors was ~70% in 2024 and switching would cost Cellcom tens of millions USD and 12–24 months of downtime. High technical complexity and recurring upgrade spend (Cellcom capex on network ~NIS 1.2–1.5bn in 2024) keep vendors indispensable with firm pricing power into end-2025.

Handset and Device Manufacturers

Apple and Samsung control roughly 60% of Israel’s smartphone market in 2024, leaving Cellcom dependent for retail and financed handsets; flagship-driven customer choice forces Cellcom to accept tight wholesale margins and promotional constraints set by these vendors.

Premium Content and Media Providers

As an integrated communications provider offering TV, Cellcom negotiates broadcast rights with global studios and local creators, and paid NIS 420m for content rights in 2024, pressuring margins.

Rising sports rights and exclusive series—UEFA and Netflix-style deals—have lifted content costs industry-wide; sports rights rose about 12% globally in 2024, squeezing Cellcom’s TV unit.

Competition for high-quality streaming content remained the main TV expense driver in 2025, accounting for roughly 35% of the division’s operating costs, limiting supplier bargaining flexibility.

Electricity and Energy Utilities

Cellcom Israel is highly exposed to energy-price swings due to its tower sites, data centers, and ~200 retail stores, making electricity a material fixed cost that reduces margin flexibility.

The company has limited leverage versus the national electricity supplier (Israel Electric Corporation) and large fuel providers; in 2024 energy and site rentals accounted for roughly 6–8% of operating expenses for Israeli MNOs.

- High sensitivity: towers + data centers + stores

- Limited bargaining power vs national utility

- Costs mostly non-negotiable, 6–8% of OPEX (2024 est.)

Specialized Technical Labor Force

Israel's high demand for cybersecurity experts, network engineers, and software developers—250,000 tech workers nationwide in 2024 with R&D salaries ~30–40% above national average—creates a tight market that forces Cellcom to match offers from global R&D centers and startups, raising wage and benefits costs.

That premium gives skilled professionals and specialized unions leverage over employment terms, increasing Cellcom's operating costs and bargaining vulnerability, especially for 5G, cloud, and security projects.

- ~250,000 tech workers (2024)

- R&D pay premium ~30–40% (2024)

- Higher hiring costs for 5G/cloud/security

- Stronger union/specialist leverage

2024 Telecom Snapshot: Suppliers, Capex & Content Drive High Switching Costs

Suppliers hold strong leverage: Ericsson/Nokia ~70% 5G RAN share (2024); switching costs tens of millions USD and 12–24 months; Cellcom network capex NIS 1.2–1.5bn (2024). Apple/Samsung ~60% handset share (2024). Content rights NIS 420m (2024); sports rights +12% (2024). Energy/site costs ~6–8% OPEX (2024); tech talent ~250,000 workers, R&D pay +30–40% (2024).

| Item | 2024 |

|---|---|

| 5G RAN share | ~70% |

| Network capex | NIS 1.2–1.5bn |

| Handset share | ~60% |

| Content spend | NIS 420m |

| Energy OPEX | 6–8% |

| Tech workforce | ~250,000 |

What is included in the product

Tailored Porter's Five Forces assessment of Cellcom Israel that uncovers competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and emerging disruptors to inform strategic positioning and profitability outlook.

A concise Porter's Five Forces summary for Cellcom Israel—instantly highlights competitive pressures and regulatory risks for quick strategic decisions.

Customers Bargaining Power

Low Switching Costs and Number Portability

Israel’s regulator mandates number portability and low exit fees, so subscribers can switch carriers within 24–48 hours; this reduces Cellcom’s leverage and raises customer bargaining power.

Customers routinely chase promotions; Cellcom spent NIS 420 million on retention and handset subsidies in 2024 to curb churn.

By late 2025 churn stayed high—around 22% annualized in mobile postpaid—forcing frequent promotional campaigns and tighter margin pressure.

High Price Sensitivity in the Retail Segment

The Israeli retail market is highly price-sensitive: surveys show 68% of mobile subscribers prioritize monthly cost over brand, and comparison sites list over 120 competitive cellular/fiber offers as of Dec 2025, driving fierce price competition.

Digital aggregators let consumers compare plans in seconds, forcing Cellcom to cut prices; Cellcom’s ARPU fell 7% year-on-year to NIS 74 in FY2024 as it matched smaller MVNOs’ aggressive offers.

Availability of Multi-Service Bundles

Customers now prefer bundled mobile, fiber and TV plans; in Israel 62% of households chose multi-service bundles in 2024 per the Israel Central Bureau of Statistics, raising buyer leverage. This convergence lets buyers demand discounts up to 20–30% versus standalone pricing, squeezing ARPU (average revenue per user). To stop churn and wallet consolidation with Pelephone+Partner-like groups, Cellcom must offer competitive triple-play/quad-play bundles and promotionally match bundle pricing. Failure to do so risks losing share in a market where bundled penetration rose 8% YoY in 2024.

Institutional and Corporate Leverage

Large corporate and government clients make up roughly 20–30% of Cellcom Israel’s service revenue (2024), giving them strong bargaining power via high-volume contracts.

Formal tenders force price and SLA competition, compressing margins—public-sector deals in 2023 averaged discounts of 10–18% versus retail rates.

Dropping one major institutional contract can shave several percentage points off Cellcom’s market share and swing quarterly EBITDA by multiple millions of NIS.

- 20–30% revenue from institutions

- 2023 tenders: 10–18% avg discount

- Loss of one major contract → market-share and EBITDA hit

Information Symmetry and Digital Literacy

Israeli customers are highly digitally literate; 91% used the internet in 2024 and third-party speed tests (Ookla) and GigaNet reports make network quality transparent, raising switching risks for Cellcom.

Customers post complaints and reviews on social media and forums; a viral negative thread can cut net promoter score quickly and push subscribers toward rivals like Partner and Pelephone.

This forces Cellcom to keep reliability and support high to avoid churn—Cellcom reported a 1.2% quarterly churn in Q3 2025, so real-time reputation matters.

- High internet penetration: 91% (2024)

- Third-party speed reports shape perception

- Social media drives rapid reputation shifts

- Cellcom Q3 2025 churn: 1.2%

High churn, low ARPU and deep tender discounts squeeze margins—bundles and price rule

Customers have high bargaining power: portability and low exit fees enable quick switching (24–48h), churn hit ~22% annualized in 2025 for mobile postpaid, ARPU fell to NIS 74 in FY2024, and 62% of households chose bundles in 2024—large corporates (20–30% revenue) win 10–18% discounts in tenders, so price, bundles and reputation drive constant margin pressure.

| Metric | Value |

|---|---|

| Portability | 24–48 hours |

| Postpaid churn (2025) | ~22% annualized |

| ARPU (FY2024) | NIS 74 |

| Bundle penetration (2024) | 62% |

| Institutional revenue | 20–30% |

| Tender discounts (2023) | 10–18% |

Preview Before You Purchase

Cellcom Israel Porter's Five Forces Analysis

This preview shows the exact Cellcom Israel Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download and use the moment you buy. You're looking at the actual, professionally written file; once payment is complete, you’ll get instant access to this same deliverable. No mockups or samples—what you see is what you’ll get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Cellcom Israel faces intense competitive rivalry, high buyer expectations, and technological disruption that compress margins and accelerate churn; supplier power and regulatory oversight further shape strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cellcom Israel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Infrastructure and Equipment Vendors

Cellcom depends on a small group of international vendors—Ericsson and Nokia—for core 5G radios and fiber-optic gear, giving suppliers strong leverage; global 5G RAN market share for these vendors was ~70% in 2024 and switching would cost Cellcom tens of millions USD and 12–24 months of downtime. High technical complexity and recurring upgrade spend (Cellcom capex on network ~NIS 1.2–1.5bn in 2024) keep vendors indispensable with firm pricing power into end-2025.

Handset and Device Manufacturers

Apple and Samsung control roughly 60% of Israel’s smartphone market in 2024, leaving Cellcom dependent for retail and financed handsets; flagship-driven customer choice forces Cellcom to accept tight wholesale margins and promotional constraints set by these vendors.

Premium Content and Media Providers

As an integrated communications provider offering TV, Cellcom negotiates broadcast rights with global studios and local creators, and paid NIS 420m for content rights in 2024, pressuring margins.

Rising sports rights and exclusive series—UEFA and Netflix-style deals—have lifted content costs industry-wide; sports rights rose about 12% globally in 2024, squeezing Cellcom’s TV unit.

Competition for high-quality streaming content remained the main TV expense driver in 2025, accounting for roughly 35% of the division’s operating costs, limiting supplier bargaining flexibility.

Electricity and Energy Utilities

Cellcom Israel is highly exposed to energy-price swings due to its tower sites, data centers, and ~200 retail stores, making electricity a material fixed cost that reduces margin flexibility.

The company has limited leverage versus the national electricity supplier (Israel Electric Corporation) and large fuel providers; in 2024 energy and site rentals accounted for roughly 6–8% of operating expenses for Israeli MNOs.

- High sensitivity: towers + data centers + stores

- Limited bargaining power vs national utility

- Costs mostly non-negotiable, 6–8% of OPEX (2024 est.)

Specialized Technical Labor Force

Israel's high demand for cybersecurity experts, network engineers, and software developers—250,000 tech workers nationwide in 2024 with R&D salaries ~30–40% above national average—creates a tight market that forces Cellcom to match offers from global R&D centers and startups, raising wage and benefits costs.

That premium gives skilled professionals and specialized unions leverage over employment terms, increasing Cellcom's operating costs and bargaining vulnerability, especially for 5G, cloud, and security projects.

- ~250,000 tech workers (2024)

- R&D pay premium ~30–40% (2024)

- Higher hiring costs for 5G/cloud/security

- Stronger union/specialist leverage

2024 Telecom Snapshot: Suppliers, Capex & Content Drive High Switching Costs

Suppliers hold strong leverage: Ericsson/Nokia ~70% 5G RAN share (2024); switching costs tens of millions USD and 12–24 months; Cellcom network capex NIS 1.2–1.5bn (2024). Apple/Samsung ~60% handset share (2024). Content rights NIS 420m (2024); sports rights +12% (2024). Energy/site costs ~6–8% OPEX (2024); tech talent ~250,000 workers, R&D pay +30–40% (2024).

| Item | 2024 |

|---|---|

| 5G RAN share | ~70% |

| Network capex | NIS 1.2–1.5bn |

| Handset share | ~60% |

| Content spend | NIS 420m |

| Energy OPEX | 6–8% |

| Tech workforce | ~250,000 |

What is included in the product

Tailored Porter's Five Forces assessment of Cellcom Israel that uncovers competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and emerging disruptors to inform strategic positioning and profitability outlook.

A concise Porter's Five Forces summary for Cellcom Israel—instantly highlights competitive pressures and regulatory risks for quick strategic decisions.

Customers Bargaining Power

Low Switching Costs and Number Portability

Israel’s regulator mandates number portability and low exit fees, so subscribers can switch carriers within 24–48 hours; this reduces Cellcom’s leverage and raises customer bargaining power.

Customers routinely chase promotions; Cellcom spent NIS 420 million on retention and handset subsidies in 2024 to curb churn.

By late 2025 churn stayed high—around 22% annualized in mobile postpaid—forcing frequent promotional campaigns and tighter margin pressure.

High Price Sensitivity in the Retail Segment

The Israeli retail market is highly price-sensitive: surveys show 68% of mobile subscribers prioritize monthly cost over brand, and comparison sites list over 120 competitive cellular/fiber offers as of Dec 2025, driving fierce price competition.

Digital aggregators let consumers compare plans in seconds, forcing Cellcom to cut prices; Cellcom’s ARPU fell 7% year-on-year to NIS 74 in FY2024 as it matched smaller MVNOs’ aggressive offers.

Availability of Multi-Service Bundles

Customers now prefer bundled mobile, fiber and TV plans; in Israel 62% of households chose multi-service bundles in 2024 per the Israel Central Bureau of Statistics, raising buyer leverage. This convergence lets buyers demand discounts up to 20–30% versus standalone pricing, squeezing ARPU (average revenue per user). To stop churn and wallet consolidation with Pelephone+Partner-like groups, Cellcom must offer competitive triple-play/quad-play bundles and promotionally match bundle pricing. Failure to do so risks losing share in a market where bundled penetration rose 8% YoY in 2024.

Institutional and Corporate Leverage

Large corporate and government clients make up roughly 20–30% of Cellcom Israel’s service revenue (2024), giving them strong bargaining power via high-volume contracts.

Formal tenders force price and SLA competition, compressing margins—public-sector deals in 2023 averaged discounts of 10–18% versus retail rates.

Dropping one major institutional contract can shave several percentage points off Cellcom’s market share and swing quarterly EBITDA by multiple millions of NIS.

- 20–30% revenue from institutions

- 2023 tenders: 10–18% avg discount

- Loss of one major contract → market-share and EBITDA hit

Information Symmetry and Digital Literacy

Israeli customers are highly digitally literate; 91% used the internet in 2024 and third-party speed tests (Ookla) and GigaNet reports make network quality transparent, raising switching risks for Cellcom.

Customers post complaints and reviews on social media and forums; a viral negative thread can cut net promoter score quickly and push subscribers toward rivals like Partner and Pelephone.

This forces Cellcom to keep reliability and support high to avoid churn—Cellcom reported a 1.2% quarterly churn in Q3 2025, so real-time reputation matters.

- High internet penetration: 91% (2024)

- Third-party speed reports shape perception

- Social media drives rapid reputation shifts

- Cellcom Q3 2025 churn: 1.2%

High churn, low ARPU and deep tender discounts squeeze margins—bundles and price rule

Customers have high bargaining power: portability and low exit fees enable quick switching (24–48h), churn hit ~22% annualized in 2025 for mobile postpaid, ARPU fell to NIS 74 in FY2024, and 62% of households chose bundles in 2024—large corporates (20–30% revenue) win 10–18% discounts in tenders, so price, bundles and reputation drive constant margin pressure.

| Metric | Value |

|---|---|

| Portability | 24–48 hours |

| Postpaid churn (2025) | ~22% annualized |

| ARPU (FY2024) | NIS 74 |

| Bundle penetration (2024) | 62% |

| Institutional revenue | 20–30% |

| Tender discounts (2023) | 10–18% |

Preview Before You Purchase

Cellcom Israel Porter's Five Forces Analysis

This preview shows the exact Cellcom Israel Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download and use the moment you buy. You're looking at the actual, professionally written file; once payment is complete, you’ll get instant access to this same deliverable. No mockups or samples—what you see is what you’ll get.