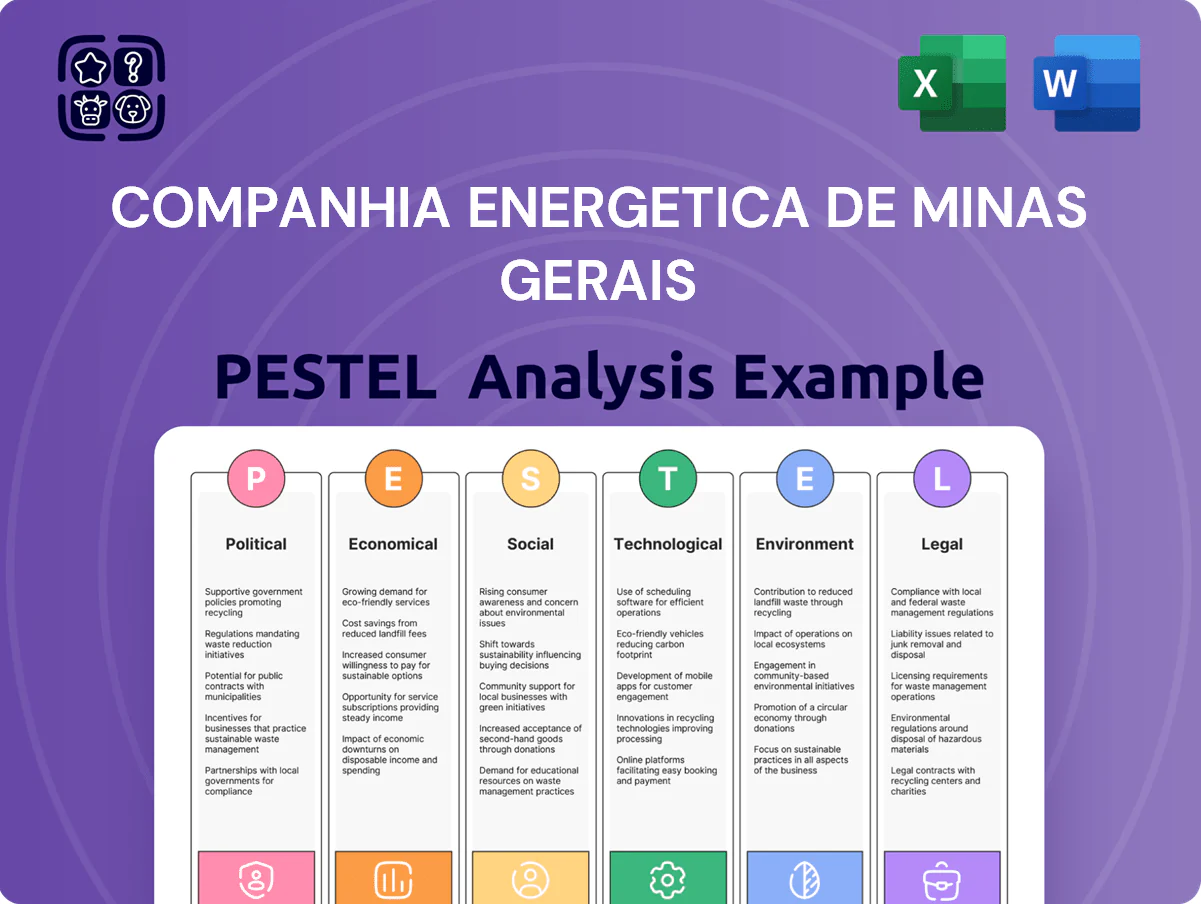

Companhia Energetica de Minas Gerais PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, commodity prices, and Brazil's energy transition are reshaping Companhia Energética de Minas Gerais—our PESTLE snapshot highlights key external pressures and opportunities that matter to investors and strategists.

From political risk and tariff reform to technological innovation in renewables and mounting environmental obligations, this concise analysis pinpoints trends that could alter CEMIG’s competitive positioning and cash flows.

Purchase the full PESTLE report for a detailed, actionable breakdown—ready to use in investment models, strategic plans, and board-level briefings; download instantly to inform smarter decisions.

Political factors

State Government Influence

As a state-controlled utility, Cemig's strategy and capital allocation are closely tied to Minas Gerais' fiscal position; the state held ~37.3% voting stake as of 2025, and the 2024 fiscal deficit prompted higher pressure on dividends. Political appointments to Cemig’s board have driven shifts toward social tariffs and off-balance concessions, affecting operational efficiency and credit metrics—net debt/EBITDA was ~3.1x in 2024. Dividend decisions often trade off the state's short-term budget needs against Cemig’s investment plan.

Privatization Debates

The privatization debate around Cemig intensified in late 2025 as proposals in the Minas Gerais assembly targeted sale of up to 49% of state-held shares, while polls showed 58% of local respondents opposing full privatization; legislative approval remains uncertain. Lawmakers face fiscal pressures—Minas Gerais recorded a 2025 budget deficit of R$6.2 billion—pushing privatization back onto the agenda but requiring regulatory changes. Investors track session outcomes and draft bills because any shift could revalue Cemig’s market cap (R$18.4 billion as of Q3 2025) and impact tariff regulation prospects.

Federal Energy Policy

The federal government's emphasis on energy security and tariff subsidies compresses Cemig's margins; government-regulated tariffs and the 2024 subsidized social energy program reduced average distribution tariffs by about 4.2%, pressuring 2024 EBITDA which fell 3.8% year-on-year.

Ministry of Mines and Energy directives on the national interconnected system can reprioritize dispatch for hydro plants, affecting Cemig's generation revenue volatility; in 2025 hydrological risk shifted dispatch leading to a ~6% swing in quarterly generation output.

Federal geopolitical alignments raised import costs for turbines and transformers after 2023–24 trade tensions, contributing to a 12–18% increase in imported equipment prices and elevating Cemig's capital expenditure projections for 2025–26.

Regulatory Agency Stability

The relationship with ANEEL is sensitive to political shifts; agency independence affects tariff-setting that determined Cemig Distribuição’s RAB-linked allowed revenues—Cemig reported R$12.8bn regulated asset base in 2024. Political pressure to cap tariffs during 2023–24 inflation spikes compressed distribution margins, contributing to a 6.1% drop in adjusted EBITDA in FY2024.

Maintaining transparent dialogue during ANEEL tariff reviews is critical: the 2024 periodic review altered revenue assumptions by ~2.3 p.p., directly impacting cash flow projections and investment planning.

- ANEEL independence crucial for stable tariff formula

- R$12.8bn RAB (2024) ties regulatory outcomes to earnings

- Tariff caps amid 2023–24 inflation cut adjusted EBITDA by 6.1%

- 2024 review changed revenue assumptions ~2.3 percentage points

Geopolitical Impact on Supply Chains

Global political tensions, including 2024–25 trade frictions, raised transformer and solar panel prices by ~8–12%, tightening Cemig's project margins and delaying 2024 CAPEX of R$2.1bn for renewables.

Brazil–China trade policies and tariffs affect import lead times; bilateral logistics slowdowns in 2024 increased component lead times by ~15%, pressuring Cemig procurement.

Strategic procurement shifts—nearshoring, diversified suppliers, and multi-year contracts—are being used to hedge against international disputes and stabilize capital expenditure forecasts.

- Transformer/solar price rise: 8–12% (2024–25)

- Cemig 2024 renewables CAPEX: R$2.1bn

- Import lead times up ~15% in 2024

- Mitigations: nearshoring, supplier diversification, multi-year contracts

Cemig’s state ties, rising capex and regulatory shifts squeeze dividends and leverage

State control (~37.3% voting stake in 2025) ties Cemig to Minas Gerais' fiscal needs (2025 deficit R$6.2bn), influencing dividends vs capex; net debt/EBITDA ~3.1x (2024). Regulatory risk: ANEEL independence and 2024 periodic review swung revenue assumptions ~2.3 p.p., RAB R$12.8bn (2024). Trade tensions raised equipment prices 8–18% (2023–25), lengthening lead times ~15% and hiking 2025–26 CAPEX.

| Metric | Value |

|---|---|

| State stake (2025) | ~37.3% |

| Minas Gerais deficit (2025) | R$6.2bn |

| Net debt/EBITDA (2024) | ~3.1x |

| RAB (2024) | R$12.8bn |

| Revenue swing (2024 review) | ~2.3 p.p. |

| Equipment price rise (2023–25) | 8–18% |

| Import lead times increase (2024) | ~15% |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces specifically shape Companhia Energética de Minas Gerais’s strategy and operations, with data-driven trends and forward-looking insights to inform executives, investors, and strategists.

A concise, PESTLE-segmented brief that distills Companhia Energética de Minas Gerais' external risks and opportunities into a slide-ready summary for fast decision-making and stakeholder alignment.

Economic factors

Interest Rate Volatility

Fluctuations in the SELIC rate—which averaged 11.75% in 2023 and was cut to 9.25% by Dec 2024—directly raise or lower Cemig’s debt servicing costs and weighted average cost of capital for new projects; a 100 bps rise increases interest expense on its R$15.8bn net debt by roughly R$158m annually. High rates deter investment in large transmission and generation builds, while easing rates improve long-term project NPV and make Cemig’s dividends more attractive to yield-seeking investors.

Inflation and Indexation

Cemig indexes much of its tariff revenue to IPCA and IGPM per concession contracts, with 2024 pass-through helping protect top-line growth as Brazil’s IPCA was 4.5% in 2024 and IGPM 6.9% year-on-year to Dec 2024.

Despite this hedge, IGPM spikes in 2023–24 caused ANEEL to approve temporary regulatory adjustments, creating short-term timing mismatches between inflation and cash receipts.

In 2024, rising O&M and fuel costs pressured margins—controlling costs is vital to sustain EBITDA, which for Cemig’s distribution segment fell 2–3% year-on-year in FY2024.

Industrial Demand in Minas Gerais

The mining and metallurgical sectors in Minas Gerais account for roughly 35% of Cemig’s industrial load, with iron ore output and steel production driving peak demand; in 2024 Minas Gerais exported about $25.6bn of iron ore-related products, linking Cemig consumption to global commodity cycles.

Commodity price swings—iron ore fell ~18% in 2024 vs 2023—translate into lower utilization rates for major industrial clients, directly reducing Cemig’s large-user energy sales and revenue volatility.

Client diversification remains critical: Cemig reported that its top 10 industrial clients represented ~42% of industrial revenue in 2024, so expanding into services, renewables supply contracts, and smaller commercial accounts mitigates regional downturn risk.

Currency Exchange Fluctuations

The Brazilian Real's 2024 average of ~R$5.20/USD and a 2025 YTD range of R$4.80–5.50 pressure Cemig's cost base, raising prices for imported turbines and inverters and increasing servicing costs on roughly $1.2bn of dollar-linked debt.

Capital goods for Cemig's renewables projects remain exchange-rate sensitive despite domestic revenues; a 10% depreciation can raise project capex by ~8–12% depending on component mix.

Management uses forward contracts and cross-currency swaps; Cemig reported hedges covering about 60% of anticipated FX exposure through 2026 to limit P&L volatility.

- Real vs USD: avg R$5.20 (2024); 2025 YTD R$4.80–5.50

- Dollar-linked debt ≈ $1.2bn

- 10% depreciation → capex +8–12%

- Hedges cover ~60% of exposure through 2026

Energy Market Liberalization

The ACL grew to 38% of Brazil’s industrial consumption by 2024, accelerating migration of high-voltage clients and intensifying competition for Cemig Comercialização, forcing adoption of dynamic pricing and hedging; Cemig reported a 12% revenue decline in regulated supply in 2023 while commercialization margins improved by 6% as of 9M2025.

Distribution revenues face pressure as ~25% of large consumers in Minas Gerais moved to the free market by 2024, requiring enhanced retention programs, bespoke contracts, and analytics-driven tariff segmentation to protect load and margin.

- ACL share 38% of industrial consumption (2024)

- Cemig regulated supply revenue down 12% (2023)

- Commercialization margins +6% (9M2025)

- ~25% of large MG consumers migrated to free market (2024)

Lower SELIC, FX risk pressure capex and boost NPVs amid iron‑ore slump

SELIC cuts to 9.25% by Dec 2024 lowered debt service; 100bps change ≈ R$158m on R$15.8bn net debt, improving project NPVs. IPCA 4.5% and IGP-M 6.9% (2024) provide tariff pass-through but ANEEL timing mismatches hit cash flow. Iron ore exports from Minas Gerais ~$25.6bn (2024) tie demand to commodity swings (iron ore -18% in 2024), reducing large-user load. FX avg R$5.20/USD (2024) and $1.2bn dollar debt make capex sensitive; 10% depreciation → capex +8–12%.

| Metric | 2024/2025 |

|---|---|

| SELIC (Dec 2024) | 9.25% |

| Net debt | R$15.8bn |

| IPCA / IGP-M (2024) | 4.5% / 6.9% |

| Iron ore exports (Minas Gerais) | $25.6bn |

| Iron ore price change (2024) | -18% |

| FX avg (2024) | R$5.20/USD |

| Dollar-linked debt | $1.2bn |

| Hedge coverage | ~60% through 2026 |

Preview the Actual Deliverable

Companhia Energetica de Minas Gerais PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; this PESTLE analysis of Companhia Energética de Minas Gerais presents the same content, structure, and professional layout you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, commodity prices, and Brazil's energy transition are reshaping Companhia Energética de Minas Gerais—our PESTLE snapshot highlights key external pressures and opportunities that matter to investors and strategists.

From political risk and tariff reform to technological innovation in renewables and mounting environmental obligations, this concise analysis pinpoints trends that could alter CEMIG’s competitive positioning and cash flows.

Purchase the full PESTLE report for a detailed, actionable breakdown—ready to use in investment models, strategic plans, and board-level briefings; download instantly to inform smarter decisions.

Political factors

State Government Influence

As a state-controlled utility, Cemig's strategy and capital allocation are closely tied to Minas Gerais' fiscal position; the state held ~37.3% voting stake as of 2025, and the 2024 fiscal deficit prompted higher pressure on dividends. Political appointments to Cemig’s board have driven shifts toward social tariffs and off-balance concessions, affecting operational efficiency and credit metrics—net debt/EBITDA was ~3.1x in 2024. Dividend decisions often trade off the state's short-term budget needs against Cemig’s investment plan.

Privatization Debates

The privatization debate around Cemig intensified in late 2025 as proposals in the Minas Gerais assembly targeted sale of up to 49% of state-held shares, while polls showed 58% of local respondents opposing full privatization; legislative approval remains uncertain. Lawmakers face fiscal pressures—Minas Gerais recorded a 2025 budget deficit of R$6.2 billion—pushing privatization back onto the agenda but requiring regulatory changes. Investors track session outcomes and draft bills because any shift could revalue Cemig’s market cap (R$18.4 billion as of Q3 2025) and impact tariff regulation prospects.

Federal Energy Policy

The federal government's emphasis on energy security and tariff subsidies compresses Cemig's margins; government-regulated tariffs and the 2024 subsidized social energy program reduced average distribution tariffs by about 4.2%, pressuring 2024 EBITDA which fell 3.8% year-on-year.

Ministry of Mines and Energy directives on the national interconnected system can reprioritize dispatch for hydro plants, affecting Cemig's generation revenue volatility; in 2025 hydrological risk shifted dispatch leading to a ~6% swing in quarterly generation output.

Federal geopolitical alignments raised import costs for turbines and transformers after 2023–24 trade tensions, contributing to a 12–18% increase in imported equipment prices and elevating Cemig's capital expenditure projections for 2025–26.

Regulatory Agency Stability

The relationship with ANEEL is sensitive to political shifts; agency independence affects tariff-setting that determined Cemig Distribuição’s RAB-linked allowed revenues—Cemig reported R$12.8bn regulated asset base in 2024. Political pressure to cap tariffs during 2023–24 inflation spikes compressed distribution margins, contributing to a 6.1% drop in adjusted EBITDA in FY2024.

Maintaining transparent dialogue during ANEEL tariff reviews is critical: the 2024 periodic review altered revenue assumptions by ~2.3 p.p., directly impacting cash flow projections and investment planning.

- ANEEL independence crucial for stable tariff formula

- R$12.8bn RAB (2024) ties regulatory outcomes to earnings

- Tariff caps amid 2023–24 inflation cut adjusted EBITDA by 6.1%

- 2024 review changed revenue assumptions ~2.3 percentage points

Geopolitical Impact on Supply Chains

Global political tensions, including 2024–25 trade frictions, raised transformer and solar panel prices by ~8–12%, tightening Cemig's project margins and delaying 2024 CAPEX of R$2.1bn for renewables.

Brazil–China trade policies and tariffs affect import lead times; bilateral logistics slowdowns in 2024 increased component lead times by ~15%, pressuring Cemig procurement.

Strategic procurement shifts—nearshoring, diversified suppliers, and multi-year contracts—are being used to hedge against international disputes and stabilize capital expenditure forecasts.

- Transformer/solar price rise: 8–12% (2024–25)

- Cemig 2024 renewables CAPEX: R$2.1bn

- Import lead times up ~15% in 2024

- Mitigations: nearshoring, supplier diversification, multi-year contracts

Cemig’s state ties, rising capex and regulatory shifts squeeze dividends and leverage

State control (~37.3% voting stake in 2025) ties Cemig to Minas Gerais' fiscal needs (2025 deficit R$6.2bn), influencing dividends vs capex; net debt/EBITDA ~3.1x (2024). Regulatory risk: ANEEL independence and 2024 periodic review swung revenue assumptions ~2.3 p.p., RAB R$12.8bn (2024). Trade tensions raised equipment prices 8–18% (2023–25), lengthening lead times ~15% and hiking 2025–26 CAPEX.

| Metric | Value |

|---|---|

| State stake (2025) | ~37.3% |

| Minas Gerais deficit (2025) | R$6.2bn |

| Net debt/EBITDA (2024) | ~3.1x |

| RAB (2024) | R$12.8bn |

| Revenue swing (2024 review) | ~2.3 p.p. |

| Equipment price rise (2023–25) | 8–18% |

| Import lead times increase (2024) | ~15% |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces specifically shape Companhia Energética de Minas Gerais’s strategy and operations, with data-driven trends and forward-looking insights to inform executives, investors, and strategists.

A concise, PESTLE-segmented brief that distills Companhia Energética de Minas Gerais' external risks and opportunities into a slide-ready summary for fast decision-making and stakeholder alignment.

Economic factors

Interest Rate Volatility

Fluctuations in the SELIC rate—which averaged 11.75% in 2023 and was cut to 9.25% by Dec 2024—directly raise or lower Cemig’s debt servicing costs and weighted average cost of capital for new projects; a 100 bps rise increases interest expense on its R$15.8bn net debt by roughly R$158m annually. High rates deter investment in large transmission and generation builds, while easing rates improve long-term project NPV and make Cemig’s dividends more attractive to yield-seeking investors.

Inflation and Indexation

Cemig indexes much of its tariff revenue to IPCA and IGPM per concession contracts, with 2024 pass-through helping protect top-line growth as Brazil’s IPCA was 4.5% in 2024 and IGPM 6.9% year-on-year to Dec 2024.

Despite this hedge, IGPM spikes in 2023–24 caused ANEEL to approve temporary regulatory adjustments, creating short-term timing mismatches between inflation and cash receipts.

In 2024, rising O&M and fuel costs pressured margins—controlling costs is vital to sustain EBITDA, which for Cemig’s distribution segment fell 2–3% year-on-year in FY2024.

Industrial Demand in Minas Gerais

The mining and metallurgical sectors in Minas Gerais account for roughly 35% of Cemig’s industrial load, with iron ore output and steel production driving peak demand; in 2024 Minas Gerais exported about $25.6bn of iron ore-related products, linking Cemig consumption to global commodity cycles.

Commodity price swings—iron ore fell ~18% in 2024 vs 2023—translate into lower utilization rates for major industrial clients, directly reducing Cemig’s large-user energy sales and revenue volatility.

Client diversification remains critical: Cemig reported that its top 10 industrial clients represented ~42% of industrial revenue in 2024, so expanding into services, renewables supply contracts, and smaller commercial accounts mitigates regional downturn risk.

Currency Exchange Fluctuations

The Brazilian Real's 2024 average of ~R$5.20/USD and a 2025 YTD range of R$4.80–5.50 pressure Cemig's cost base, raising prices for imported turbines and inverters and increasing servicing costs on roughly $1.2bn of dollar-linked debt.

Capital goods for Cemig's renewables projects remain exchange-rate sensitive despite domestic revenues; a 10% depreciation can raise project capex by ~8–12% depending on component mix.

Management uses forward contracts and cross-currency swaps; Cemig reported hedges covering about 60% of anticipated FX exposure through 2026 to limit P&L volatility.

- Real vs USD: avg R$5.20 (2024); 2025 YTD R$4.80–5.50

- Dollar-linked debt ≈ $1.2bn

- 10% depreciation → capex +8–12%

- Hedges cover ~60% of exposure through 2026

Energy Market Liberalization

The ACL grew to 38% of Brazil’s industrial consumption by 2024, accelerating migration of high-voltage clients and intensifying competition for Cemig Comercialização, forcing adoption of dynamic pricing and hedging; Cemig reported a 12% revenue decline in regulated supply in 2023 while commercialization margins improved by 6% as of 9M2025.

Distribution revenues face pressure as ~25% of large consumers in Minas Gerais moved to the free market by 2024, requiring enhanced retention programs, bespoke contracts, and analytics-driven tariff segmentation to protect load and margin.

- ACL share 38% of industrial consumption (2024)

- Cemig regulated supply revenue down 12% (2023)

- Commercialization margins +6% (9M2025)

- ~25% of large MG consumers migrated to free market (2024)

Lower SELIC, FX risk pressure capex and boost NPVs amid iron‑ore slump

SELIC cuts to 9.25% by Dec 2024 lowered debt service; 100bps change ≈ R$158m on R$15.8bn net debt, improving project NPVs. IPCA 4.5% and IGP-M 6.9% (2024) provide tariff pass-through but ANEEL timing mismatches hit cash flow. Iron ore exports from Minas Gerais ~$25.6bn (2024) tie demand to commodity swings (iron ore -18% in 2024), reducing large-user load. FX avg R$5.20/USD (2024) and $1.2bn dollar debt make capex sensitive; 10% depreciation → capex +8–12%.

| Metric | 2024/2025 |

|---|---|

| SELIC (Dec 2024) | 9.25% |

| Net debt | R$15.8bn |

| IPCA / IGP-M (2024) | 4.5% / 6.9% |

| Iron ore exports (Minas Gerais) | $25.6bn |

| Iron ore price change (2024) | -18% |

| FX avg (2024) | R$5.20/USD |

| Dollar-linked debt | $1.2bn |

| Hedge coverage | ~60% through 2026 |

Preview the Actual Deliverable

Companhia Energetica de Minas Gerais PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; this PESTLE analysis of Companhia Energética de Minas Gerais presents the same content, structure, and professional layout you’ll download immediately after payment.