Cengage Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

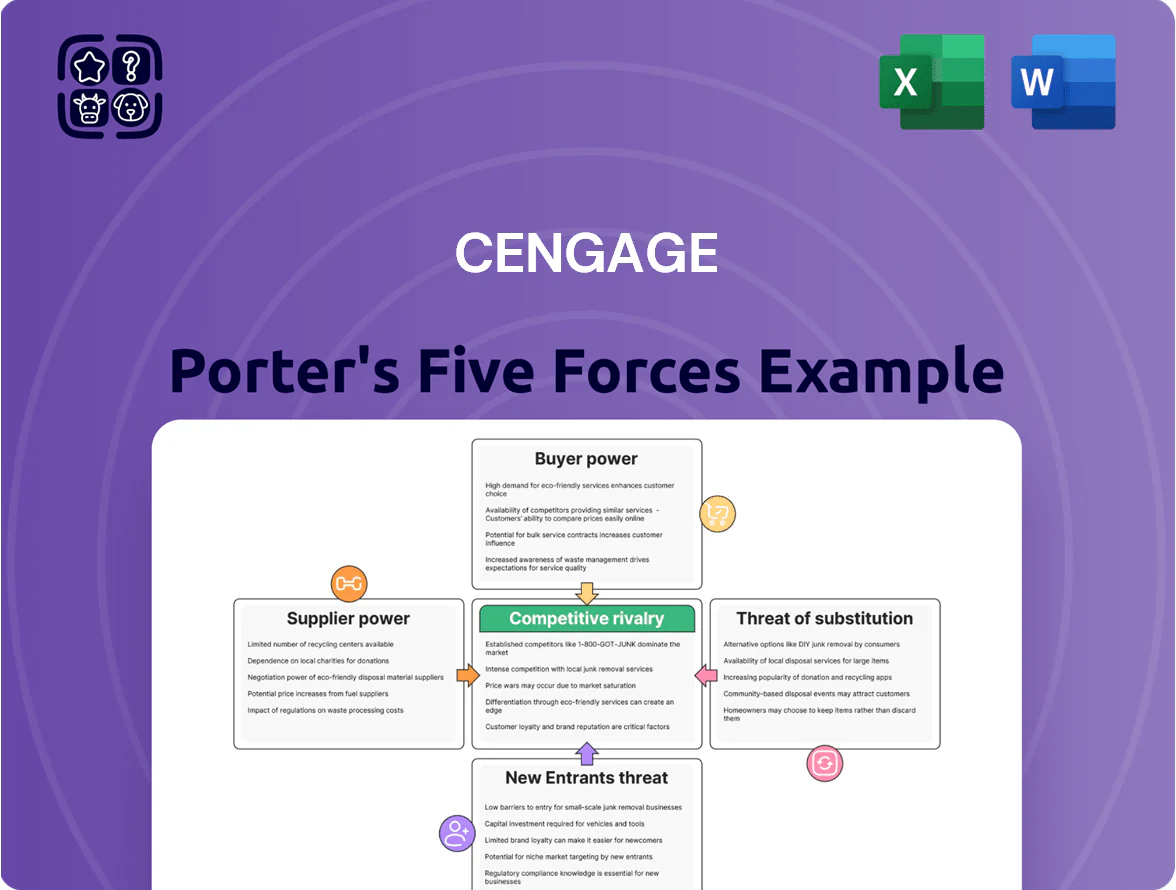

Cengage faces moderate supplier power and high buyer sensitivity amid digital disruption, with substitution threats from free edtech resources and steady competitive rivalry from major publishers and platform providers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cengage’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Academic Authors and Subject Matter Experts

The primary suppliers for Cengage are academic authors and subject-matter experts who create the core IP for textbooks and digital courses; top-tier authors command higher fees but represent a small share of titles.

A large global pool of academic talent—over 4 million higher-education faculty in the US and EU combined as of 2024—limits collective bargaining power, keeping supplier leverage moderate.

Cengage retains leverage through global distribution, library and campus licensing, and the MindTap/Learn platform, which together drove about $1.6B in 2024 digital revenue, assets individual authors can’t match.

Cloud Infrastructure and SaaS Providers

As Cengage shifts digital-first, reliance on cloud providers like Amazon Web Services and Microsoft Azure grows, giving suppliers moderate bargaining power because migrating 10s of TB of content and integrated LMS (learning management system) components incurs high technical and cost barriers.

Third-Party Content and Licensing Partners

Cengage licenses specialized media, software, and assessment tools from external vendors to boost digital course value, and these suppliers gain leverage when their proprietary components power high-demand courses or professional-cert programs.

Supplier pressure rose in 2024 as Cengage reported 63% of revenue from digital and services; losing a unique vendor could disrupt adoption and margins in niche catalogs.

To reduce risk, Cengage builds in-house replacements and diversified licensing — by 2025 it aimed to cut single-vendor dependency by 30% across core titles.

Specialized AI and Software Developers

Specialized AI and software developers command strong supplier power for Cengage in 2025 because personalized learning features need niche AI-integration experts and firms, scarce in EdTech.

Global estimates show a 35% shortfall in senior AI engineers for education platforms in 2024–25, boosting supplier leverage and premium rates.

Cengage must use competitive partnerships, earnouts, or targeted acquisitions—often costing $10M–$200M per deal—to secure tech access and keep pace.

- 35% shortfall in senior AI engineers (2024–25)

- Acquisition price range: $10M–$200M

- Options: partnerships, earnouts, equity incentives

Paper and Printing Logistics Providers

Paper and printing suppliers remain relevant because physical textbooks still account for about 25% of tertiary textbook revenue globally in 2024, but their bargaining power is low as demand for print fell ~8% CAGR 2019–24. Cengage can negotiate lower unit costs and longer-term print contracts as volumes decline, though raw-material shocks (pulp price spikes: +22% in 2022) pose residual supply-chain risk.

- Print = ~25% of revenue (2024)

- Print demand −8% CAGR 2019–24

- Pulp price spike +22% in 2022

- Low supplier leverage; negotiation upside for Cengage

Moderate supplier power: authors command premiums, AI/cloud leverage rises as digital leads

Supplier power for Cengage is moderate: authors and SMEs are many (4M+ faculty US/EU 2024) but top authors demand premiums; cloud and niche AI vendors exert rising leverage amid digital revenue of ~$1.6B in 2024 and 63% digital mix; print suppliers have low power as print = ~25% revenue (2024) with −8% CAGR 2019–24.

| Metric | Value |

|---|---|

| Digital revenue (2024) | $1.6B |

| Digital share (2024) | 63% |

| Faculty pool (US+EU, 2024) | 4M+ |

| Print share (2024) | 25% |

| Print demand CAGR 2019–24 | −8% |

| AI engineer shortfall (2024–25) | 35% |

What is included in the product

Tailored Porter's Five Forces analysis for Cengage that uncovers competitive pressures, buyer/supplier influence, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers to protect and grow market share.

A concise Porter's Five Forces summary tailored to Cengage—helps teams quickly spot competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Individual Student Price Sensitivity

Institutional Procurement and Bulk Licensing

Large universities and K-12 districts wield strong buyer power, negotiating cohort-wide licenses that forced textbook and digital-provider discounts of 20–40% on average in 2024, per EDUCAUSE procurement surveys.

They demand LMS integration (Canvas, Blackboard, Moodle) and API/customization, raising Cengage’s implementation cost but locking multi-year deals that supplied ~55% of institutional digital revenue in FY2024.

Faculty Influence on Material Selection

In higher education, faculty drive adoption: 85% of course material decisions are faculty-led, so professors’ preference for pedagogical tools and platform ease-of-use directly shapes Cengage’s market share.

Cengage spent $190 million on faculty-facing marketing and professional development in FY2024 to influence adoption and maintain preferred status in classrooms nationwide.

Although students pay, faculty bargaining power is high because their selections determine purchase rates and renewal of digital courseware licenses.

Growth of Subscription Model Expectations

The rise of Netflix-style subscriptions has shifted student and institutional expectations toward flat-fee, continuously updated access; Cengage’s 2024 Revel digital subscriptions reported a 22% YoY uplift in engagement, raising stakes for content freshness and cross-device sync.

Because users can cancel easily and compare services, buyer power grows—industry churn for edtech subscriptions averaged ~18% in 2023—so perceived value must exceed low switching costs to retain revenue.

- Expect continuous updates and cross-platform access

- 2024 engagement +22% for subscription offerings

- Edtech subscription churn ~18% (2023)

- Low switching costs increase buyer leverage

Alternative Credentialing Seekers

- 58% US workers reskilling (2024)

- 20–40% reported salary uplift from credentials

- High vendor choice → strong customer bargaining

- Career outcomes + employer ties = retention

High buyer power: price‑sensitive students, faculty-driven adoptions, institutions cut 20–40%

| Metric | Value |

|---|---|

| Avg new textbook (2024) | $129 |

| Annual student spend | $700 |

| Subscription churn (2023) | 18% |

| Institutional revenue share (FY2024) | 55% |

| Faculty influence on adoptions | 85% |

| Workers reskilling (2024) | 58% |

What You See Is What You Get

Cengage Porter's Five Forces Analysis

This preview shows the exact Cengage Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

No mockups or edits; this is the final, ready-to-use analysis delivered instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cengage faces moderate supplier power and high buyer sensitivity amid digital disruption, with substitution threats from free edtech resources and steady competitive rivalry from major publishers and platform providers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cengage’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Academic Authors and Subject Matter Experts

The primary suppliers for Cengage are academic authors and subject-matter experts who create the core IP for textbooks and digital courses; top-tier authors command higher fees but represent a small share of titles.

A large global pool of academic talent—over 4 million higher-education faculty in the US and EU combined as of 2024—limits collective bargaining power, keeping supplier leverage moderate.

Cengage retains leverage through global distribution, library and campus licensing, and the MindTap/Learn platform, which together drove about $1.6B in 2024 digital revenue, assets individual authors can’t match.

Cloud Infrastructure and SaaS Providers

As Cengage shifts digital-first, reliance on cloud providers like Amazon Web Services and Microsoft Azure grows, giving suppliers moderate bargaining power because migrating 10s of TB of content and integrated LMS (learning management system) components incurs high technical and cost barriers.

Third-Party Content and Licensing Partners

Cengage licenses specialized media, software, and assessment tools from external vendors to boost digital course value, and these suppliers gain leverage when their proprietary components power high-demand courses or professional-cert programs.

Supplier pressure rose in 2024 as Cengage reported 63% of revenue from digital and services; losing a unique vendor could disrupt adoption and margins in niche catalogs.

To reduce risk, Cengage builds in-house replacements and diversified licensing — by 2025 it aimed to cut single-vendor dependency by 30% across core titles.

Specialized AI and Software Developers

Specialized AI and software developers command strong supplier power for Cengage in 2025 because personalized learning features need niche AI-integration experts and firms, scarce in EdTech.

Global estimates show a 35% shortfall in senior AI engineers for education platforms in 2024–25, boosting supplier leverage and premium rates.

Cengage must use competitive partnerships, earnouts, or targeted acquisitions—often costing $10M–$200M per deal—to secure tech access and keep pace.

- 35% shortfall in senior AI engineers (2024–25)

- Acquisition price range: $10M–$200M

- Options: partnerships, earnouts, equity incentives

Paper and Printing Logistics Providers

Paper and printing suppliers remain relevant because physical textbooks still account for about 25% of tertiary textbook revenue globally in 2024, but their bargaining power is low as demand for print fell ~8% CAGR 2019–24. Cengage can negotiate lower unit costs and longer-term print contracts as volumes decline, though raw-material shocks (pulp price spikes: +22% in 2022) pose residual supply-chain risk.

- Print = ~25% of revenue (2024)

- Print demand −8% CAGR 2019–24

- Pulp price spike +22% in 2022

- Low supplier leverage; negotiation upside for Cengage

Moderate supplier power: authors command premiums, AI/cloud leverage rises as digital leads

Supplier power for Cengage is moderate: authors and SMEs are many (4M+ faculty US/EU 2024) but top authors demand premiums; cloud and niche AI vendors exert rising leverage amid digital revenue of ~$1.6B in 2024 and 63% digital mix; print suppliers have low power as print = ~25% revenue (2024) with −8% CAGR 2019–24.

| Metric | Value |

|---|---|

| Digital revenue (2024) | $1.6B |

| Digital share (2024) | 63% |

| Faculty pool (US+EU, 2024) | 4M+ |

| Print share (2024) | 25% |

| Print demand CAGR 2019–24 | −8% |

| AI engineer shortfall (2024–25) | 35% |

What is included in the product

Tailored Porter's Five Forces analysis for Cengage that uncovers competitive pressures, buyer/supplier influence, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers to protect and grow market share.

A concise Porter's Five Forces summary tailored to Cengage—helps teams quickly spot competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Individual Student Price Sensitivity

Institutional Procurement and Bulk Licensing

Large universities and K-12 districts wield strong buyer power, negotiating cohort-wide licenses that forced textbook and digital-provider discounts of 20–40% on average in 2024, per EDUCAUSE procurement surveys.

They demand LMS integration (Canvas, Blackboard, Moodle) and API/customization, raising Cengage’s implementation cost but locking multi-year deals that supplied ~55% of institutional digital revenue in FY2024.

Faculty Influence on Material Selection

In higher education, faculty drive adoption: 85% of course material decisions are faculty-led, so professors’ preference for pedagogical tools and platform ease-of-use directly shapes Cengage’s market share.

Cengage spent $190 million on faculty-facing marketing and professional development in FY2024 to influence adoption and maintain preferred status in classrooms nationwide.

Although students pay, faculty bargaining power is high because their selections determine purchase rates and renewal of digital courseware licenses.

Growth of Subscription Model Expectations

The rise of Netflix-style subscriptions has shifted student and institutional expectations toward flat-fee, continuously updated access; Cengage’s 2024 Revel digital subscriptions reported a 22% YoY uplift in engagement, raising stakes for content freshness and cross-device sync.

Because users can cancel easily and compare services, buyer power grows—industry churn for edtech subscriptions averaged ~18% in 2023—so perceived value must exceed low switching costs to retain revenue.

- Expect continuous updates and cross-platform access

- 2024 engagement +22% for subscription offerings

- Edtech subscription churn ~18% (2023)

- Low switching costs increase buyer leverage

Alternative Credentialing Seekers

- 58% US workers reskilling (2024)

- 20–40% reported salary uplift from credentials

- High vendor choice → strong customer bargaining

- Career outcomes + employer ties = retention

High buyer power: price‑sensitive students, faculty-driven adoptions, institutions cut 20–40%

| Metric | Value |

|---|---|

| Avg new textbook (2024) | $129 |

| Annual student spend | $700 |

| Subscription churn (2023) | 18% |

| Institutional revenue share (FY2024) | 55% |

| Faculty influence on adoptions | 85% |

| Workers reskilling (2024) | 58% |

What You See Is What You Get

Cengage Porter's Five Forces Analysis

This preview shows the exact Cengage Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

No mockups or edits; this is the final, ready-to-use analysis delivered instantly upon payment.