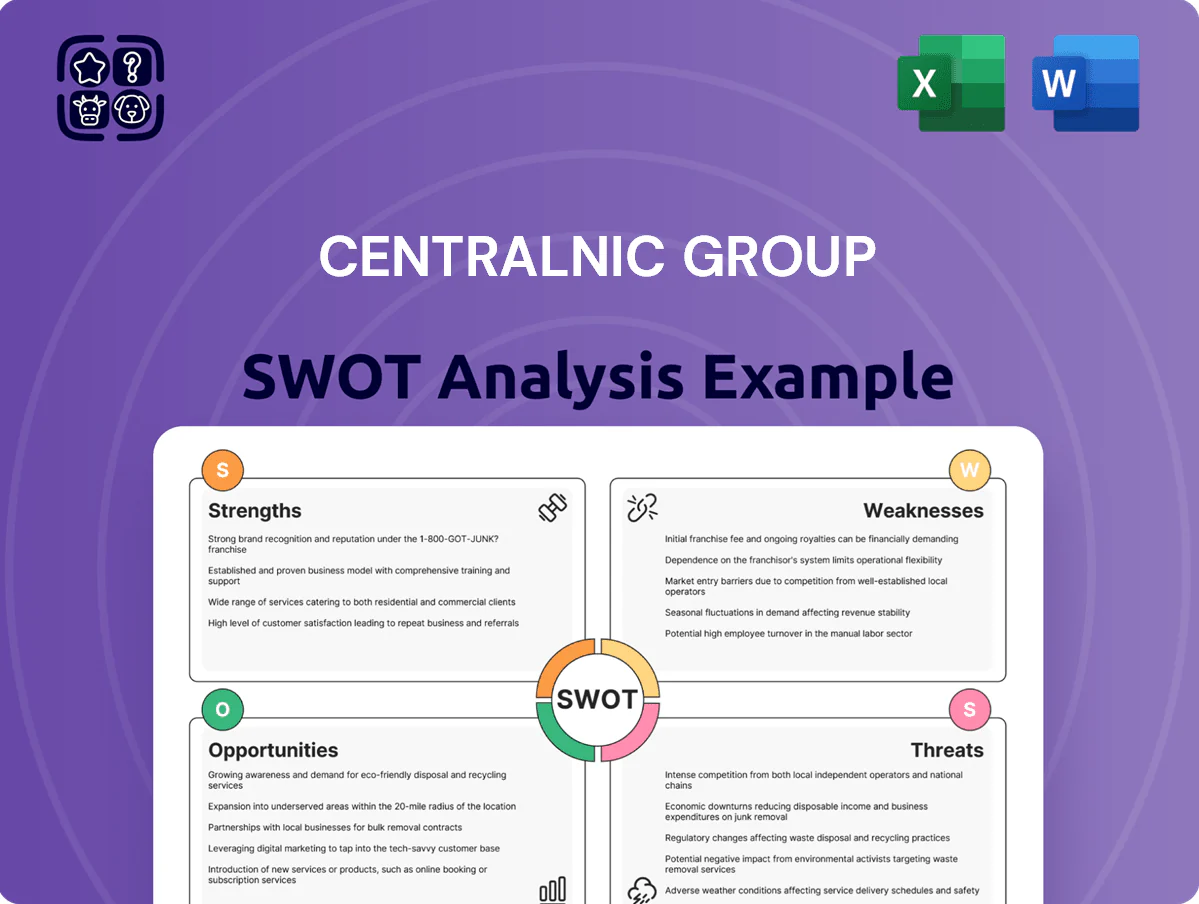

CentralNic Group SWOT Analysis

Your Strategic Toolkit Starts Here

CentralNic Group’s position as a domain and digital services consolidator brings scale and recurring revenue, but faces margin pressure from integration costs and fierce competition in registrars and ad tech; regulatory shifts and domain market cycles pose risks while strategic M&A and platform expansion fuel growth potential. Purchase the full SWOT analysis to access a professionally formatted Word report and editable Excel matrix with actionable tactics and financial context.

Strengths

Robust Recurring Revenue Model

CentralNic Group secures a large share of revenue from subscription-based domain services, giving predictable, recurring cash flow; in FY 2024 recurring revenue was about 68% of total revenue (£202.3m revenue, recurring ~£137.6m). Renewal rates through late 2025 remain strong—industry-average retention ~75–80%—forming a stable base for long-term planning and debt servicing. This steady cash generation lets CentralNic reinvest in high-growth areas like brand services and marketplace expansion without heavy external financing, lowering leverage risk and supporting organic M&A.

Diversified Global Operations

CentralNic Group operates in over 190 countries and reported FY 2024 revenue of $377.2m, with no single country accounting for more than 12% of sales, which spreads geographic risk across multiple continents.

This diversified footprint reduces exposure to local downturns and regional regulatory changes, as seen when EMEA, Americas and APAC each contributed roughly one-third of revenue in 2024.

Balancing revenue across jurisdictions helped CentralNic limit annual volatility to about ±4% in 2022–2024, supporting a more resilient profile against global market swings.

Scalable Proprietary Technology

CentralNic Group runs a scalable proprietary tech stack powering domain registry and online marketing platforms, enabling gross margins above 60% as incremental customer costs remain low versus lifetime revenue (2024 revenue £228.5m, adjusted EBITDA margin ~23% in FY2024). Continuous AI investment through 2025 improved ad-tech yield, boosting programmatic RPMs by an estimated 12% year-over-year and lowering acquisition unit costs.

Strong Market Position in Ad-Tech

CentralNic Group’s online marketing arm is a leader in privacy-safe customer acquisition, generating £170m revenue in FY2024 and growing segment margins above 22% as advertisers shift from tracking to context-based ads.

By prioritizing non-intrusive, context-driven advertising, CentralNic reduced reliance on third-party cookies and maintained traffic quality, delivering a 15% year-on-year increase in advertiser ROI in 2024.

That positioning made CentralNic a preferred partner for compliance-focused advertisers, evidenced by a 28% rise in repeat advertiser spend in 2024 and solidifying market share in programmatic contextual channels.

- £170m revenue FY2024

- 22%+ segment margin

- 15% YoY advertiser ROI gain

- 28% rise in repeat spend

Proven M and A Integration Track Record

CentralNic Group has a proven M and A integration track record, consistently identifying and acquiring complementary businesses that expand technical capabilities and market share; acquisitions since 2019 have been accretive, lifting adjusted EBITDA by about 28% collectively through 2023.

By end-2025 the group refined its integration playbook, routinely extracting cost synergies of ~12–15% within 12 months and reducing time-to-ROI to under 18 months for typical deals.

- Acquisitions since 2019: accretive, +28% adj. EBITDA (through 2023)

- Cost synergies: ~12–15% realized within 12 months

- Time-to-ROI: under 18 months by end-2025

CentralNic: High-margin, recurring revenue and 75–80% renewals fuel global ad-tech growth

CentralNic’s recurring revenue (~£137.6m, 68% of £202.3m FY2024) and ~75–80% renewal rates deliver stable cash flow; diversified presence in 190+ countries (no country >12% sales) limits regional risk; scalable tech yields gross margins >60% and adj. EBITDA margin ~23% (FY2024); ad-tech/contextual ads segment £170m revenue with 22%+ margin and 15% YoY advertiser ROI gain.

| Metric | Value (FY2024) |

|---|---|

| Revenue | £202.3m |

| Recurring revenue | £137.6m (68%) |

| Adj. EBITDA margin | ~23% |

| Contextual ads revenue | £170m |

| Advertiser ROI YoY | +15% |

What is included in the product

Provides a concise SWOT overview of CentralNic Group, outlining its core strengths and weaknesses alongside market opportunities and external threats to inform strategic decision-making.

Provides a concise SWOT matrix for CentralNic Group to speed strategic alignment and clarify domain, acquisition, and market-positioning trade-offs for executives and analysts.

Weaknesses

Reliance on Major Search Partners

A substantial share of CentralNic Group’s FY2024 online marketing revenue—about 62% of the £148m segment—comes from a handful of major search partners, creating concentration risk.

Any adverse change in terms or revenue shares by these dominant search engines could cut segment margins quickly; a 10% rate reduction would lower FY2024 segment revenue by ~£9.2m.

This dependency leaves CentralNic exposed to strategic moves by big tech—algorithm shifts, product integrations, or exclusivity deals—that can disrupt traffic and short-term profitability.

High Levels of Intangible Assets

Following years of aggressive acquisitions, CentralNic Group carried goodwill and intangible assets of 393.5 million GBP on its 2024 balance sheet (FY to Dec 31, 2024), raising real impairment risk if acquired units miss targets.

Large intangibles can trigger material write-downs and volatility in reported equity; investors often discount book value when intangibles exceed ~50% of total assets—CentralNic’s intangibles were ~62% of assets in 2024.

Complex Corporate Structure

Operating across 50+ brands and subsidiaries, CentralNic Group faces internal silos and reporting complexity that can obscure segment-level performance; FY2024 pro forma revenue was $382m, but disaggregated margins vary widely by unit.

Streamlining since 2022 cut overlap, yet multifaceted operations still inflate admin costs—central admin was ~18% of revenue in 2024 versus ~12% for more focused peers—making cost control a persistent weakness.

Vulnerability to Privacy Policy Shifts

The company remains exposed to abrupt browser and OS privacy changes—Apple's ITP and Google’s phased third-party cookie deprecation have already pressured ad revenues industry-wide; CentralNic reported 2024 online marketing revenue decline of 8% YoY, showing this sensitivity.

New tracking or monetization limits could disrupt established margins in the online marketing segment, forcing reallocations that hurt FY profit; adapting needs ongoing R and D spend—CentralNic’s tech and product investment was 6.2% of revenue in 2024.

Keeping pace requires continuous, costly R and D to rebuild context-based capabilities and server-side measurement, raising operating risk and compressing ROIC.

- 2024 online marketing revenue -8% YoY

- R&D spend 6.2% of revenue in 2024

- Risk: sudden browser/OS policy shifts

Moderate Debt Levels from Acquisitions

CentralNic Group's growth-by-acquisition strategy has relied on leverage, leaving net debt at about $162m as of FY2024 (Dec 31, 2024), requiring disciplined capital management.

Operating cash flow covers interest today, but higher global rates (bank base rates ~4–5% in 2024) would raise service costs and compress free cash.

This debt profile constrains near-term dividends and limits room for aggressive bolt-on M&A until leverage falls or cash generation improves.

- Net debt ~$162m (FY2024)

- Interest coverage adequate but rate-sensitive

- Limits short-term dividends and M&A

CentralNic risk alert: 62% partner concentration, large intangibles & interest-sensitive debt

CentralNic’s FY2024 concentration risk: ~62% of £148m online marketing revenue from few search partners; a 10% cut ≈ £9.2m revenue hit. Large intangibles £393.5m (~62% of assets) raise impairment risk and equity volatility. FY2024 online marketing revenue -8% YoY; R&D 6.2% of revenue; net debt ≈ $162m, interest-sensitive at 4–5% rates.

| Metric | 2024 |

|---|---|

| Online marketing revenue concentration | 62% |

| Online marketing rev | £148m |

| Margin shock (10%) | ~£9.2m |

| Intangibles & goodwill | £393.5m (62% assets) |

| Online marketing YoY | -8% |

| R&D | 6.2% rev |

| Net debt | ~$162m |

Same Document Delivered

CentralNic Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats tailored to CentralNic Group.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

CentralNic Group’s position as a domain and digital services consolidator brings scale and recurring revenue, but faces margin pressure from integration costs and fierce competition in registrars and ad tech; regulatory shifts and domain market cycles pose risks while strategic M&A and platform expansion fuel growth potential. Purchase the full SWOT analysis to access a professionally formatted Word report and editable Excel matrix with actionable tactics and financial context.

Strengths

Robust Recurring Revenue Model

CentralNic Group secures a large share of revenue from subscription-based domain services, giving predictable, recurring cash flow; in FY 2024 recurring revenue was about 68% of total revenue (£202.3m revenue, recurring ~£137.6m). Renewal rates through late 2025 remain strong—industry-average retention ~75–80%—forming a stable base for long-term planning and debt servicing. This steady cash generation lets CentralNic reinvest in high-growth areas like brand services and marketplace expansion without heavy external financing, lowering leverage risk and supporting organic M&A.

Diversified Global Operations

CentralNic Group operates in over 190 countries and reported FY 2024 revenue of $377.2m, with no single country accounting for more than 12% of sales, which spreads geographic risk across multiple continents.

This diversified footprint reduces exposure to local downturns and regional regulatory changes, as seen when EMEA, Americas and APAC each contributed roughly one-third of revenue in 2024.

Balancing revenue across jurisdictions helped CentralNic limit annual volatility to about ±4% in 2022–2024, supporting a more resilient profile against global market swings.

Scalable Proprietary Technology

CentralNic Group runs a scalable proprietary tech stack powering domain registry and online marketing platforms, enabling gross margins above 60% as incremental customer costs remain low versus lifetime revenue (2024 revenue £228.5m, adjusted EBITDA margin ~23% in FY2024). Continuous AI investment through 2025 improved ad-tech yield, boosting programmatic RPMs by an estimated 12% year-over-year and lowering acquisition unit costs.

Strong Market Position in Ad-Tech

CentralNic Group’s online marketing arm is a leader in privacy-safe customer acquisition, generating £170m revenue in FY2024 and growing segment margins above 22% as advertisers shift from tracking to context-based ads.

By prioritizing non-intrusive, context-driven advertising, CentralNic reduced reliance on third-party cookies and maintained traffic quality, delivering a 15% year-on-year increase in advertiser ROI in 2024.

That positioning made CentralNic a preferred partner for compliance-focused advertisers, evidenced by a 28% rise in repeat advertiser spend in 2024 and solidifying market share in programmatic contextual channels.

- £170m revenue FY2024

- 22%+ segment margin

- 15% YoY advertiser ROI gain

- 28% rise in repeat spend

Proven M and A Integration Track Record

CentralNic Group has a proven M and A integration track record, consistently identifying and acquiring complementary businesses that expand technical capabilities and market share; acquisitions since 2019 have been accretive, lifting adjusted EBITDA by about 28% collectively through 2023.

By end-2025 the group refined its integration playbook, routinely extracting cost synergies of ~12–15% within 12 months and reducing time-to-ROI to under 18 months for typical deals.

- Acquisitions since 2019: accretive, +28% adj. EBITDA (through 2023)

- Cost synergies: ~12–15% realized within 12 months

- Time-to-ROI: under 18 months by end-2025

CentralNic: High-margin, recurring revenue and 75–80% renewals fuel global ad-tech growth

CentralNic’s recurring revenue (~£137.6m, 68% of £202.3m FY2024) and ~75–80% renewal rates deliver stable cash flow; diversified presence in 190+ countries (no country >12% sales) limits regional risk; scalable tech yields gross margins >60% and adj. EBITDA margin ~23% (FY2024); ad-tech/contextual ads segment £170m revenue with 22%+ margin and 15% YoY advertiser ROI gain.

| Metric | Value (FY2024) |

|---|---|

| Revenue | £202.3m |

| Recurring revenue | £137.6m (68%) |

| Adj. EBITDA margin | ~23% |

| Contextual ads revenue | £170m |

| Advertiser ROI YoY | +15% |

What is included in the product

Provides a concise SWOT overview of CentralNic Group, outlining its core strengths and weaknesses alongside market opportunities and external threats to inform strategic decision-making.

Provides a concise SWOT matrix for CentralNic Group to speed strategic alignment and clarify domain, acquisition, and market-positioning trade-offs for executives and analysts.

Weaknesses

Reliance on Major Search Partners

A substantial share of CentralNic Group’s FY2024 online marketing revenue—about 62% of the £148m segment—comes from a handful of major search partners, creating concentration risk.

Any adverse change in terms or revenue shares by these dominant search engines could cut segment margins quickly; a 10% rate reduction would lower FY2024 segment revenue by ~£9.2m.

This dependency leaves CentralNic exposed to strategic moves by big tech—algorithm shifts, product integrations, or exclusivity deals—that can disrupt traffic and short-term profitability.

High Levels of Intangible Assets

Following years of aggressive acquisitions, CentralNic Group carried goodwill and intangible assets of 393.5 million GBP on its 2024 balance sheet (FY to Dec 31, 2024), raising real impairment risk if acquired units miss targets.

Large intangibles can trigger material write-downs and volatility in reported equity; investors often discount book value when intangibles exceed ~50% of total assets—CentralNic’s intangibles were ~62% of assets in 2024.

Complex Corporate Structure

Operating across 50+ brands and subsidiaries, CentralNic Group faces internal silos and reporting complexity that can obscure segment-level performance; FY2024 pro forma revenue was $382m, but disaggregated margins vary widely by unit.

Streamlining since 2022 cut overlap, yet multifaceted operations still inflate admin costs—central admin was ~18% of revenue in 2024 versus ~12% for more focused peers—making cost control a persistent weakness.

Vulnerability to Privacy Policy Shifts

The company remains exposed to abrupt browser and OS privacy changes—Apple's ITP and Google’s phased third-party cookie deprecation have already pressured ad revenues industry-wide; CentralNic reported 2024 online marketing revenue decline of 8% YoY, showing this sensitivity.

New tracking or monetization limits could disrupt established margins in the online marketing segment, forcing reallocations that hurt FY profit; adapting needs ongoing R and D spend—CentralNic’s tech and product investment was 6.2% of revenue in 2024.

Keeping pace requires continuous, costly R and D to rebuild context-based capabilities and server-side measurement, raising operating risk and compressing ROIC.

- 2024 online marketing revenue -8% YoY

- R&D spend 6.2% of revenue in 2024

- Risk: sudden browser/OS policy shifts

Moderate Debt Levels from Acquisitions

CentralNic Group's growth-by-acquisition strategy has relied on leverage, leaving net debt at about $162m as of FY2024 (Dec 31, 2024), requiring disciplined capital management.

Operating cash flow covers interest today, but higher global rates (bank base rates ~4–5% in 2024) would raise service costs and compress free cash.

This debt profile constrains near-term dividends and limits room for aggressive bolt-on M&A until leverage falls or cash generation improves.

- Net debt ~$162m (FY2024)

- Interest coverage adequate but rate-sensitive

- Limits short-term dividends and M&A

CentralNic risk alert: 62% partner concentration, large intangibles & interest-sensitive debt

CentralNic’s FY2024 concentration risk: ~62% of £148m online marketing revenue from few search partners; a 10% cut ≈ £9.2m revenue hit. Large intangibles £393.5m (~62% of assets) raise impairment risk and equity volatility. FY2024 online marketing revenue -8% YoY; R&D 6.2% of revenue; net debt ≈ $162m, interest-sensitive at 4–5% rates.

| Metric | 2024 |

|---|---|

| Online marketing revenue concentration | 62% |

| Online marketing rev | £148m |

| Margin shock (10%) | ~£9.2m |

| Intangibles & goodwill | £393.5m (62% assets) |

| Online marketing YoY | -8% |

| R&D | 6.2% rev |

| Net debt | ~$162m |

Same Document Delivered

CentralNic Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats tailored to CentralNic Group.