Centrica Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Centrica faces intense buyer power, regulated pricing pressures, and rising threats from renewables and agile challengers, while supplier leverage and capital intensity temper margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Centrica’s competitive dynamics, market pressures, and strategic advantages in detail.

Get the complete, consultant-grade report—force ratings, visuals, and actionable implications—ready for presentations and investment decisions.

Suppliers Bargaining Power

Wholesale Energy Market Volatility

The global natural gas and power markets remain Centrica’s chief supplier risk; UK wholesale gas spiked to ~220 p/therm in Aug 2022 and, while easing, averaged ~70 p/therm in 2024, directly raising Centrica’s cost base.

Centrica has diversified into UK retail, services, and upstream gas but still purchases on international markets where geopolitical shocks—eg Russia-Ukraine and 2023 LNG tightness—set prices.

Hedging programs (covering a multi-year portion of volumes) reduce volatility exposure, yet Centrica is effectively a price taker when global supply-demand swings move margins and cash flow.

Transition to Renewable PPA Providers

As Centrica shifts to net-zero, reliance on third-party renewable developers via PPAs rose—Centrica had committed to 1.2 GW of low‑carbon contracts by end‑2024—giving suppliers leverage as UK/Ireland corporate demand exceeds ~8 GW of announced capacity; tight supply pushes upwards pressure on prices and contract terms. Long tenors (10–15 years) force Centrica to lock favorable rates early to protect retail margins and customer pricing.

Specialized Green Technology Labor

The shift to home energy services like heat pumps and EV chargers needs highly skilled, certified engineers, and the UK faces a shortage—BEIS reported a 2024 gap of ~78,000 low-carbon heat installers needed by 2035 to meet targets. This scarcity boosts bargaining power of specialized labor and training providers, pushing Centrica's service costs and lead times up; median installer pay rose ~12% in 2023. Higher training fees and retention spend increase unit service costs and delay rollout timelines.

Digital Infrastructure and Software Vendors

Centrica depends on cloud and AI platforms to run grid flexibility and customer data; AWS reported 2024 revenue of $88.9bn and Salesforce $36.3bn, so supplier clout is moderate given high migration costs and integration time.

These vendors enable Centrica’s smart-home services and automated billing; a failed migration could cost millions and disrupt 7.9m UK customer accounts.

- High switching costs — multi-year integrations

- Moderate supplier power — few large providers

- Critical for smart-home, billing, grid ops

Regulatory Infrastructure and Network Operators

The physical delivery of gas and electricity is controlled by monopoly transmission and distribution operators (eg, National Grid ESO, UK Distribution Network Operators), so Centrica must use these networks and pay regulated charges set by Ofgem and the government.

These non-negotiable transmission and distribution charges accounted for about 30–40% of a UK household energy bill in 2024, making them a significant cost component Centrica cannot avoid.

- Monopoly network owners: National Grid, regional DNOs

- Charges set by: Ofgem / government

- 2024 share of household bill: ~30–40%

- Costs non-negotiable; high supplier bargaining pressure

Suppliers wield rising power: gas, networks, PPAs and cloud vendors tighten Centrica’s margins

Suppliers hold moderate–high power: global gas prices (avg ~70 p/therm in 2024 after 220 p/therm peak Aug 2022) and network charges (30–40% of UK bill in 2024) limit Centrica’s pricing flexibility; 1.2 GW PPAs by end‑2024 and 78,000 installer shortfall to 2035 raise supplier leverage in low‑carbon inputs; cloud vendors (AWS $88.9bn, Salesforce $36.3bn 2024) add switching costs.

| Metric | 2024/Note |

|---|---|

| UK gas price | ~70 p/therm |

| Network share | 30–40% |

| PPAs committed | 1.2 GW |

| Installer gap | ~78,000 by 2035 |

What is included in the product

Tailored exclusively for Centrica, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its market position and profitability.

A concise Porter's Five Forces snapshot for Centrica—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Low Switching Costs in Retail Markets

Domestic energy customers in the UK and Ireland can switch providers easily due to government rules that simplified switching; Ofgem reported 4.7m domestic supplier switches in GB in 2023, up 18% from 2022, showing active churn. Digital comparison sites and automated switching services (e.g., Ofgem Enduring Framework tools) let consumers chase lower prices or better service anytime, raising price sensitivity. This forces Centrica to keep innovating in pricing, customer experience, and bundled services to retain customers and limit margin erosion; Centrica reported a 2024 churn rate around industry average of ~12% in household markets.

Impact of Regulatory Price Caps

The Ofgem price cap limits Centrica’s ability to pass wholesale cost rises to ~9 million standard variable tariff customers, capping typical unit margins and restraining retail revenue growth; in 2024 UK cap averages (about £1,923/year for typical dual-fuel households in Oct 2024) directly compressed Centrica’s retail margin and contributed to a 2024 UK customer margin decline; so Centrica must cut costs and shift to fixed-price and services to protect EBITDA.

High Sensitivity to Cost of Living

Ongoing cost-of-living pressures have made energy a top household expense, with UK household energy bills up ~65% from 2019 to 2023, driving acute price sensitivity and churn risk for Centrica.

Consumers defect to leaner suppliers if they spot weak value; Ofgem data show smaller suppliers gained ~7% market share in 2023 as price competition intensified.

British Gas faces extra scrutiny—public expectations for affordability are higher, so even small price deviations versus the market average raise cancellation likelihood.

Demand for Sustainable and Transparent Options

Modern consumers increasingly demand green tariffs and clear carbon reporting; Ofgem reported in 2024 that 28% of UK customers consider supplier sustainability a key switching factor, pressuring Centrica to speed decarbonization.

Failure to meet these expectations risks share loss to niche green suppliers: Octopus Energy grew UK retail market share to ~11% by 2025, showing customer willingness to switch.

Investors and corporates also push transparency—Centrica disclosed Scope 1–3 targets in 2024, but faster action may be needed to retain customers.

- 28% of UK customers cite sustainability as switching factor (Ofgem 2024)

- Octopus ~11% UK market share by 2025

- Centrica published Scope 1–3 targets in 2024

Commercial and Industrial Negotiation Power

Large commercial and industrial customers negotiate bespoke contracts and SLAs, running tenders that force Centrica to compete on price, flexibility and services such as onsite generation; in 2024 corporate energy contracts accounted for roughly 18% of Centrica’s UK B2B revenue, so losing a major account can dent margins and cash flow materially.

- Major C&I clients demand bespoke SLAs

- Tenders push aggressive pricing and value-adds

- Onsite generation and flexibility win deals

- ~18% of UK B2B revenue (2024) at risk from single-account loss

Switching Surge, Price Cap Pain: Centrica Faces Churn, Cost Cuts & Sustainability Threat

High switching (4.7m switches GB, 2023) and price sensitivity (bills +65% 2019–23) give customers strong bargaining power; Ofgem price cap (≈£1,923/yr Oct 2024) limits margin pass-through, pushing Centrica to cut costs, sell fixed contracts and services; sustainability matters (28% cite it, Ofgem 2024) as Octopus hit ~11% share by 2025; ~18% of UK B2B revenue (2024) is at risk from churn.

| Metric | Value |

|---|---|

| GB switches (2023) | 4.7m |

| Price cap Oct 2024 | £1,923/yr |

| Household bill change 2019–23 | +65% |

| Sustainability switching (2024) | 28% |

| Octopus UK share (2025) | ~11% |

| UK B2B revenue at risk (2024) | ~18% |

What You See Is What You Get

Centrica Porter's Five Forces Analysis

This preview shows the exact Centrica Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; the full document is fully formatted and ready to use.

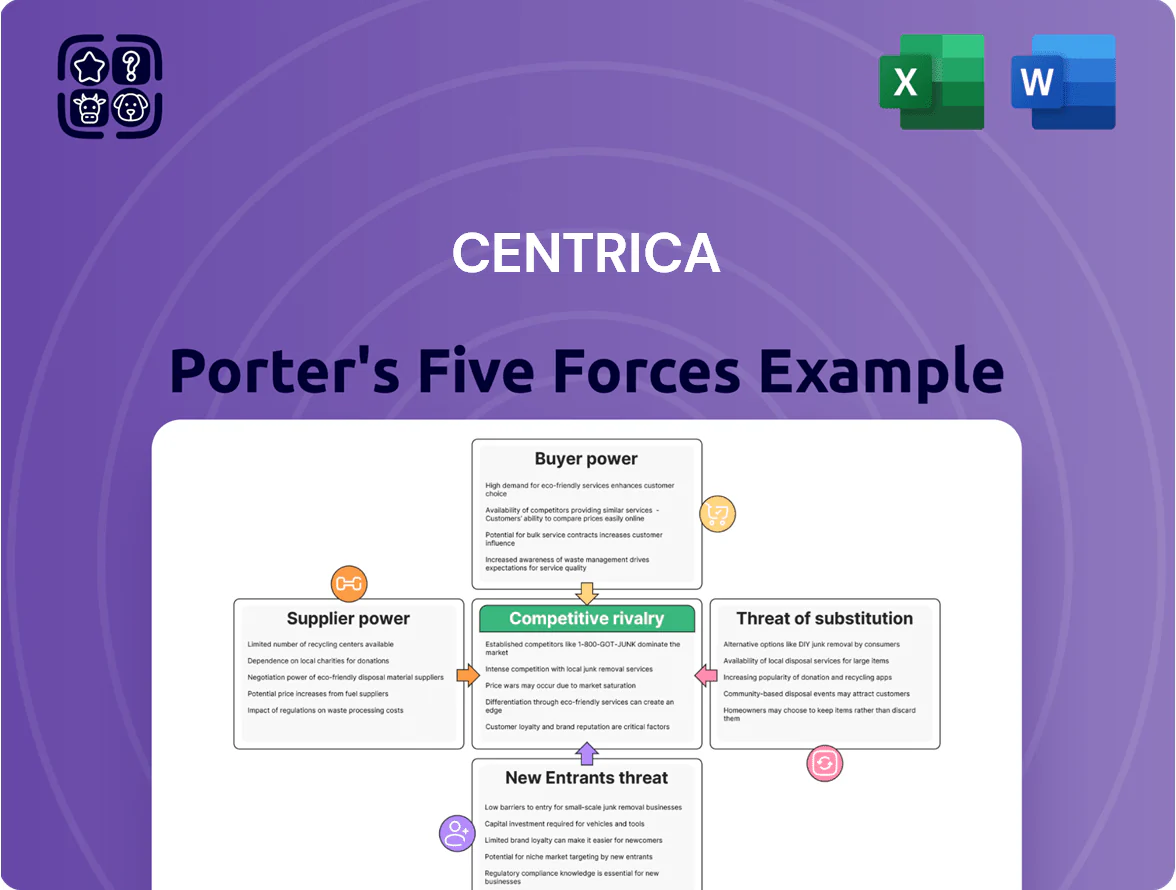

It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and data-driven conclusions for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Centrica faces intense buyer power, regulated pricing pressures, and rising threats from renewables and agile challengers, while supplier leverage and capital intensity temper margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Centrica’s competitive dynamics, market pressures, and strategic advantages in detail.

Get the complete, consultant-grade report—force ratings, visuals, and actionable implications—ready for presentations and investment decisions.

Suppliers Bargaining Power

Wholesale Energy Market Volatility

The global natural gas and power markets remain Centrica’s chief supplier risk; UK wholesale gas spiked to ~220 p/therm in Aug 2022 and, while easing, averaged ~70 p/therm in 2024, directly raising Centrica’s cost base.

Centrica has diversified into UK retail, services, and upstream gas but still purchases on international markets where geopolitical shocks—eg Russia-Ukraine and 2023 LNG tightness—set prices.

Hedging programs (covering a multi-year portion of volumes) reduce volatility exposure, yet Centrica is effectively a price taker when global supply-demand swings move margins and cash flow.

Transition to Renewable PPA Providers

As Centrica shifts to net-zero, reliance on third-party renewable developers via PPAs rose—Centrica had committed to 1.2 GW of low‑carbon contracts by end‑2024—giving suppliers leverage as UK/Ireland corporate demand exceeds ~8 GW of announced capacity; tight supply pushes upwards pressure on prices and contract terms. Long tenors (10–15 years) force Centrica to lock favorable rates early to protect retail margins and customer pricing.

Specialized Green Technology Labor

The shift to home energy services like heat pumps and EV chargers needs highly skilled, certified engineers, and the UK faces a shortage—BEIS reported a 2024 gap of ~78,000 low-carbon heat installers needed by 2035 to meet targets. This scarcity boosts bargaining power of specialized labor and training providers, pushing Centrica's service costs and lead times up; median installer pay rose ~12% in 2023. Higher training fees and retention spend increase unit service costs and delay rollout timelines.

Digital Infrastructure and Software Vendors

Centrica depends on cloud and AI platforms to run grid flexibility and customer data; AWS reported 2024 revenue of $88.9bn and Salesforce $36.3bn, so supplier clout is moderate given high migration costs and integration time.

These vendors enable Centrica’s smart-home services and automated billing; a failed migration could cost millions and disrupt 7.9m UK customer accounts.

- High switching costs — multi-year integrations

- Moderate supplier power — few large providers

- Critical for smart-home, billing, grid ops

Regulatory Infrastructure and Network Operators

The physical delivery of gas and electricity is controlled by monopoly transmission and distribution operators (eg, National Grid ESO, UK Distribution Network Operators), so Centrica must use these networks and pay regulated charges set by Ofgem and the government.

These non-negotiable transmission and distribution charges accounted for about 30–40% of a UK household energy bill in 2024, making them a significant cost component Centrica cannot avoid.

- Monopoly network owners: National Grid, regional DNOs

- Charges set by: Ofgem / government

- 2024 share of household bill: ~30–40%

- Costs non-negotiable; high supplier bargaining pressure

Suppliers wield rising power: gas, networks, PPAs and cloud vendors tighten Centrica’s margins

Suppliers hold moderate–high power: global gas prices (avg ~70 p/therm in 2024 after 220 p/therm peak Aug 2022) and network charges (30–40% of UK bill in 2024) limit Centrica’s pricing flexibility; 1.2 GW PPAs by end‑2024 and 78,000 installer shortfall to 2035 raise supplier leverage in low‑carbon inputs; cloud vendors (AWS $88.9bn, Salesforce $36.3bn 2024) add switching costs.

| Metric | 2024/Note |

|---|---|

| UK gas price | ~70 p/therm |

| Network share | 30–40% |

| PPAs committed | 1.2 GW |

| Installer gap | ~78,000 by 2035 |

What is included in the product

Tailored exclusively for Centrica, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its market position and profitability.

A concise Porter's Five Forces snapshot for Centrica—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Low Switching Costs in Retail Markets

Domestic energy customers in the UK and Ireland can switch providers easily due to government rules that simplified switching; Ofgem reported 4.7m domestic supplier switches in GB in 2023, up 18% from 2022, showing active churn. Digital comparison sites and automated switching services (e.g., Ofgem Enduring Framework tools) let consumers chase lower prices or better service anytime, raising price sensitivity. This forces Centrica to keep innovating in pricing, customer experience, and bundled services to retain customers and limit margin erosion; Centrica reported a 2024 churn rate around industry average of ~12% in household markets.

Impact of Regulatory Price Caps

The Ofgem price cap limits Centrica’s ability to pass wholesale cost rises to ~9 million standard variable tariff customers, capping typical unit margins and restraining retail revenue growth; in 2024 UK cap averages (about £1,923/year for typical dual-fuel households in Oct 2024) directly compressed Centrica’s retail margin and contributed to a 2024 UK customer margin decline; so Centrica must cut costs and shift to fixed-price and services to protect EBITDA.

High Sensitivity to Cost of Living

Ongoing cost-of-living pressures have made energy a top household expense, with UK household energy bills up ~65% from 2019 to 2023, driving acute price sensitivity and churn risk for Centrica.

Consumers defect to leaner suppliers if they spot weak value; Ofgem data show smaller suppliers gained ~7% market share in 2023 as price competition intensified.

British Gas faces extra scrutiny—public expectations for affordability are higher, so even small price deviations versus the market average raise cancellation likelihood.

Demand for Sustainable and Transparent Options

Modern consumers increasingly demand green tariffs and clear carbon reporting; Ofgem reported in 2024 that 28% of UK customers consider supplier sustainability a key switching factor, pressuring Centrica to speed decarbonization.

Failure to meet these expectations risks share loss to niche green suppliers: Octopus Energy grew UK retail market share to ~11% by 2025, showing customer willingness to switch.

Investors and corporates also push transparency—Centrica disclosed Scope 1–3 targets in 2024, but faster action may be needed to retain customers.

- 28% of UK customers cite sustainability as switching factor (Ofgem 2024)

- Octopus ~11% UK market share by 2025

- Centrica published Scope 1–3 targets in 2024

Commercial and Industrial Negotiation Power

Large commercial and industrial customers negotiate bespoke contracts and SLAs, running tenders that force Centrica to compete on price, flexibility and services such as onsite generation; in 2024 corporate energy contracts accounted for roughly 18% of Centrica’s UK B2B revenue, so losing a major account can dent margins and cash flow materially.

- Major C&I clients demand bespoke SLAs

- Tenders push aggressive pricing and value-adds

- Onsite generation and flexibility win deals

- ~18% of UK B2B revenue (2024) at risk from single-account loss

Switching Surge, Price Cap Pain: Centrica Faces Churn, Cost Cuts & Sustainability Threat

High switching (4.7m switches GB, 2023) and price sensitivity (bills +65% 2019–23) give customers strong bargaining power; Ofgem price cap (≈£1,923/yr Oct 2024) limits margin pass-through, pushing Centrica to cut costs, sell fixed contracts and services; sustainability matters (28% cite it, Ofgem 2024) as Octopus hit ~11% share by 2025; ~18% of UK B2B revenue (2024) is at risk from churn.

| Metric | Value |

|---|---|

| GB switches (2023) | 4.7m |

| Price cap Oct 2024 | £1,923/yr |

| Household bill change 2019–23 | +65% |

| Sustainability switching (2024) | 28% |

| Octopus UK share (2025) | ~11% |

| UK B2B revenue at risk (2024) | ~18% |

What You See Is What You Get

Centrica Porter's Five Forces Analysis

This preview shows the exact Centrica Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; the full document is fully formatted and ready to use.

It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and data-driven conclusions for strategic decision-making.