Century Aluminum Boston Consulting Group Matrix

See the Bigger Picture

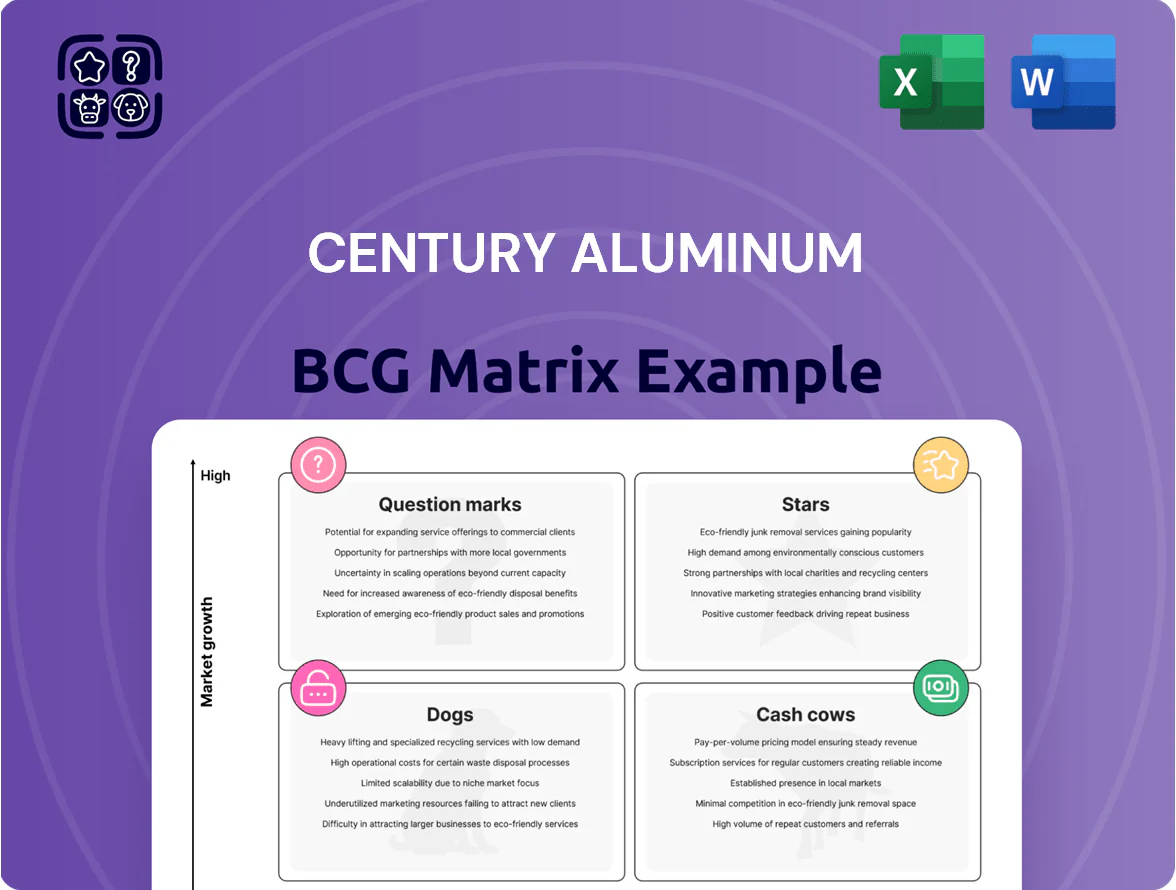

Century Aluminum’s BCG Matrix preview highlights how its product lines and smelting assets map across growth and market-share dynamics amid energy costs and raw-aluminum demand shifts; expect mixes of Cash Cows in legacy contracts and Question Marks where capacity and cost curves are under pressure. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Green Aluminum Natur-Al

Natur-Al, Century Aluminum’s Iceland-made green aluminum produced with 100% renewable energy, is the company’s primary growth engine as of late 2025, showing 28% year-over-year volume growth through Q3 2025. The segment rides a high-growth market: low-carbon aluminum demand is forecast to grow ~12% CAGR through 2028 due to automotive and packaging ESG mandates. With a completed 150,000-ton supply deal in Jan 2026, Natur-Al now holds a leading share of the premium low-carbon aluminum niche and contributed an estimated $220 million in incremental revenue in 2025.

Automotive Billet and Value-Added Products

Century Aluminum shifted toward high-margin value-added billet for automotive lightweighting; by end-2025 billet demand was tight and sold at premiums ~18–25% above LME alloy prices, supporting U.S. share leadership.

Management forecasts billet-driven EBITDA uplift of $30 million in 2026, reflecting high growth and market share in the domestic automotive supply chain; billet margins outpaced standard upstream alumina smelter margins.

U.S. Domestic Primary Aluminum Production

Century Aluminum is the largest U.S. primary aluminum producer, holding roughly 35–40% of domestic capacity in 2025 as the market faces a structural supply deficit of about 1.2 million metric tons annually.

Mid-2025 imposition of 50% Section 232 tariffs created a protective moat, lifting domestic premiums ~USD 300–400/ton and enabling Century to capture sustained high market share.

Federal initiatives like the 2024 CHIPS+ and 2025 DOE manufacturing grants, plus procurement preferences, support domestic supply growth and reduce import reliance, reinforcing Century’s star status.

Icelandic Smelting Operations (Grundartangi)

Grundartangi (Iceland) is a Star: high-growth, high-share thanks to low cash costs (~$1,400/ton in 2025) and near-zero grid emissions from geothermal and hydro, selling premium low-carbon aluminum into Europe.

Late-2025 equipment failures caused ~12% downtime but production and contracts stayed intact, keeping market leadership in sustainable aluminum supply.

- Low cash cost ~$1,400/ton (2025)

- Near-zero grid emissions, premium pricing +5–10%

- 12% downtime late-2025, quick restart

- Long-term advantage as EU carbon pricing rises

Midwest Premium Pricing Power

Century Aluminum captured Midwest Premium pricing, which surged to record highs in 2025, creating a high-growth revenue stream for the company.

As a primary U.S. supplier, Century leveraged ~30–35% regional market share to benefit from Midwest Premium spikes above $1,500/mt by Q4 2025, boosting U.S. unit margins vs. global peers.

The premium-driven mechanism delivered outsized returns after accounting for lower U.S. logistics and no import tariffs, widening EBITDA margins in 2025.

- Midwest Premium > $1,500/mt by late 2025

- Century regional share ~30–35%

- Higher U.S. unit margins vs. global rivals

- EBITDA margin uplift in 2025

Grundartangi shines: $1.4k/ton cash cost, Natur‑Al +28% and $220M revenue lift

Grundartangi (Iceland) is a Star: 2025 low cash cost ~$1,400/ton, near-zero grid emissions, Natur-Al grew 28% YoY through Q3 2025, added ~$220M incremental 2025 revenue, billet premiums +18–25%, Midwest Premium >$1,500/mt by Q4 2025, Century U.S. share ~35–40%, Section 232 tariffs lifted domestic premiums ~$300–400/ton.

| Metric | 2025 Value |

|---|---|

| Natur-Al YoY volume growth | 28% |

| Incremental revenue | $220M |

| Grundartangi cash cost | $1,400/ton |

| Billet premium | 18–25% |

| Midwest Premium | >$1,500/mt |

| US market share | 35–40% |

| Section 232 uplift | $300–400/ton |

What is included in the product

Company-level BCG Matrix mapping Century Aluminum’s products into Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page Century Aluminum BCG Matrix placing each business unit in a quadrant for quick strategic decisions.

Cash Cows

Standard Grade Primary Aluminum Ingots

Standard grade primary aluminum ingots remain Century Aluminum’s core cash generator, accounting for roughly 70% of 2024 smelter shipments and about $1.1 billion of consolidated sales in 2024, in a mature global market with ~2% annual demand growth.

Growth is low versus value-added alloys, but established plants keep unit cash costs near $1,900/ton in 2024, enabling high-volume production with minimal capex.

These steady cash flows funded the Oklahoma smelter restart capex (~$120 million in 2024) and underwrite R&D and downstream trials.

Sebree Smelter Operations

Sebree Smelter Operations in Kentucky is a reliable Cash Cow for Century Aluminum, with ~220,000 metric tonnes annual capacity and contributing roughly 25–30% of company shipments in 2024–2025. By end-2025 Sebree ran with optimized cost structure thanks to long-term power contracts and stable industrial customers, lowering unit cash costs to the mid-$1,700s/ton. Cash flows from Sebree primarily service corporate debt and keep liquidity buffers intact.

Mt. Holly Established Capacity

The Mt. Holly smelter in South Carolina runs as a Cash Cow, producing about 220 ktpa (thousand tonnes per annum) of primary aluminum for the U.S. market and delivering steady EBITDA margins near 18% in 2024.

With a power contract locked through 2031 and industry-scale electrolysis barriers, the site faces low competitive threat and supports predictable cash flow.

Those stable margins funded Century Aluminum’s corporate SG&A and R&D, covering roughly $120–140 million of annual overhead in 2024.

Bauxite and Alumina Supply via Jamalco

Century Aluminum’s majority stake in Jamalco secures about 60% of its alumina needs, cutting spot-market exposure and lowering feedstock costs by an estimated $70–90/ton versus third-party purchases in 2024.

Backward integration into bauxite mining and refining functions as a Cash Cow: steady cashflow, low reinvestment needs (capital intensity ~5–7% of segment EBITDA in 2024) and protection from alumina price swings.

Industry maturity means limited growth capex but high strategic value—Jamalco provided roughly $120–150 million in attributable EBITDA to Century in 2024 (company disclosure estimates).

- Majority ownership → ~60% internal alumina supply

- Estimated cost advantage $70–90/ton (2024)

- Low growth capex ~5–7% of segment EBITDA (2024)

- Attributable EBITDA ~ $120–150M (2024)

Long-term Hedging and Derivative Contracts

Century Aluminum’s long-term hedging of LME (London Metal Exchange) prices and power costs stabilizes cash flows, acting as a Cash Cow by reducing revenue volatility and supporting dividend capacity.

As of Q4 2025 the company reports hedges covering about 60% of expected 2026 primary aluminum volumes and ~70% of 2026 power exposure, creating a predictable income stream for capex and payouts.

Locking prices during 2023–2025 peaks let Century run through cyclical troughs with maintained operations and reduced cash-flow stress.

- Hedges cover ~60% of 2026 metal volumes

- ~70% of 2026 energy exposure hedged

- Supports dividend and $150–200M annual capex range

- Reduces EBITDA volatility by an estimated 25%

Century Aluminum: Cash-Cow Assets, Strong Hedges Fueling Stable EBITDA & Growth

Century Aluminum’s cash cows: standard primary ingots (~70% shipments, $1.1B sales 2024), Sebree (~220ktpa, mid-$1,700s/ton cash cost), Mt. Holly (~220ktpa, ~18% EBITDA 2024), Jamalco alumina (~60% supply, $120–150M EBITDA 2024; $70–90/ton cost advantage), and hedges (≈60% metal, 70% power for 2026) sustaining $120–140M SG&A and $150–200M annual capex.

| Asset | 2024–25 |

|---|---|

| Primary ingots | 70% shipments; $1.1B |

| Sebree | 220ktpa; mid-$1,700s/ton |

| Mt. Holly | 220ktpa; 18% EBITDA |

| Jamalco | 60% supply; $120–150M EBITDA |

| Hedges | 60% metal; 70% power |

Delivered as Shown

Century Aluminum BCG Matrix

The Century Aluminum BCG Matrix you're previewing on this page is the exact, final document you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report tailored for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Century Aluminum’s BCG Matrix preview highlights how its product lines and smelting assets map across growth and market-share dynamics amid energy costs and raw-aluminum demand shifts; expect mixes of Cash Cows in legacy contracts and Question Marks where capacity and cost curves are under pressure. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Green Aluminum Natur-Al

Natur-Al, Century Aluminum’s Iceland-made green aluminum produced with 100% renewable energy, is the company’s primary growth engine as of late 2025, showing 28% year-over-year volume growth through Q3 2025. The segment rides a high-growth market: low-carbon aluminum demand is forecast to grow ~12% CAGR through 2028 due to automotive and packaging ESG mandates. With a completed 150,000-ton supply deal in Jan 2026, Natur-Al now holds a leading share of the premium low-carbon aluminum niche and contributed an estimated $220 million in incremental revenue in 2025.

Automotive Billet and Value-Added Products

Century Aluminum shifted toward high-margin value-added billet for automotive lightweighting; by end-2025 billet demand was tight and sold at premiums ~18–25% above LME alloy prices, supporting U.S. share leadership.

Management forecasts billet-driven EBITDA uplift of $30 million in 2026, reflecting high growth and market share in the domestic automotive supply chain; billet margins outpaced standard upstream alumina smelter margins.

U.S. Domestic Primary Aluminum Production

Century Aluminum is the largest U.S. primary aluminum producer, holding roughly 35–40% of domestic capacity in 2025 as the market faces a structural supply deficit of about 1.2 million metric tons annually.

Mid-2025 imposition of 50% Section 232 tariffs created a protective moat, lifting domestic premiums ~USD 300–400/ton and enabling Century to capture sustained high market share.

Federal initiatives like the 2024 CHIPS+ and 2025 DOE manufacturing grants, plus procurement preferences, support domestic supply growth and reduce import reliance, reinforcing Century’s star status.

Icelandic Smelting Operations (Grundartangi)

Grundartangi (Iceland) is a Star: high-growth, high-share thanks to low cash costs (~$1,400/ton in 2025) and near-zero grid emissions from geothermal and hydro, selling premium low-carbon aluminum into Europe.

Late-2025 equipment failures caused ~12% downtime but production and contracts stayed intact, keeping market leadership in sustainable aluminum supply.

- Low cash cost ~$1,400/ton (2025)

- Near-zero grid emissions, premium pricing +5–10%

- 12% downtime late-2025, quick restart

- Long-term advantage as EU carbon pricing rises

Midwest Premium Pricing Power

Century Aluminum captured Midwest Premium pricing, which surged to record highs in 2025, creating a high-growth revenue stream for the company.

As a primary U.S. supplier, Century leveraged ~30–35% regional market share to benefit from Midwest Premium spikes above $1,500/mt by Q4 2025, boosting U.S. unit margins vs. global peers.

The premium-driven mechanism delivered outsized returns after accounting for lower U.S. logistics and no import tariffs, widening EBITDA margins in 2025.

- Midwest Premium > $1,500/mt by late 2025

- Century regional share ~30–35%

- Higher U.S. unit margins vs. global rivals

- EBITDA margin uplift in 2025

Grundartangi shines: $1.4k/ton cash cost, Natur‑Al +28% and $220M revenue lift

Grundartangi (Iceland) is a Star: 2025 low cash cost ~$1,400/ton, near-zero grid emissions, Natur-Al grew 28% YoY through Q3 2025, added ~$220M incremental 2025 revenue, billet premiums +18–25%, Midwest Premium >$1,500/mt by Q4 2025, Century U.S. share ~35–40%, Section 232 tariffs lifted domestic premiums ~$300–400/ton.

| Metric | 2025 Value |

|---|---|

| Natur-Al YoY volume growth | 28% |

| Incremental revenue | $220M |

| Grundartangi cash cost | $1,400/ton |

| Billet premium | 18–25% |

| Midwest Premium | >$1,500/mt |

| US market share | 35–40% |

| Section 232 uplift | $300–400/ton |

What is included in the product

Company-level BCG Matrix mapping Century Aluminum’s products into Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page Century Aluminum BCG Matrix placing each business unit in a quadrant for quick strategic decisions.

Cash Cows

Standard Grade Primary Aluminum Ingots

Standard grade primary aluminum ingots remain Century Aluminum’s core cash generator, accounting for roughly 70% of 2024 smelter shipments and about $1.1 billion of consolidated sales in 2024, in a mature global market with ~2% annual demand growth.

Growth is low versus value-added alloys, but established plants keep unit cash costs near $1,900/ton in 2024, enabling high-volume production with minimal capex.

These steady cash flows funded the Oklahoma smelter restart capex (~$120 million in 2024) and underwrite R&D and downstream trials.

Sebree Smelter Operations

Sebree Smelter Operations in Kentucky is a reliable Cash Cow for Century Aluminum, with ~220,000 metric tonnes annual capacity and contributing roughly 25–30% of company shipments in 2024–2025. By end-2025 Sebree ran with optimized cost structure thanks to long-term power contracts and stable industrial customers, lowering unit cash costs to the mid-$1,700s/ton. Cash flows from Sebree primarily service corporate debt and keep liquidity buffers intact.

Mt. Holly Established Capacity

The Mt. Holly smelter in South Carolina runs as a Cash Cow, producing about 220 ktpa (thousand tonnes per annum) of primary aluminum for the U.S. market and delivering steady EBITDA margins near 18% in 2024.

With a power contract locked through 2031 and industry-scale electrolysis barriers, the site faces low competitive threat and supports predictable cash flow.

Those stable margins funded Century Aluminum’s corporate SG&A and R&D, covering roughly $120–140 million of annual overhead in 2024.

Bauxite and Alumina Supply via Jamalco

Century Aluminum’s majority stake in Jamalco secures about 60% of its alumina needs, cutting spot-market exposure and lowering feedstock costs by an estimated $70–90/ton versus third-party purchases in 2024.

Backward integration into bauxite mining and refining functions as a Cash Cow: steady cashflow, low reinvestment needs (capital intensity ~5–7% of segment EBITDA in 2024) and protection from alumina price swings.

Industry maturity means limited growth capex but high strategic value—Jamalco provided roughly $120–150 million in attributable EBITDA to Century in 2024 (company disclosure estimates).

- Majority ownership → ~60% internal alumina supply

- Estimated cost advantage $70–90/ton (2024)

- Low growth capex ~5–7% of segment EBITDA (2024)

- Attributable EBITDA ~ $120–150M (2024)

Long-term Hedging and Derivative Contracts

Century Aluminum’s long-term hedging of LME (London Metal Exchange) prices and power costs stabilizes cash flows, acting as a Cash Cow by reducing revenue volatility and supporting dividend capacity.

As of Q4 2025 the company reports hedges covering about 60% of expected 2026 primary aluminum volumes and ~70% of 2026 power exposure, creating a predictable income stream for capex and payouts.

Locking prices during 2023–2025 peaks let Century run through cyclical troughs with maintained operations and reduced cash-flow stress.

- Hedges cover ~60% of 2026 metal volumes

- ~70% of 2026 energy exposure hedged

- Supports dividend and $150–200M annual capex range

- Reduces EBITDA volatility by an estimated 25%

Century Aluminum: Cash-Cow Assets, Strong Hedges Fueling Stable EBITDA & Growth

Century Aluminum’s cash cows: standard primary ingots (~70% shipments, $1.1B sales 2024), Sebree (~220ktpa, mid-$1,700s/ton cash cost), Mt. Holly (~220ktpa, ~18% EBITDA 2024), Jamalco alumina (~60% supply, $120–150M EBITDA 2024; $70–90/ton cost advantage), and hedges (≈60% metal, 70% power for 2026) sustaining $120–140M SG&A and $150–200M annual capex.

| Asset | 2024–25 |

|---|---|

| Primary ingots | 70% shipments; $1.1B |

| Sebree | 220ktpa; mid-$1,700s/ton |

| Mt. Holly | 220ktpa; 18% EBITDA |

| Jamalco | 60% supply; $120–150M EBITDA |

| Hedges | 60% metal; 70% power |

Delivered as Shown

Century Aluminum BCG Matrix

The Century Aluminum BCG Matrix you're previewing on this page is the exact, final document you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report tailored for strategic decision-making.