Century Aluminum Business Model Canvas

Century Aluminum Business Model Canvas: Downloadable Blueprint for Investors & Innovators

Unlock Century Aluminum’s strategic playbook with a concise Business Model Canvas that maps value propositions, revenue streams, key partners, and cost drivers—perfect for investors, consultants, and entrepreneurs seeking actionable industry insight; download the full Word/Excel canvas to benchmark, plan, and apply these proven strategies to your own projects.

Partnerships

Strategic Alumina Supply Agreements

Century Aluminum depends on long-term alumina supply contracts—notably with Glencore—to secure ~70% of its feedstock, cutting exposure to spot-price swings and keeping smelters near 85–90% capacity utilization. By 2025, amid geopolitical supply risks, these agreements underpin operational stability and helped limit input-cost spikes that pushed alumina index prices up ~30% YoY in 2024.

Energy Utility and Grid Providers

Century Aluminum relies on long-term power purchase agreements with utilities such as Santee Cooper (US) and Landsvirkjun (Iceland); these deals, often with renewable shares, lock in prices that drive regional margins—electricity can be >30% of smelter cash costs. In 2024 Century reported energy costs ~25–35% of site COGS and a 10–15% EBITDA swing per $10/MWh change in power price.

Department of Energy and Government Agencies

Logistics and Maritime Shipping Partners

Century Aluminum contracts global shipping lines and US rail carriers to move alumina inbound and finished aluminum outbound, cutting landed cost—Iceland plants shipped ~180 kt of primary aluminum to Europe in 2024, where logistics added an estimated $150–$250/ton to landed cost.

These partners handle bulk cross-border transit and deep-water port operations, reducing delays and demurrage that can swing margins by several dollars per ton.

- ~180 kt Iceland shipments (2024)

- Logistics adds ~$150–$250/ton

- Rail + ocean needed for inland US customers

Financial Institutions and Hedging Partners

Century Aluminum partners with major investment banks and commodity brokers to hedge LME (London Metal Exchange) price swings; in 2024 hedging activity helped limit realized aluminum price variance to ±6% versus spot volatility over 18%.

These partners supply contracts to hedge finished aluminum and inputs like alumina and natural gas, supporting cash flow—Century reported $160–$220 million EBITDA sensitivity reduction in 2023–24 from hedging programs.

- Hedging vs LME: reduced realized volatility to ±6%

- Input cost hedges: alumina, natural gas

- EBITDA sensitivity cut: ~$160–$220M (2023–24)

Century Aluminum partners lock feedstock, power, funding, logistics and price risk to 2025

Century Aluminum’s key partners—Glencore (alumina, ~70% supply), Santee Cooper/Landsvirkjun (power PPAs), US DOE (>$220M grants + $85M tax credits), shipping/rail (180 kt Iceland exports, +$150–$250/ton logistics), and banks/brokers (hedges cutting realized price volatility to ±6%)—stabilize feedstock, energy, financing, logistics, and price risk through 2025.

| Partner | 2024–25 KPI |

|---|---|

| Glencore | ~70% alumina |

| PPAs | Energy = 25–35% site COGS |

| DOE | $220M grants + $85M credits |

| Logistics | 180 kt; +$150–$250/ton |

| Hedging | Volatility ±6%; $160–$220M EBITDA benefit |

What is included in the product

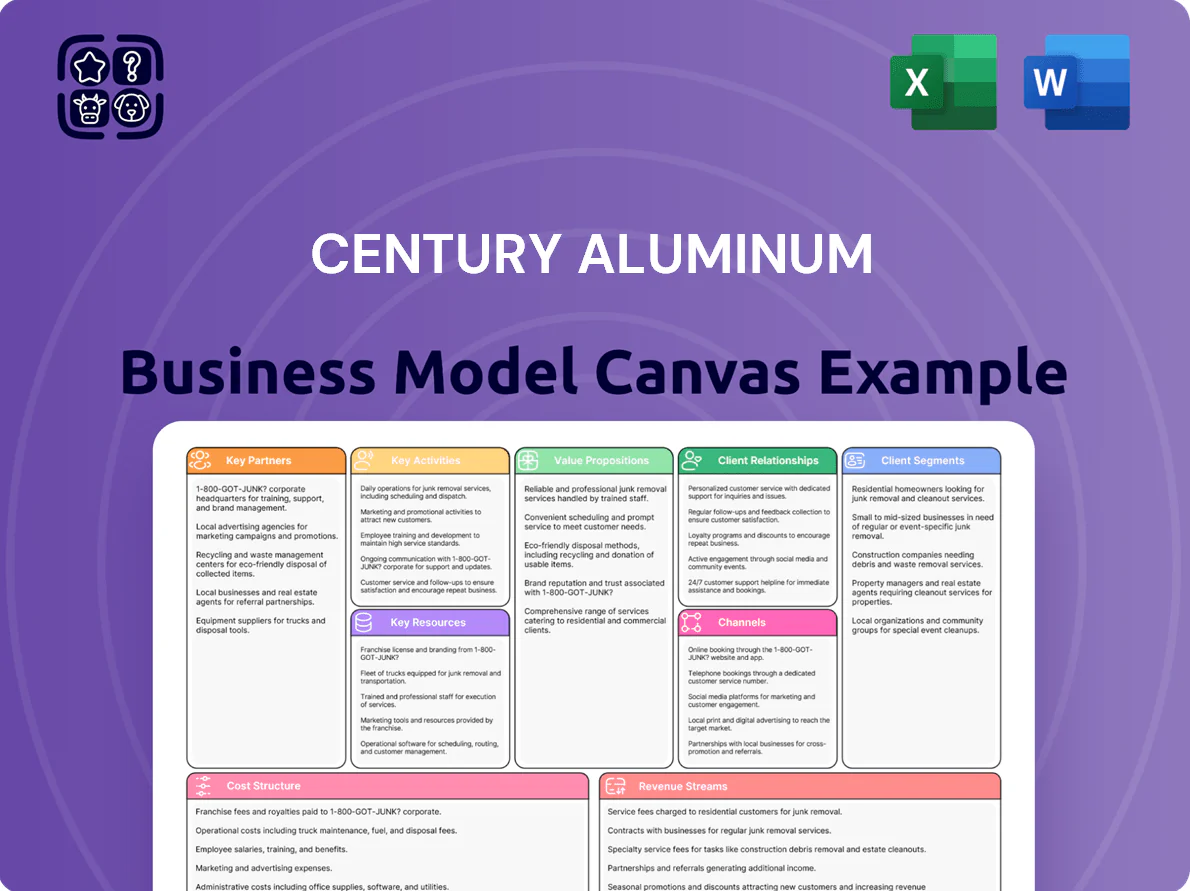

A concise Business Model Canvas for Century Aluminum detailing its nine-block structure—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—aligned to its alumina/aluminum production, smelting operations, and market-facing strategies.

High-level view of Century Aluminum’s business model with editable cells to quickly pinpoint revenue drivers, cost pressures, and downstream risks.

Activities

Primary Aluminum Smelting

The core activity is continuous electrolytic reduction of alumina into liquid aluminum in reduction cells; Century Aluminum ran ~1.1 million metric tons annual capacity in 2024 and must keep pots at ~950–980°C to avoid solidification and pot failure.

Management targets high amperage and cell efficiency—raising current efficiency by 1 percentage point can cut energy per ton by ~30–40 kWh; energy was ~13,500 kWh/ton industry-wide in 2024, so small gains materially lower costs.

Value-Added Product Casting

Century Aluminum casts molten aluminum into billets, slabs, and sow beyond standard ingots, targeting automotive and construction alloy specs to secure higher margins; cast-product sales contributed about 22% of 2024 revenues, lifting segment margins ~350 basis points versus standard ingots. Continuous capex in casting tech—roughly $45 million in 2024—keeps physical properties within evolving OEM tolerances and reduces scrap rates by ~18% year-over-year.

Energy Procurement and Management

Active daily management of Century Aluminum’s energy portfolio balances fixed-price contracts and spot exposure to control volatility; in 2024 power costs were ~35% of COGS at smelters, so hedging saved an estimated $45–60 million vs. full spot pricing. The company also monitors grid stability and joins demand-response programs, curtailing production for credits that trimmed annual energy spend by roughly $8–12 million in 2023–2024.

Research and Development for Green Aluminum

Century Aluminum dedicates ~15% of 2025 operating R&D spend to Natur-Al and low-carbon tech, piloting new inert anode chemistries and a 100 ktCO2/year carbon capture pilot to meet EU/US 2025 regs.

Work shifts to circularity: recycling trials aim to cut process emissions 25% and reduce energy intensity per tonne by 12% versus 2022 baseline.

- 15% of 2025 R&D budget

- 100 ktCO2/year pilot capture

- 25% emissions cut target

- 12% energy intensity reduction

Supply Chain and Inventory Optimization

- ERP visibility daily

- 200–300 days alumina cover (2024)

- 10–15% working-capital cut target

- Tariff/232 risks ±3–5% margin impact

High‑efficiency 1.1Mt smelter: 13,500 kWh/t, $45–60M hedging, 2025 low‑carbon push

Core activities: continuous electrolytic reduction (~1.1 Mtpa capacity in 2024) keeping pots at 950–980°C; high-amperage efficiency (1 ppt current-efficiency gain ≈30–40 kWh/ton saved; industry energy ≈13,500 kWh/ton in 2024); casting into billets/slabs (cast = ~22% revenue, +350 bp margins); energy hedging (power ≈35% of COGS, hedging saved $45–60M in 2024); 2025 R&D ~15% to inert anodes and 100 ktCO2/yr capture pilot; 200–300 days alumina cover (2024).

| Metric | Value (2024/2025) |

|---|---|

| Smelter capacity | ~1.1 Mtpa (2024) |

| Energy intensity | ~13,500 kWh/ton (2024) |

| Cast revenue | ~22% (2024) |

| Power share of COGS | ~35% (2024) |

| Hedging benefit | $45–60M (2024) |

| R&D to low-carbon | ~15% (2025) |

| CCS pilot | 100 ktCO2/yr (2025) |

| Alumina cover | 200–300 days (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the exact Century Aluminum Business Model Canvas you’ll receive—no mockup or sample—offering the same content, structure, and formatting shown here.

After purchase you’ll instantly download the complete file ready for editing, presenting, and sharing in the same professional layout displayed in this preview.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Century Aluminum Business Model Canvas: Downloadable Blueprint for Investors & Innovators

Unlock Century Aluminum’s strategic playbook with a concise Business Model Canvas that maps value propositions, revenue streams, key partners, and cost drivers—perfect for investors, consultants, and entrepreneurs seeking actionable industry insight; download the full Word/Excel canvas to benchmark, plan, and apply these proven strategies to your own projects.

Partnerships

Strategic Alumina Supply Agreements

Century Aluminum depends on long-term alumina supply contracts—notably with Glencore—to secure ~70% of its feedstock, cutting exposure to spot-price swings and keeping smelters near 85–90% capacity utilization. By 2025, amid geopolitical supply risks, these agreements underpin operational stability and helped limit input-cost spikes that pushed alumina index prices up ~30% YoY in 2024.

Energy Utility and Grid Providers

Century Aluminum relies on long-term power purchase agreements with utilities such as Santee Cooper (US) and Landsvirkjun (Iceland); these deals, often with renewable shares, lock in prices that drive regional margins—electricity can be >30% of smelter cash costs. In 2024 Century reported energy costs ~25–35% of site COGS and a 10–15% EBITDA swing per $10/MWh change in power price.

Department of Energy and Government Agencies

Logistics and Maritime Shipping Partners

Century Aluminum contracts global shipping lines and US rail carriers to move alumina inbound and finished aluminum outbound, cutting landed cost—Iceland plants shipped ~180 kt of primary aluminum to Europe in 2024, where logistics added an estimated $150–$250/ton to landed cost.

These partners handle bulk cross-border transit and deep-water port operations, reducing delays and demurrage that can swing margins by several dollars per ton.

- ~180 kt Iceland shipments (2024)

- Logistics adds ~$150–$250/ton

- Rail + ocean needed for inland US customers

Financial Institutions and Hedging Partners

Century Aluminum partners with major investment banks and commodity brokers to hedge LME (London Metal Exchange) price swings; in 2024 hedging activity helped limit realized aluminum price variance to ±6% versus spot volatility over 18%.

These partners supply contracts to hedge finished aluminum and inputs like alumina and natural gas, supporting cash flow—Century reported $160–$220 million EBITDA sensitivity reduction in 2023–24 from hedging programs.

- Hedging vs LME: reduced realized volatility to ±6%

- Input cost hedges: alumina, natural gas

- EBITDA sensitivity cut: ~$160–$220M (2023–24)

Century Aluminum partners lock feedstock, power, funding, logistics and price risk to 2025

Century Aluminum’s key partners—Glencore (alumina, ~70% supply), Santee Cooper/Landsvirkjun (power PPAs), US DOE (>$220M grants + $85M tax credits), shipping/rail (180 kt Iceland exports, +$150–$250/ton logistics), and banks/brokers (hedges cutting realized price volatility to ±6%)—stabilize feedstock, energy, financing, logistics, and price risk through 2025.

| Partner | 2024–25 KPI |

|---|---|

| Glencore | ~70% alumina |

| PPAs | Energy = 25–35% site COGS |

| DOE | $220M grants + $85M credits |

| Logistics | 180 kt; +$150–$250/ton |

| Hedging | Volatility ±6%; $160–$220M EBITDA benefit |

What is included in the product

A concise Business Model Canvas for Century Aluminum detailing its nine-block structure—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—aligned to its alumina/aluminum production, smelting operations, and market-facing strategies.

High-level view of Century Aluminum’s business model with editable cells to quickly pinpoint revenue drivers, cost pressures, and downstream risks.

Activities

Primary Aluminum Smelting

The core activity is continuous electrolytic reduction of alumina into liquid aluminum in reduction cells; Century Aluminum ran ~1.1 million metric tons annual capacity in 2024 and must keep pots at ~950–980°C to avoid solidification and pot failure.

Management targets high amperage and cell efficiency—raising current efficiency by 1 percentage point can cut energy per ton by ~30–40 kWh; energy was ~13,500 kWh/ton industry-wide in 2024, so small gains materially lower costs.

Value-Added Product Casting

Century Aluminum casts molten aluminum into billets, slabs, and sow beyond standard ingots, targeting automotive and construction alloy specs to secure higher margins; cast-product sales contributed about 22% of 2024 revenues, lifting segment margins ~350 basis points versus standard ingots. Continuous capex in casting tech—roughly $45 million in 2024—keeps physical properties within evolving OEM tolerances and reduces scrap rates by ~18% year-over-year.

Energy Procurement and Management

Active daily management of Century Aluminum’s energy portfolio balances fixed-price contracts and spot exposure to control volatility; in 2024 power costs were ~35% of COGS at smelters, so hedging saved an estimated $45–60 million vs. full spot pricing. The company also monitors grid stability and joins demand-response programs, curtailing production for credits that trimmed annual energy spend by roughly $8–12 million in 2023–2024.

Research and Development for Green Aluminum

Century Aluminum dedicates ~15% of 2025 operating R&D spend to Natur-Al and low-carbon tech, piloting new inert anode chemistries and a 100 ktCO2/year carbon capture pilot to meet EU/US 2025 regs.

Work shifts to circularity: recycling trials aim to cut process emissions 25% and reduce energy intensity per tonne by 12% versus 2022 baseline.

- 15% of 2025 R&D budget

- 100 ktCO2/year pilot capture

- 25% emissions cut target

- 12% energy intensity reduction

Supply Chain and Inventory Optimization

- ERP visibility daily

- 200–300 days alumina cover (2024)

- 10–15% working-capital cut target

- Tariff/232 risks ±3–5% margin impact

High‑efficiency 1.1Mt smelter: 13,500 kWh/t, $45–60M hedging, 2025 low‑carbon push

Core activities: continuous electrolytic reduction (~1.1 Mtpa capacity in 2024) keeping pots at 950–980°C; high-amperage efficiency (1 ppt current-efficiency gain ≈30–40 kWh/ton saved; industry energy ≈13,500 kWh/ton in 2024); casting into billets/slabs (cast = ~22% revenue, +350 bp margins); energy hedging (power ≈35% of COGS, hedging saved $45–60M in 2024); 2025 R&D ~15% to inert anodes and 100 ktCO2/yr capture pilot; 200–300 days alumina cover (2024).

| Metric | Value (2024/2025) |

|---|---|

| Smelter capacity | ~1.1 Mtpa (2024) |

| Energy intensity | ~13,500 kWh/ton (2024) |

| Cast revenue | ~22% (2024) |

| Power share of COGS | ~35% (2024) |

| Hedging benefit | $45–60M (2024) |

| R&D to low-carbon | ~15% (2025) |

| CCS pilot | 100 ktCO2/yr (2025) |

| Alumina cover | 200–300 days (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the exact Century Aluminum Business Model Canvas you’ll receive—no mockup or sample—offering the same content, structure, and formatting shown here.

After purchase you’ll instantly download the complete file ready for editing, presenting, and sharing in the same professional layout displayed in this preview.